Whitney Tilson’s email to investors discussing policing American tech giants; Stock Idea of the Day: Criteo SA (NASDAQ:CRTO); More from Scott Galloway, Tesla Inc (NASDAQ:TSLA)’s solar business.

1) News broke over the weekend related to the U.S. government taking a harder look at the tech giants, Amazon (AMZN), Facebook (FB), Alphabet (GOOGL), and Apple (AAPL). I continue to recommend the stocks of the first three, favoring Alphabet over Apple for reasons I outlined in my May 1 e-mail.

Q1 hedge fund letters, conference, scoops etc

But all shareholders need to carefully follow these investigations (and similar ones happening all over the world) and consider their implications. For now, I believe they are unlikely to derail the dominance of these companies, but I'm open to changing my mind if the facts change.

Personally, I think they should all be broken up, which would be good for society – and for shareholders. But barring a President Elizabeth Warren, this is extremely unlikely to happen...

Here are two front-page articles from today's Wall Street Journal and New York Times:

They all have dominant market shares in their sectors – from search to social media, e-commerce, online advertising and smartphone apps – and are protected by practices and conditions that make it hard for new rivals to challenge them.

The regulators' moves are small and preliminary, and could easily come to nothing. But if the agencies pursue cases, Google and Amazon will almost certainly face reams of bad publicity, rising consumer distrust and falling employee morale. An inquiry would remind everyone that Google, with its early motto of "Don't be evil," held itself to standards it sometimes could not match.

2) Today's Stock Idea of the Day is ad firm Criteo (CRTO), which is around $18 a share and is trading near its all-time low in the five-and-a-half years it's been public. It was recently written up on Value Investor's Club. (For those of you who are members, click here; for those who aren't, here are links to the 2016 long and 2017 short posts.)

For the many readers who are new to this list, my Stock Idea of the Day is not a recommendation – just something I've found that I think is interesting enough to be worth further investigation...

Here's my analyst, Steve Culbertson, on CRTO:

If you're anything like me, when you hear "online ads," you immediately think of tech behemoths Google, Facebook, and Amazon. So I was surprised to learn that this obscure company was a major player in this industry.

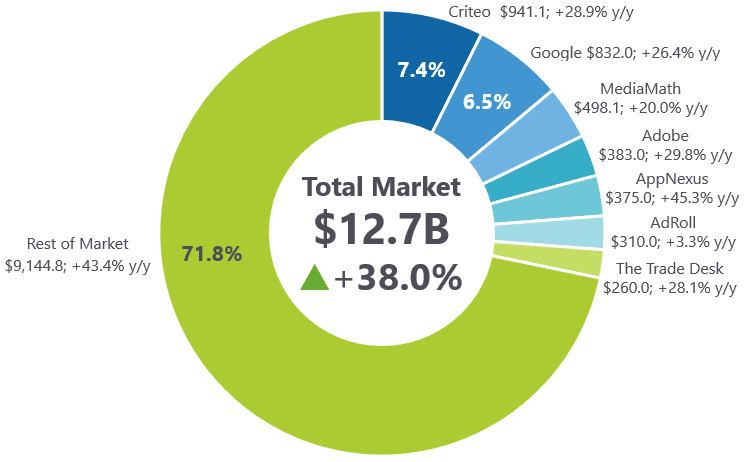

Criteo launched in France in 2005 and has grown into a global company with 2,700 employees in 31 offices serving nearly 20,000 clients. The company analyzes more than $800 billion of online sales transactions and serves more than 1 trillion online ads annually.

Criteo's business is in retargeting ads. Let me explain what that means...

Every day, millions of people browse many e-commerce sites. Some know exactly what they want and complete their purchases, while others don't and are essentially "window shopping."

Yet another group is undecided. They know what they're looking for but haven't committed. These shoppers might have several shopping carts with the same or similar products for later consideration. You can imagine how online retailers want them to follow through with a purchase. Criteo helps them by retargeting personalized ads toward these high-intent shoppers.

The company's software is embedded in thousands of retailers' websites. Each time someone visits a site, Criteo gathers small pieces of information and weaves them into an online profile that it can then use to target ads.

It's important to note that Criteo doesn't gather sensitive information, such as names or home addresses. Instead, it relies on analyzing data from more than 1.5 billion users to learn when and where to show the most appropriate ads.

