What is a Value Stock

There is no shortage of investor definitions as to what constitutes a value stock. Most investors would agree that, at a minimum, value stocks must have a low Price to Earnings ratio and/or Price to Book ratio. Some investors consider additional metrics such as the Price / Sales ratio or even the PEG ratio, which is Price / Earnings divided by the expected earnings growth rate.

So what is low? One school of thought measures value relative to an absolute standard, such as a Price / Earnings ratio less than 10 or a Price / Book ratio less than 1. Other investors think of value as low P/E’s and P/B’s relative to the overall market, or relative to the company’s industry.

My preference is to look for value relative to a company’s own industry. Industries themselves have widely different “normal” price to earnings and price to book ratios. For example, if we look at software infrastructure companies (think Microsoft or Oracle) vs. integrated oil and gas companies (think Exxon Mobil or Chevron) we will see marked differences. Right now, the average price to earnings ratio for software infrastructure companies is over 30. For integrated oil and gas companies, the average P/E is around 10. There is a similar story for Price / Book. For software infrastructure companies, the average P/B is around 9; for integrated oil and gas companies, around 1. Quite a difference.

Another reason for using value relative to industry norms is that it circumvents the problem of selecting stocks from only one, or a few industries. For example, coal companies by traditional valuation measures are spectacularly cheap. If we did value across all stocks, then we may end up picking only coal companies. Not something we are after when trying to build a diversified value portfolio.

Value Stocks vs. Value Traps

The idea of a value stock is that it is somehow undervalued by the market and is “too cheap”. The approach value investors take is to spot these “too cheap” stocks before the market does, invest in them and then wait, the idea being that eventually the market will come around and see there is indeed “more value” in these value stocks, and as a result will bid the prices up. The value investor sells when the price rises to the level where the stock is no longer a value, and moves on to find new value stocks.

This all works great when it works. However, a lot of value stocks are cheap for a reason and, in fact, often only get cheaper. Such stocks are known as “value traps”. They appear cheap; however, they perform horribly in the market. No matter how cheap they are, it is astounding how much cheaper they seem to get.

Usually, at some point, something happens and investors realize that they were never really cheap at all. That something may be a devastating quarterly earnings announcement. Or an investigation into questionable accounting practices. Maybe the unexpected loss of a major customer or contract. The recall of the flagship product. The unexpected entrance of a well-financed new competitor into the company’s primary market. You name it. There is no shortage of “unexpected issues” that make cheap stocks even cheaper.

Being able to distinguish between true value stocks and value traps is what separates successful value investors from unsuccessful ones.

How Do We Find Value Stocks

We will begin the process of finding potential value stocks by creating and running a value screener and then doing additional research on the passing stocks to try to separate the true value stocks from the value traps.

So, the search for value begins with a screener specifically developed to hone in on the value criteria we are after. Using Stock Rover as our screening platform, we find that there are over 500 different metrics we can use to screen. Many of these metrics are useful for building value-oriented screeners.

I want to emphasize that there are many different ways to screen for value stocks. For the purposes of this article, I will select one approach that I think works well. However, there many roads that can lead to value.

Our screener will build on the notion of finding potentially inexpensive companies relative to their industry group, rather than using absolute measures, such as Price to Earnings under 10 or Price to Book less than 1. The latter approach generally results in too much concentration in specific sectors and industries, while ignoring many other promising sectors and industry that are deemed too expensive. This approach will help us build a more diversified sector portfolio, which in turn will result in better overall portfolio risk-adjusted performance.

Among the many metrics Stock Rover provides, we can select specific value metrics from Stock Rover that allow us hone in on stocks that are inexpensive relative to their industry. This will help us root out relative value companies within their industries.

So, what we need to do first is select our value metrics and build our screener. Then we run it and presto, a set of value candidates appear. Let’s do that.

