Logica Capital commentary for the month ended August 31, 2021.

Q2 2021 hedge fund letters, conferences and more

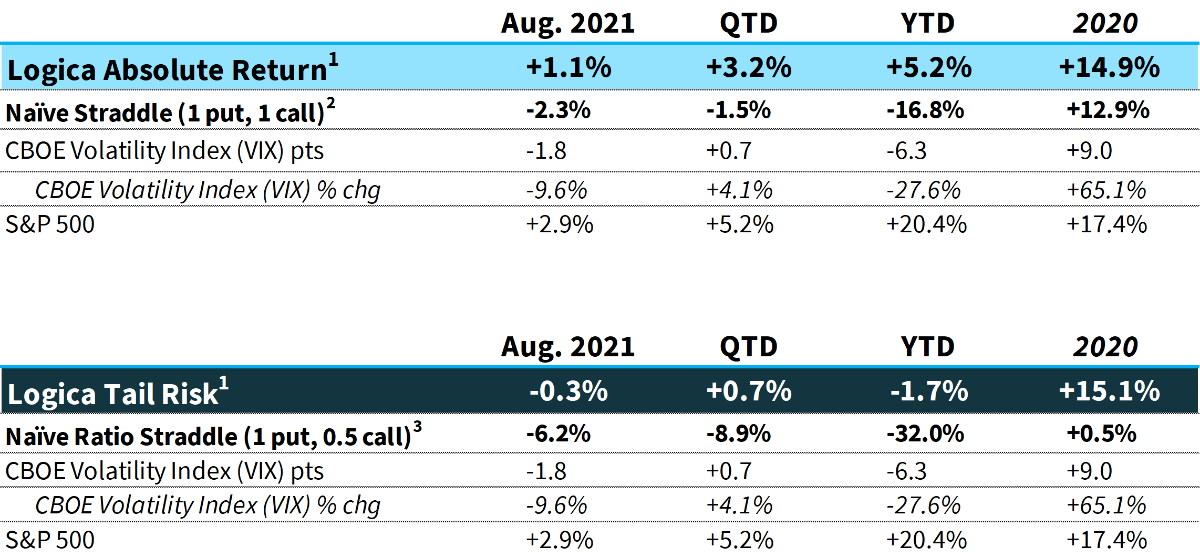

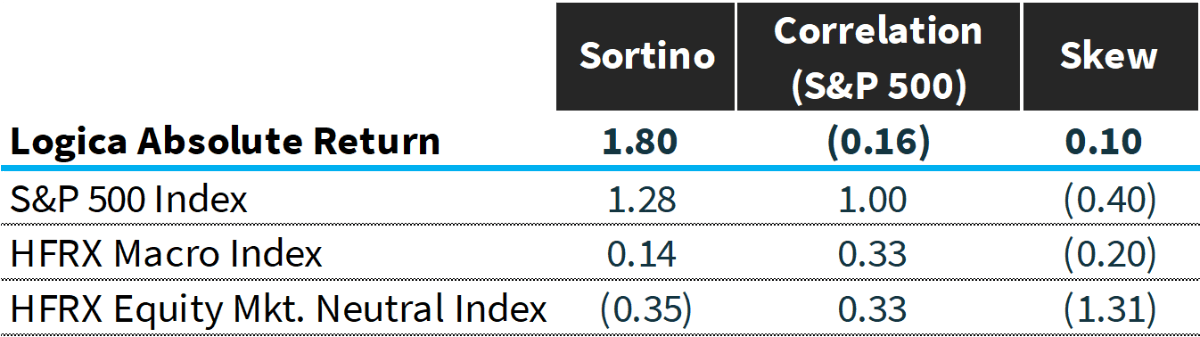

Logica Absolute Return (LAR) – Upside/Downside Convexity – No Correlation

- Tactical/dynamic balanced Put/Call allocation – Straddle

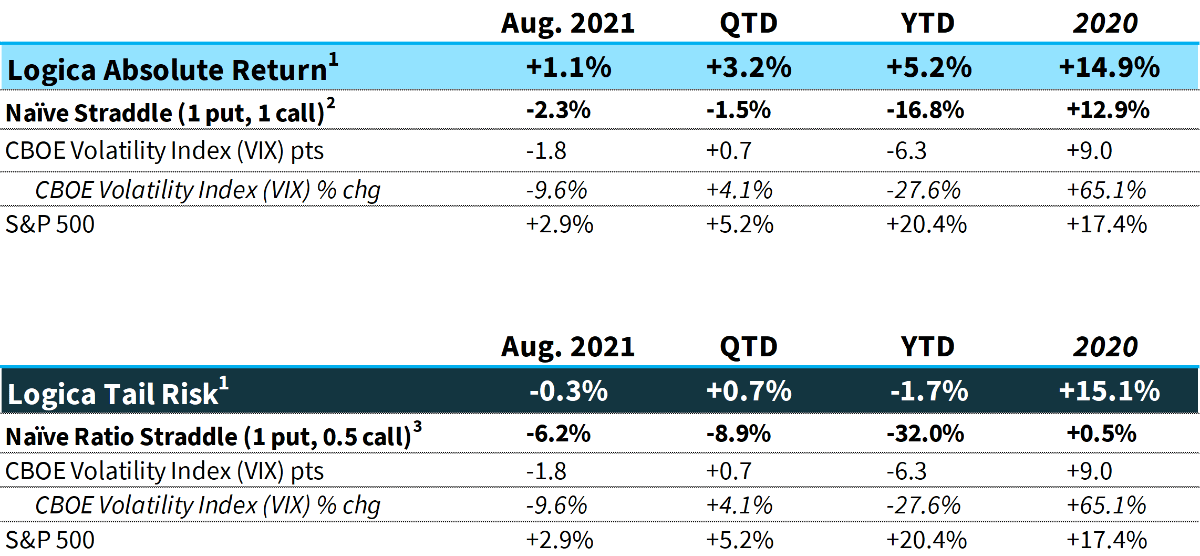

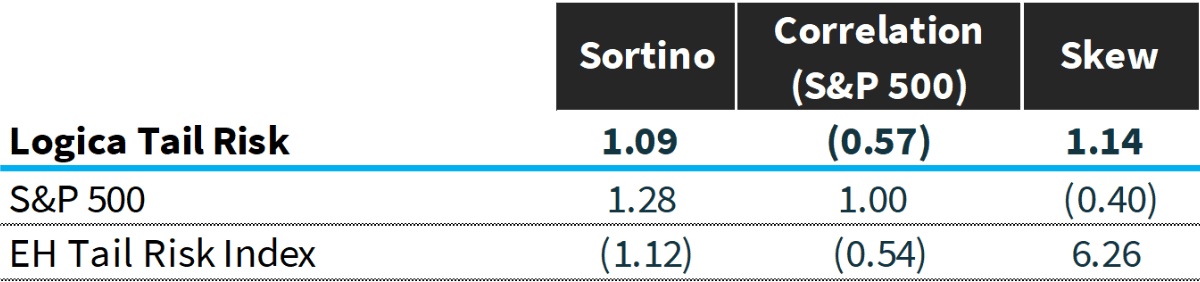

Logica Tail Risk (LTR) – Max Downside Convexity – Strong Negative Correlation

- Tactical/dynamic downside tilted Put/Call allocation – Ratio Straddle

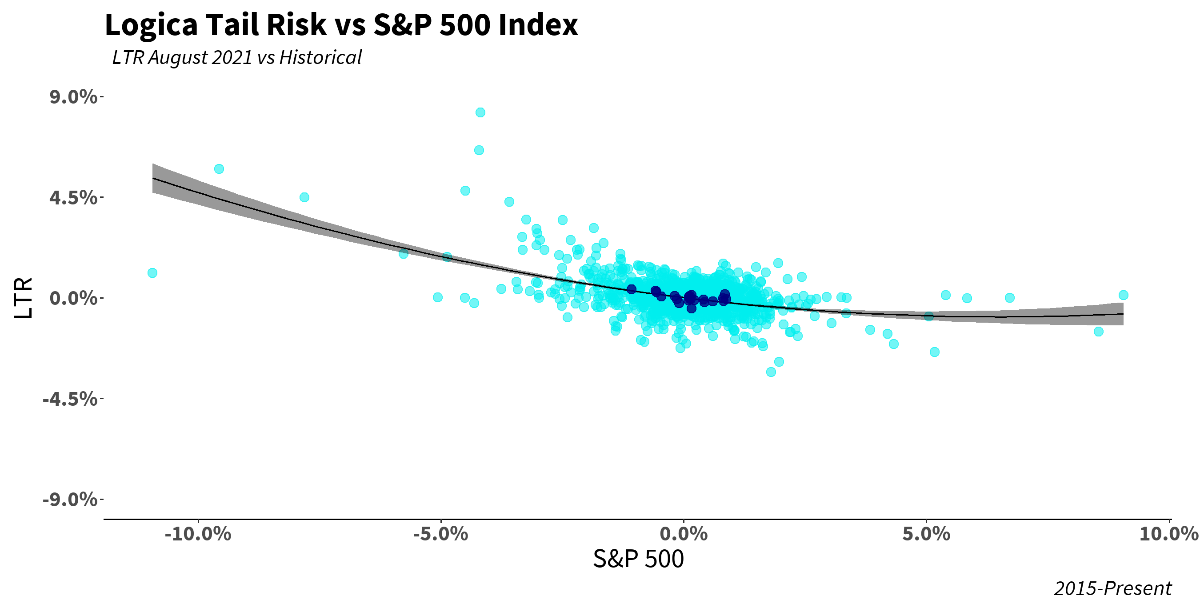

