Horos Value Iberia and Horos Value Internacional commentary for the second quarter ended June 30, 2019.

Dear co-investor,

The end of May marked one year since the launch of Horos, a project dedicated to maximising returns for our investors in the long term. They have been twelve months of hard work and dedication on the part of the entire firm, to which the confidence and trust of our investors has served as an incentive to work everyday to the highest possible standards. The confidence of our investors demonstrates that we have a customer base that shares and understands our investment philosophy.

Q2 hedge fund letters, conference, scoops etc

In these first twelve months we have experienced enormous volatility in the markets as a whole and strong corrections in a large number of stocks, which have impacted the short-term results of our portfolios. While understanding how we invest can make these periods of uncertainty and negative returns easier to bear, we think it may be useful to reflect on and review what may be expected from our form of investing. It is to this end that we dedicate the present document.

As always, I would like to take this opportunity to thank you for your confidence.

Yours sincerely,

Javier Ruiz, CFA

CIO

Horos Asset Management

Trust the Process

Make the best use of what is in your power, and take the rest as it occurs. Some things are up to us and some things are not up to us. - Epictetus

The quote above from Epictetus2 reflects one of the maxims of Stoic philosophy. This school urged, among other things, the control of the impulses and emotions that negatively condition and influence peoples' character and actions. It never ceases to amaze us that this insight of the Stoics has existed for twenty-five centuries and yet was not taken into account until relatively recently with regard to the impact of human behaviour on economic and financial models3. Every decision we make, especially in environments of incomplete information and high uncertainty, is highly conditioned by our emotional self, causing us fall into mental short cuts (heuristics) and making it difficult for us to make decisions that we could qualify as rational. Can you think of a world where information is often enormously incomplete and full of uncertainty? Indeed, financial markets are excellent environments for falling into biases or cognitive errors that generate continuous inefficiencies in the valuation of assets waiting to be exploited by the willing investor.

Knowing the existence of these psychological biases can be very useful when it comes to investing for two fundamental reasons. On the one hand, we can limit the number of mistakes we make as investors. On the other hand, understanding how inefficiencies originate helps us to exploit them, obtaining attractive returns and incurring less risk to achieve them (potential permanent loss of invested capital). It is vital we have a decision-making process that isolates our emotions as much as possible and allows us to avoid falling into these psychological biases, while at the same time attempting to take advantage of the investment opportunities they generate. As we have stressed on previous occasions, short-term returns are not a reflection of the benefits of a good investment process. We need returns that are consistent across the long term and not the fruits of good fortune or the taking of risks that will ultimately end up costing us. As Nassim N. Taleb4explains, earning ten million dollars playing Russian roulette is not the same as working as a dentist. I think we can all agree that the former depends much more on randomness and its potential negative outcome would be unacceptable to the majority.

Returning to the quote from Epictetus, it is very important to be aware that, in the world of investment as well as in our day-to-day life, there are events that are within our control and others that are not. For example, we have no control over the evolution of stock prices. However, what is specifically within our control is working with a solid decision-making process that allows us to take advantage of price movements and build a portfolio that meets the objective of achieving sustainable and satisfactory long-term returns. Understanding what is beyond our control in the markets and how to take advantage of it is one of our fundamental tasks as investors. That is why we would like to share with you recurring situations that exemplify everything that has been said so far.

Investors' sentiment.

The four most dangerous words in investing are “This time it's different”. — Sir John Templeton

If you have followed our quarterly publications, you will remember that in Horos we try to avoid labels or investment categories (read letter), since our way of investing includes companies that could be categorised as value, growth or even a mix of both styles. This is because our objective as investors (and our way of understanding value investing) is always to find companies whose valuation is, in our opinion, much higher than the valuation the market is discounting, regardless of their growth profile or their liquidation value. At present, however, much is being said about the poor evolution of value style investment compared to growth investment. Without going into these labels, it is true that in recent months we have seen larger and more liquid companies (such as large global consumer companies), outperforming entities belonging to cyclical sectors or those of smaller size and liquidity. The reason? Although trying to extract causal relationships from correlations is not usually the most recommendable thing in financial markets, in our opinion two powerful motives may be pushing this behaviour.

On the one hand, fixed income has long since ceased to be a sufficiently attractive investment for investors with more conservative profiles. It should be noted that 25% of the public debt issued by states around the world or, worse still, even the debt of some European companies with low quality ratings (junk in financial jargon), offer certain negative yields, except default, for those investors who buy their debt today and wait until it matures.6 This historical anomaly is caused by the increase in money supply in recent years by central banks around the world, which increases the aggregate demand for financial assets and forces the mass of “compulsory” investors (such as insurance companies or large pension funds) to invest in fixed income at any price, even though this means, inexorably, losing money. Faced with this repressive outlook, many investors are forced to invest in stocks of companies with predictable flows that can act as (imperfect) substitutes for bonds. On the other hand, fears of an economic slowdown stemming from the political uncertainty of recent times (see tariff wars, potential economic cooling in China, tensions with Iran or the endless Brexit) have caused investors to pursue a flight-to-quality, abandoning the most cyclical companies (less certainty of flows) and those of smaller size and liquidity. In nervous climates such as the current one, certainty and liquidity become qualities that are highly coveted by many investors.