Screening For Value

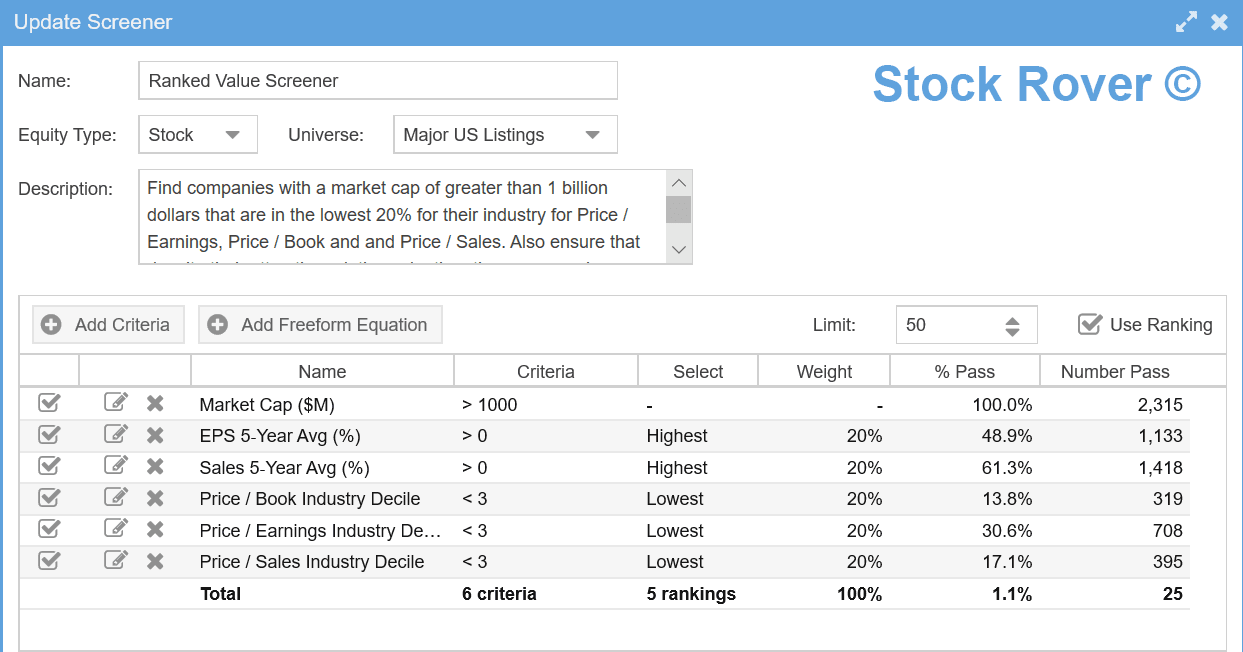

I have built a value screener in Stock Rover called the Ranked Value Screener that will not only find candidate value stocks, but will rank them on their relative “value-ness” The screenshot shown below from Stock Rover illustrates the criteria we are using to find our value stocks.

To describe this screener in English: we are screening the Major US Listings for stocks which includes companies on the NYSE and NASDAQ exchanges. We have set the criteria to select companies with at least a one billion dollar market cap.

Two other criteria are used that are not related to value; ensuring that over the last five years a company’s sales are growing and their earnings per share are also growing. This eliminates companies that are not thriving and are more likely to be value traps.

The actual value criteria are straightforward. To be considered a value candidate, a company must be in the cheapest 20% of its industry by Price to Book, Price to Earnings and Price to Sales.

