As the harsh winter gives way to early spring, I usually find myself excited not only for the upcoming outdoor activities, but also for the upcoming corporate proxy season (usually February to June), when shareholders can cast their votes on matters, including management compensation. A proxy statement1 may include information about the board of directors, members of various committees on the board, information about the auditor, and other corporate actions. But one of the most important sections of the proxy statement is the discussion about management compensation, particularly the section on bonuses, incentives, and option or stock grants. Sometimes, the structure of the compensation package and timing of the grant date will give us outsiders a signal about what the board of directors and management are expecting the business to do in the near, medium, and long term. While the strength of such signals will vary from case to case, I believe understanding the nuances of incentive programs, performance thresholds, vesting schedules, and change-of-control payments can give us a keyhole view into the future. Some signals are implicit, while others are explicit. Let me explain with a couple of examples. First up, the implicit kind.

Q1 2021 hedge fund letters, conferences and more

Implicit Signals

Most public companies around the world hand out options or performance share units (PSUs), restricted stock units (RSUs), or other forms of equity to their senior management as part of their incentive compensation. Best practice in handing out such equity would be to grant them after releasing Q4/annual earnings, when such information is likely to be priced into the stock. However, sometimes the board of directors will move the meeting and/or grant dates. Usually such changes are innocuous, but sometimes it can be a strong implicit signal of what is to come. One such signal, I believe, came from Evolution Gaming Group AB (OM:EVO) in early 2020. I recently wrote about this portfolio company, which you can find here.

EVO, the Swedish Live Casino provider, went public on the Stockholm exchange in March 2015. At the 2016 annual general meeting (AGM), the board decided to adopt an incentive program and issue warrants to the senior management team.

Companies more commonly issue stock options than stock warrants, which are typically included as a “sweetener” for an equity or debt issue. Like stock options, a stock warrant gives the holder the right to buy or sell stock at a set price on a particular date. Typically, warrants have a longer life (approximately ten years) than options, but in this case, EVO’s warrants to its employees, with only a three-year lifespan, are more like traditional stock options. Since the focus of this note is about signals rather than the type of equity compensation, let me take you back to our regularly scheduled program.

Here was the sequence of events from the 2016-2019 warrant program:

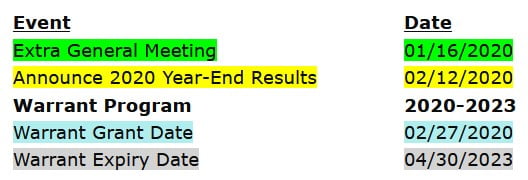

The board issued a new set of warrants in 2018:

So, the established sequence was: 1) release year-end financial results, 2) conduct AGM, and 3) grant warrants. However, when the company issued a new set of warrants in 2020, the sequence of events changed. The board of EVO conducted an extra general meeting on January 16, 2020, almost a month ahead of the year-end 2019 earnings release on February 12, 2020, and advanced the grant date by four months when it decided to issue warrants to senior management.

While some of the answers to questions around why the meeting date was moved or why the grant date was changed will never become public, the question helps us focus on some implicit signals.

We know that sticking with the established sequence would have meant holding an AGM in April 2020 and having a warrant grant date of July 1, 2020. Did the dates change because there were ongoing negotiations on a big transaction? On June 24, 2020, EVO announced a SEK 19.6 bill. acquisition of NetEnt AB (OM:NET B), which was one of its biggest competitors. While it may not have been possible to identify this potential acquisition, a deeper proxy analysis might have shed some light.

Within Live Casino (a fast growing vertical), EVO, through both organic and inorganic methods, has been growing at an even faster clip. Picking up the signal early in many other situations might not have mattered much. But in a market-dominant company within a fast-growing industry, it mattered a lot. EVO’s stock price doubled between 1/16/20 (the date of the 2020 EGM) and 6/23/20 (the eve of the NetEnt AB acquisition announcement). EVO has continued to perform well; as of this writing, EVO stock price is up 420% since 1/16/20.

********

Explicit Signals

Next up? The explicit kind of signal. As the Great Financial Crisis (GFC) was unraveling in 2008, the share price of many businesses declined precipitously without regard for their quality. One such victim was Copart, Inc. (CPRT), one of my portfolio companies. I have written about CPRT in the past, which you can find here and here. After hitting an all-time high of $12.11/share2 on June 23, 2008, the price of CPRT declined by almost 50% by early December 2008. That’s when Willis Johnson (founder, then CEO) and his son-in-law Jay Adair (then president, current CEO) came up with an innovative compensation program.