Criteo boasts a 90% customer retention rate, which it claims is a result of its system beating the competition 90% of the time in head-to-head tests. Supporting this claim is that 73% of the company's revenues come from uncapped budgets. In other words, its customers entrust Criteo to deploy ad dollars on their behalf – a sure sign of how valuable its service is.

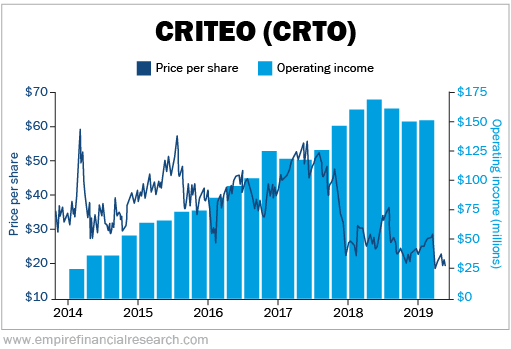

The stock went public in October 2013 and, as you can see in this chart, it's now close to an all-time low despite trailing 12-month operating income rising sixfold:

What explains the stock's weakness? It started in June 2017, when Apple rolled out its Intelligent Tracking Prevention ("ITP") policy. This effectively made it impossible for Criteo and other ad tech companies to track Safari users across different websites.

The stock took another dive in March after this Adweek article, Google Mulls Third-Party Ad-Targeting Restrictions, which speculated that Google would implement its own ITP into its market-leading Chrome browser.

The author of the VIC write-up argues that Google will not deploy ITP on its browser because it would be hurting its own ad business in the process. What's more, he thinks the company can return to a moderate rate of growth.

If he's right, there could be substantial upside, as the stock is trading at low trailing multiples of 0.5 times EV/revenue, 4.6 times EV/EBITDA, and 14 times P/E.

3) Following up on last Thursday's e-mail about Scott Galloway... If you don't have time to read his new book that I enjoyed so much, The Algebra of Happiness: Notes on the Pursuit of Success, Love, and Meaning, here are two interviews he did recently on YouTube and a podcast (I recommend listening to both at double speed).

Best regards,

Whitney

The Phony Case For Electric Cars

1) Here’s an article that I’m sure will get some hackles up (and how evil I am for even sending it out): The Phony Case For Electric Cars. Excerpt:

......

“Cities should offer up-front incentives to buy zero-emission cars, for instance, as well as non-financial benefits such as parking vouchers. Higher taxes on petrol and diesel cars — whether via congestion tolls or at the pump — will encourage drivers to switch and offset some of the costs of the transition,” the editorial board says.

................

The truth is that every city in America has made massive improvements in air quality over the past several decades — progress that was made without any help from electric buses, cars or taxis, and while “gas guzzlers” continued to dominate domestic car sales. Air quality in most places today is above, or well above, the government’s standards for safety.

2) A (surely even more evil!) friend shared these comments on it:

I agree 100% with this article, as it makes the point I have been trying to make for much of the last decade: In the U.S., cars have been getting cleaner every single year since at least 1973 or 1974. Despite many more cars, driven many more miles, air quality has therefore kept improving every single year for essentially 45 years in a row.

A brand new gasoline car -- or diesel, as they have the exact same pollution standard they need to meet in the U.S., since 2009 -- today emits so little that if it were deployed in certain (sub-sections of) metropolitan areas, it would actually clean the air: the air coming out of the tailpipe is cleaner than what’s being ingested through the car’s air filter.

But let’s look at what’s going on with the U.S. automotive fleet: We have approximately 253 million cars on the road in the U.S. New light vehicle sales in the U.S. has been around 17 million per year for the last couple of years, and the consensus estimates for 2019 are somewhere between 16.5 and 17.0 million.

That means that in a flat overall market, the fleet would “turn over” in 15 years (253 / 17). But what cars are actually turned over?

As a practical and statistical matter, the 17 million new cars sold into the U.S. market are replacing the oldest cars on the road. Those are the dirtiest ones. Most of the ones replaced are cars from the 1990s and 1980s -- and even 1970s, still on the road.

You know this because you can literally smell them, and sometimes even visibly see the pollution coming out of the tailpipe. You know it if you’re in New York City and one happens to be idling next to you in traffic.

But why do people keep driving around in those cars from the 1990s, 1980s, and even the 1970s? The answer is, mostly, cost.