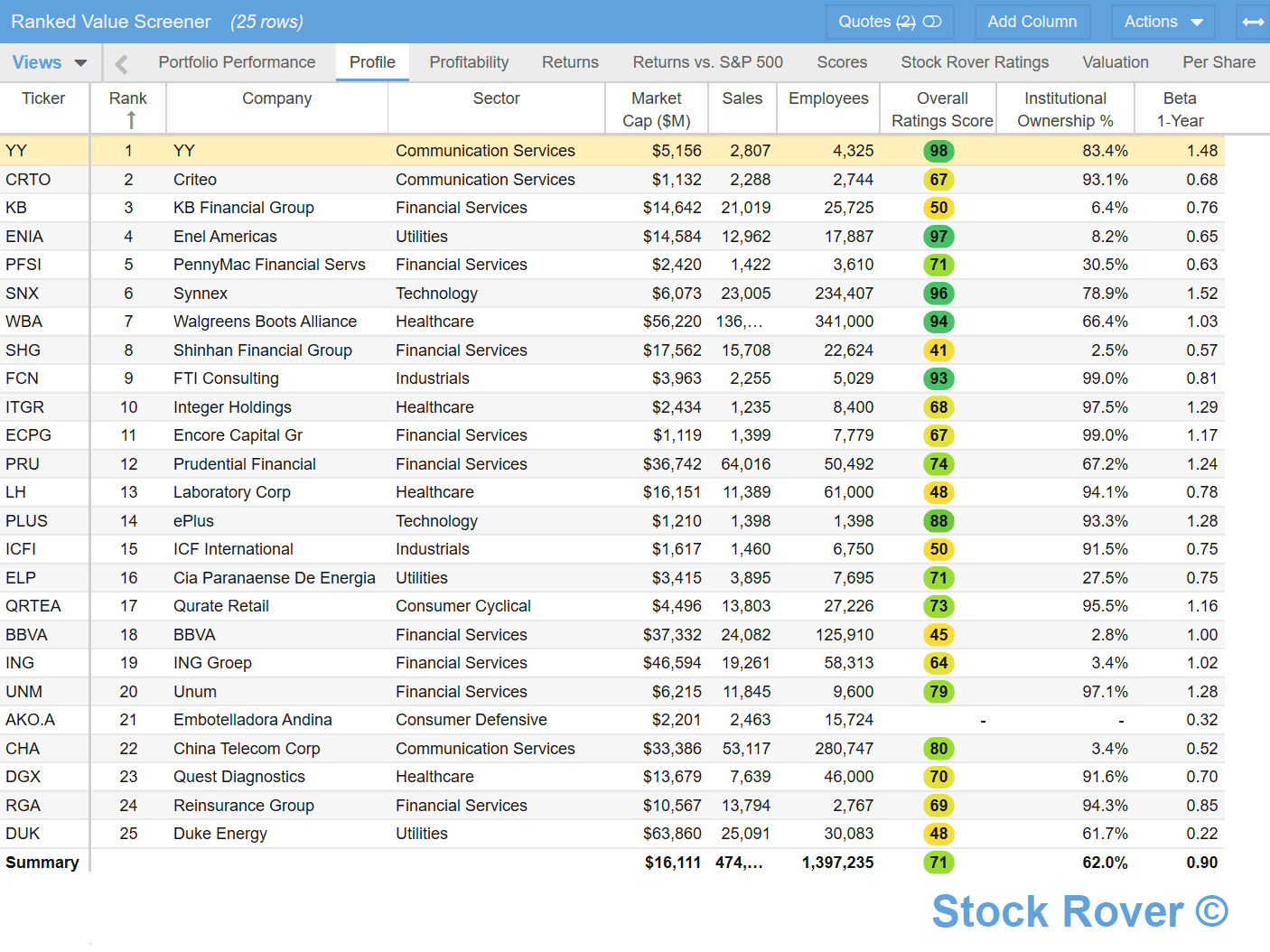

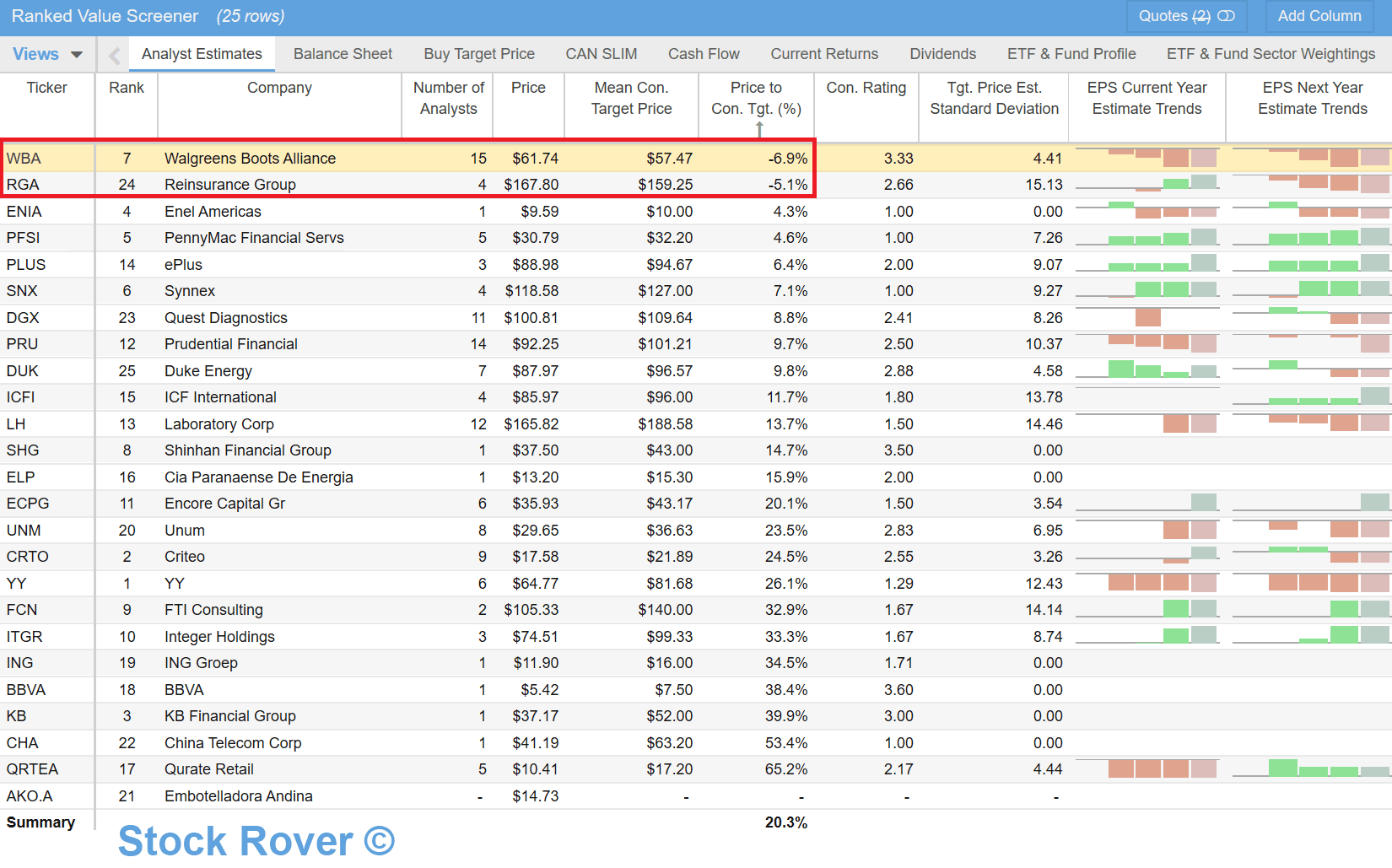

When we look at the over 2,300 candidate companies, only 25 or just over 1% pass the screening criteria. And these 25 will be our value candidates. Let’s take a look at who they are. They are displayed in the screenshot below.

As I mentioned previously, the screener will not only look for passing value stocks, it will also rank them. The rankings weight each of the five criteria we use to screen as 20% of the overall ranking score. This results in an ordering of our 25 candidates from highest to lowest value ranking score. We can see that the company YY ranked the highest (best value) of the passing companies and Duke Energy ranked the lowest.

We also see a nice dispersion across sectors. This is the positive byproduct of looking for value relative to industry norms rather than absolute values.

Digging Deeper

To this point, we have made major strides – we have located 25 promising value candidates from a population of over 2,300 stocks. However, screening is only the first step. We now need to ascertain whether these stocks are true value stocks or value traps. Unfortunately, this can only be determined by doing additional research, stock by stock.

And while the in-depth research required for each stock exceeds the scope of this article, I can show you how to use some of the neat comparative features of Stock Rover to cull the herd a bit. To do that, we use Stock Rover’s dynamic table to help us understand which stocks look good and which ones don’t.

