Crescat Capital’s commentary for the month ended September 2021, titled, “The Psychology Of Inflation.”

Q3 2021 hedge fund letters, conferences and more

The Psychology Of Inflation

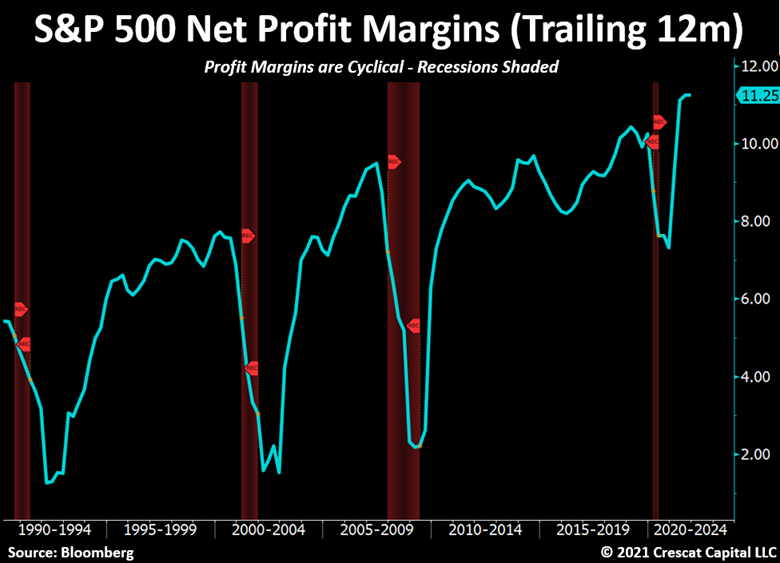

Today’s macro environment is indeed very different than any other period we have experienced in the last four decades. Inflation is infiltrating the mindset of US households in a way not seen since the wage-price spirals of the 1970s. Prices for the goods and services that individuals require to meet basic needs have been increasing at an accelerated pace. These necessities include shelter, food, energy, and transportation. The rising cost of living is due to both supply constraints and increased demand from fiscal and monetary stimulus. In the mix, net profit margins for S&P 500 companies at large are at record highs today, because these firms have been able to pass rising costs onto their customers in the short run.

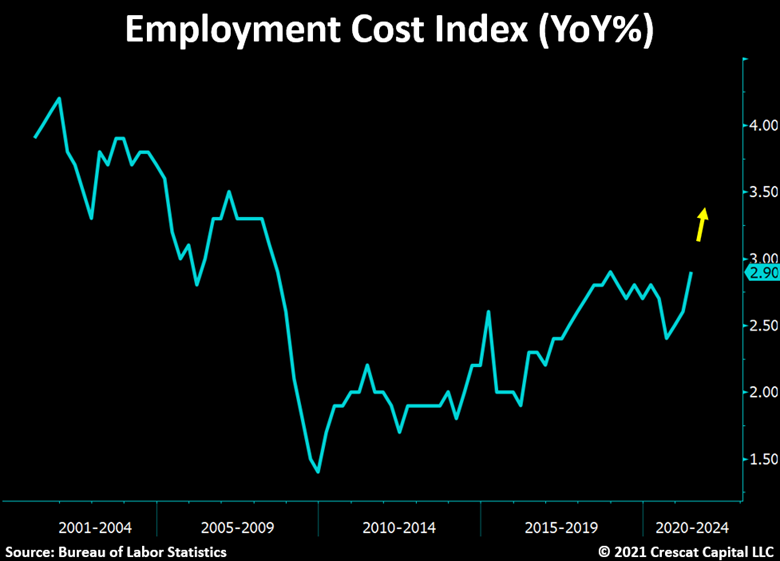

These windfall profit margins are unsustainable and poised to reverse quickly in our analysis. The two biggest costs of running a business that affect net profit margins are on track to rise imminently: taxes and labor. Corporate tax rate hikes are almost certain with the legislation now under consideration by the Democratic-controlled Congress and White House. Even less discounted by today’s buoyant stock market in our view is an impending rise in labor costs. Individuals and families cannot rely on continued government handouts to the degree they were provided during the pandemic lockdowns and the US government cannot afford to provide them. We believe a new and well-justified psychology of rising inflation will be forcing more of the population back into the labor force. At the same time, we are likely to see workers at large both demanding and receiving significantly higher wages and salaries contributing to a substantial squeeze to corporate profit margins in the years ahead.

