Alpine Capital Research commentary for the fourth quarter ended December 31, 2020, titled, “A Triumph of Science.”

Q4 2020 hedge fund letters, conferences and more

Our year-end commentary begins with gratitude for the multiple vaccines that look likely to finally end the pandemic. We stand upon the shoulders of the scientists, entrepreneurs, and workers who developed the breakthrough technologies and incremental improvements that got us to this point. It could have been so much worse.

Imagine if the virus struck 40 years ago in 1980. How long might it have taken to deliver an effective vaccine and (or) reach herd immunity? How would the economy and supply chains function without modern technologies like the Internet? One shudders to think about the cost to humanity after several years of COVID-19 overrunning our healthcare systems and killing millions a year.

Yes, we could have done better. The SARS-CoV-2 virus was bad, but this is also a trial run for a potentially worse pathogen more fatal or less amenable to vaccination. Our task now is to study precisely what went right and wrong. Let us insist that our elected leaders invest in the resources and properly incentivize the scientific community so we can be far better prepared for what is almost sure to happen again someday.

Our commentary is divided into four digestible vignettes to summarize where we have been and where we believe we are going.

2020 Results: A Predictably Unpredictable Ending

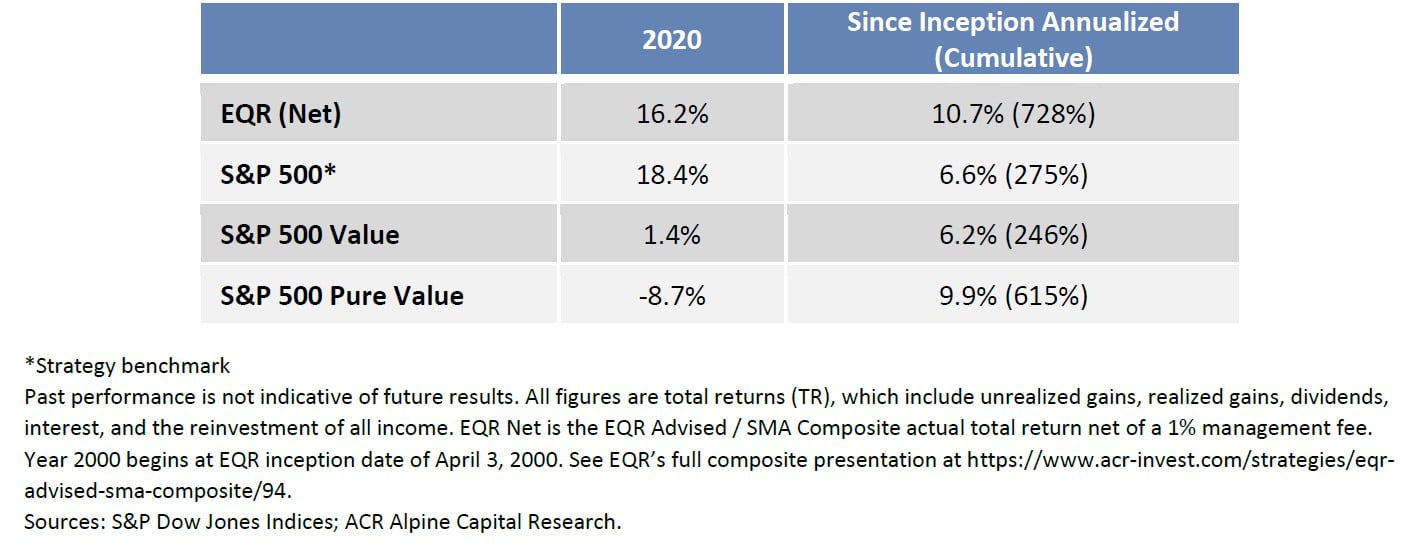

Equity investment results are more properly assessed over a decade than a year. Nonetheless, we adhere to the convention of reporting results after a turn of the earth around the sun. Just don’t ask us to call one year’s results a proper return. A return occurs when you get your money back through dividends, realized capital gains, or successfully reinvested retained earnings. One year reflects price fluctuations that may or may not stick.

Our advantage in 2020 compared to the value indexes is mostly due to the deployment of our significant cash reserves as prices plummeted in March. Financial markets and our portfolio thereafter spent much of the year recovering. Finally, we were rewarded late in the year after several of our beaten down “value” stocks surged, and our EQR strategy almost caught up with the tech-heavy S&P 500 Index.