Summary: Equity markets continue to rise while realized/implied volatility remained somewhat dormant, but still at interestingly elevated levels relative to historical phases of similar bullishness.

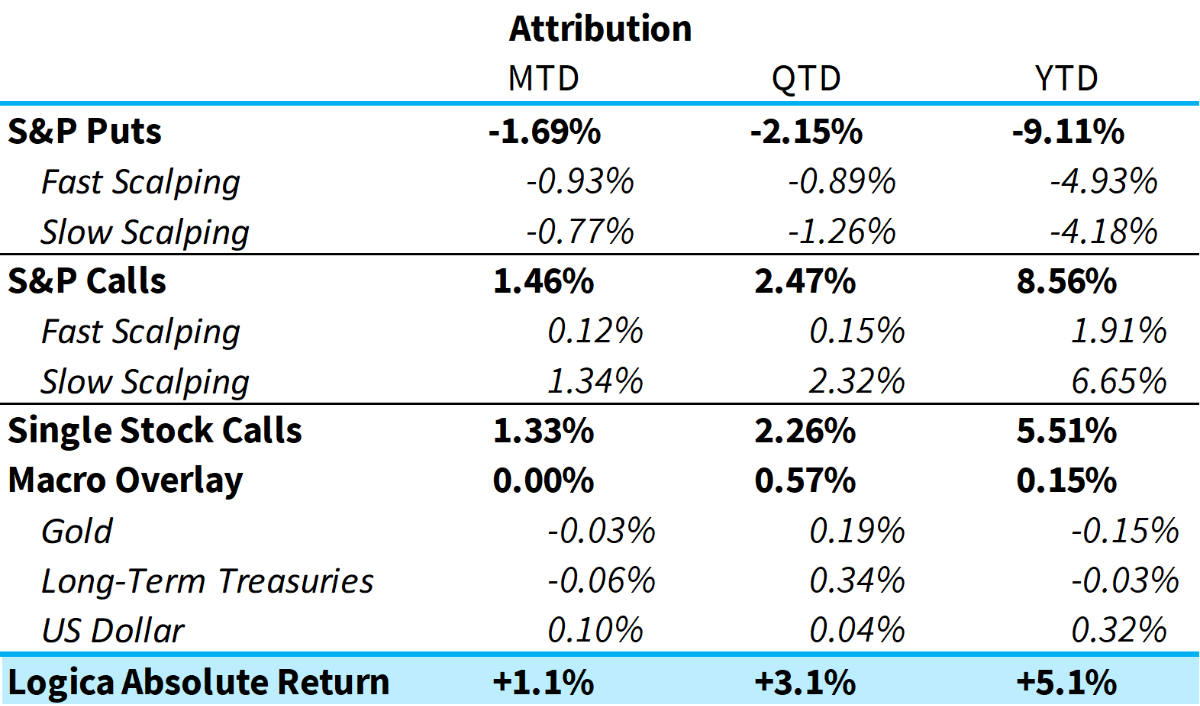

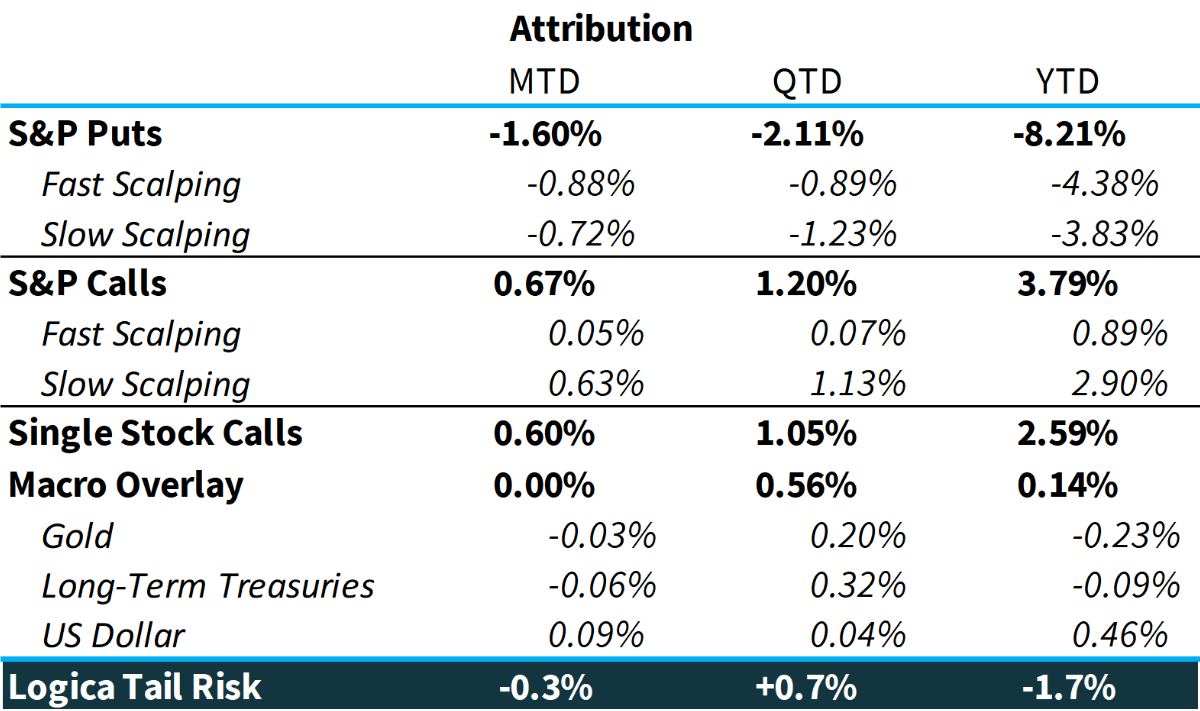

1 Returns are Gross of fees. LAR Fund +0.97% (net), LTR Fund -0.46% for August 2021

2 Naïve Straddle Return: a 1.5 month out, S&P 500 at-the-money put and call bought on the final trading day of prior month and sold on the final trading day of current month. This return on premium is divided by a factor of 6 to be comparable to Logica’s typical AUM-to-premium ratio.

