Spruce Point initiates strong sell opinion on Dollarama Inc. (TSX: DOL / OTC: DLMAF), sees 40%+ downside potential

Spruce Point Capital Management is pleased to support the Robin Hood Foundation, and honored to have spoken yesterday at its marquee New York investor conference. From inception, Spruce Point was founded on the belief that we should do good, help others, and give back to society. Our mission has been to provide unique, actionable, and alpha-oriented research to the public, while exposing poor managers, and those that abuse shareholder trust. Robin Hood’s goal is to fight poverty and help those in need. We ask our readers to please consider making a donation to this worthwhile cause.

Executive Summary

Report Entitled “Hard To Bargain For A Higher Price”

Spruce Point believes that Dollarama (TSX: DOL / OTC: DLMAF or “the Company”) is now a broken growth story that will fail to hit its lofty long-term growth targets, placing its industry-leading margins and valuation multiple at risk of material contraction. As a result, we see ~40% downside risk to C$24.60 per share.

Q3 hedge fund letters, conference, scoops etc

A discount retailer facing serious fundamental headwinds and pursuing unrealistic growth targets with high likelihood of failure

- Rising product prices, progressively saturated markets due to heightened competition, and increasingly stale stores out of touch with Millennials have caused per-store traffic to contract for several years as consumers realize it is no longer a true dollar store. The Company is on pace for its lowest new store count in years despite management’s continued efforts to expand the store base.

- Dollarama’s gross and EBITDA margins are inexplicably high relative to peers, and seem too good to be true. Management also claims to have never closed a store for performance reasons. We expect growth and profitability expectations to fall back to reasonable levels as a number of fundamental factors – tougher competition, wage increases, FX, and logistics costs, among others – pressure the business going forward.

Questionable accounting and governance practices cast doubt on management and the underlying health of the business

- The Rossy family’s tight control over management has led to the appearance of nepotism, questionable related-party real estate dealings, and is perhaps to blame for Dollarama’s strategic missteps and the increasing staleness of its brand.

- Executives are compensated on EBITDA targets, encouraging aggressive accounting and inefficient capital allocation that flatters the income statement. EBITDA-based bonus targets have been adjusted down following misses to allow executives to continue to earn their bonuses.

- Management appears to use aggressive FX hedges and an off-balance-sheet relationship with a Central American retail affiliate to boost margins in a non-transparent way. Adding further opacity, management doesn’t disclose store closings or remodels.