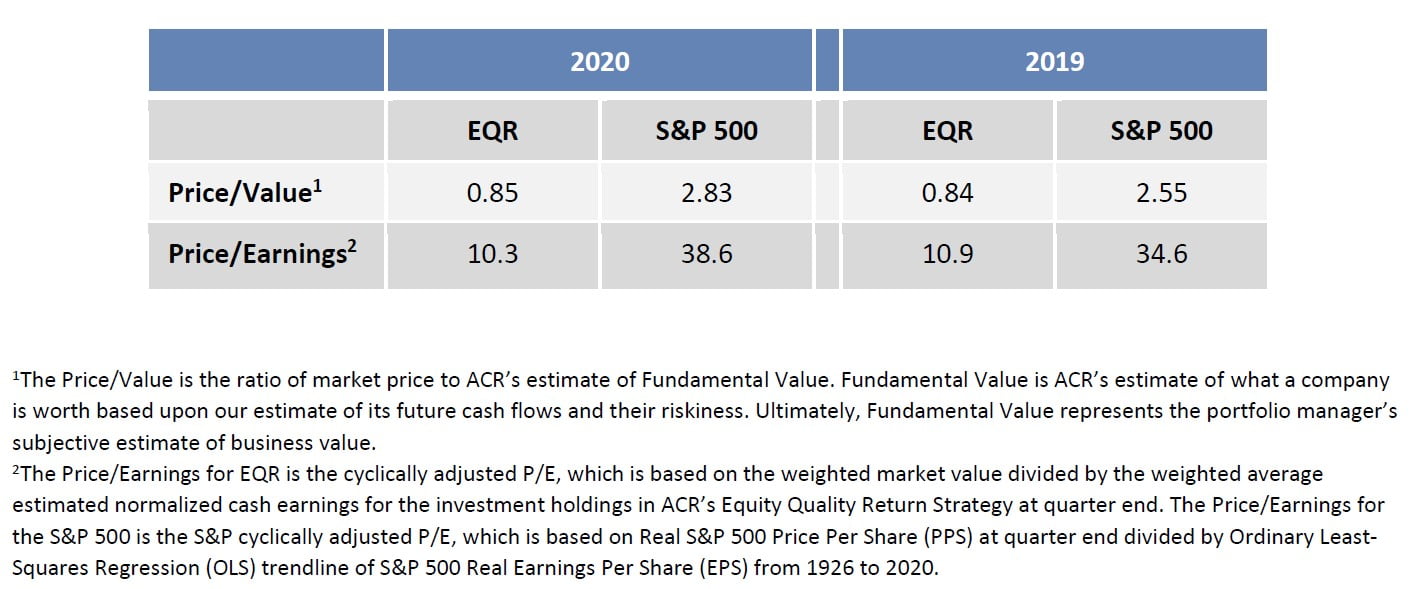

The upshot is that we sidestepped weaker results in the value indexes while still retaining what we believe is latent unrealized value in both our value-oriented portfolio and the S&P 500 Pure Value Index. Conversely, our analysis shows that the S&P 500 is more overvalued than ever. Oddly enough, the year ended with markets more distorted than they were at the end of 2019. Key valuation statistics are below:

Our first quarter commentary detailed how we navigated the pandemic in real time. Core snippets of this recap follow.

The economy ended 2019 with unemployment near all-time lows and equity-market valuations near all-time highs. Our EQR strategy held a 38% cash balance at the time of the market peak on February 19, as we found more companies to sell than to purchase from 2017-2019. Coronavirus reality then set in, and on March 23, a mere 33 days later, the S&P 500 was down 34%.

As prices plummeted, the ACR investment team sprang into action. The nature, severity, and dynamics of the virus were assessed. Our macroeconomic advisor Professor Steve Fazzari was early in forecasting a historic GDP decline. He also counseled that the economic dynamics associated with the shutdowns were less likely to result in a conventional depression than they might following a more typical financial crisis. Bolstered by a strong fiscal response, we believed that recovery could therefore be quicker than in past business cycles. Nevertheless, ACR’s foremost objective remains capital protection, so we prepared for the worst and hoped for the best.

Portfolio companies and potential purchase candidates were assessed for shutdown impact and loss estimate ranges. Importantly, our analytical framework did not rely on precise virus containment and economic reopening timelines for success. The exact path toward normalization was unknown and, therefore, many companies remained beyond assessment. However, our analysis showed that certain companies had the financial strength and cash-flow durability to survive a longer-than-expected shutdown.

