Warren Buffett said that The Intelligent Investor is the best book ever written on investing. This book contains over 600 pages of wisdom. The wisdom that serves as the building blocks for all value investors.

This is The Intelligent Investor Summary. Enjoy!

Q3 hedge fund letters, conference, scoops etc

Warren Buffett Preface to The Intelligent Investor Book (Fourth Edition)

The intelligent investor by Benjamin Graham is such a great book that even Warren Buffett himself wrote a preface for it. Warren said that he first read the first edition of the book in 1950. He was only nineteen years old at the time. He thought then, and still is now, that The Intelligent Investor is by far the best book about investing.

Warren said that to invest successfully over a lifetime does not require a stratospheric IQ, unusual business insights, or inside information. We only need a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework. And The Intelligent Investor book precisely and clearly prescribes the proper framework. But Warren said that it is still us that must supply the emotional discipline.

Warren specifically pointed out chapter 8 (Mr. Market) and 20 (Margin of Safety) as the main two chapters that contain invaluable advice. He said that if we pay special attention to those 2 chapters, we will not get a poor result from our investments.

But as to whether we achieve outstanding results, it would depend on the effort and intellect we apply to our investments, as well as the amplitudes of stock market folly that prevail during our investing career. The sillier the behavior of the market, the greater the opportunity for businesslike investor. If we follow Graham, we will profit from folly rather than participate in it.

Setting Your Expectations Right:

on What You Can Expect Out of The Intelligent Investor Book

It is important to note that The Intelligent Investor book will not talk a lot about the technique of analyzing securities. More attention will be paid to investment principles and investor’s attitudes. Benjamin Graham also said that this book would not teach us how to beat the market. No truthful book can.

You can expect The Intelligent Investor Book to teach us 3 powerful lessons:

[1] How we can minimize the odds of suffering irreversible losses, [2] how we can maximize the chances of achieving sustainable gains and [3] how we can control self-defeating behavior that keeps most investors from reaching their full potential.on My Intelligent Investor Summary:

As much as I try my best to write the best Intelligent Investor summary ever, it will not be perfect. There will be some inaccuracy and misinterpretation. But I hope that you will find this of value. I will do my best to summarize the wisdom of Benjamin Graham with the valuable commentary by Jason Zweig.

To sum up 600 over pages of wisdom in such a classic value investing book is no easy task. I start out this task by first not taking it lightly. And second, looking at it from the point of view as a reader. What do I want to see in a great The Intelligent Investor book summary? I pondered for a while. And the answer is clear. I would want something that I can look at as a refreshment on a consistent basis. During a market crash. During market euphoria. Because for me, I plan to refer back to this page often to revise the classic lessons that the father of value investing, Benjamin Graham has imparted to us through his book. And the well-written commentary by Jason Zweig.

What does Graham meant by an “intelligent” investor?

Patience, Disciplined, Eager to Learn, Harness our Emotions and Think for Ourselves

He made it clear back in the first edition of the book that It simply means being patient, disciplined, and eager to learn; we must also be able to harness our emotions and think for ourselves. This kind of intelligence, explains Graham, “is a trait more of the character than of the brain.”

Do You Have High IQ? Not Enough

There is evidence that high IQ and education are not enough to make an investor intelligent. In 1998, Long-Term Capital Management L.P., a hedge fund run by a battalion of mathematicians, computer scientists, and two Nobel Prize-winning economists, lost more than $2 billion in a matter of weeks on a huge bet that the bond market would return to “normal.” But the bond market kept right on becoming more and more abnormal—and LTCM had borrowed so much money hat its collapse nearly capsized the global financial system.

Most of the time, people who failed in investing is not because they are stupid. It’s because they have not developed the emotional discipline that successful investing requires.

Graham always says that “while enthusiasm may be necessary for great accomplishments elsewhere, on Wall Street it almost invariably leads to disaster.” History tells us that people who got carried away on internet stocks, on big “growth” stocks let other investors’ judgments determine their own. They ignored Graham warning that “the really dreadful losses” always occur after “the buyer forgot to ask ‘How much?’ ” The investor’s chief problem and even his worst enemy is likely to be himself.

The Difference Between Investment & Speculation – Chapter 1

Investment and speculation are different

It is not an unethical thing to speculate. What is important is that we keep the activities of investing and speculation totally separate. It is dangerous to think that we are investing when we are actually speculating. Graham advises us to limit our allocation to our speculation position (also known as “mad money account”) to no more than 10% of the investment funds. Never mingle the money in our speculative account with what is in our investment accounts. Do not allow our speculative thinking to spill over into our investing activities.