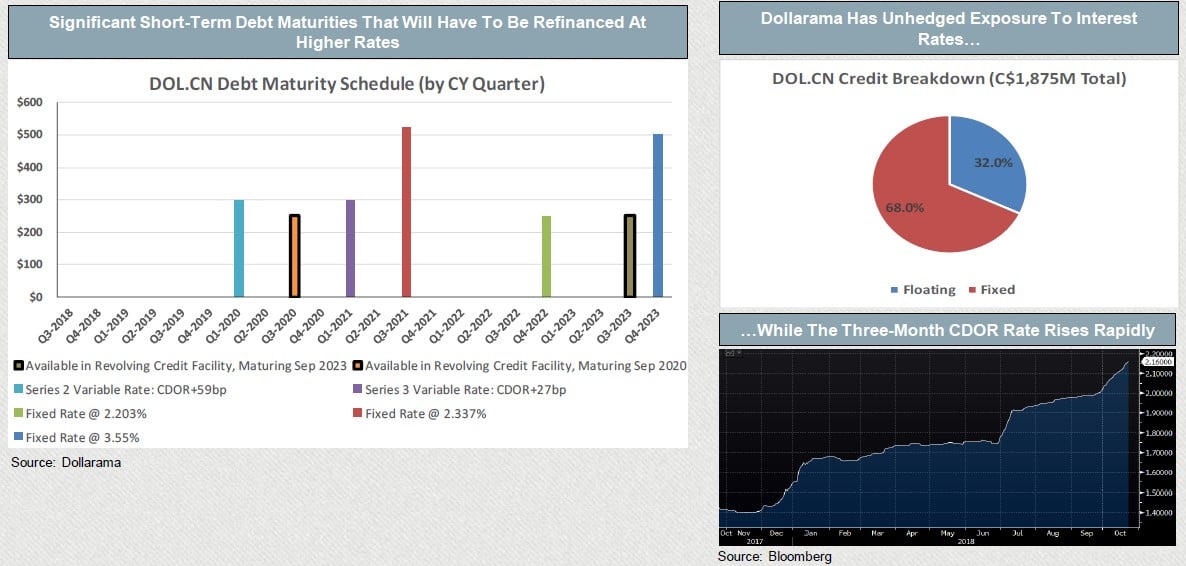

Debt load for share repurchases is skewed to short-term borrowings, presenting material refinancing risk as interest rates rapidly rise

- Close to C$1.4B of Dollarama’s debt matures within the next 12 quarters. Recent CDOR rate increases have and will continue to drive materially higher interest expenses due to the Company’s dependence on short-term debt, magnifying the financial risks to business overexpansion.

▪ Management has been net sellers of stock at attractive prices while the Company overpays. The CFO owns no shares, creating misaligned incentives.

▪ Dollarama would be better served allocating capital towards refreshing its stores and optimizing its logistics chain rather than repurchasing shares.

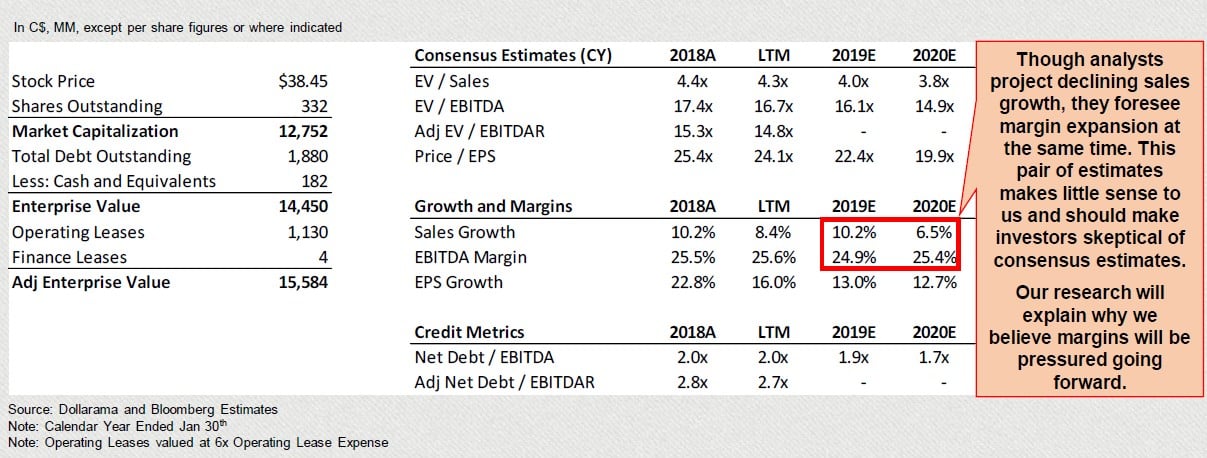

Canadian sell-side analysts are blissfully optimistic, and see little risk that Dollarama’s industry-leading valuation will compress

- A majority of analysts rate Dollarama a “Buy” without questioning its growth plans or profitability. The sell-side collectively sees 24% upside in DOL.

- If we assume that Dollarama will hit its lofty growth targets and aggressively value it as a mature, ex-growth business today, we are hard-pressed to justify a price target much more than C$43.62, or just 11% upside.

- Valued at 4x revenue, 16x EBITDA, and 23x EPS, DOL is priced at a 50-60% premium to its discount retailer peers. These multiples put DOL in an elite class of retail stocks, and are more reminiscent of what one would expect to see in an established high-fashion retailer than a low/no-moat dollar store facing fundamental headwinds. In a base-case scenario, we believe shares have ~40% downside risk.

