David Kim is a writer on Seeking Alpha and Better and Higher. David has a background in venture commercial banking and in public accounting.

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Few REITs are better known than Realty Income (O), a monthly dividend paying REIT and a member of the S&P 500. Per its 2016 10-K, Realty Income “is a member of S&P High Yield Dividend Aristocrats index for having increased its dividends every year for more than 20 consecutive years” through December 31, 2016.

Realty Income owns a diversified real estate portfolio. According to its recent September 30, 2017 10-Q, Realty Income owned 5,062 properties in 49 states and Puerto Rico, containing over 86.4 million leasable square feet (for context, that’s a tad shy of 2,000 acres; a football field is about 1.3 acres). It is the Company’s strategy primarily to own single-tenant properties, though it owns some multi-tenant properties.

Realty Income manages these properties across “47 activity segments,” of which 20 are separately reported in the most recent 2016 10-K. Most of Realty Income leases require the tenants to pay operating expenses, so rental revenue is the only component of the segment profit and loss the Company measures. The biggest single revenue generating segment is Drug stores. Incidentally, Walgreens (WBA) is the largest single tenant, accounting for 6.6% of rental revenues through September 30, 2017. The next largest segments are Convenience stores and Dollar stores. Among Realty’s top tenants by revenues (after Walgreens) include the likes of FedEx, LA Fitness, Dollar General, AMC Theatres, Walmart, CVS, and 7-Eleven.

This gives you some idea of the scale and nature of this diversified real estate company. Clearly, Realty Income is a big company. In this post, I won’t be analyzing the Realty Income’s payout ratio or surface analysis of its financial metrics. Instead, I want to look at Realty Income’s real estate investments and rental revenue disclosures over the past several years to figure out how effectively the Company is making real estate investments year to year. Realty Income is a real estate company, so just how good is its real estate investing record?

To frame the question differently, how many properties did Realty Income buy in 2014, and how profitable were they? And did Realty Income repeat the success in 2015, and again in 2016? How do you go about answering this question?

Now, we already know that Realty Income has been a successful and reliable REIT for quite a few years. But, growth and profitability always become more challenging once a company reaches a certain scale. So, I wanted to know, is Realty Income still making good acquisitions? After all, dividend safety ultimately reflects a Company’s operational excellence and the soundness of its business strategy.

Bottom-Up Approach: Buried In the Footnotes

To answer that question, we have to dig into and organize some footnote information. I’ve done the grunt work for you. Being the generous man that I am, I will share the data with you. But, after I give you the fish, I want to spend a moment to show you how to fish.

The table above highlights how much Realty Income spent during any given year to acquire new properties. In 2015 (light highlight), the Company spent $1.26 billion to purchase 286 properties. If you do the simple division, that comes to around $4.4 million purchase price per property. If you look at the same metric across the years, you can see a time series of both the scope of the investing activity and the cost per property across the years.

It was no surprise to me that the Company spent so little in 2009 to buy new properties. Everyone was scared and credit markets had frozen back then. There were some surprises for me, such as the relatively expensive 2011 acquisitions. I’ve added an asterisk to the 2011 to clarify the kinds of properties Realty Income bought that year, including quick-service restaurants and grocery stores. The amount of 2013 acquisitions was larger than usual because of the American Realty Capital Trust (ARCT) acquisition that year.

You can get these figures from the “Investment in Real Estate” footnote to the audited financial statements in 10-K. (Unless otherwise noted, all the tables and charts are author’s, and are based on information disclosed in 10-K’s.) For 2015 figures, below is an excerpt of 2015 10-K Footnote 4.

That’s good and fine, but apart from some interesting historical context, it doesn’t tell you a whole lot about whether Realty Income is making a good investment decision year to year. To get at that point, we flip over to management’s discussion of Rental Revenue. For the same 2015 reporting period, that disclosure looks like the following.

This discussion talks about current year’s acquisitions. But, to me the more interesting piece is the discussion of the previous year’s purchases and how much rent they generated last year and this year. (As a quick aside, the number of properties acquired in the rental revenue disclosure and in the footnote won’t tie out exactly; still, the management discussion encompasses the bulk of the new investments.)