We have to know the difference between investing and speculation. Investing is an operation which, upon thorough analysis promises safety of principal and an adequate return. Operations not meeting these requirements are speculations.

The intelligent investor never dumps a stock purely because its share price has fallen. The intelligent investor will always ask first whether the value of the company’s underlying businesses has changed. As Graham never stops reminding us, stocks do well or poorly in the future because the businesses behind them do well or poorly – nothing more, and nothing less.

Inflation (What We Can Do to Help Us Beat Inflation) – Chapter 2

“Americans are getting stronger. Twenty years ago, it took two people to carry ten dollars’ worth of groceries. Today, a five-year-old can do it” – Henry Youngman

Inflation is real and it erodes our purchasing power over time

A dollar 10 years ago is worth more as compared to A dollar today. What this means is that cash is a terrible investment. We need to make use of the cash. To get more cash. To beat inflation.

Investors often overlooked the importance of understanding inflation. Psychologists called this the “money illusion”. For example, if we receive 2% raise in salary in a year when inflation runs at 4%, we will most certainly feel better than if we take a 2% pay cut during a year when inflation is zero. Yet both changes in the 2 scenarios leaves us in a virtually identical position: Which is 2% worse after inflation.

How can the intelligent investor guard against inflation?

- Invest in stocks

A standard answer would be to “buy stocks”. But as common answers so often are, it is not entirely true. From 1926 through 2002, when the prices of consumer goods and services fell, stock returns were terrible too. When inflation shot up above 6%, stocks also tanked. The stock market lost money in 8 of the 14 years in which inflation exceeded 6%.

A mild amount of inflation allows companies to pass increased cost of raw goods to consumers. But high inflation forces consumers to stop purchasing. And this results in bad business results and therefore bad stock market returns.

- Invest in REITs (Real Estate Investment Trusts)

REITs are companies that own and collect rents from buildings. There are many types of REITs. Such as commercial and residential properties REITs. These companies do a decent job of combating inflation.

My note: So Graham says that stocks might not be a good investment when inflation runs high. But historically, stocks is definitely still a good investment for those who know what they are doing. And to combat inflation, Graham suggests us to invest in REITs. Which essentially are also stocks.

The Stock Market (A Century of History) – Chapter 3

The most important thing that we can learn so far from one hundred years of stock market history is that the intelligent investor must never forecast the future of the stock market simply by extrapolating based on the past. The stock market will not go up indefinitely. We have to always be careful and keep in mind that when stock prices rise, it becomes riskier, not less.

Benjamin Graham asks 3 simple questions:

- Why should the future returns of stocks always be the same as their past returns?

- If every investor comes to believe that stocks are guaranteed to make money in the long run, won’t the market end up being wildly overpriced?

- And once that happens, how can future returns possibly be high?

Should We Be a Passive/Defensive Investor or Active/Enterprising Investor – Chapter 4, 5, 6, 7, 14 & 15

To Be Passive or Active Investor? Not Only Depending on the Degree of Risk You can Take

It is a common belief that those who cannot take risks should be contented with a relatively low return on their invested funds. Hence, it is also the common belief that the rate of return which an investor should aim for is more or less proportionate to the degree of risk he or she is ready to go for.

But The Intelligent Investor has a different view.

To Be Passive or Active Investor? Also Depends on the Amount of Effort You Are Willing to Put In!

Graham says that the rate of return an investor should expect to receive is according to the amount of intelligent effort the investor is willing and able to bring to bear on his or her task. The minimum return is to the passive or defensive investor who wants both safety and freedom. The maximum return would be to the active or enterprising investor who exercises maximum intelligence and skill.

Here’s why age should not determine the amount of risk we can take:

- For example, an 89-year-old with $3 million, an ample pension, and a gaggle of grandchildren would be foolish to move most of her money into bonds. She already has plenty of income, and her grandchildren (who will eventually inherit her stocks) have decades of investing ahead of them.

- On the other hand, a 25-year-old who is saving for his wedding and a house down payment would be out of his mind to put all his money in stocks.

To determine the amount of risk you can take, ask yourself:

- Are you single or married? What does your spouse or partner do for a living?

- Do you or will you have children? When will the tuition bills hit home?

- Will you inherit money, or will you end up financially responsible for aging, ailing parents?

- What factors might hurt your career? (If you work for a bank or a homebuilder, a jump in interest rates could put you out of a job. If you work for a chemical manufacturer, soaring oil prices could be bad news.)

- If you are self-employed, how long do businesses similar to yours tend to survive?