Since going public in 1994, CPRT has never been unprofitable. In fact, in 2007 and 2008, CPRT generated a return on capital of 14.9% and 17.4%, respectively. After buying back 8.8 mill. shares in 2007, management bought back another 20.3 mill. shares in 2008. In the company’s Q4 2008 earnings call, Jay Adair said, “So we’re excited that we’ve gone out and acquired additional stock and that we’re bringing this number down; and we think that’ll be great for long-term growth and improved EPS. And, of course, you know, we think we have a great future ahead of us in 2009.” While concerned about the overall market conditions, Jay was optimistic and confident about CPRT’s future. This was the background to the above-referenced innovative compensation program.

Also, according to the proxy filed in 2009, “Historically, we have not determined our compensation levels based on specific peer company benchmarks or analyses prepared by outside compensation consultant.” This is a peculiar arrangement for a public company, and one that is in line with how Warren Buffett likes to handle executive compensation. Most public companies these days, as a part of CYA, have a compensation consultant provide voluminous information on peer-group CEOs and CFOs and help design their compensation programs.

So, what was the compensation program? Both Willis Johnson and Jay Adair proposed that they get $1.00 per year in cash compensation and 2.0 mill. options each to buy CPRT shares, at an exercise price equal to the closing price on the date of grant, 20% of the options to vest on the first anniversary, and the balance on a monthly basis over the next 48 months. Willis Johnson and Jay Adair owned 11.5% and 1.6% of the outstanding shares at that time. According to Semler Brossy, an executive compensation consulting firm, such front-loaded equity incentive programs are not for every situation but are more commonly used by private equity firms, companies undergoing a turnaround or transformation, and companies undertaking a big-bet strategy. Twelve years after the GFC, such a compensation program may look unimpressive, but, during the depths of the crisis, for the founder/owners of the business to propose a compensation program that would not only increase their equity commitment but also save $19.7 mill. in cash compensation was a strong explicit signal. In fact, the compensation committee believed it demonstrated an extraordinary senior-management commitment to CPRT and its shareholders and offered strong evidence of management’s conviction concerning CPRT’s strategy and prospects. On April 14, 2009 (CPRT3 closed at $7.55), this program was approved.

In 2013, Jay Adair (CEO4) and Vincent Mitz (then president) proposed a similar program where Jay and Vincent would get options for 4.0 mill. and 3.0 mill. CPRT shares, respectively. At that time, Willis Johnson and Jay Adair owned 12.0% and 4.7% of the company, respectively. This program was approved on October 2, 2013 (CPRT closed at $16.58). While market conditions had improved considerably compared to during the GFC, I believe the proposal was another strong explicit signal.

Finally, on June 12, 2020, the compensation committee approved an option plan for Jay Adair5to acquire 1.0 mill. shares6 of CPRT at an exercise price of $85.04, with a vesting schedule similar to the previous programs. In addition, the committee included a performance condition such that, before any portion of the option can be exercised, the average closing price must exceed $191.34 for at least 20 consecutive trading days. This performance threshold is ~50% above where CPRT closed on 4/23/21. I believe it’s another strong explicit signal about long-term prospects for the business.

********

Charlie Munger said, “Never, ever, think about something else when you should be thinking about the power of incentives.” Proxy statements provide plenty of information about management teams’ motivations. When combined with business and financial analysis, proxy statement analysis can sometimes provide deep insight. I like the spring and proxy season.

Footnotes

1) In the US, companies file a separate SEC document on form DEF 14A, while in many other countries such information is incorporated into the annual report.

2) After adjusting for a two-for-one stock split in 2012 and another two-for-one stock split in 2017.

3) After adjusting for a two-for-one stock split in 2012 and another two-for-one stock split in 2017.

4) In early 2010, Willis Johnson handed over the reins of the company to Jay Adair and, to date, remains as chairman of the board.

5) Vincent Mitz retired from CPRT on Dec 31, 2018.

6) While the company still doesn’t use a compensation consultant on an annual basis, it used Compensia, a compensation consultant, in 2020 and previously when it promoted Jeff Liaw to president.