So, in the 2015 10-K, you’ll learn that in 2014, Realty Income’s 479 properties purchased generated $65.9 million rent in 2014, but $99.3 rent million in 2015. That’s a 51% increase in one year! Now, how the heck did Realty Income do that? Realty Income magic, I suppose. Underneath that rent increase, I imagine there were numerous changes, including leasehold improvements and new lease contracts, but it’s still impressive.

The next bullet point describes existing store rent increases at yawn-inducing 1.3%. But, in the improvements to recently acquired properties, you can gain an insight into how Realty Income is generating growth.

Go through this exercise of finding prior year and current year rent for newly purchase properties, and you can compile the following table. I’ve compiled this data since 2009 for you.

Let’s briefly walk through this table. 2014 figures are highlighted. Again, those figures are from 2015 10-K’s Rental Revenue discussion. So, prior year refers to 2014 rent revenue. Current year refers to 2015 rent revenue, and so on for other years. For 2016, the data is for the first 9-months of the year only, because the data comes from 2017 Q3 10-Q (September 30, 2017).

Now things are getting more interesting! This table adds more color to the Property Investment disclosure we reviewed earlier.

As impressive as the 51% rent increase in 2014 properties are, Realty Income generated a whopping 252% increase to its 2010 properties in 2011. (2009 increase over prior year is less impressive because of the tiny base amount. Again, harder to grow at large scale; you can turn a small boat quickly, but not an aircraft carrier.)

So, has Realty lost its property investment touch in recent years at operating at a large scale? Not at all! 2015 and 2016 acquisitions show a healthy year over year rent increase from acquired properties.

Now, my guess is that once the walls are re-painted, and parking lots re-paved, and the tenant lease re-negotiated, then it’s the low single-digit annual rent increase thereafter. So, there is a dimension of one-off gain. But, this ability to take a subprime property one year, and then polish it up to a prime (relatively speaking)… that ability is pretty impressive.

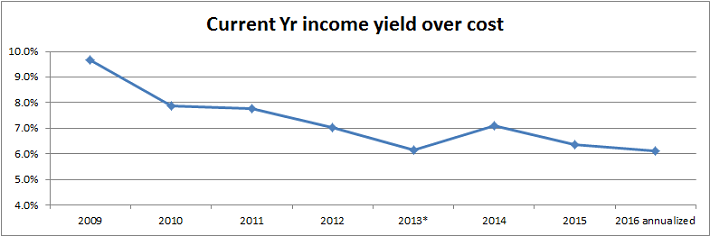

We can do one better. Take the current year rental income. Then, divide by the aggregate cost of the purchases from the first table, and you get a proxy for rental income yield of recently purchased properties over the years.

That table is shown below. Again, don’t be misled by the high 2009 yield; the base was so low. You might infer that 2010 – 2011 yields are higher than mean, because those represent purchases when there were still many bargains to be found in the real estate market post housing crisis. In that light, 2014 yield is more impressive. Overall, we are seeing yields in excess of 6% throughout.

We’ve gleaned important information from a seemingly minor piece of detail in the 10-K filings. For example, we’ve been able to see that Realty Income team buys up properties and is able to yield 6% or higher rental income on cost, and do so consistently over the years. If you visualize the table above, you get the following rent income yield over the years. (Lest you be disappointed by the 6% yield, let me remind you that this is but one snapshot of a real estate business. For instance, it doesn’t reflect how such improved properties may sell above or below market premiums down the road. This is a limited, but useful analysis for prior year and current year rental income comparison.)

The previous discussion focused on analyzing a subset of newly acquired properties of the Company. It was a bottom-up analysis. To add further context, I’d like to review Realty Income’s market cap growth and also compare the Company’s dividend yield against the 10-year Treasury yield. It is my hope that doing so will shed a top-down perspective useful to investors.