- Do you need your investments to supplement your cash income? (In general, bonds will; stocks won’t.)

- Given your salary and your spending needs, how much money can you afford to lose on your investments?

If after considering all these factors and we feel that we can take a higher risk, we can own more stocks and be an enterprising investor. If not, we should be a defensive investor.

My note: Take a deep look into yourself. Reflect well. And analyze if you are currently more suitable to be a defensive or enterprising investor.

For the defensive investor – high-grade bonds and common stocks

The defensive investor should divide his funds between high-grade bonds and high-grade common stocks. A fundamental guiding rule is that the investor should never have less than 25% or more than 75% of his funds in common stocks. The standard division should be equal ones of 50-50 between stock and bonds. A sound reason to increase the percentage in common stocks is when there are more stocks in a bear market at a bargain price. Conversely, they should reduce common stock component to below 50% when the market level has become dangerously high.

Stock selection for the defensive investors:

- Adequate size of the enterprise

Graham idea is to exclude small companies that are more volatile.

- A sufficiently strong financial condition

Current assets should be at least twice of current liabilities for industrial firms. Long-term debt should not be more than net current assets. For public utilities, the debt should not exceed twice the equity.

- Earnings stability

Positive earnings for each of past 10 years.

- Dividend record

Uninterrupted for past 20 years.

- Earnings growth

A minimum increase of at least one-third in per-share earnings in the past ten years using three-year averages at the beginning and end.

- Moderate price to earnings ratio

No more than 15 times average earnings of the past 3 years.

- A moderate ratio of price to assets

Should not be more than 1.5 times the book value last reported. However, a low pe ratio below 15 can justify a higher price to book value. PE ratio x PB ratio should not be more than 22.5.

Graham has 4 rules for the portfolio of the defensive investors:

- It should contain a minimum of 10 stocks and a maximum of 30

- Each company should be large, prominent and conservatively financed.

- Each company should have a long record of continuous dividend payments.

- The defensive investors should impose some limit on the price they will pay for the company over its average earnings of 7 years. Not more than 25 times the average. And not more than 20 times of the earnings of the last 12 months.

Rule no 4 above would exclude almost the entire category of “growth stocks.” Graham excludes “growth stocks” because he regards them as too uncertain and risky a vehicle for the defensive investor.

Graham says that if the list of stocks for the defensive investor has been competently selected in the first place, there should be no need for frequent or numerous changes. It is important for defensive investors to note that they should not have the belief that they can pick stocks without doing any homework. It is crucial that they do their research beforehand.

Image source: TheStreet.com

Stock selection for the enterprising investor:

- Financial condition: [1] Current assets at least 1.5 times current liabilities, and [2] debt not more than 110% of net current assets (for industrial companies).

- Earnings stability: no deficit in the last five years.

- Dividend records: Some current dividend.

- Earnings growth: Last year’s earnings more than those of 1966.

- Price: Less than 120% net tangible assets.

It is important to note that many of the best professional investors first get interested in a company when its share price goes down, not up. Looking at the daily list of the new 52-week lows can be 1 way to get started. We can also use websites that are able to screen stocks with the statistical figure suggested by Graham.

My note: We need to think in today’s context too with the above stock selection policy for enterprising investor. Especially number 4 on the criteria of earnings being more than those in 1966. We can probably adjust it to earnings being more than the average of 3 or 5 years ago. In chapter 11 below, we will go more in detail on how Graham analyzes stocks.

Zieg says that Warren looks for “franchise” companies with strong consumer brands

As well as easily understandable businesses, robust financial health, a near monopoly in their markets. Buffett likes to snap up a stock when a scandal happens. Like when he bought Coca-Cola as soon as the disastrous rollout of “New-Coke.” and market crash of 1987. Warren also looks for managers who set and meet realistic goals; build their businesses from within rather than through acquisition. Allocate capital wisely. And do not overpay themselves in stock options. Insists on steady and sustainable growth in earnings.

Portfolio policy for the enterprising investor:

- Buying in low markets and selling in high markets

Enter the market during depression period and sell out in the advanced stages of a boom.

- Buying carefully chosen “growth stocks”

A growth stock may be defined as one that has done better than the average over the past and is expected to do so in the future.

This is harder than it looks. It merely takes a screening to know which stocks have “out-performed the averages” in the past.

Two key problems with buying growth stocks: [1] Stocks with good records and seemingly good prospects usually are selling at a high price. The investor might be right in his judgment of the prospects but because he has paid in full or overpaid, the investment will still not do well. [2] The investor judgment of the future may be wrong. Unusually rapid growth cannot keep up forever. The increase in size makes the repeat of its past achievement more difficult. At a point, the growth curve will flatten and often, it turns downward.