Numerous companies capable of surviving a depression-like scenario were suddenly on sale. The investment team deployed $850 million during March, lowering the cash balance in our EQR strategy from 38% to approximately 12%. Equities purchased were on average 47% off their highs and selling at 59 cents on the dollar (a price/value of 0.59 based on our assessments of company values). Our fundamental discipline is to safely lock up durable cash flows at low prices. Prices were low, and we executed on our strategy.

We believed that regardless of what the next few years held, our March purchases would prove to be profitable due to the favorable prices secured. We provided specific estimates in our first quarter commentary that we continue to stand by. What happened next was something that we had never witnessed: a bubble in a crash.

Almost as quickly as the shutdown recession struck in March, direct stimulus and government-sponsored lending facilities helped to rescue the economy. Perhaps unavoidably, savings also spiked, and stock market speculators ran wild. Market participants myopically and radically bet on “stay at home” stocks and promising technologies, which in turn created a historic imbalance in equity prices. Numerous companies without a dollar in profit, and in some cases no revenue, exploded into multibillion-dollar market values. We follow innovative technologies closely as they drive corporate profits and productivity, but we have no interest in radically overpaying for them.

Conversely, financials, industrials, energy, and other old-school companies, which were selling at historically depressed values relative to growth companies prior to the pandemic, declined even faster than the market during March, and in most cases were slower to recover, at least until later in the year. While our EQR strategy rebounded over 70% from its March 23rd low through year-end, nine of 18 portfolio companies still sold below 10x our estimate of their normalized cash earning power at year-end.

What’s Next: A Wile E. Coyote Moment?

So where does that leave us today? We believe that our EQR strategy will generate a return from January 1 of this year consistent with its historical average of approximately 10% per year, net of fees. Our forecast is based on simple math and disciplined work. The simple math can be boiled down to a high level of normalized profit relative to prices. The discipline comes from painstakingly selecting a portfolio of companies that produce real cash profits rather than accounting fiction, where business prospects are sound and cash earning power is durable, and where capital allocation policies provide assurance that we as shareholders will receive those profits via dividends, share retirements, or successfully reinvested retained earnings.

As for the market, many believe that a “new normal” has set in and that life will be radically altered by the SARS-CoV-2 coronavirus. “New normal” may be two of the most dangerous words in investing, just behind the four most dangerous words: “this time is different.” One of the investor’s central tasks is to sort through endless reams of information for what is truly important and to identify lasting economic drivers among cyclical or shorter-term trends.

The world is constantly evolving. In that sense, each year is a new normal. Industries rise and decline, new technologies replace old. Brick and mortar retail is both dying and evolving as it is replaced by digital commerce, a trend that has been unfolding for years. The pandemic accelerated the trend, yet there will also be a one-time stay-at-home “bump” that will recede post-pandemic as the secular trend resumes. Certainly, the pandemic will alter some behaviors permanently.

The ACR investment team follows changing patterns of consumer and business behavior in real time at the company and industry level. For example, it became clear in May that automobile purchases would not be a casualty of the work-from-home movement. Trend miles driven are likely to be somewhat reduced post-pandemic, but vehicle ownership was not going the way of the dinosaur just yet. Conversely, we are less sure of normalized business travel post-pandemic and have adjusted revenue trends in commercial aerospace accordingly.

Globally, recovery is likely to be robust in 2021, but a return to trendline GDP growth in the next couple of years and a recovery in corporate profits should not be confused with support for equity prices. Buy on the rumor, sell on the news. The rumor of a full recovery is well known. By the time the economic data are fully registered, the financial markets will be straining to see around the next corner. Most importantly, investors must never confuse robust profit growth with investment returns, as investment returns are contingent on both profits and the price paid for them.

Today’s problem is not a broken economy or corporate sector. It is the price one has to pay to own the corporate sector. Like the boy who cried wolf, we have been complaining of this growing imbalance for more than five years. The problem has only gotten worse, and so have our cries. For the many companies with sky-high valuations relative to little or low current profits, only time will tell how patient the market will be as the fantastic growth expectations for these companies unfold. Prices will no doubt reflect cash profits someday. The question is which companies will have their Wile E. Coyote moments: flying off the edge of a cliff, suddenly realizing that profit is miles below.