Price Performance

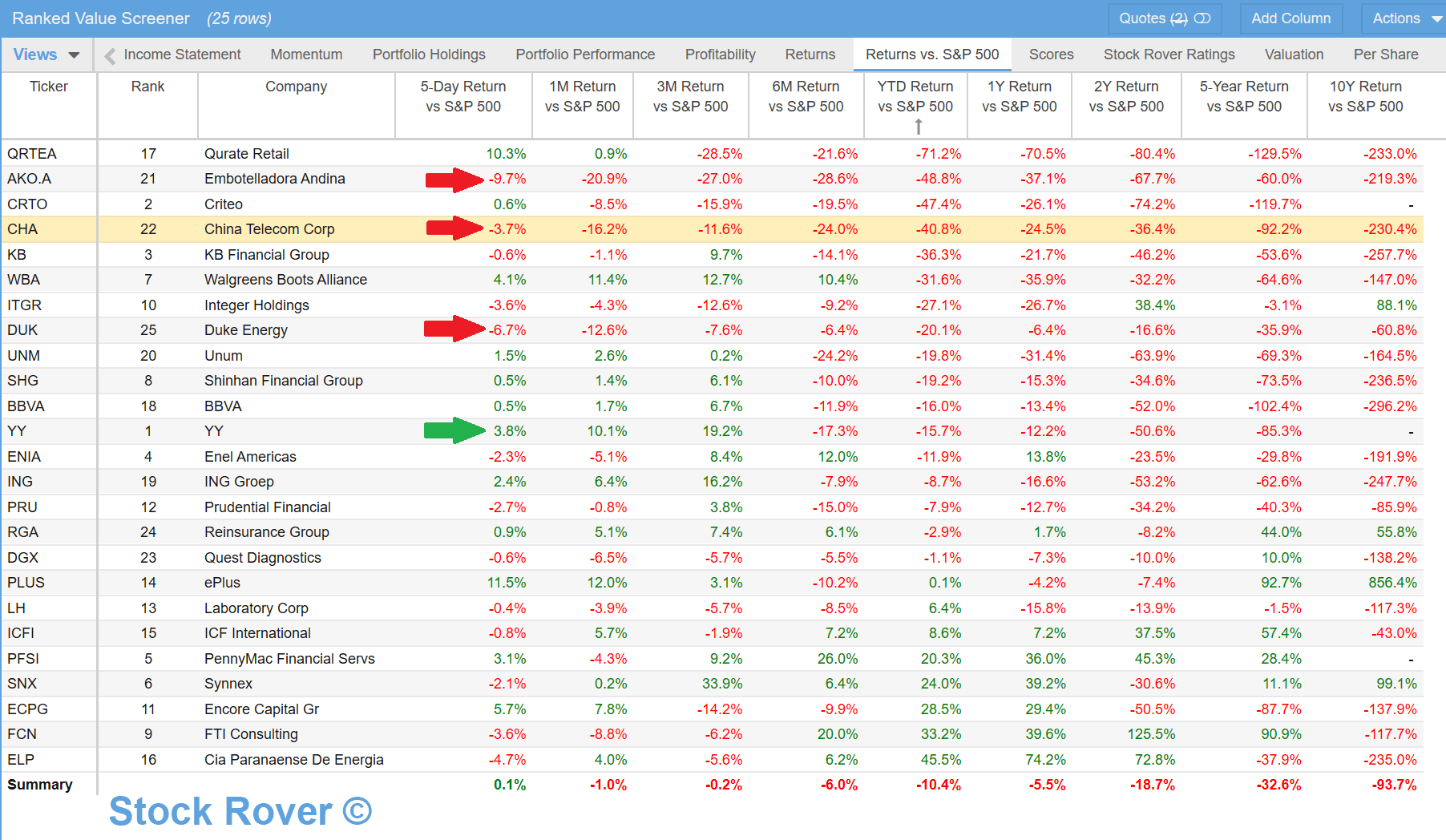

We begin by trying to separate true value stocks from value traps, those cheap stocks that keep getting cheaper. One of the first things I like to look at is the relative performance of the stock vs. the S&P 500 over a multitude of time periods, as shown below.

Here you see that three of the stocks, Embotelladora Andina (AKO.A), China Telecom Corp (CHA) and Duke Energy (DUK), indicated by red arrows, have never beaten the S&P 500 for any measured period, from 5 days to 10 years. So, unless you know something that is going to change the fate of each of these companies for the better in the future, I would classify these as value traps and avoid them.

On the other hand, the #1 ranked value stock YY, indicated by the green arrow, was also a value trap up until three months ago. Now it seems the market may be recognizing some true value in this stock and it could turn out to be a promising candidate.