- Buying bargain issues of various types

Usually created by [1] currently disappointing results and [2] protracted neglect of unpopularity.

Bargain issues are one which on the basis of facts established by analysis, it appears to be worth considerably more than it is selling for. The issues are not a true “bargain” unless the value is at least 50% more than the price.

Two tests: [1] Estimate future earnings and then multiplying them by a factor appropriate to the particular issue. If the resultant value is at least 50% above the current market price – and if the investor is confident of the valuation method used – he can tag the stock as a bargain. [2] Value the business from the view of a private owner. Similar to the first method but more focus on the realizable assets values, with emphasis on net current assets or working capital.

- Buying into “special situations”

For example, buying potential acquisitions target (usually smaller companies)

Undervalued bonds are another example

- Buying relatively unpopular large company

While smaller growth companies can be trading at an extremely high multiple, large companies may be trading at a super low multiple due to the current unpopularity

Advantages of large companies are that they are more stable.

In order for the enterprising investor to obtain better than average results over the long run, the policy of selection of stocks should:

- Meet the objective or rational tests of underlying soundness

- Must be different from the policy followed by most investors or speculators

For the enterprising investor, Graham lists out the “don’ts”:

- High yield or “second-grade” or junk bonds – too costly and troublesome to diversify away from the risk of default

- Foreign bonds

- Day trading – Graham believes that day trading stocks few hours at a time is one of the best weapons for financial suicide. Some of your trades will make money, most will lose money. Your brokers always win.

- Initial public offerings – For every successful IPOs like Microsoft, there are thousands of more loss-making ones.

Graham says that what we do not do is as important as what we do.

“It requires a great deal of boldness and a great deal of caution to make a great fortune; and when you have got it, it requires ten times as much wit to keep it.”- Nathan Mayer Rothschild

My note: How true the above quote is! What we do not do is as important as to what we do. That is why I have never done any of the 4 above “don’ts” by Graham. Look at the recent 2018 IPO flop like Snapchat and Spotify!

Should you go for 100% stocks portfolio?

Graham says that a 100% stock portfolio may make sense only for a tiny minority of investors. These are the investors that:

- Have set aside enough cash to support your family for at least one year

- Will be investing steadily for at least 20 years to come

- Survived the bear market that began in 2000 (or in my opinion, any other bear market)

- Did not sell stocks during the bear market that began in 2000 (or in my opinion, any other bear market)

- Bought more stocks during the bear market that began in 2000 (or in my opinion, any other bear market)

- Have read Chapter 8 in this book and implemented a formal plan to control your own investing behavior.

Unless we can honestly say yes to all the above questions, Graham says we should not put all of our money in stocks. Graham says that anyone who panicked in the last bear market is going to panic in the next one – and will regret having no cash or bonds with them. Hence, Graham says that investing is more of a trait of character than IQ.

Stock Market Volatility (Mr. Market Concept) – Chapter 8

Graham says that the true investor scarcely ever is forced to sell his shares. The intelligent investor only pays attention to the current stock price when it suits him. The investor who permits himself to be worried by unjustified market declines in his holdings is essentially transforming his basic advantage into a basic disadvantage.

Mr. Market Parable

Imagine that we own small shares in a private business that costs us $1,000. One of our partners is called Mr. Market. Mr. Market is a very obliging partner. Every day, he tells us what he thinks our interest is worth and furthermore, offers either to buy us our or to sell us an additional interest on that basis. Sometimes his idea of value appears justified and plausible by business developments and prospects as we know them. Often, on the other hand, Mr. Market lets his enthusiasm or his fears run away with him, and the value he proposes seems to you a little short of silly.

If we are a prudent investor or a sensible businessman, will we let Mr. Market’s daily communication determine our view of the value of a $1000 interest in the enterprise? Only when we agree with him, or we want to trade with him. We may happy to sell out to him when he quotes a ridiculously high price, and equally happy to buy from him when his price is low. But the rest of the time, we would be wiser to form our own views of the value of our holdings, based on full reports from the enterprise about its operations as well as its financial positions.

The speculator’s main interest is to anticipate and profit from fluctuations in the market. The investor’s primary interest is to acquire and hold suitable securities at suitable prices. Investing is not about beating others at their game, it’s about controlling yourself at your own game. Most investors fail because they pay too much attention to what the stock market is doing currently.