Our Mea Culpa – Capital Protection

As students of history, the ACR investment team is well acquainted with the details of past booms, busts, and financial crises, including the Spanish Flu of 1918. Yet nothing can fully prepare one for what it is like to live and make decisions during historic times. Our 2010 year-end commentary was devoted to “Lessons and Myths” from the Great Recession of 2008, which were many. While we have learned several lessons from the pandemic, we will focus here on one that led us to an important mea culpa.

ACR’s foremost objective is to protect capital from impairment. Our mistake was to inadvertently align capital protection and volatility reduction when communicating with clients.

While we have gone to great pains to express our strongly held view that risk is not volatility, and we have often repeated that our goal is not to protect against volatility, we emphasized “downside capture” and “downside protection.” Both measures could imply volatility protection, which has never been an explicit ACR objective.

Let us then be clear about what we mean by capital protection, and equally important, what we do not mean by capital protection. Our foremost objective is to protect our investors’ capital from an unsatisfactory return caused by a decline in the earning power of the companies we own or an excessive purchase price. Capital protection comes not from reduced volatility but owning companies with durable profits and paying the right price for them.

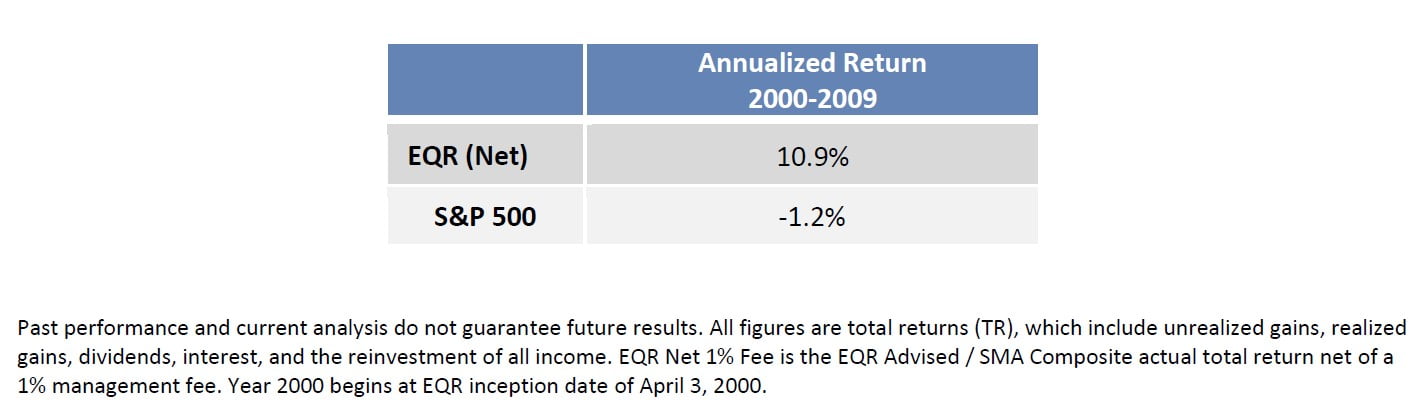

One reason the topic of capital protection can be confusing is that the stock market always goes up in the long term, if you give it enough time. Yet this is disingenuous. Investors deserve an equity-like return over a reasonable time horizon. In our view, 10 years is sufficiently long. The 2000s were an excellent example of a decade that required true capital protection:

Now let us describe what capital protection is not. Capital protection is not lower volatility than the market or prices that decline less than the market. During declining markets our portfolios are likely to decline less than the market, yet such results will not hold in every circumstance or period. Case in point: we strongly believe that the best way for a fundamental value investor to have navigated pandemic corporate earning power declines and excessive prices was to purchase “value” companies whose prices were declining faster than the market in March.

Owning companies with healthy balance sheets and durable businesses is how we protected against a decline in company earning power. The risk of declining earning power has been largely realized and is now receding. The discipline necessary to buy neglected, undervalued stocks rather than popular momentum stocks is how we have protected against excessive prices. The risk of excessive prices has not been realized and is now greater than ever. While we expect the economy and corporate profits to recover and resume their upward trend, we also expect EQR and overall market returns to look more like 2000-2009 than 2010-2019.

* * *

As this commentary was being penned, the January 6, 2021 attack on the U.S. Capitol shocked us and the world. If this feeble insurrection was meant to incite others to take up arms, it thankfully appears to have failed. Instead, citizens and politicians of practically all stripes came together and condemned the violence and the perpetrators. The coronavirus pandemic and extreme political divisiveness that have roiled our nation now appear to be simultaneously reaching explosive endings. Let us endeavor to make the coming year one of peace, respect, and healing.

Nick Tompras

January 2021