Motiwala Capital annual letter to investors for the year ended December 31, 2017.

Dear Investors,

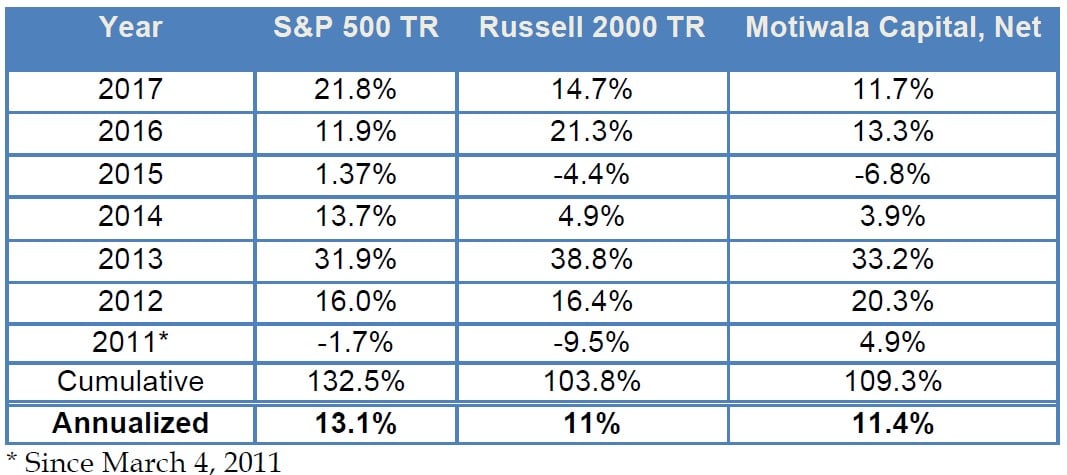

During 2017, global equity markets rose non-stop and relentlessly. The US markets did not experience a single negative month. Large caps led the way with the S&P 500 logging a total return of 21.8%. Small caps and value indices logged much lower returns compared to the S&P 500. Motiwala Capital accounts on an aggregate basis returned 11.7% after fees and expenses.

2017 Performance

When the entire market is rising, it is difficult to take credit for stock picking. That said I am pleased that only a few mistakes were made. The numbers in brackets that follow the company names are the contribution to the portfolio performance. The two positions that detracted from performance were New York REIT (-0.9%) and Hennessy Advisors (-0.4%). Positions that contributed positively to performance included Fortress Investment Group (1.1%), Google (0.85%), Cision (0.85%), Hostess Brands (0.75%), AmerisourceBergen (0.5%), Dollar General (0.5%), Dollar Tree (0.5%), Linamar (0.8%), Retail Holdings (0.6%), Vistra Energy (0.6%), LyondellBasell (0.5%), Vanguard Financials ETF (0.5%) and Japanese stocks (1.7%).

Portfolio Composition

Our portfolios are divided into three buckets. The ‘Generals’ are undervalued equities that require either earnings improvement and/or multiple expansion to be profitable. The second bucket is Special situations where a specific corporate event could unlock value. Since Q3 2017, deep value Japanese stocks comprise the third bucket of the portfolio. The size of each bucket may vary depending on the relative attractiveness of the potential investments. In the Generals bucket, the portfolio held 24 positions at the end of the year.

Portfolio Activity since July 2017

Positions sold:

During the second half of 2017, we sold two profitable positions.

ebay (EBAY) was sold as shares appreciated to my target valuation. In early 2016, EBAY was

trading in the $22-$23 range. Here is the snippet from my 2016 letter.

Ebay (EBAY) operates the well-known ecommerce platform along with classifieds and the StubHub event ticket platform. In early 2016, Ebay shares were under pressure possibly due to slowing growth in its core business and increasing competition from Amazon and other platforms. At purchase, Ebay had a strong net cash balance sheet and generated excellent free cash flow and available at a low valuation. Fast forward two years later and the stock has doubled. The company has performed reasonably but their profits have not doubled. The low valuation of early 2016 has been corrected and investors who bought when the shares were out of favor have been rewarded. I was likely conservative in my valuation and sold along the way and hence did not capture the full upside.

Syntel (SYNT) is an Information technology and Knowledge process outsourcing service provider. SYNT shares had been under pressure since purchase as the company warned of tougher business conditions and kept reducing guidance. Luckily I had purchased a small initial position and I added to the position on continued decline in the share price. At one point the stock was down 40% to $16 from the initial purchase price of $27 (dividend adjusted). Despite the decline in revenues and profits, the company was quite profitable, produced ample free cash flow and the valuation was attractive. From the summer of 2017, the stock reversed course and hit $25+ and I sold the position. If the business resumes growth, my sale may prove to be conservative. However, given that the turnaround was still in the works and the stock had given us a decent return it felt prudent to sell the stock.

Positions reduced:

I trimmed several positions as prices increased thus reducing the gap between price and value. These included Vistra Energy, Cision, Hill International and Dollar General.