Investing in Funds & Its Advisors – Chapter 9 & 10

Image source: Cartoon Stock

Investing in investment funds is more suitable for the defensive investor

A well-picked one provides a good solution for preventing the investor from making terrible mistakes. They should be wary of high fees, excessive trading and erratic fluctuations in performance. Checking at least the last 5 years performance of the fund is crucial.

Financial scholars have been studying mutual-fund performance for at least 50 years:

- The average fund does not pick stocks well enough to overcome its costs of researching and trading them

- The higher a fund’s expenses, the lower its returns

- The more frequently a fund trades its stocks, the less it tends to earn

- Highly volatile funds, which bounce up and down more than average, are likely to stay volatile

- Funds with high past returns are unlikely to remain winners for long.

Ultimately you have to know yourself well. Many investors are more comfortable having a second opinion from a good financial adviser. Some people need others to show them what rate of return they need to earn on their investments. Or how much they should be saving to meet their financial goals. Some others may simply need someone to blame when their investments go down, instead of beating themselves up. This might give these people some boost needed to keep investing steadily over the long run instead of giving up completely during a bear market.

Graham says you might need help on your investments if:

- You have suffered a big loss of more than 40% for your portfolio

He gave an example of the time period from beginning 2000 to end of 200.

- Busted budgets

You struggle to make end meets. Do not know where your money go. Impossible to save regularly. Always fail to pay your bills on time. Simply put, your finances are out of control.

- Chaotic portfolio

A professional “asset-allocation” can help.

- Major changes

If you have become self-employed and need to set up a retirement plan. Or your aging parents do not have their finances in order. Or college for your kids looks unaffordable. A genuine financial adviser might help to improve the quality of your life.

Trust, then verify

A lot of financial advisers are con artists who make you trust them. And talk you out of investigating them. Before you put your financial future with them, it is important to find someone honest. Ronald Reagan used to say, “trust, then verify”. Always do your due diligence. And make sure that your adviser truly knows his stuff, about the true fundamentals of investing. And a satisfactory amount of years with skin in the game.

Beware of financial advisers who use these words

- The opportunity of a lifetime

- Don’t you want to be rich?

- You should focus on performance, not fees

- Can’t lose

- The upside is huge

- No one else knows how to do this

- It’s no-brainer

- The smart money is buying it

- It’s a sure thing

My note: There are many financial advisors who are unethical in Singapore. There are some who are genuine and good. Those who have skin in the game and really is genuine in looking out for you is the one to go for. It is hard to find because their pay is ties to them selling policies to you. Take your time. Do not trust easily. Verify!

Investment Selection (How to Analyze Stocks and Bonds) – Chapter 11

When analyzing bonds

The most important criteria to take note of is the number of times that total interest charges have been covered by available earnings. We should analyze for at least 7 years in the past.

For preferred stocks

It is the number of times the bond interest and preferred dividends combined have been covered by the available earnings for 7 years in the past.

For stocks

We have to compare our valuations of the company to the current price that the company is trading at in the stock market. We should always seek a margin of safety – purchasing the stock for less than its intrinsic value. The lesser the assumptions we have to make about the future during analysis, the lesser the possibility for error is. So we should not make too many assumptions when doing our analysis of stocks.

The biggest source of value for stocks should be the average of the future potential earnings. And we have to also take into account the required rate of return too. Depending on the quality of investment, the required rate of return will differ.

Five elements to determine how much the enterprising investor should pay for a stock:

1. Long-term prospects of the company

Download at least five years’ worth of annual reports (10K) from the company’s website. Gather evidence in the financial statements that answer two questions: What makes this company grow? Where do (and where will) its profits come from?

Beware of companies that are:

a. a serial acquirer

Companies that average more than 2 or 3 acquisitions a year are a sign of trouble. If a company would rather buy stock of other companies than themselves, that is a hint that we as an investor should too. Check their track records as an acquirer. Watch out for firms that took on acquisitions only to write it down in the future proving they had overpaid for the past acquisitions. Bad omen for future decision making.

b. OPM addict

A company that likes to borrow debt or sell stock to get other people’s money are dangerous. OPM are labeled as “cash from financing activities” of the statement of cash flows in the annual report. They can make a sick company looks to br growing even if the underlying business is not generating enough cash.

c. Johhny-One-Note

A company that relies on one customer (or a handful) for most of its revenues.

