Euclidean Technologies letter for the fourth quarter ended December 31, 2018, titled, “What Happens When Valuation Multiples Compress.”

Three months ago, we noted the market had been locked in a tight embrace of expensive and profitless companies. [1] We also stated that we believe our style of investing will distinguish itself over long periods when profitable companies are in favor and valuation multiples compress.

Q3 hedge fund letters, conference, scoops etc

Since then, equity valuations have dropped in a big way. Even as the S&P 500 posted its worst December in more than 85 years, smaller public companies fared much worse with the Russell 2000 falling over 27% from its late August peak before slightly rebounding at year-end. Euclidean’s holdings also declined, bringing this year’s return down from +9.8% as of third quarter’s end to -8.6% at December 31st.

In this letter, we explain why we welcome—and why we believe all long-term, value-minded investors should welcome—this decline, particularly if it indicates the markets are making a lasting transition to a less exuberant regime.

The Market That Is/Was

We believe it is speculative to invest in companies that are either richly valued in relation to earnings or have not yet demonstrated an ability to consistently generate cash for their owners. This belief, and our corresponding unwillingness to compromise on valuation, has a strong foundation. Across decades of market history, there is abundant evidence that getting the most demonstrated (not imagined) earning power for your investment dollar has been key to long-term success. [2]

And yet, outside of a brief interlude in 2016, we have been living through the longest period of expensive-stock dominance since World War II. [3] This period has been characterized by investor enthusiasm for fast-growing companies that have not yet delivered the earnings necessary to support their lofty valuations. While some of these companies may ultimately deliver results that justify investors’ willingness to “bet on the come,” owning the market’s most expensive stocks has generally proven to be an unfruitful basis for long-term investing. [4]

In this context, the valuation difference between the market’s most expensive and inexpensive companies has widened. On a variety of valuation measures, the spread is approaching what was last seen at the end of the dot-com era. [5]

Of course, there have been other enthusiastic periods in the past. In each case, they challenged the endurance of value investors whose discipline prevented them from owning the expensive stocks that led the market. But these periods have always eventually come to an end. And, after they ended, our sense is that value investors did well because other investors were reminded of two things: One, even great companies became bad investments when priced too high. And two, companies with established cash flows provided a reliable foundation for valuation.

This is a reason that, as we discuss in more detail later in this letter, a large portion of value investing’s attractive relative returns have come after buoyant markets ended, across multi-year periods when earnings multiples came down.

And so, if the market’s fourth quarter signals an emerging transition away from this exuberant market regime, then the fall is welcome. But this does not mean that the transition to a more conducive value environment should feel especially smooth or comfortable.

What Happened in the Fourth Quarter?

During the last three months of 2018, investors were reminded that, from time to time, market prices significantly fall. Our perspective is that these kinds of drops are not only a core element of how markets work, they are also essential for investors who depend on opportunities to buy securities at prices below their intrinsic values.

While price and value are often perceived to be the same thing, we view them as two very different concepts. You can see the difference by comparing the volatility of share prices and company fundamentals. [6] For example, well-established public companies such as Amazon, AT&T, and Exxon show 52-week highs 40–75% higher than their 52-week lows. And yet, the actual financial results and future potential of these companies has not fluctuated to anywhere near the same degree as their stock prices.

Divergences between price and value can emerge whenever investor attention is taken away from company fundamentals. They may appear when investors become fearful about how some macro event will impact the world economy. They may also arise when investors become forced sellers.

At the end of 2018, we believe both of these causes have been at play. Investor attention has been focused on trade negotiations, government dysfunction, the potential of an upcoming recession, and the path of interest rates. In this context, many companies had their market values decline by 20–30% while enduring no impairment to their long-term earning power. These declines may have been amplified by fund liquidations and year-end withdrawals, general deleveraging, and tax-loss harvesting.

So, during the fourth quarter, we perceive that many investment decisions have been made for reasons disconnected from companies’ long-term fundamentals. Thus, a setting has emerged that is ripe for creating bargains.