Increases in the general price level for goods and services and the rising inflation expectations that go along with them are a self-reinforcing helix that is set to become a durable feature of the economy. Just like the 1970s, these inflationary macro forces will likely lead to shorter economic expansions and more frequent stagflationary recessions in the 2020s and beyond than we have had in the last four decades under a generally disinflationary regime. These more contractions in real GDP due to rising inflation are likely to contrast with the deflationary recessions of the 2008-2009 Global Financial Crisis and the short-lived Covid recession in 2020. Starting from record valuations relative to underlying cash flows in the broad financial markets today, combined with historic loose financial conditions, we see substantial downside risk in crowded and highly speculative equity and fixed income markets at large. Rising inflationary pressures and ultimate Fed tightening measures needed to counter them will put downward pressure on hyper-overvalued, low yielding, long duration growth stocks and fixed income investments. We believe investors should be reducing exposure to these limited-upside and high downside-risk-areas of the financial markets today.

We see a silver lining, however, in deep value and high near-term fundamental growth investments in the energy and materials sectors of the economy that are likely to be among the biggest beneficiaries of the new secular stagflationary environment ahead. These sectors are not without volatility but represent a calculated risk with substantial value-driven upside potential for investors who want to profit from the underlying fundamental tailwinds identified by Crescat’s equity and macro models. Diversifying among the best industries and companies within these sectors is what we are focused on now at Crescat with our own money and for clients with a like-minded outlook, risk tolerance, needs, and objectives. In our analysis, this approach is the highest probability path to generating strong risk-adjusted, real returns in the immediate years ahead.

Supply Problems are Structural

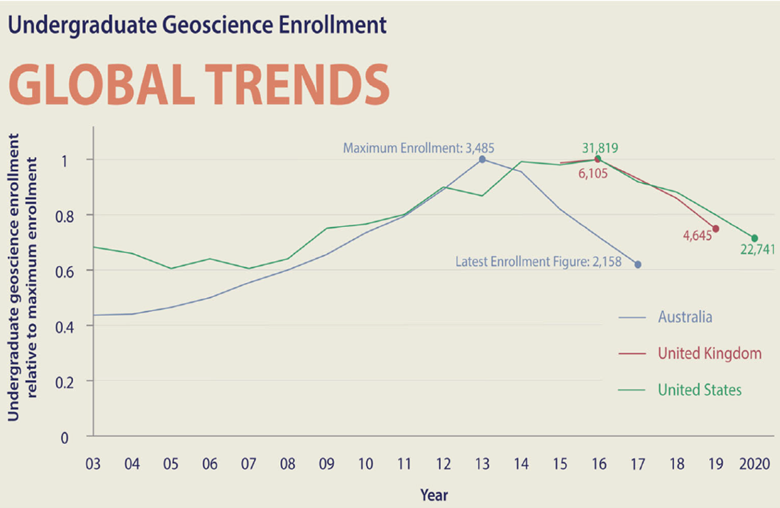

Supply chain disruptions will be with us for some time. They are due to complex structural problems that include a new deglobalization countertrend, particularly between the US and China. Another problem is the chronic underinvestment in the energy and basic materials sectors of the economy. As capital has overwhelmingly flowed to the information technology and innovation sectors of the economy in the last decade, the capital needs of the primary resource producing sectors of the economy got left behind. The goods produced by these industries are at the core of the supply chain and have long lead times with challenging permitting issues and heavy capital expenditure requirements. While demand continues to increase for the raw materials produced by these industries, companies are having difficulty filling jobs with qualified management and technical professionals to produce them efficiently. A decade of declining college enrollment in geosciences worldwide is one of the long-term structural imbalances affecting the oil and gas and mining industries. Skilled tradespeople in these industries are also in short supply.