Look for companies that:

a. Has a wide “moat” or competitive advantage

Some companies can be easily stormed while others are impregnable. Several forces that can widen a company’s moat include a strong brand identity (like Harley Davidson), a monopoly or near monopoly, economies of scale, low-cost (Gilette that can produce blades by the billion), unique intangible asset (Coca-cola), a resistance to substitution (most businesses have no alternative to electricity so utility companies are an example of one).

b. The company runs a marathon, not sprint

The fastest growing companies tend to overheat and dies out. Look for companies that have grown smoothly and steadily over the past 10 years. A sudden 1 or 2 year burst is hardly sustainable.

c. The company sows and reaps

All companies must spend some money on research and development. R&D may not be a source of growth today. But it will be tomorrow. A company that spends too little on R&D is as vulnerable as one that spends too much.

2. Management competency

Fair to assume that outstandingly successful company has unusually good management. Look for management that says what they will do, and do what they said. A good manager will admit failures and take responsibility for them.

Good management will not overpay their CEO. They will spend more time managing the company in private instead of promoting it to the investing public. Also, ask whether their accounting practices are designed to make their financial results transparent or opaque. If “nonrecurring” charges keep on recurring or “extraordinary” items crop up so often they seemed ordinary, EBITDA takes priority over net income, this is a company that does not put shareholders interest first.

3. Financial strength & capital structure

A good business generates more cash that it consumes. See in the statement of cash flows whether cash from operations has grown steadily over the past 10 years.

Look at Warren Buffett popularized the concept of owner earnings which is net income plus amortization and depreciation, minus normal capital expenditures. Subtract from the net income any “unusual”, “nonrecurring” or “extraordinary” charges. Also minus any costs of granting stock options that diluted earnings away from existing shareholders into the hands of new inside owners. As well as any “income” from the company’s pension fund. Look for a company that has owner earning per share that has grown steadily by at least 7% over the past 10 years.

In the company’s capital structure, the debt should be under 50% of total capital. In the footnotes to the financial statements, determine whether long-term debt is a fixed rate (with constant interest payments) or variable (with payments that fluctuate, which could become costly if interest rates rise). Look out also for the ratio of earnings to fixed charges.

4. Dividend record

One of the most persuasive tests of high-quality companies is an uninterrupted record of dividend payments going back over many years. Graham suggests 20 years. He also said that the defensive investor might be justified in limiting his purchases to those that met this test.

5. Current dividend rate

My note: I think the above 5 points are really good starting criteria for analyzing companies – for the enterprising investor.

Graham advises a Two-Part Appraisal Process for Stocks

The analyst should first work out the “past-performance value.” This should be based on solely past record. If it assumes that its relative past performance will continue unchanged into the future. The second part is to consider to what extent the value of the past should be modified due to new conditions expected into the future.

Graham has always been a long-term thinker. He is wary of putting too much importance in short-term earnings. We should look at earnings that have been averaged over a long period of time (at least 7 to 10 years). Looking at the longer term provides a better indicator of the future health of the company. This is because short-term earnings have greater analysis required such as scrutinizing any special charges, depreciation changes, income tax anomalies, dilution factors, etc.

But be wary of pro forma earnings. Pro forma earnings enable companies to show how well a company might have done if they did not do as badly as they did. Best thing to do with pro forma earnings is to ignore them.

Look into the footnotes!

Be wary of aggressive revenue recognition practices. It is a sign of dangers that run deep and large.

Also be wary of companies that do not charge expenses against revenues when it is suitable to. Instead, treat these expenses as a capital expenditure that increases the company’s total assets instead of decreasing net income.

Convertible Issues & Warrants – Chapter 16

Convertibles bonds behave like stocks, work like options. And cloaked in obscurity,

They have been marketed often times by Wall Street as a great thing – “the best of both worlds.” You can keep the bond and continue earning interest. Or you can exchange it for common stock of the issuing company at a predetermined ratio.

This is not necessarily a good thing. The buyer of such issues usually would need to give up some yield (they get a lower interest rate) and accept greater risk in exchange for the right of conversion.

All convertible issues should be analyzed individually

Simply being a convertible issues does not warrant it a good investment.

We should also be wary of new convertible issues during near the end of bull markets – where it is most advantageous for the company. A lot of the good bargains of issues are found among the older ones.

My note: I do not have any experience with convertible issues. But from what Graham says, it is not that good of a thing either. So i guess I will stick to stocks/bonds.

Graham wants us to realize something basic but profound.