This is why we welcome the current market decline. No question, it can feel crummy to receive a statement that shows a negative return. But we are playing a long game. The lower the prices at which we can buy pieces of good businesses, the higher we expect our long-term returns to be. We believe the current market decline provides the fuel needed to deliver the attractive long-term returns you count on from Euclidean.

And this gets to an important point. If this decline signals a transition away from the recently exuberant market regime, what can we learn from how different strategies perform during more pessimistic times, when overall valuations trend down across several years?

Where The Opportunities Are When Valuation Multiples Compress

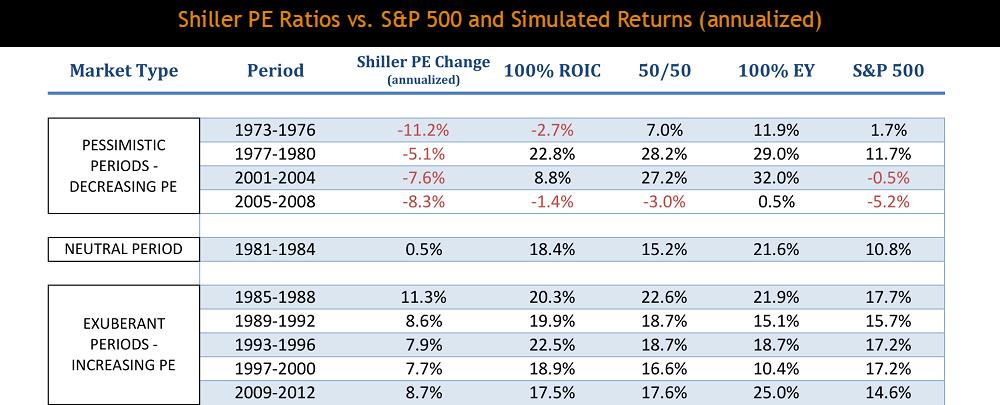

Five years ago, we made a series of observations that inform how we think about the recent market fall and the opportunity for Euclidean’s investors. Those observations emerged from looking at how different strategies might have performed during optimistic and pessimistic times, when valuation multiples had been expanding or contracting, respectively. While more detail can be found where we originally described the study, we provide a summary here.

In the study, we segmented the past into optimistic and pessimistic periods. We divided the previous 40 years into 10 four-year segments, defining each one as pessimistic or optimistic based on whether valuation multiples increased or decreased across its span. Our measure of valuation was the Shiller P/E—also known as the Cyclically Adjusted P/E—which looks at the S&P 500 index level in relation to the trailing 10-year earning power of the index’s constituent companies. [7]

Next, during each of those four-year periods, we compared the simulated returns of three different 50-company portfolios to the S&P 500’s total return. One portfolio represented “good companies” and consisted of the most highly ranked companies based on their returns on invested capital (ROIC). Another portfolio represented “good prices” and consisted of the most highly ranked companies based on their earnings yields (EY). [8] And the third portfolio used the combined rank of good companies and good prices to hold 50 stocks with the best combinations of returns on invested capital and earnings yield. The results follow:

These are simulated returns and do not represent actual performance

You will notice that the relative results varied depending on the market environment. During optimistic times, you may have done well by being insensitive to price, and investing in the best companies (the 100% weighted ROIC portfolio) while ignoring the value opportunities.

On the other hand, investors sometimes are less willing to pay premium valuations. When this occurs and overall market valuations come down, it appears that index investors would have generally realized poor returns. During these pessimistic periods, however, we believe a good place to hide has been with the overwhelming advantage offered by the least expensive companies (e.g., the 100% weighted EY portfolio).

Perhaps as we end 2018, after years of increasing valuations and growth stock outperformance, we are moving from an exuberant period to a more pessimistic one. While the monthly returns may be volatile along the way, we think such a transition should bode well for Euclidean and our value-minded brethren during the years ahead.