Valuation

Given that we are looking at value vs. a company’s own industry, you can expect a wide variation in valuation. However, with that, there may be stocks that just seem too expensive on an absolute basis to qualify as value. The next table from Stock Rover shows some key valuation metrics for the stocks passing our valuation screener.

Here, by way of example, we will focus on ICF International (ICFI) which is in the Consulting Services Industry in the Industrial Sector. This industry as a whole has well above market multiples. Hence a P/E of 24.3 and an Enterprise Value to Free Cash Flow ratio of 47 may be a value in the industry, but on an absolute basis, it’s tough to call that value. So that would be another candidate to cull from our value herd.

Growth

Another key area where we can perform a quick check on our candidates is growth. The screener already ensures there has been growth in sales and earnings per share over the last five years. But what about recently? And what about the company’s prospects for the future? The following growth table from Stock Rover can shed some light on these issues.

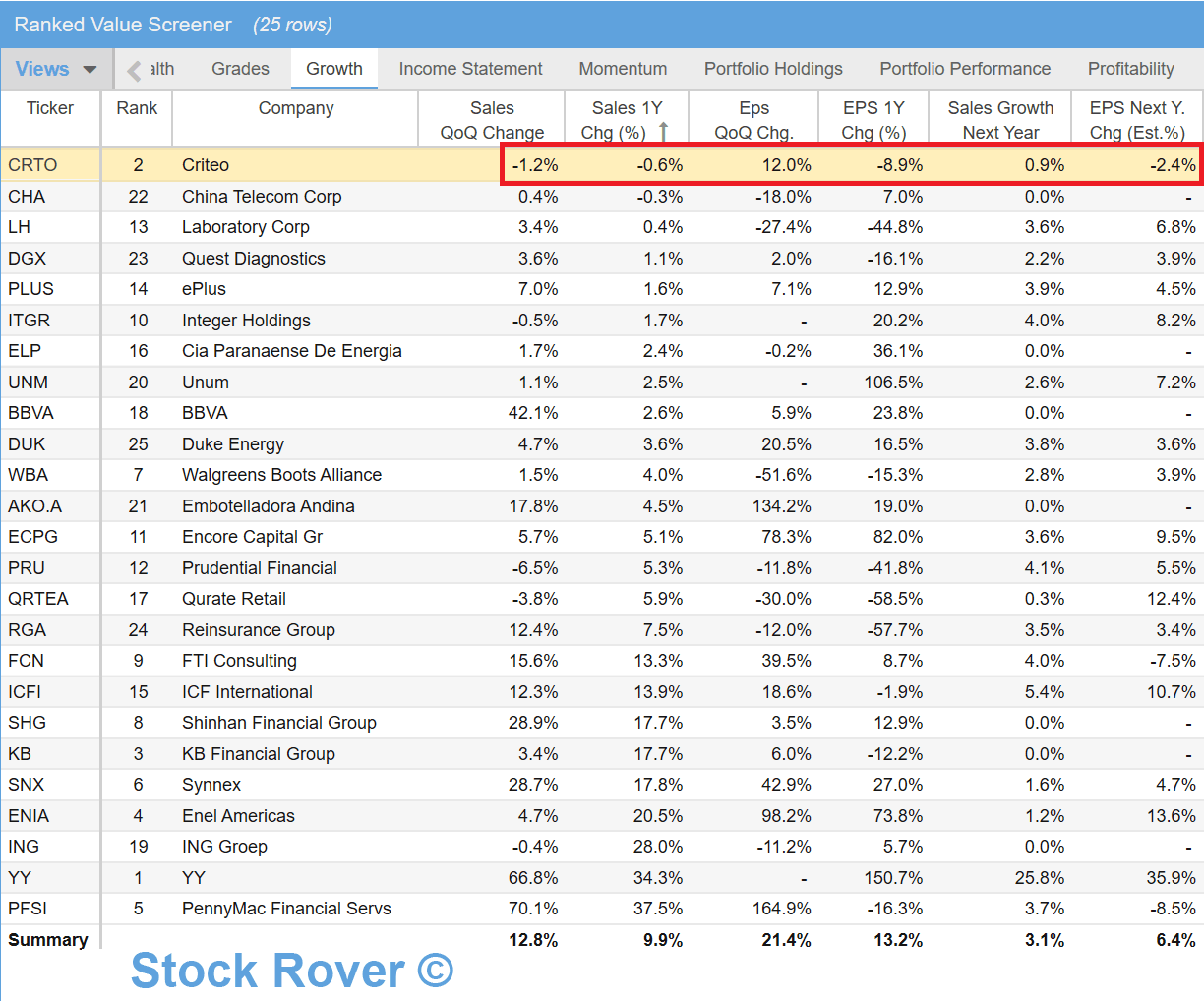

In this table we see that our #2 ranked stock Criteo (CRTO) is exhibiting some worrying signs on growth. Even though we are after value companies, we still want companies that are growing since growing companies are more likely to thrive in the future.

Criteo had a negative quarter to quarter change in sales in its most recent quarter, comparing it to the same quarter last year. Similarly, the one-year sales numbers have declined slightly from one year ago, as did the earnings. Finally, next year’s projected earnings are expected to decrease slightly as well. None of this is good. Additional research would need to be done to understand why. In any case, on the surface, this may indicate a value stock that we want to avoid.

Fair Value

Stock Rover performs extensive “Fair Value” calculations for all stocks in its coverage universe. We do this by performing a discounted cash flow analysis of a company to determine its intrinsic value. Then based on the current price of the stock vs. the intrinsic value and factoring in the sector and market multiples, we compute the overall fair value price and compare it to the current price.

Note: there is a blog post on the Stock Rover web site that describes fair value and margin of safety in detail.