When we buy a stock, we become an owner of the company

Its managers, all the way up to the CEO, work for us. Its board of directors must answer to us. Its cash and businesses belong to us. Graham advises shareholders to be more active as owners of the company. Management that has goods results should be rewarded and those with bad results should be questioned. He thinks that shareholders should demand a portion of the company’s earnings to be returned to as dividends if the company does not know the best use of the excess capital of the company. In summary, shareholders should think more like an owner when buying stock. Instead of simply treating stock as a piece of paper that wiggles in price daily,

My note: I think that Graham version is akin to today’s becoming a more active shareholder that tries to influence management. I personally do not think this chapter is that important. Because it takes too much effort to try to influence the management. The bulk of work should be analysing past management’s action and be accepting of it before investing in the company.

A Margin of Safety (Most Important!) – Chapter 20

Margin of safety can be a number of things

For example, a railroad company should have earned its total fixed charges better than 5 times (before tax), for their bonds to qualify as investment grade. This ability can constitute as a margin of safety requirement. For bonds, it can also be said that if the business owes $10 million and is fairly worth $30 million, there is room (margin of safety) for shrinkages of two third its value) before bondholders will suffer a loss.

Margin of safety is often said by Benjamin Graham as “the secret of sound investment.”

And “the central concept of investment.” These 3 words – margin of safety – are the most important words in The Intelligent Investor Book.

Margin of safety in stock investing is the difference between the intrinsic value of the company and the price we pay.

The amount of price paid is the most important factor in investment

Determining the purchase price, and having the discipline to only buy at or below the price is where the true test lies at. Graham says that a sufficiently low price can turn stocks of mediocre quality into a sound investment opportunity. Provided that the buyer is informed and experienced and that he practices enough diversification.

The greater the margin of safety, the more leeway we have for things to go bad – before we lose money. If the future is as we expect it to be, or better, the profits we will get are also much higher.

For example, we analyzed a company to be worth $100 and we purchase it with a 25% margin of safety ($75). If the stock reaches the intrinsic value of $100, we have a 33.33% return. However, if we had bought the stock with a 50% margin of safety (50%), we will have a 100% profit.

My note: It is not easy to be patient enough to wait until there is enough margin of safety. In the bull market, there are lesser opportunities. More opportunities in a bear market. That is why value investors welcome it.

The most important reason to use margin of safety

Hardly anyone in the world can hardly make an accurate forecast into the future of a company. There is always a risk of paying too high. The reason for having a margin of safety is essentially to make an accurate forecast of the future less necessary. There is a buffer for inaccurate forecasts.

One of the main reason for investor’s loss Graham says is through buying low-quality stocks at times of favorable business conditions without a margin of safety.

Most investors came into a wrong conclusion about the earnings of a company based on past few good years. This is dangerous. No good company will have great results forever. There is danger in buying growth stocks because investors usually project future earnings of growth companies at rates far above average and place a too high of a premium for these stocks. That leaves little rooms for error. Growth stocks should be purchased only when there is a good amount of margin of safety based on a conservative projection.

Diversification is also a key component of the margin of safety based on Graham

The odds would be with us when we only invest in individual stocks with a large enough margin of safety. The truth is some will not live up to expectations. Having large enough diversification, Graham says that the combined gains will be much higher than the losses. In diversification, the more opportunity we find, the greater the probability that the portfolio will have an above average gain.

My note: I understand myself and my personal style if I am still managing a small amount of money (<100 mn), would be to go for concentration instead of diversification.

A Comparison of 4 Listed Companies, 4 Case Histories & 8 More Pairs of Companies (Examples by Benjamin Graham) – Chapter 13, 17 & 18

Graham gave many examples of companies and case studies in the above 3 chapters. The biggest lesson that we can take away is that there will always be cases where people got too greedy and pay ridiculous prices for stock of companies who is not fundamentally sound. The outcome is definitely not desirable.

There will be cases where companies are currently unpopular but the business is doing well. That means that the stock may currently not be doing well. But the company is doing well. The outcome is usually more desirable investing in such a company. Some good characteristics of a company that will outperform are one that is owned by little institutional investors, no long-term debt and of course, truly superb business characteristics. When the business does well, the stock will do well.

Four extremes to avoid:

- an overpriced “tottering giant”

- an empire-building conglomerate

- a merger in which a tiny firm took over a big one

- an initial public offering of shares in a basically worthless company

Summing It All Up

The intelligent investor is one that is patient, disciplined, and eager to learn. They are also able to harness their emotions and think for themselves. This kind of intelligence as Graham says, “is a trait more of the character than of the brain.”

Warren said to invest successfully over a lifetime does not require us to have a stratospheric IQ, unusual business insights or inside information. We only need a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework.

Whether we achieve outstanding results from our investment, it would depend on the effort and intellect we apply to our investments, as well as the amplitudes of stock market folly that prevail during our investing career. The sillier the behavior of the market, the greater the opportunity for businesslike investor. If we follow Graham, we will profit from folly rather than participate in it.