3 Naïve Ratio Straddle Return: a 1.5 month out, S&P 500 at-the-money put and at-the-money call (divided by 2) bought on the final trading day of prior month and sold on the final trading day of current month. This return on premium is divided by a factor of 6 to be comparable to Logica’s typical AUM-to-premium ratio.

“Hard times create strong men, strong men create good times, good times create weak men, and weak men create hard times.” -Michael Hopf

Commentary & Portfolio Return Attribution

August 2021 may have set a record for our subjective (and recency-biased) “boring” factor. Boring markets are music to the ears of most portfolios, given the proclivity of a large portion of their investments tending toward short volatility and/or short convexity.

But “boring” isn’t very quantitative and given our proclivity toward quantifying and categorizing, let’s have a go at some better descriptors.

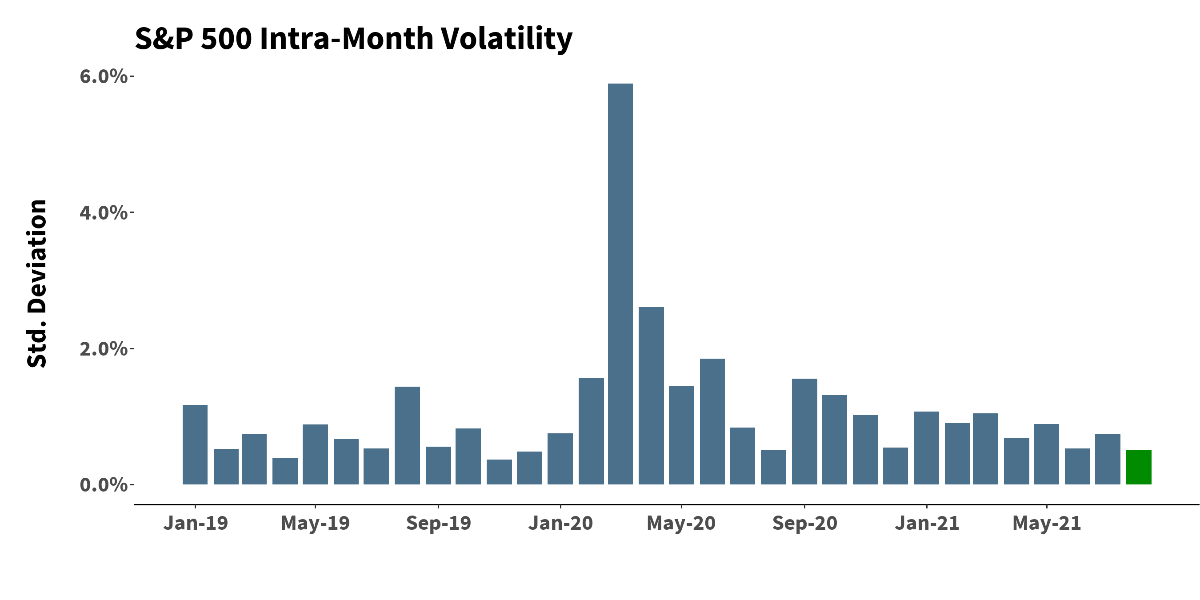

We’d have to go back to late 2019 to find intra-month realized volatility on the S&P500 (defined here as standard deviation of returns) as low as it was in August.