The excess of the fair value price above the current price constitutes the margin of safety for the stock. And the bigger that number is, the better. Below is a screenshot of the Stock Rover Fair Value table for our ranked value screener.

Here we see that every value stock for which a fair value can be reliably computed has a positive margin of safety, except for BBVA, which has a negative 14% fair value. So according to Stock Rover’s discounted cash flow calculation, this value stock may actually be overpriced and hence is a candidate to be dropped from the herd.

Analysts

It is important to consider what the analysts think. First, we want to consider how many analysts follow each company. Bigger companies generally have more analysts following them. The stocks passing our value screener range from 1 analyst for YY to 25 analysts for Duke Energy. Quite a spread of coverage by the investment community.

Here I have highlighted two of our value candidates, Walgreens Boots Alliance (WBA) and Reinsurance Group (RGA), that both are above the consensus analysts target prices. This means the analysts think these stocks are expensive. Given that it is hard to find a group more optimistic about the futures of companies they follow than securities analysts, this is not a good thing.

Furthermore, if you look at the rightmost columns, you will see that the analyst estimates are becoming increasingly pessimistic about Walgreens and Reinsurance Group, based on the red estimate trends in the columns. This means that future earnings estimates are decreasing. Also not a good sign.

In the absence of countervailing information, these are two companies I would avoid.

Next Steps

We have covered a lot of ground. We built a custom screener aligned with our notions of value. Then using it, we found a population of 25 promising candidate value stocks. We then performed some initial analysis in five different key dimensions; Price Performance, Valuation, Growth, Fair Value and Analyst Ratings. Each of these examinations found stocks that “have issues” and should probably be dropped from consideration in our final value portfolio.

That still leaves quite a large number of stocks to dig deeper on. Unfortunately, the deep dive on each stock is beyond the scope of this article, but I can at least outline what those some of those steps are.