Stocks become riskier as their prices rise. Less risky as their prices fall. It is not a crime to speculate but Graham suggests to keep it to no more than 10% of our portfolio. Investing is an operation which, upon thorough analysis promises safety of principal and an adequate return. Operations not meeting these requirements are speculations.

Inflation is real. Investing in stocks or REITs are just 2 ways to combat them.

The most important thing that we can learn so far from one hundred years of stock market history is that the intelligent investor must never forecast the future of the stock market simply by extrapolating based on the past. The stock market will not go up indefinitely.

The rate of return an investor should expect to receive is according to the amount of intelligent effort the investor is willing and able to bring to bear on his or her task. The minimum return is to the passive or defensive investor who wants both safety and freedom. The maximum return would be to the active or enterprising investor who exercises maximum intelligence and skill.

The intelligent investor only pays attention to the current stock price when it suits him. Mr. Market works for us and not against us.

The main 5 things to look out for when analyzing a stock (for the active or enterprising investor) are:

- Management competency

- Long-term prospects of the company

- Financial strength

- Capital structure

- Dividend record and current dividend rate

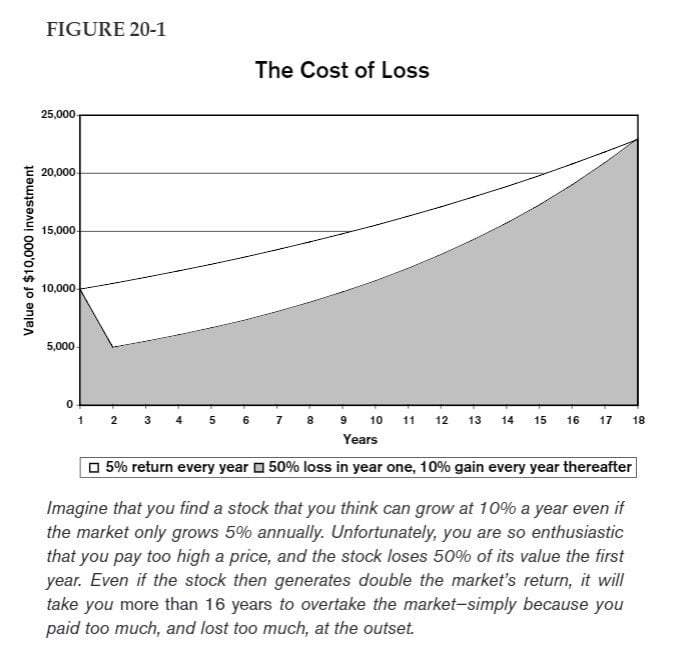

The most important 3 words in investing are Margin of Safety, We should always buy the company’s stock at least 50% below its intrinsic or its true value. To get rich, minimize downside as much as possible. Not losing money is more important than making money. Always have a margin of safety. Look at the image below to see the impact of losing 50% in year one and making 10% every year after vs simply making 5% a year from the outset. Which one do you think is easier? Making double, or not losing money by employing a margin of safety?

Image source: The Intelligent Investor

Losing some money is understandable. We must ensure we do not lose most or all of our money. The biggest risk of investing is ultimately in yourself. Do we overstate our ability? Do we have “well-calibrated confidence” (do I understand this investment as well as I think I do)? And “correctly-anticipated regret” (how will I react if my analysis turned out to be wrong)?

To know whether our decisions are well calibrated, ask how much experience I have, my track record with similar past decisions. Also, asks why people are selling if I am buying. If I am selling, why others are buying. To anticipate our regret correctly, ask if I fully understand the consequences if my analysis turns out to be wrong. Ask how much could I lose if I am wrong.

And always remember, investment is most intelligent when it is most businesslike.

Let us know what you think about this article. Submit a letter to Chris at [email protected]. Subscribe now.

About the Author

Chris is the founder of Re-Thinkwealth.com. Since 21, he started investing in Singapore and U.S. stock market utilizing value investing & options selling strategies. He was glad that he started early because it helped him to accumulate relevant investing experience early. And propelled him to achieve his financial freedom goals faster. He invests & helps complete beginners to learn and apply value investing and options selling by conducting this 1:1 course that guarantees application using real money to invest in stocks. In a maximum 1 year time. Or your money back.

Disclaimer:

The information provided is for general information purposes only and is not intended to be a personalized investment or financial advice.

Important: Please read our full disclaimer.

This article first appeared on Re-ThinkWealth.com.