It’s simply too expensive to buy a new car. While you can pick up a decent new car for around $15,000 after the most extreme dealer discounts in the market today, let’s call $20,000 a more universal number for a broader range of body styles and sizes. Everyone in the U.S. can get into a very decent car for somewhere in the $15,000 to $20,000 today.

The problem is that only a decade ago, that number was closer to $10,000 -- not $15,000 to $20,000. And not long before then, it was $8,000 or somewhere around there.

New cars have simply become less affordable. As a consequence, people keep the oldest cars, that pollute way over 100 times more than a new car. In some cases even 1,000 or 10,000 times more.

What’s driving those increasing costs for new cars? Ironically, pollution controls. They are expensive, costing several thousand dollars more per car. Plus, another thing that I will get into in a moment.

I am going to use a few conveniently “round” numbers and decimal points here, but they are necessary to prove a point. Let’s say that it it costs $1,000 per car to reduce pollution by 99.999%. Then, to get to a 99.9999% reduction, it would have to cost $5,000 per car -- and incremental $4,000 for that extra decimal point.

How many people could buy a new car for $12,000 net vs those who would replace their old car if the new car was $16,000? The answer: A lot more people buy a new car if it’s $12,000 vs when it would be $16,000.

The difference is that the $12,000 car reduces pollution (compared to the 1997 Ford Taurus they’re trading in) by 99.999%, but the otherwise identical car, priced at $16,000, reduces it by $99.9999%.

If the environmental goal is to reduce total pollution, you will want more people replacing their old cars -- even if it’s only a 99.999% reduction instead of 99.9999%.

Stated differently: If you make new car pollution controls expensive, then people keep their old cars around, and you end up with more pollution -- not less.

That’s why it would actually be a hugely positive thing for the environment to avoid tightening pollution standards going forward. Freeze them at the current level instead. That would avoid that $16,000 car today to bump up its price to $20,000 or more in the next couple of years. Because that’s what is about to happen if current U.S. Federal and state policies don’t change.

Back to that other thing that is also driving up cost of a basic gasoline car: Paying for electric car subsidies. In California and a few other states, the states have set quotas for electric car sales. Seeing as those quotas are higher than the free-market demand, the automakers are effectively forced to sell them below cost. That’s why you see such cheap EV car leases in states such as California, for example.

So, automakers are having to internally subsidize EV car sales -- mostly far more expensive cars than those who are used to replace 20+ year old pollution stinkers. A new EV is far more likely to replace a 3 year old BMW 3-series or Mercedes C300 that’s come off a lease. Actually, the most common trade-in for an EV is a Toyota Prius. In other words, that new subsidized EV is not replacing an old stinker -- it’s replacing the next-cleanest car on the road.

All of those internal automaker subsidies come from somewhere. The automakers are not just going to eat those losses. Those subsidies simply get added to the price of a “regular” basic gasoline or diesel car. That means that $16,000 car is now $17,000 or $18,000, all other things equal. And that means that some guy in South Dakota or Florida who thought he was going to replace his 1995 Toyota Corolla with a new 2019 Toyota Corolla hybrid, can’t afford to do it. He can’t both afford to subsidize a Silicon Valley billionaire buying his fifth Tesla (which replaced his fourth Tesla), and also buy his own replacement for his 1995 Toyota Corolla. So he’s left with driving his old car, which would pollute 1,000 or 10,000 times more than a 2019 Corolla hybrid.

Increasing pollution controls on a new car today is simply self-defeating: If you increase them too much, then fewer and fewer people can afford buying a new car to replace the oldest cars on the road today. The only sensible solution is to freeze pollution standards at today’s already most stringent level, and to cease forcing the automakers add to the price of their cheapest cars for the purpose of internally subsidizing more expensive electric cars.

That’s how you maximize clean air, while still not shrinking the overall size of the automotive fleet.

An incredible story from a former SolarCity employee

It would be hard to find a better example of one of the major reasons why I run this Tesla email list: the incredible information, analysis and insights I get from people on it.

Here’s an email I received recently from someone I’d never heard from before (shared with permission – and a few tweaks to maintain his anonymity). While some parts of his story are well known, overall he paints a detailed and damning picture of Musk’s delusion and deception that I’ve never seen before, at least to this degree:

I worked for SolarCity/Tesla for a number of years in solar system sales. I left the company late last year because of the drastic changes Tesla made to the solar business. As publicly disclosed, this included eliminating all direct sales channels, which reduced the sales force from 4,000 salespeople to only about 60 inside sales reps in a Las Vegas call center to service the entire country. Musk also conducted an experiment by tasking the vehicle reps in Tesla stores to sell both cars and solar systems but that didn’t work (of course this move was moot after many stores were closed a few months later). Finally, Musk hired a new executive from Amazon who had no experience in the solar industry to run the energy business right before I left.