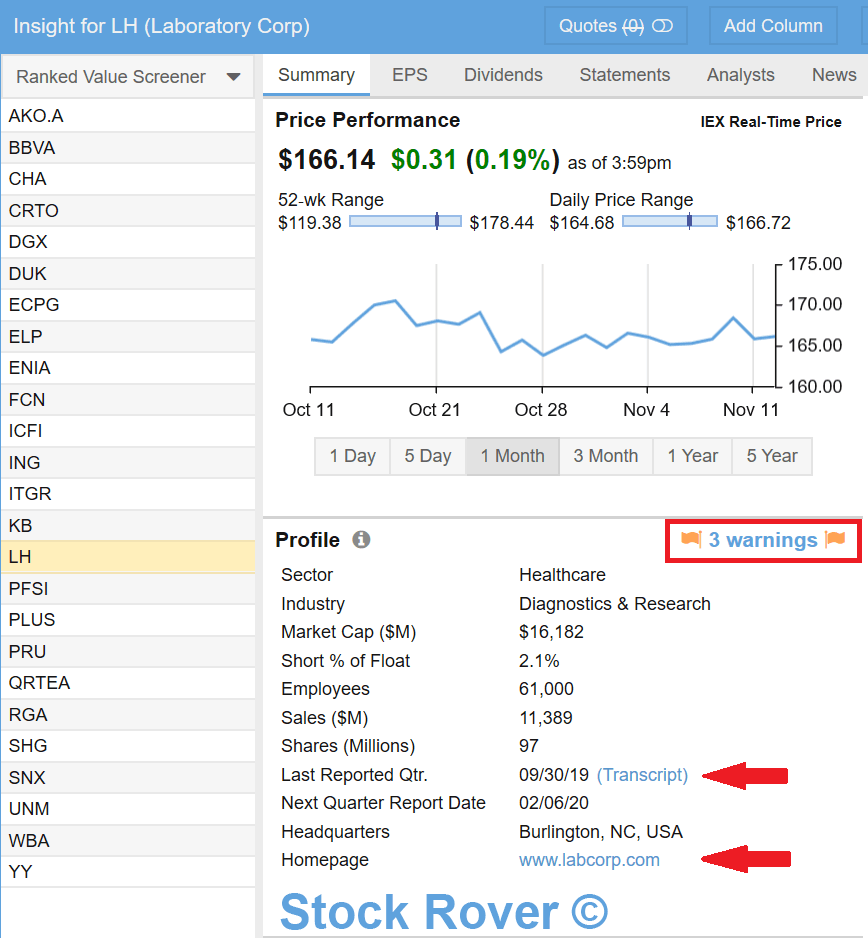

First, it is always best to get information directly from the horse’s mouth. For that I would read the earnings call transcripts, which you can get from a link in Stock Rover as highlighted below with the red arrow. The transcript allows you to see how the CEO and the management team describe the business and how they respond to analysts’ questions.

In addition to earnings call transcripts, the company’s homepage, which you can also link to from Stock Rover as shown above, will generally have an investor relations section where you can often get investor slide decks and company presentations. The quality and tone of the communication can often provide valuable hints on the culture and confidence that is elicited by the management team.

Notice in the screenshot above that Stock Rover has three investor warnings for the stock as indicated by the orange flags. Warnings make investors aware of certain characteristics of a given stock that makes it riskier and less desirable from an investment standpoint. There is a blog post on the Stock Rover web site that describes this valuable facility in detail. In any case, all warnings should be investigated to decide whether the issues raised are deal breakers or not.

Other key things to look at include the company’s financial statements, which are provided in great detail with lots of cool comparative features in Stock Rover.

A company’s 10K (annual) and 10Q (quarterly) filings are critical to examine. This is where the management team describes the nitty gritty of the company’s competitive, financial and operating performance, as well as its management compensation structure. You definitely want to avoid companies with greedy management.

Other valuable resources are independent analyst research reports. Often these can be obtained from the research pages of the brokerage website where you have your investment accounts. For example, both Fidelity and Charles Schwab provide a number of company research reports from a variety of analyst firms.

Conclusion

We have done a very quick A – Z tour of value investing. Hopefully, after reading this blog post, you will feel more confident in performing the steps involved in identifying and constructing a solid portfolio of quality value stocks.

One final word of caution. To be a good value investor requires patience. Value stocks can sit still for a long time before their intrinsic characteristics are fully appreciated by the general market. But if you have done your homework and have selected the right value stocks, your patience will be often be amply rewarded.

About the Author

Mr. Reisman is a Phi Beta Kappa and magna cum laude graduate of Brown University, where he earned degrees in mathematics and in economics. He has been involved with software design and engineering his entire career, leading teams that have created many commercially successful software products.

Finding investment research frustrating and tedious, Mr. Reisman founded Stock Rover with the goal of creating a product that investors would actually look forward to using and would make them better, more informed investors. The rapid growth of the Stock Rover community indicates Mr. Reisman wasn’t alone in his thoughts that investment research can be done better and more easily.