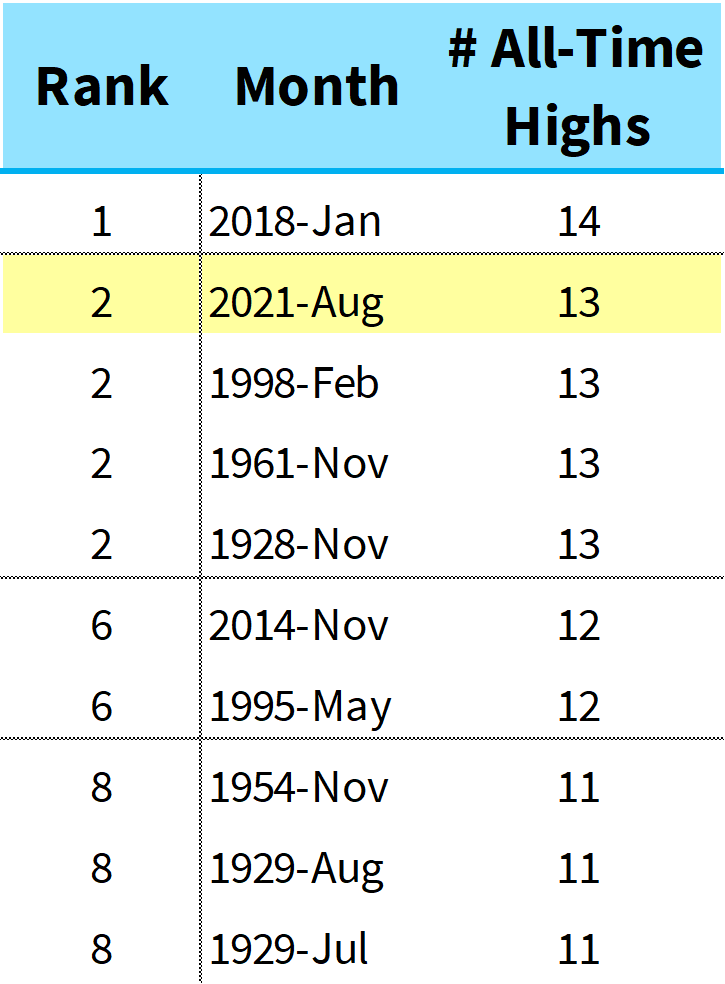

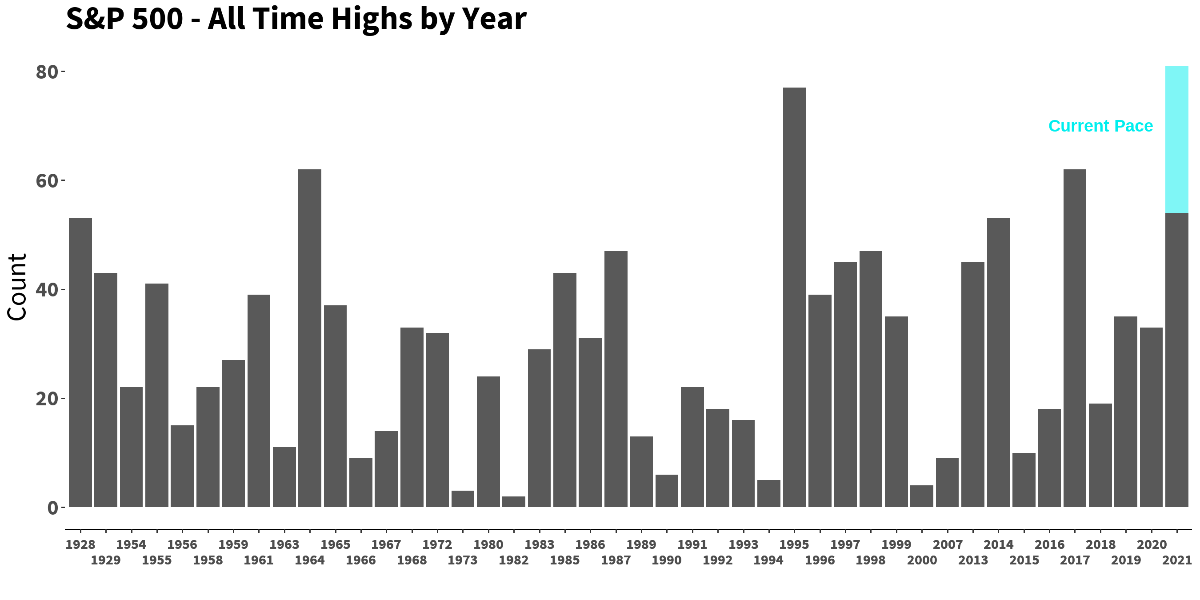

Quite incredibly, we find that the number of all-time highs (“ATH”s) in August (13!) narrowly missed tying the record for most ATHs ever achieved in a calendar month (14):

Speaking of records, 2021 as a whole is on a similar pace. The number of ATH closing prices already seen through the end of August puts us on pace to realize the most ever in a calendar year. If that data point hasn’t rung the bell quite as loudly as it should’ve, let’s repeat that once more: the all-time highs of 2021, in the midst of a global pandemic, are outpacing all prior years on record.

So what does this mean for us? Well – it’s interesting in that it provides context, and it’s some more data for our models to chew on. But frankly, on the whole, “my dear, we don’t give a damn.” Or more pointedly, our strategies don’t. Our Absolute Return strategy is designed to thrive in nearly every possible environment (or market path), and while our Tail Risk strategy might be less enamored with the summer doldrums and constant new highs, it is designed with a similar goal, and thus the potential bleed from being purely long vol – and strongly negatively correlated to the S&P 500 – has been largely contained thus far.

What is a little more pertinent to us is the fact that implied volatilities across moneyness/term structure remain well above levels seen in 2014-2017, when the S&P 500 had a generally similar return profile and realized volatility as 2021. While we don’t spend much time writing pieces about the structural factors that may be contributing to this, we have previously touched on the seeming shift in volatility regime that occurred in February 2018, post-Volpocalypse, and it continues to be of heightened relevance. Obviously, strategies that are long volatility should benefit from a higher “floor” in one simple sense: there’s less room to go down. But it does create a situation for fewer “value” investments.

The crux of the issue is twofold: have structural factors created a new regime with a higher implied volatility floor? And, does this higher floor actually portend an increase in reflexivity (we could get into the weeds on this, but this broadly means that there’s equal potential for much larger moves to the upside for volatility [market downside], even if starting from a higher floor).

At Logica, our exploration of the data alongside thinking deeply on the surrounding factors has driven us further toward confirmation of this thesis. While we don’t think it’s possible to fully understand a complex system to the extent of being able to parse out the contribution of each individual component, the behavior of equity and derivative markets since 2018 seems to support the thesis that something has changed. Or perhaps, many little somethings, that are tending toward this shared behavioral outcome.

The beautiful thing about long volatility positioning is that we don’t actually need precise answers to these seemingly unanswerable questions: robust, path independent strategies do the heavy lifting for us, and allow us to sleep well at night with our asymmetry leaning in the “right” direction.

We’ll have more to say about these phenomena in upcoming letters. For now, let’s get on with August.

“Be like a duck. Calm on the surface, but always peddling like the dickens underneath.” -Michael Cane