Below, I’ve compiled Realty Income’s dividend yields over the past few years (using dates disclosed in 10-K). Then, I compared those yields against the 10-year Treasury yield of the same date. Take the difference, and you have a yield spread table. If you make the simplifying assumption of viewing Realty Income’s dividends like a monthly bond interest income, then this spread represents a risk premium investors have assigned to Realty Income relative to a risk-free instrument. (And yes, you could have selected a 15-year treasury for the same task. Personally, I felt that the 10-year maturity horizon was a reasonable benchmark.)

Graphing the spreads, then you get the following chart. For reference, I’ve added a linear trend line through the data.

The chart represents the risk premium assigned to Realty Income’s dividends over 10-year Treasuries. It is interesting, but not surprising, to see that this risk premium has come down over the years since the housing crisis. As of a recent quarter-end, the premium is around 2%.

At this point, it’s worth observing that 10-year Treasury yield has been on the rise in 2018. As recently as September 30, 2017, the Treasury yield was 2.33% (see table). The 10-year Treasury yield started 2018 at 2.46%. As of February 2, 2018, the yield stood at 2.84% (that’s a 21.9% increase over the September 30, 2017 yield).

For an income producing asset like a bond (and for bond proxies like utilities, high dividend paying stocks, and REITs), a rising interest rate exerts a downward pressure on asset valuation. Think of it this way. Recently, the market was demanding about a 2% premium over 10-year Treasury for Realty Income dividends. When the Treasury yield was only 2%, then a 4% dividend yield was “acceptable.” Now, when the Treasury yield is closer to 3%, the Company dividend yield had better increase to 5% to keep pace. Further, if the economy falters – for instance, market fears rise as inflation heats up – then the market’s risk premium demand might increase. A 3% premium over 10-year Treasury would require a 6% dividend yield.

Either way, Realty Income likely will have to generate a higher dividend yield than it is today. If the Company can’t do that overnight, then the stock price will have to decline in order to generate the same yield on cost for investors. Also, the above analysis of recent acquisitions and rent yields from those acquisitions (recently maxing out at around 6%), represents an upper limit on how much internal yield Realty Income could generate in the short run. Intuitively, the scenario feels like a squeezing of Realty Income’s operations.

Of course, I’m jumping ahead of the current realities a little. But, I think there is something to the higher interest rates as a potential concern. Simple bond math aside, real estate businesses will find cheap sources of capital increasingly scarce.

There is one last piece of historical data I’d like to leave you with. The table below shows Realty Income’s market cap in $ billions since June 30, 2008. Since real growth is exponential, we take a natural logarithm of the market cap.

This graph of market cap shows how Realty Income’s market cap compares to its own long-term trend line. I pause to say that I’m NOT a chart guy. After all, a Company isn’t undervalued because the chart shows a dip below a long-term trend line. Instead, a Company is undervalued when the current stock market price of a company’s stock is trading below its intrinsic value. Without an understanding of the intrinsic value of a Company, the stock chart is meaningless. But, for us, having gone through an analysis of how the Company generates growth, the recent market price depression is interesting.

Final Thoughts

Realty Income owns a diversified real estate portfolio of over 5,000 properties, and is well-known as the monthly dividend Company. Realty Income’s biggest tenants include blue chip companies like Walgreens, CVS, FedEx, and Walmart. The Company’s key segments include recession resistant drug stores, convenience stores, and dollar stores, among others.

In this post, we took a bottom-up look at the Company’s recent property purchase activity and reviewed how profitable those investments become under Realty Income’s management. We took a shot at taking that data to compute a yield on cost of the invested properties and found that Realty Income continues to generate impressive returns in the form of higher rent revenues on newly acquired properties. We also took a top-down look at the Company’s dividend yield and how that compares to 10-year Treasury yields over time. In doing so, we saw a trend in the risk premium that investors seemed to demand.

From this analysis, my general takeaway is that Realty Income continues to be a well-run company with strong internal fundamentals. However, the current rising interest rate environment represents a strong headwind for any income producing asset. In other words, be sure your investments are made with a long-term view.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

Article by David Kim, Sure Dividend

The world’s best investors have trounced the market decade-after-decade. The course Invest Like The Best uses actionable cases studies from investors like Warren Buffett, Peter Lynch, Seth Klarman (and more) to teach you the tools and techniques of super investors. Click here to enroll today and save $100.