The latest rumored strategy I’ve heard to reignite the solar business is that Tesla will somehow be introducing a solar panel that is priced at about 50% per watt below the rest of the market. I can’t imagine how that is possible. I suspect it’s just more reality-distortion pandering to the existing employee base to keep them engaged.

When Tesla acquired SolarCity, the company had about a 42% market share of the residential solar market. I suspect that share has now dwindled to low single digits. At its peak, the solar business was about $750 million in annual revenue; I suspect it’s now less than $200 million, if that.

Contrast this reality with Musk’s multiple public statements to employees and investors that he expected Tesla’s “solar business” to be bigger than the car business in 10 years. I couldn’t believe what I was hearing. At that time, the solar business had already been severely cut back and the car business was on pace to reach a $20 billion revenue annual run rate. Thus, for the solar business to have even a remote chance of catching the car business, the car business would have to contract and the solar business would have to miraculously reverse its severe revenue decline and grow 1,000% per year. This struck me as vintage Steve Jobs-like reality distortion.

The new sales strategy is to mainly focus on cross-selling solar systems to Tesla owners who own homes. This certainly makes sense, but severely limits the addressable market and cedes the lion’s share of the market to others. When I left, Solar Roof installations were a nothing burger. As far as I could tell, there were maybe 20 installed, many of which had been installed on current and former Tesla executive’s homes.

By the way, coverage of Tesla’s solar business often erroneously makes it sound like Tesla manufactures its own solar panels. It is public information that all the panels Tesla installed are mostly made by Panasonic, plus panels from a few other manufactures from time to time. The inverters are provided mainly by SolarEdge, Delta and ABB. Powerwall is of course made by Tesla.

In a follow-up email, he continued:

My information is a little dated, so things could have changed. But everything I shared is fact based, true and based on conversations with former employees who worked there for a few months after I left. You can look up the name of the executive hired from Amazon in Tesla press releases. I think he was hired around June 2018.

I don’t know if the low-cost solar panels ever materialized, but I suspect that was wishful thinking or the former employee who told me about it got his story wrong. That said, if you go back and look at the investor presentation that justified the acquisition of SolarCity I’m sure you will see that Tesla overpromised and underdelivered. They did promise investors $155 million in savings (synergy) by eliminating “duplicative sales channels” and SG&A. They certainly delivered on that promise.

The part about Musk going on record that the solar business would eventually surpass the car business is absolutely true. I personally heard him say that multiple times.

I’m not sure how relevant any of this is to bolstering the case for shorting Tesla since the solar business is such a small part of Tesla and contributes a relatively small amount of revenue and profit (if any). In addition, many of us believed the real impetus for the acquisition was for Elon to save his own wealth and that of the other two co-founders who were Musk’s first cousins – Lyndon Rive (CEO) and Peter Rive (CTO). You may know that Musk himself was SolarCity’s largest shareholder with 23% of the stock. In addition, Tesla as I recall had purchased more than $100 million in SolarCity bonds over the years. SolarCity was on track to lose a billion dollars and probably would have gone bankrupt or been sold at a huge discount had Tesla not come to the rescue.

[I just did some reading to refresh my memory on the SolarCity acquisition. Tesla announced it on June 21, 2016, when its stock closed at $219.61, valuing SC at $2.6 billion. Its stock dropped 10.5% the next day to close at $196.66, so the market correctly viewed this as a bad deal for Tesla, I suspect mainly because Tesla roughly doubled its debt load by taking on $2.93 billion of SC’s net debt. By the time the deal closed on Nov. 21, 2016, the stock was at $184.52, which means that, at least according to one article I read, Tesla issued $2.04 billion in stock for the deal. I’m not sure which number is right.Here is Tesla’s lengthy blog post on Nov. 1, 2016 defending the deal: https://www.tesla.com/blog/tesla-and-solarcity. In it is this doozy: “The transaction is expected to be additive to Tesla’s cash balance. SolarCity increased its cash from Q2 to Q3 2016 and expects to increase it further in Q4 2016. We expect SolarCity to add more than half a billion dollars in cash to Tesla’s balance sheet over the next 3 years.”]