Best regards,

John & Mike

The opinions expressed herein are those of Euclidean Technologies Management, LLC (“Euclidean”) and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Euclidean reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Euclidean Technologies Management, LLC is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Euclidean including our investment strategies, fees and objectives can be found in our ADV Part 2, which is available upon request.

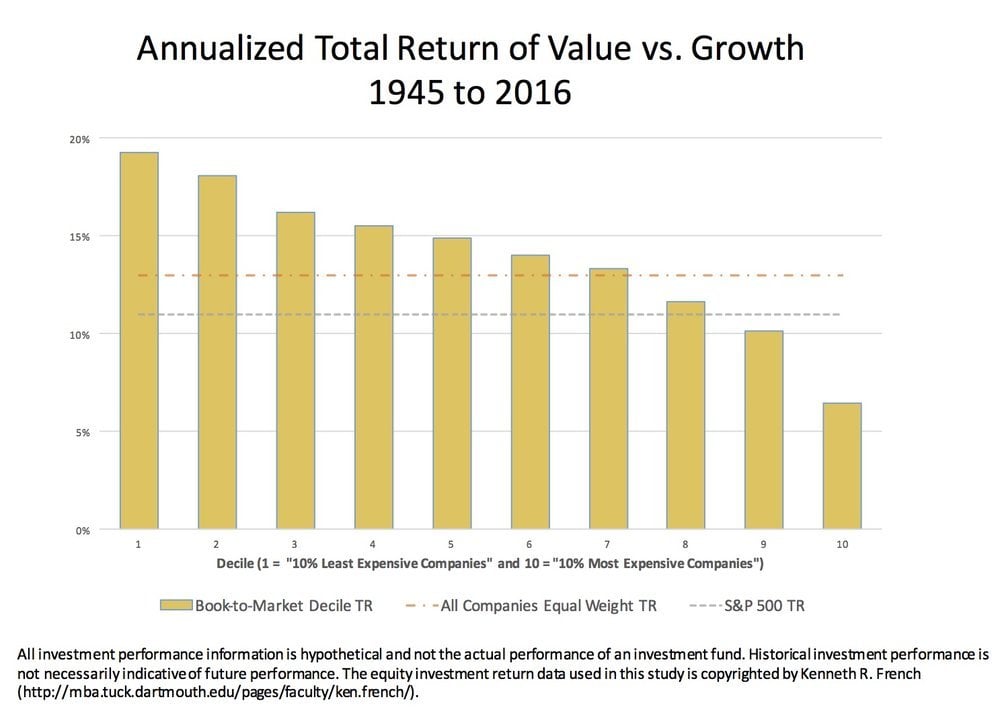

[1] WSJ | Unprofitable Firms Are Outperforming Other Growth Stocks [2] Yes, it is true that a company’s future value will be determined by its future cash flows. But what is the best way to estimate these future cash flows? Our view is well-captured by this quote from Benjamin Graham’s Security Analysis: “The soundness of a security purchase is determined by future developments and not by past history or statistics. But the future cannot be analyzed; we can seek only to anticipate it intelligently and to prepare for it prudently. Here the past comes in—through the back door, as it were—because long experience tells us that investment anticipations, like other business anticipations, cannot be sound or dependable unless they are closely related to past performance." [3] Euclidean Letter, Q2 2017 - The Current Value Recovery Has a Lot of Upside Potential [4] The chart below shows the annualized total return of value vs. growth from 1945 to 2016. The market is divided into ten groups, with each constituent company given equal weight in its respective group’s results. The least expensive 10% of companies are represented in the group furthest to the left, and the companies that are most expensive in relation to their book values are on the far right. We use book-to-market, as it is both a widely studied factor and it allows this analysis to stretch back 70 years. We have seen a similar advantage for inexpensive companies when expensiveness is measured in relation to other fundamental qualities such as sales and earnings. In this analysis, on an annualized basis, the least expensive companies returned 13% more than the most expensive ones.

Earnings Yield = (Earnings Before Interest & Taxes + Depreciation − CapEx) / Enterprise Value (Market Value + Debt − Cash)

Article by Euclidean