Source: Samuel Boone and Mark Quigley, University of Melbourne.

Resource logistics issues are compounded by the environmental moment, which has captured both social norms and government technocrats, significantly adding to costs and lead times to produce basic resources. The push for the new green economy might be well intentioned but continues to have many blind spots regarding the need for traditional energy and material resources to ensure a healthy economy today as well as in the more environmentally friendly future.

Stagflation is Here

The problem is that while consumer prices are rising, we are also seeing signs that the global economy is starting to decelerate. China is the elephant in the room in that respect. The second largest economy in the world has achieved that spot while creating a property and credit bubble that, as measured by banking assets to GDP, is more than four times the size of the US housing and financial sector bubble ahead of the GFC. With its equity markets under pressure since February, the Evergrande collapse, and nationwide energy shortages, China’s economy appears to be in a serious meltdown. The spillover effects should not be underestimated. We need to start discounting now the ultimate new global fiscal and monetary stimulus that will be needed to counter China’s currently unfolding credit collapse and what that portends for its currency given its communist banking system with a whopping $52 trillion of suspiciously priced assets. As we have learned throughout the world in the post GFC era, the speed at which governments can create new central bank money is instantaneous. At the same time, and more than ever today, the speed at which countries can deliver the basic resources to meet their citizens’ needs is significantly impaired.

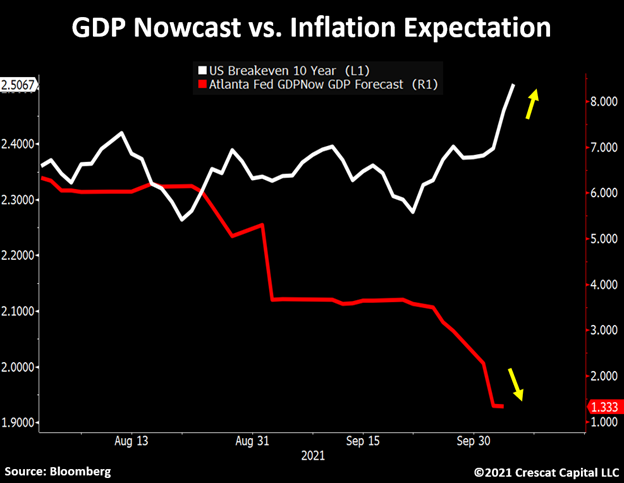

The US economy has already started to slow significantly. The Atlanta Fed GDP nowcast, for instance, just went from 6% to 1.3% in the last couple of months. With business activity now decelerating as inflation remains historically elevated, the set of monetary and fiscal policies needed to fix one problem would worsen the other. At the same time, with historic high valuations for equity and credit markets in the US at large, there is much downside risk. The Fed is trapped to do anything to prevent a rotation out of speculatively priced assets with deteriorating fundamentals.

Note the tight correlation between the real-time Atlanta Fed’s macro quantitative measure of real GDP growth and actual subsequently reported economic growth after inflation.

Great Rotation

Financial markets are not correctly priced for the stagflation that is already evident in the macro data. This creates both risks and opportunities for a large swath of investors who are crowded on the wrong side of this trade in our view. First and foremost, we see a major shift out of overpriced growth stocks and fixed income securities and into a much narrower group of deeply undervalued and high near-term growth stocks and commodity investments that will be the primary beneficiaries of stagflation, creating a reflexive inflationary loop. The smart money should be the first to make this move. We call it the Great Rotation. The motivation for such a shift in our research is that it is the most highly probable way to both protect against the downside risk of significantly rising inflation to financial assets at large while potentially substantially profiting from it at the same time.