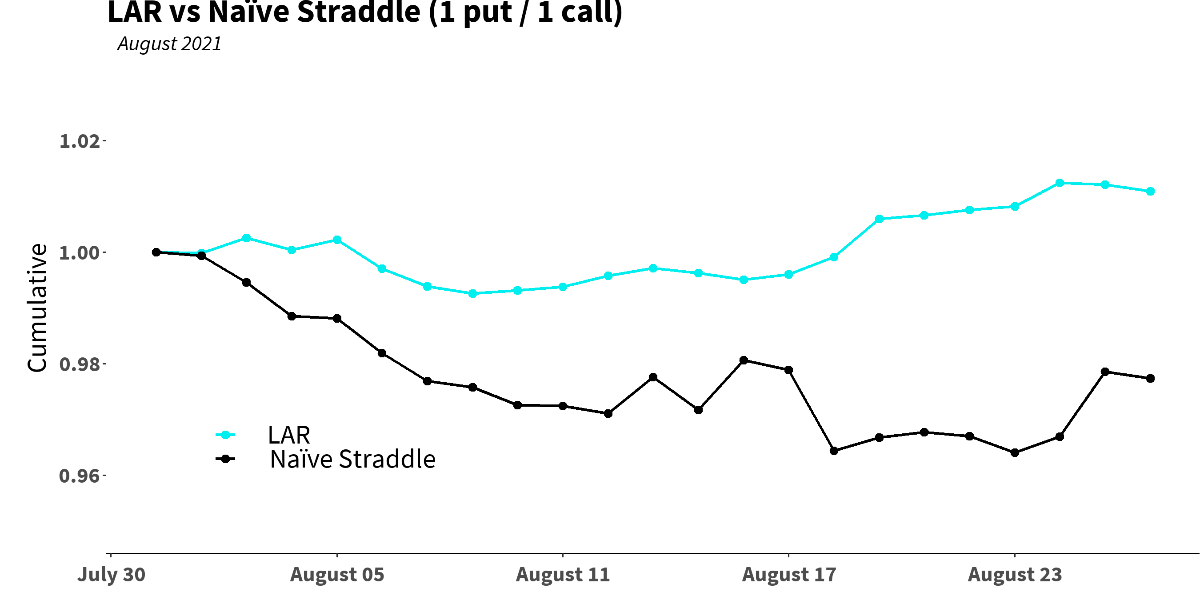

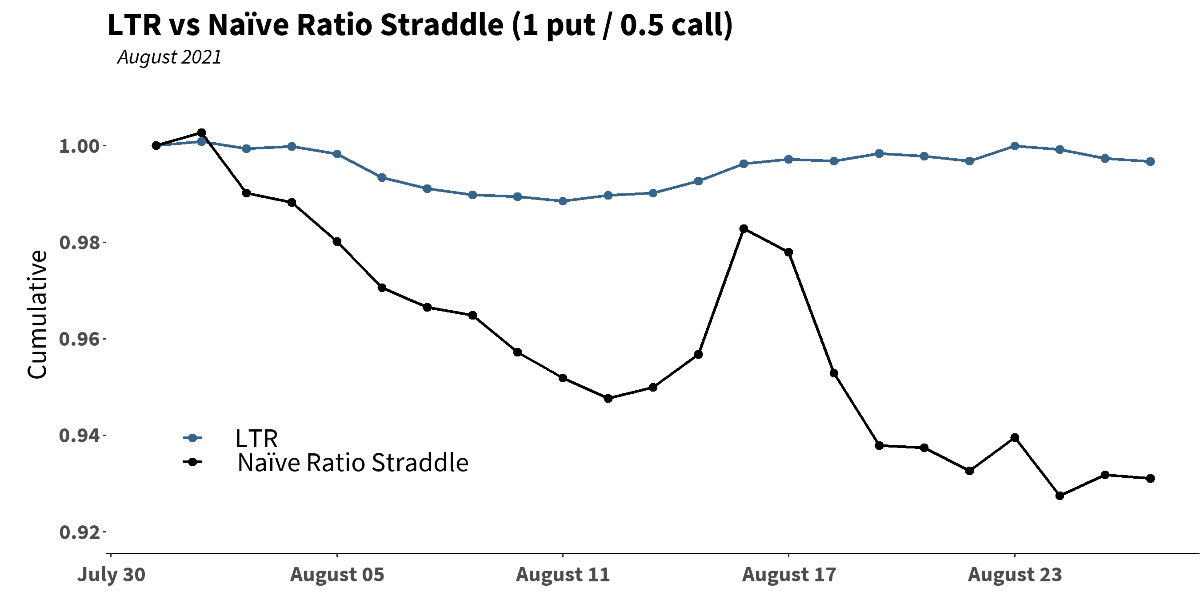

There weren’t many surprises this month in our attributions. Single stock calls performed very well, led by both our pure momentum portfolio and large cap growth/tech book. There were very few opportunities for gamma scalping, given the lack of realized volatility. Albeit, we were able to monetize some gains in our fast scalping modules following the “pullback” on 8/17 and 8/18. This provided some tailwind that, even though minimal during August, over time is accretive and of course necessary to minimize the ever-present cost of carry.That said, both strategies nicely outpaced a naïve straddle in August. We continually see how a naïvely implemented strategy (think “buy and hold”) consistently fails to hold on to gains when volatility spikes:

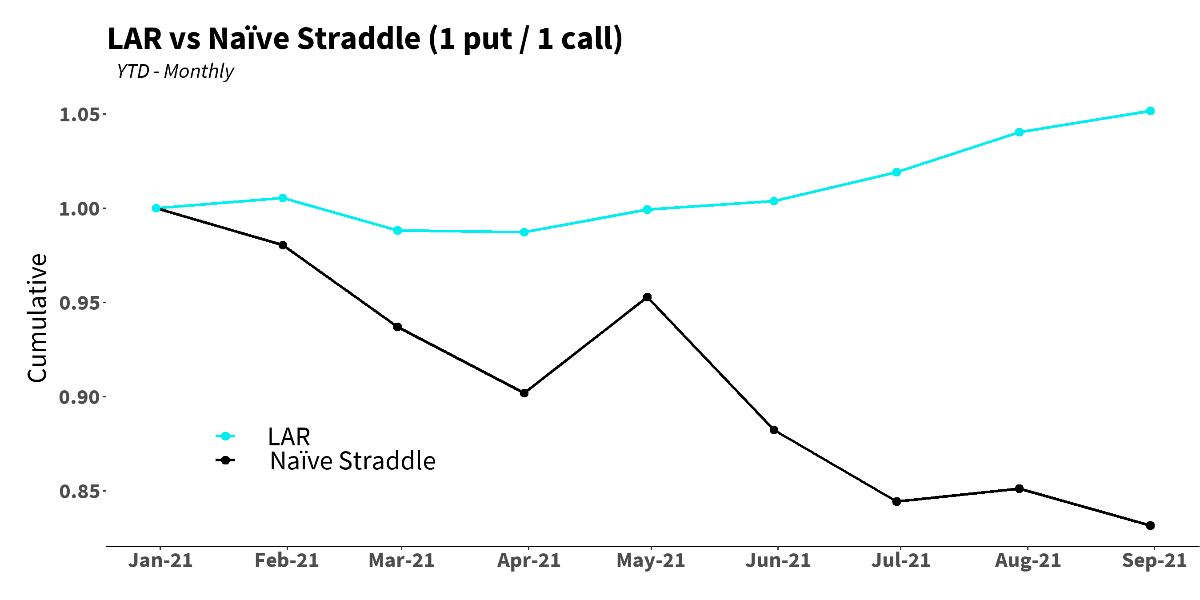

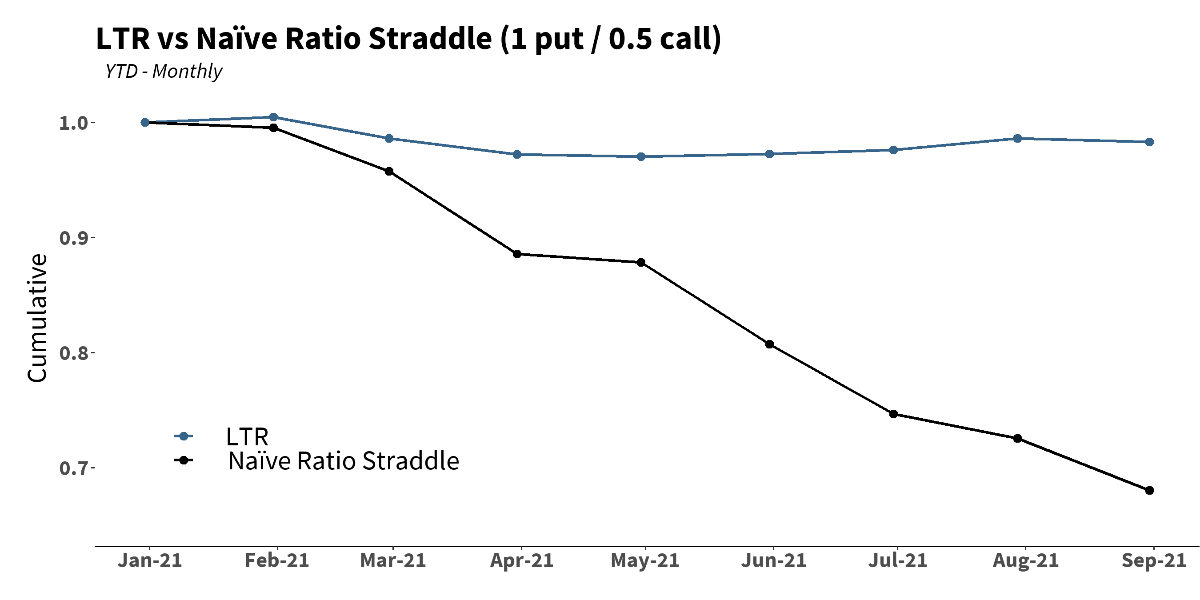

And Year-to-Date, we see the same phenomenon:

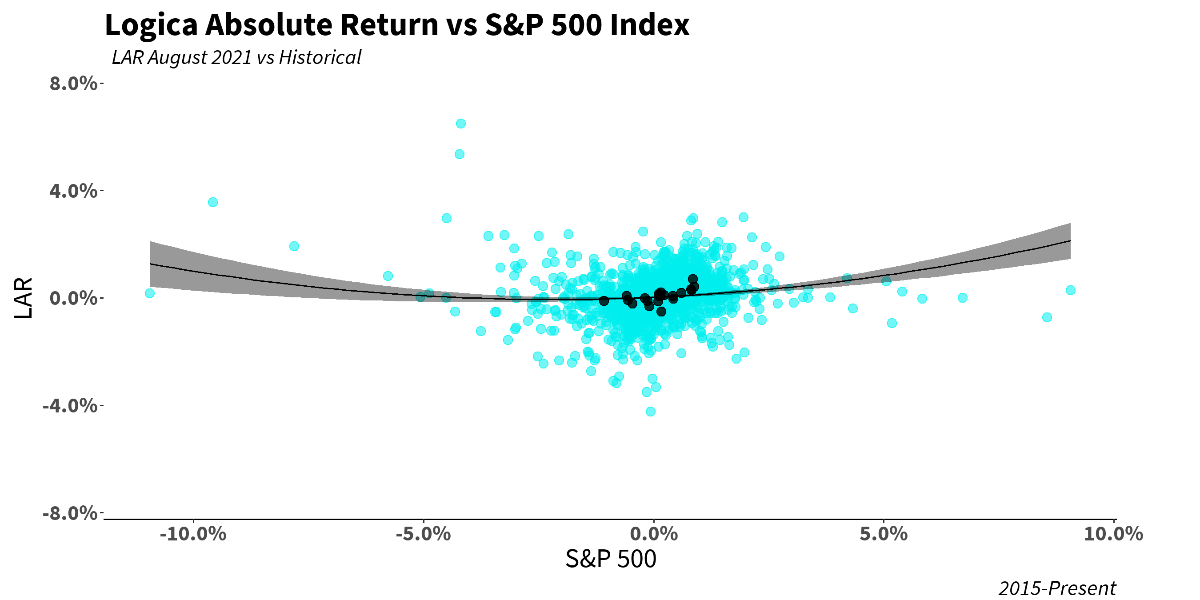

Digging deeper, our daily distribution of returns was as expected, with slightly better than usual performance on the largest S&P upside days:

“Risk is a function of how poorly a strategy will perform if the ‘wrong’ scenario occurs.” – Michael Porter

The great thing about a straddle-like exposure is the fact that the risk is bounded. Of course, this is the attractiveness of long optionality in general, whether it’s a derivative contract on the S&P 500, or an equity interest in a business venture. Most in our business discuss the under/overvalued nature of assets at any given time. We contend that the concept of optionality itself continues to be underappreciated and therefore “mispriced.”

We consider bounding our risk in nearly every aspect of our lives: insurance is a popular example (health insurance, to be sure, but life insurance even goes so far as to bound others’ risk!). Cutting off the riskiest outcomes in life is non-controversial, and the idea is so pervasive to human ways of thinking that we see it everywhere: we network so that if our current job doesn’t pan out, we aren’t on the streets. We save money for rainy days; we limit our speed on freeways, etc… Loss aversion nearly rules our life. Why, then, would we not apply this to our investments?

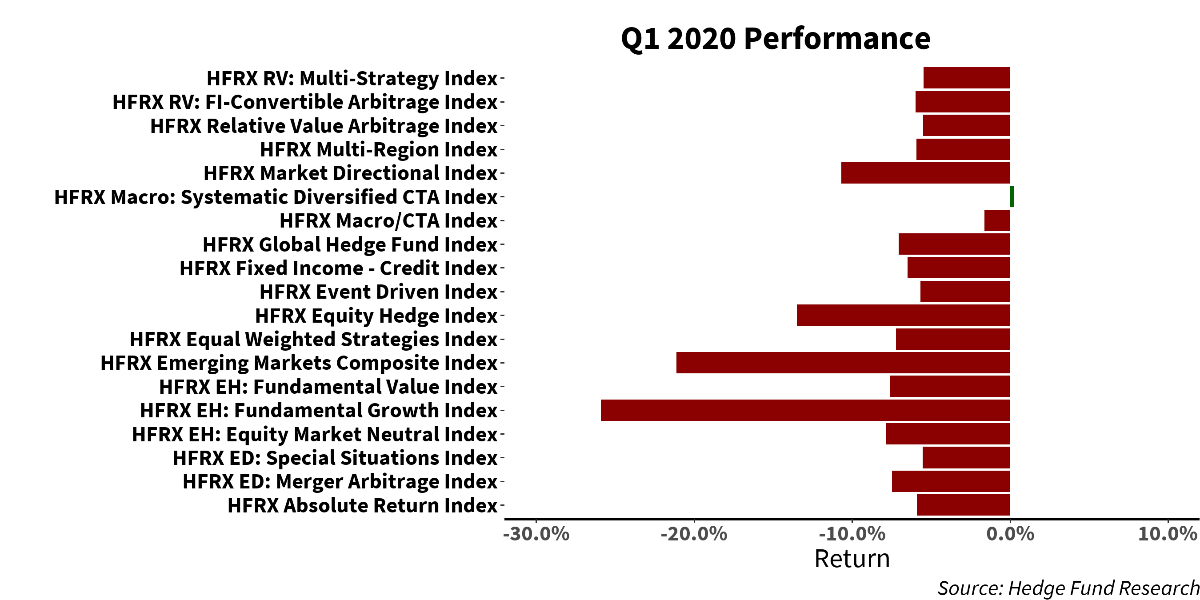

Optionality (and the associated convexity, or positive asymmetry) is the only true way to bound risk. Other diversification methods suffer from unstable correlations/relationships: bonds, commodities, real estate, even most “hedge” funds are unreliable:

In our everyday life, we own insurance directly on an asset – our cars, our homes, our bodies. And we own convexity on the protection of these assets should they realize a disastrous fate. It would not make much sense to think that our real estate investment will be there for us if we total our car. Sure, a good investment gives us cash to fall back on – but the point is timing. Almost all of us desire a smooth life – and this means replenishing lost capital ASAP, or more so, concurrent with some unrelated financial distress. Similarly, a great way for an investment portfolio to realize the maximum long-term geometric return is to minimize downside variance, all else equal…a smooth path, we might say. For that, we need truly uncorrelated assets, and we need convexity.

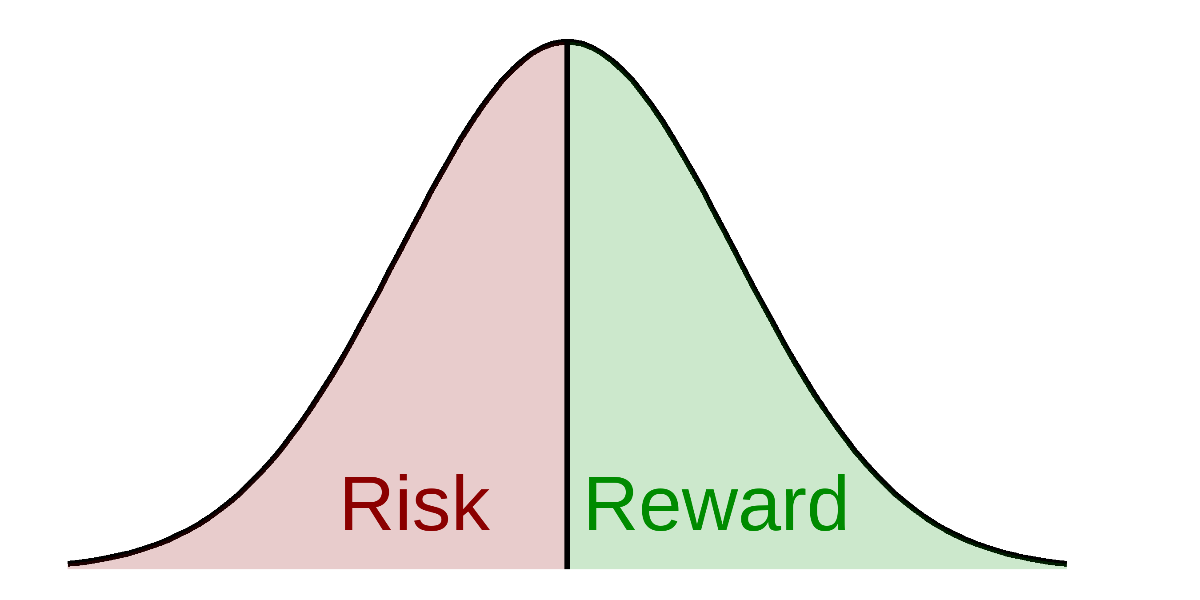

Accordingly, our goal with our approach is to change the overall Risk distribution of a portfolio. We want to trade an unknown, boundless risk, for a known, bounded one. And the holy grail is to accomplish this, of course, while not paying a large premium as one would with typical insurance. Demonstrated statistically, we need to shift the normal long equities distribution from something like this:

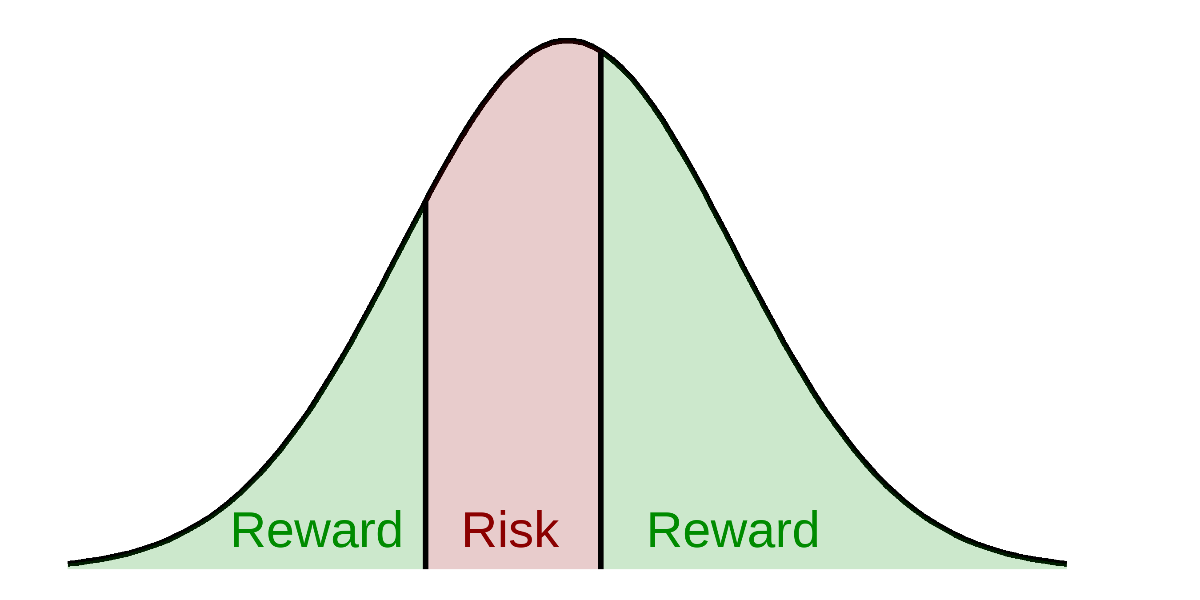

…to something like this, where we sacrifice a little upside (moving the rightward boundary outward) to greatly bound the downside (moving the leftward boundary materially inward):

By changing the distribution in this way, or “re-distributing the risk”, we are not only bounding the downside, but doing so at a time when it’s needed the most. The opportunities in equity markets are typically greatest after large drawdowns – precisely the time when a portfolio needs to able to access and deploy fresh capital to take advantage of such an environment. By improving the distribution, we believe that we are not only enabling a portfolio to realize a superior long-term geometric return, but also offering it the flexibility to take some powerful swings at the most opportune times.

Business Update

We are happy to share that the Logica team continues to grow. Over recent months, we have added two new team members, including Alexandra Imbro, who will be assisting our client relations team, and Jam Zovein, who will be heading up our Product Development & Strategy. Alex comes to us from a long stint at Aegis Capital, and Jam comes to us with long term experience in similar institutional roles at Nuveen, Wilshire Associates, and quant hedge fund Algert Global. Welcome aboard to our new team members!

In the News

Hedge Fund Alert featured Logica’s Tail Risk strategy launch in its recent issue. See below for the link to the article:

Logica Capital – Hedge Fund Alert

Logica Strategy Details

Note: We have comprehensive statistics and metrics available for our strategies, but only include a select few to highlight what we believe is our most valuable contribution to any larger portfolio.

If you would like to learn more about our strategies, please reach out to:

[email protected]