Spruce Point Believes Dollarama (TSX: DOL) Is A “Strong Sell” With ~40% Downside Risk

Dollarama (DOL or “the Company”) is a dollar store which, following a series of price hikes over the course of several years,is no longer a true “dollar store.” As a result, DOL has fallen out of favor with value-oriented customers, causing average store traffic to contract and thus necessitating further price hikes to support SSS growth. Management is nonetheless aggressively pursuing unrealistic growth targets even as competitors flood the discount retail market and threaten its improbable margins. DOL’s shares trade at a 50% premium to peers in the value retail space – even following a ~20% drop after a disappointing Q2 – questionable governance and poor earnings quality notwithstanding.

We believe that DOL will continue to miss lofty investor expectations, and that its premium valuation will continue to be pressured.

A Retailer Of Low-End Products With Declining Fundamentals In An Increasingly Competitive Environment

- Undifferentiated Products: Dollarama sells a variety of low-priced products, mostly sourced directly from Its purported advantage in “sourcing” is contradicted by conversations with industry sources as well as numerous IP infringement lawsuits filed against the Company.

- Moving Upmarket Is A Risky Strategy: Faced with years of negative average traffic growth and an increasingly saturated market, Dollarama is driving comparable store sales growth by selling higher-priced However, in doing so, it is quickly losing its reputation as a true “dollar store,” and per-store traffic numbers are declining as a result. Big Lots (NYSE: BIG) undertook a similar strategy in the 2000s, but reversed course after admitting its failure.

- Saturation Is Imminent: Dollarama cited a 900 store target at the time of its IPO in 2009, when it had just 585 Management has since revised this number upwards multiple times: first to 1,200, then to 1,400, and most recently to 1,700. Our analysis shows that this target is unrealistic, and that the market is already bordering on oversaturation. Dollarama’s FY ‘19 store opening pace has thus far been its slowest in years.

- Margins Inexplicably High And Likely Unsustainable: Gross margins of 39-40% are remarkably high for a discount retailer, but intensifying competition, rising labor costs, rising transportation costs, and a lapsing currency hedge benefit all threaten Dollarama’s high profitability Patterns in Dollarama’s hedging profits and gross margins ex-hedging suggest that management may be leaning on its FX-related profits to prevent its headline gross margin number from declining (see note on next page).

Troublesome Management And Governance Red Flags

- Founding Family (And A Director) Have Significant Related-Party Deals: The Rossy family launched Dollarama from its legacy retail chain in 1992 and owns significant real estate assets that are employed by the This may have played a role in management’s recent decision to acquire Dollarama’s existing Montreal distribution center from the Rossys rather than open a second distribution facility in western Canada, as have most peers.

- CEO Stepped Down And Installed His Son: Larry Rossy stepped down as CEO in 2016 (and as Chairman in 2018), selecting as his replacement his son Neil – previously Dollarama’s Chief Merchandising We question whether a thorough and arms-length search was conducted to fill this position.

- Opaque Supplier Relationship: As part of a deal struck in 2013, Dollarama supplies goods (at an undisclosed profit margin) to Central American discount retailer Dollar City in exchange for an option to acquire the chain in However, Dollarama currently has no formal stake in Dollar City, and therefore does not consolidate Dollar City’s results. We are concerned that Dollar City could be overpaying its vendors to lessen the financial burden on Dollarama.

- Insider Ownership Declining: Former CEO Larry Rossy has sold or transferred ~75% of his shares since the 2009 Bain Capital liquidated the last of its shares in 2011 at a split-adjusted price of $5 per share, 1/8th the current price. The current CFO owns no shares and regularly liquidates options.

Questionable Accounting Techniques And Capital Allocation Decisions Weaken Quality Of Earnings And Financial Position

- Currency Hedge Supposedly A Pure Offset To CAD Depreciation, But Has Been A Material Profit Center: Dollarama claims to hedge currencies only to lock in consistent prices (in CAD) on which its customers can However, in practice, the Company adjusts prices to match non-hedged competitors, leaving us to wonder why it hedges at all. Much of the recent hedge benefit appears to have reversed, but gross margins ex-hedges conveniently rose by just enough over the last two years to maintain steady profitability. If nothing else, we question whether Dollarama’s elevated margins are sustainable.