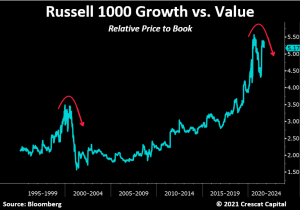

Investors should take note while overall price to book values for the broad market are at record highs along with many other fundamental measures, the relative price-to-book value of the Russell 1000 Growth compared to the Russell 1000 Value indices is about 60% higher than it was at the peak of the tech bubble in 2000, further illustrating the extreme imbalances and market risks along with the set-up for a growth to value rotation.

Getting Ahead with Gold and Silver

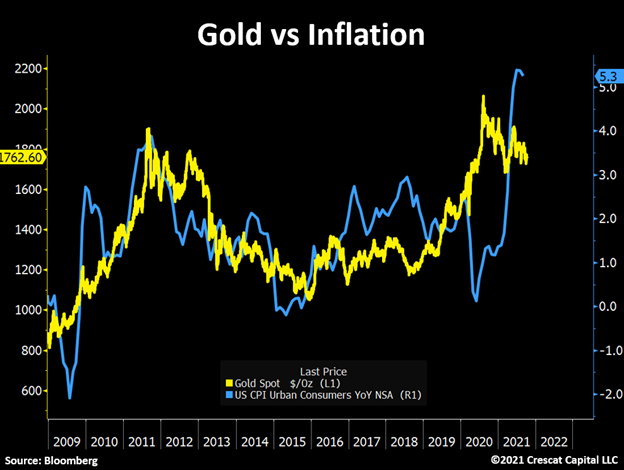

As inflation continues to develop in the economy, the chart below shows the incredible link between gold prices and CPI since the Global Financial Crisis. Note how after the pandemic lows, gold front ran the potential risk of a rise in consumer prices and the entire precious metals market appreciated sharply. Gold and silver not only diverged from CPI but also significantly outperformed the rest of the commodities market. It is important to remember that before recently peaking, gold had been going on a streak for two years already. The metal was up more than 75% from August 2018 to August 2020 and even reached historical highs during this period. Back then, with CPI around 1%, very few investors foresaw inflation as a risk to the economy. Now it is a real problem. We think gold likely appreciated too quick and too fast becoming what some thought as an obvious trade. Extreme sentiment probably explains the reason for its recent weakness after signaling way earlier than any other asset the possibility that an inflationary environment could be ahead of us. We are now on the other side of this extreme. Gold looks fundamentally cheap, technically oversold while inflation continues to gain traction. We think the historic relationship between precious metals and the growth in consumer prices will continue to be strong and the recent pullback in gold and silver related assets poses an incredible opportunity for investors to deploy capital at what we believe to be truly attractive levels. Also, keep in mind that we are using government reported numbers to gauge inflation in this analysis. We should all know by now that the true cost of goods and services is growing at a drastically faster pace than CPI.