New Positions

Dave and Busters (PLAY) owns and operates entertainment and dining venues in N. America. Their mega sized restaurants offer large assortment of video games as well as live sports viewing. This sets them apart from other restaurants and their margins are best in class. PLAY has grown rapidly since 2011 doubling its store base to 105 stores. It has generated cash-on-cash returns of 52% since 2011 and its growth has been self-funded. The company has a solid balance sheet and generates excellent cash flows. Most of this cash flow has been re-invested in its growth. PLAY intends to open 10+ stores annually. Recently, it has been repurchasing shares. Shares began a sharp decline in the summer of 2017 as same store sales first cooled off and then turned negative. While this is a concern, it does not seem that the business is broken. The valuation of 8x enterprise value to operating cash flow was attractive relative to its trading history as well as its potential growth.

Cision (CISN) provides public relations software, media distribution and media intelligence services via a cloud-based platform. CISN has a short operating history and came public via a reverse merger with a shell company (aka SPAC). While CISN has a debt heavy balance sheet, it produces solid free cash flow and should be able to reduce debt over the next 2-3 years. CISN has very little coverage and if it keeps executing, it should attract analyst and investor attention.

Positions added:

I added to the following existing holdings.

Hostess Brands after the stock declined following the resignation of their COO and reporting weaker than expected Q3 results.

Dollar Tree post its sharp decline after Amazon’s announcement of Whole Foods acquisition. I felt confident that the dollar stores category would not be an easy segment for Amazon to compete in.

McKesson was added at a price higher than the original purchase, as shares remained undervalued.

AmerisourceBergen and CVS were also added as share prices declined despite reasonable operating performance.

Japan Deep Value

As I mentioned in the semi-annual letter, I have managed a personal account investing in deep value stocks in Japan since the summer of 2013. I was intrigued by Ben Graham’s deep value strategy but did not know where to find such bargains. A friend pointed me in the direction of Japan. Over a four and half year period, this strategy has produced annual returns in excess of 20%. In August 2017, I started investing 10% in these opportunities. While it is very early, the initial results have been good. The combined Japan portfolio contributed 1.7% to the full year portfolio performance. I intend to increase the investment in the ‘Japan basket’.

I am employing two strategies in Japan.

(1) Net Nets: A Net- Net is term coined by Ben Graham and refers to a stock that is trading at a discount to its net current asset value or NCAV. NCAV is simply total current assets – total liabilities. When a company’s market cap is below NCAV, it is considered a net-net. It is an extreme level of cheapness as no value is assigned to non-current assets but all liabilities are subtracted. Graham advocated a diversified net-net portfolio. Several studies have shown that this investing strategy has exhibited excellent investment returns. I start with screening to find candidate investments and then conduct further due diligence on the historical financials and valuation ranges.

Example Net Net (all numbers in Yen)

Nichiwa Sangyo (TSE:2055) is packaged foods and meats company in Japan. It sported a market cap of 6.3 Billion, book value 17 Billion, total current assets 21.7 Billion, total liabilities 10.8 Billion. NCAV = Total current assets – Total liabilities = 21.7 – 10.8 = 10.9 Billion. P / NCAV = 6.3 / 10.9 = ~0.6. P/B = 0.37. Nichiwag Sango trades at a 40% discount to NCAV while being profitable, paying a dividend and having excess cash on its balance sheet. It meets my criteria for a net-net holding.

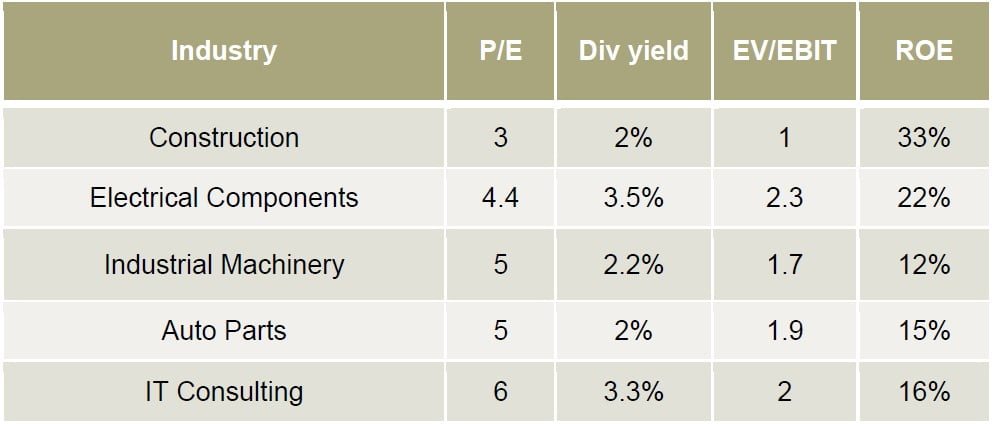

(2) Low multiple stocks: The second strategy I employ is buying companies that trade at very low valuation multiples. I shortlist companies with history of operating profit and strong balance sheets. Companies that meet majority of my criteria are selected for addition to the portfolio.

Sample low multiple stocks

The Japan strategy is now open to current and potential clients as a separate strategy. Please contact me if you have an interest.

US Tax Reform

In December 2017, tax reform bill was passed in the US. Major highlight was the reduction in the federal corporate tax rate from 35% to 21% and a lower tax rate to repatriate overseas profits. The reduced tax rate should boost corporate profit after tax and cash flows and encourage investment.

Thank you for the opportunity to manage portion of your assets. I will continue to work hard to protect and grow your capital in 2018 and beyond.

Sincerely,

Adib Motiwala

Portfolio Manager

See the full PDF below.

{kind=link}