424-652-9500

Follow Wayne on Twitter @WayneHimelsein

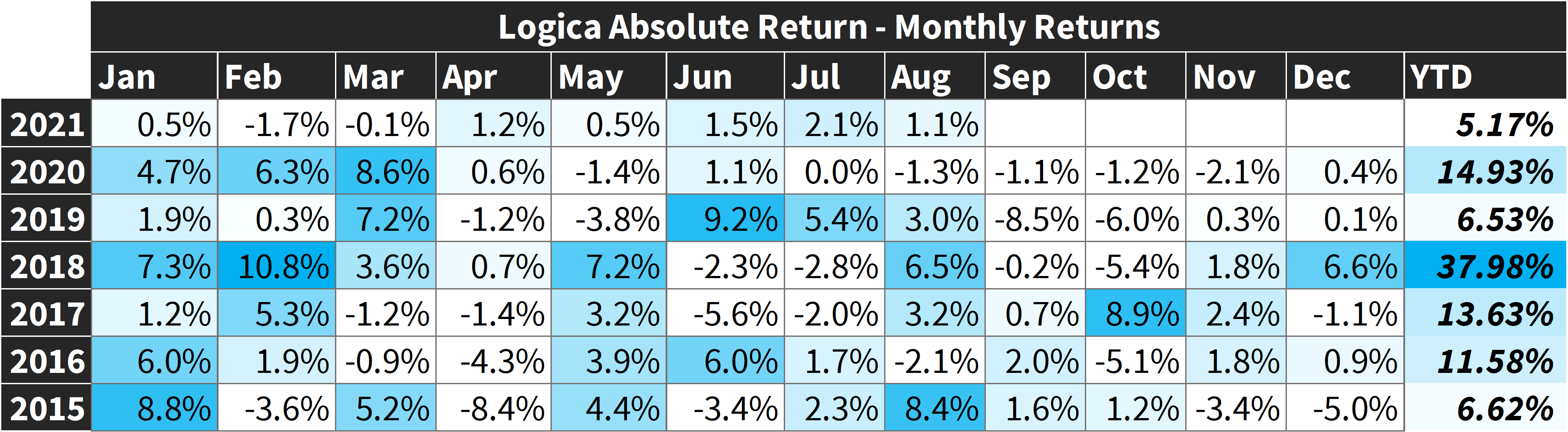

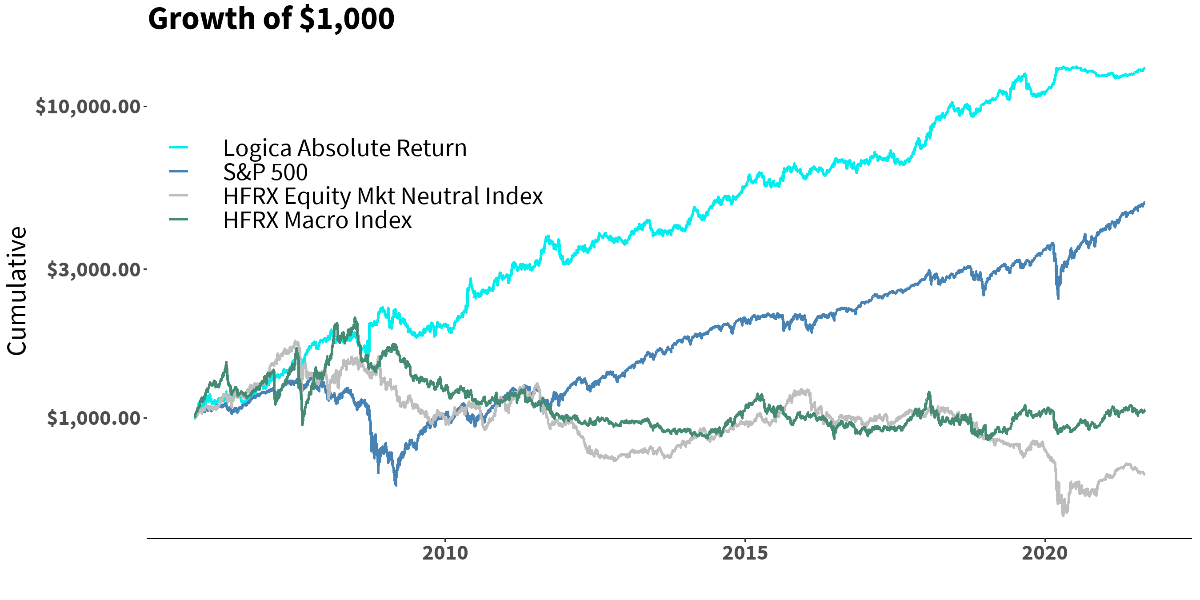

Logica Absolute Return

2015-2019 stats & grid, reconstitution of live sub-strategies normalized to 16% annualized volatility

2005 to present growth of $1000 chart, simulation

Jan 2020 live

*HFRX Indices have been scaled up to 15% annualized volatility to be comparable to LAR and S&P 500.

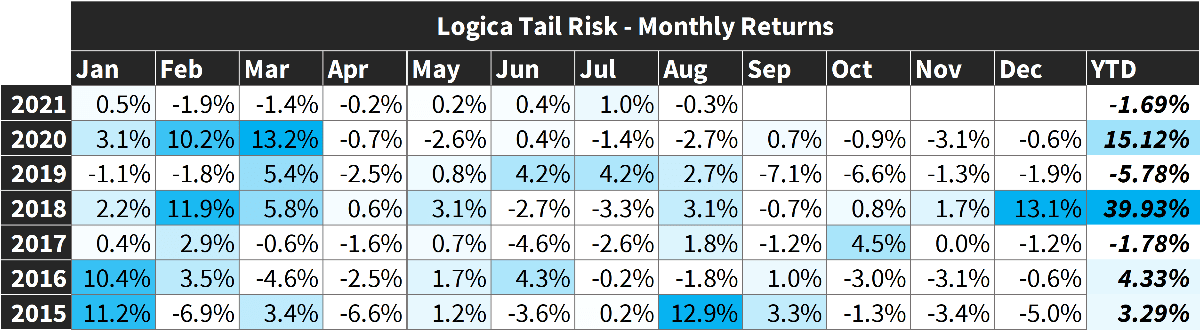

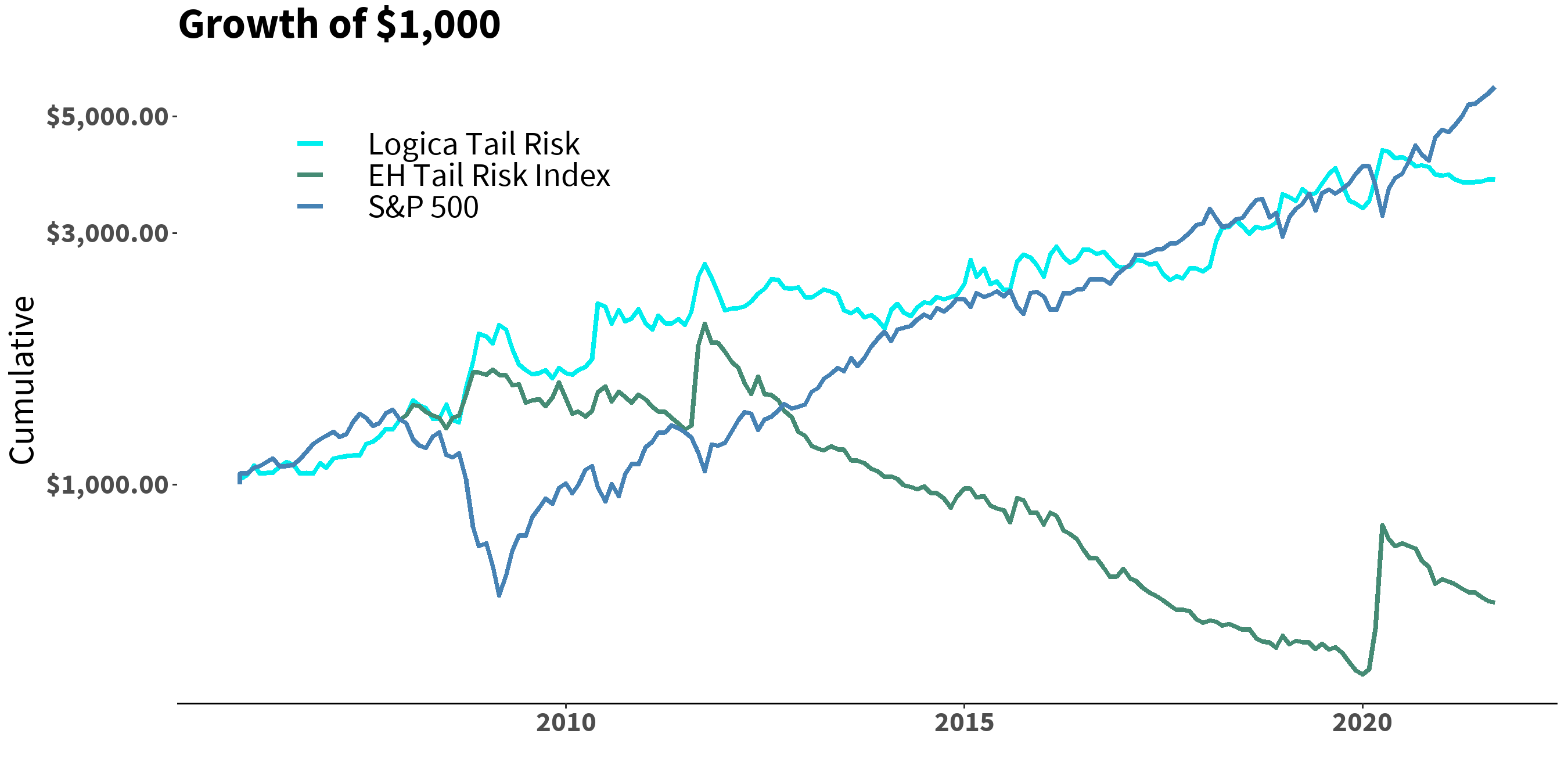

Logica Tail Risk

2015-2019 stats & grid, reconstitution of live sub-strategies normalized to 16% annualized volatility

2005 to present growth of $1000 chart, simulation

Jan 2020 live

*EHTR Index has been scaled up to 17% annualized volatility to be comparable to LTR.