Recent Pullback in Precious Metals Presents Constructive Buying Opportunity

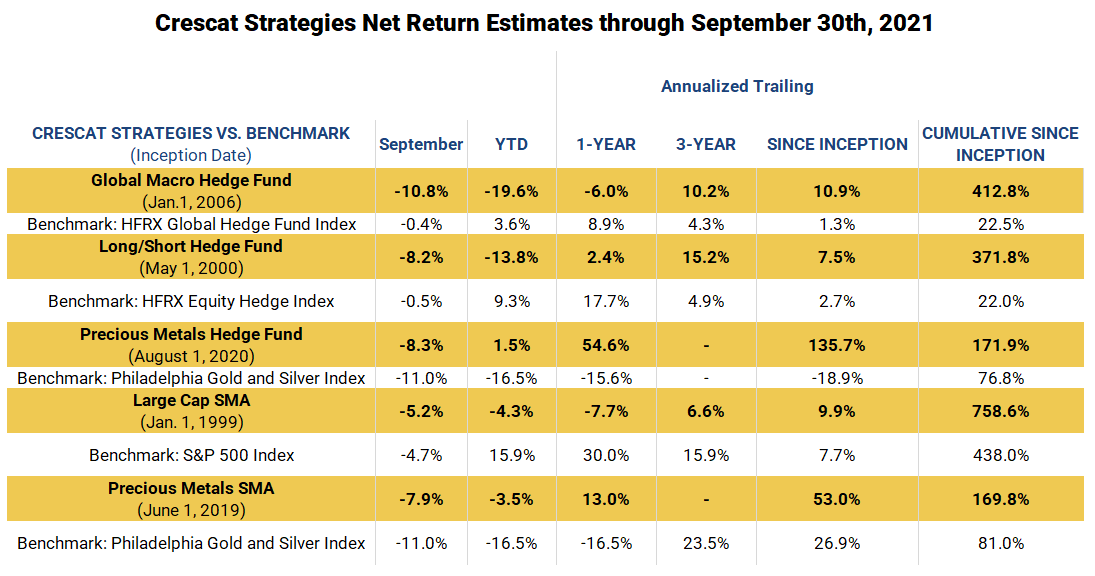

The decline in Crescat’s strategies in the past two months has been almost entirely attributable to our precious metals long holdings which has been deliberately the largest exposure we have had firmwide. Our gold and silver names are ultra-cheap, worth an estimated 15 times their current market prices in aggregate according to our company-by-company model in the Crescat Precious Metals Fund. This fund was up 235% net in its first year ended in July and has experienced an 18.9% net pullback in August and September. The precious metals longs similarly have been the largest contributor to the last two-month decline in our Global Macro and Long/Short funds. These latter two funds also have significant short positions that have held the fund back year to date. We believe they are poised to deliver strong returns as the broad equity markets appear to finally be breaking down.

We are not pleased at all with the recent pullback, but believe it is an inevitable part of the game. We think that accepting a moderate amount of volatility is necessary to build wealth and protect against rising inflation in the current environment of financial repression that we live in where governments maintain artificially low risk-free interest rates compared to true inflation. The goal of this policy is to resolve unsustainable debt-to-GDP imbalances with hidden inflation. We have been increasing our exposure to other resource industries in Large Cap, Global Macro, and Long/Short to add more diversification also with strong upside potential, based on our equity fundamental model scores within the energy and materials sectors. We remain highly committed and significantly exposed on the long side to activist positions in gold and silver mining companies with a strong focus on exploration under the guidance of our Geologic and Technical Director, Quinton Hennigh, Ph.D.

We believe gold and silver commodity and equity markets are due for a major bull market resumption. This market may have already turned in our favor this month from deeply oversold levels for mining stocks and extreme negative sentiment despite incredibly positive fundamentals. All Crescat strategies are up month to date in October. Overvalued equity short positions in our Global Macro and Long/Short also generated positive profit attribution in September though modestly. We aim to increase our short exposure in these two funds to be able to take advantage of the abundant opportunities on this side of the market now that the risk of shorting has been decreased with inflationary pressures becoming more acknowledged and the Fed attempting to start tapering. With Crescat’s three high conviction macro themes coalescing, and after the recent pullback in Crescat’s strategies, we believe it is a highly constructive time for new and existing clients to be adding money to our strategies.

HFM Award

We are pleased to announce that the Crescat Global Macro Fund was just shortlisted for a HFM performance award in the macro category for funds with assets under $1 billion for the one-year period ended June 30, 2021. The final winner will be announced next month in NYC. We understand this is one of the most prestigious awards in the hedge fund industry. There is no guarantee that we will win, but for what it’s worth, according to Bloomberg and eVestment data, our fund was far-and-away the best performer for the period among all five shortlisted for the category. The fund was up 45% net over that time frame.

September Performance Estimates

Sincerely,

Kevin C. Smith, CFA

Member & Chief Investment Officer

Tavi Costa

Member & Portfolio Manager

For more information including how to invest, please contact:

Marek Iwahashi

Client Service Associate

303-271-9997

Cassie Fischer

Client Service Associate

(303) 350-4000

Linda Carleu Smith, CPA

Member & COO

(303) 228-7371

© 2021 Crescat Capital LLC