- Tenant Allowances And Leasehold Improvements Are Amortized Over Very Different Periods: While accounting rules may give sufficient leeway to permit this difference, we question why lease term assumptions should differ for these two capital accounts. Earnings quality suffers notwithstanding.

- Sales Of Certain Assets, Such As Vehicles, Appear To Be Completed At Above-Market Prices: While the financial impact of these moves is difficult to quantify (perhaps due in part to Dollarama’s opaque relationship with Dollar City), the liquidation of certain assets is significant in some quarters.

- Leverage Is Increasing: Dollarama makes long-term financing decisions using short-term debt, the cost of which has risen with recent debt issuances and is likely to continue to increase with rising interest rates – and as the Company’s credit profile grows We question management’s decision to increase leverage to support buybacks and dividends simply because the earnings yield is above the after-tax cost of debt. We also worry about the state of the balance sheet should the economic environment turn, or should the business decline more rapidly.

- Depreciation Is Well Below Capex And Has Been For Years: Capital spending easily bests industry peers, both as a percentage of sales and vis-à-vis steadier D&A The mismatch with D&A suggests poor quality of earnings at the very least. Meanwhile, management’s growth orientation has diverted capital spending away from store remodeling, giving stores a stale and dated feel despite rising price points.

- Acquiring Real Estate Flatters EBITDA: Acquiring related-party real estate not only lines the pockets of the founding family, but also allows Dollarama to shift rent expenses out of the operating The artificial EBITDA boost helps management to achieve its EBITDA-based compensation targets.

Easy To Justify ~40% Downside In DOL Shares

- Valuation Is Indefensible: DOL currently trades at a ~50% premium to peers and carries among the highest multiples of any global Higher only are the valuations of crème de la crème global fashion brands – Hermes, Prada, Ferragamo, etc. Such lofty multiples are inappropriate for a dollar store with serious near-to-medium-term business risks. Analyst estimates are not sufficiently skeptical of management’s targets in light of these concerns.

- Even If Nothing Goes Wrong, The Stock Is Overvalued: Even if Dollarama executes its growth plan perfectly, maintains its world-leading margin, and retains a hefty valuation premium to its peers, the stock is at best fairly valued at ~$43.

- Under More Reasonable Assumptions, DOL Stock Is Overvalued By 40% At Current Levels: Even assuming that Dollarama achieves full market penetration – with no negative impact on per-store revenues from competition or cannibalization – the stock is worth $28 under normalized margins and at a multiple closer to peer norms, down ~40% from current

- Analysts Bullish, But Wavering: Dollarama’s disappointing Q2 – including SSS guidance contraction and a YoY decline in operating cash flow – provoked some downgrades, but analysts still see ~26% upside in DOL shares regardless. We believe that analysts are too trusting of DOL’s growth targets, but that the Q2 miss put the Company on notice with a number of analysts. Further disappointing quarters could bring more drastic analyst revisions.

Capital Structure And Valuation

At present, Dollarama demonstrates impressive margins and is not egregiously over-levered on a Net Debt-to-EBITDA basis. However, as competition increases, customers push back against recent price hikes, and operating costs creep upwards, we believe that management will have a difficult time maintaining current profitability levels – particularly while pursuing an aggressive growth strategy. Leverage will be less sustainable should the business’ performance decline or the economic environment turn, threatening management’s ability to support continued buybacks / dividends while growing store count.

Short-Term Debt In A Rising Rate Environment Introduces Refinancing Risk

Dollarama refinanced significant short-term debt just last evening, levering up the business in the process.

Management refinanced its C$400M of 3.095% fixed-rate notes due this November with C$500M of 3.55% fixed-rate notes due November 2023. Management’s use of short-term debt has burdened the business with refinancing risk in an environment in which the CDOR rate has risen sharply and is expected to rise for the foreseeable future, which has now forced the Company to bear materially higher interest expenses (compare to its 2.203% fixed-rate credit due in 2022). The Company still has C$1.4B of debt due to mature within the next 12 quarters (including its credit facility), leaving it exposed to further rate increases. The Company’s weighted average debt maturity is about 3.5 years.

Article by Spruce Point Capital