As a consequence of all this, companies valued by investors as "quality" become more and more overvalued (expensive), turning an investment with no apparent risk into a potentially unsatisfactory investment. One should never lose sight of the notion that even the best business in the world can be ruinous as an investment if it is not purchased at an appropriate price. In our opinion, and without having a crystal ball, investing today in visibility and liquidity may be giving a false sense of security and end up being very expensive. The other side of the coin is found in the rest of the companies, whose continuous stock market collapse places them, in many cases, at levels of undervaluation not seen since the height of the crisis in 2008 and 2009.

Obviously, we have no control over these movements and sentiments of investors, nor over their duration, but we can try to take advantage of the opportunities that, in our opinion, are being generated by this phenomenon. An example of this could be our investment in Microsoft in 2012. At the time, Redmond's technology giant was being penalized by investors for failing to benefit from the rise of smart mobile devices, leaving its Windows operating system (the undisputed leader in laptops and PCs) to be overtaken by Android (Google) and iOS (Apple). Such was the negativism of the moment with respect to Microsoft that the company was at that time trading at 5 times its free cash flow. Again, as investors we did not control what perception the market had of the company, but we were clear that it was a company with revenue and profit growth close to double-digit, thanks to having the best and most used office software in the world (Microsoft Office) and the leading operating system in desktops and laptops. With these attributes, we were convinced that it was only a matter of time before we would see the market picking up its true value. We invested in Microsoft at about $25 per share and liquidated our position, a few years later, with capital gains close to 200%. Today, Microsoft is listed at about $140 per share and is the “darling girl” of the big research firms, whose analysts are willing to pay 20 times the company's free cash flow. We still think that it is a company of enormous quality and interesting growth profile, but one should never lose sight of the price at which one is buying a business and the opportunity cost of letting other more attractive alternatives slip away.

But where are we finding investment opportunities, derived from these inefficiencies generated by the sentiment of market agents, today? As we said before, we are finding them in companies of smaller size and liquidity, as well as in those belonging to more cyclical businesses and with less predictability in their future cash flows. Although in the latter, which we will talk about shortly, we can understand relative underperformance (not so much the magnitude) in the market, we are beginning to be very surprised by the stock market evolution of some of our smaller investments. Such is the case with Asia Standard International, the Hong Kong investment and real estate development company (especially offices in prime locations) of which we are shareholders with our international portfolio. At the beginning of June, its subsidiary Asia Standard Hotel Group announced a positive results alert, informing the market that the business was doing better than they had previously estimated. This is something that would usually have a positive impact on the stock market value of any company. Despite this, the stock price of both entities remained unchanged during the period. In fact, weeks later, Asia Standard International would publish results that would significantly improve our expectations and would again be ignored by the market. This is a clear example of a small and illiquid company ignored by the investment community, which contributes to increase its undervaluation in a continuous way, until the investment feeling changes or some catalyst appears that contributes to uncovering its true value.

However, the situation of companies with more cyclical businesses is very different. The momentum of the cycle, in many cases, is the most unfavourable in decades, which explains its poor progress in the stock market in recent years. Now, every cycle ends up turning around and, historically, buying shares of companies with this profile at the worst time for its business can be a good strategy to obtain significant returns. The price to pay? The high volatility of these stocks at times of greater uncertainty, such as the present times. Indeed, volatility is the second example of what we can and cannot control as investors that we would like to share with you.

Price Volatility

Many of the best bargains at any point in time are found among the things other investors can’t or won’t do. — Howard Marks

One of the mantras of value investors is to treat market volatility as an ally and not as a fearsome enemy to flee from every time it makes an appearance. In order to be able to act in this way, it is essential not to forget that shares are the property titles of listed businesses and the evolution of their price in the long term will always be linked to the progress of that business. Therefore, the value of the business acts like the implacable gravity that returns a ball to the ground after being thrown into the air by a child in the school yard. However, in the short term, investor sentiment can cause large deviations between the value of the business and the price of its shares. Sometimes gravity acts quickly to correct this anomaly, but sometimes the ball can stay in the air longer than usual if, for example, other children hit it before it can fall to the ground. Eventually its destiny will be the same, but we don't control when it will come to pass.

What we do control is being able to take advantage of these temporary inefficiencies. To do this, we need to estimate the value of the companies in which we invest (or plan to invest in, if the price becomes sufficiently attractive) and use price volatility to our advantage. If, for example, a company's stock price falls well below our value estimate, we will increase our investment in it. If, on the other hand, the company enjoys the blessing of the investment community and its stock price increases until it approaches or exceeds our estimate of its value, then we will reduce or sell our position. Obviously, the greater the volatility, the more opportunities will arise and the more profitability we will get from this process. As a result, our portfolios may reflect high turnover, even though the number and names of the companies in our portfolios remain very stable over time.

Here are two examples of investments still present in our portfolios, where volatility has been particularly important and how we have acted (or are acting) to try to take advantage of it. The first case concerns our investment in Qiwi, the Russian company dedicated, among other things, to electronic payment methods and money transfers. Over the last twelve months this company has seen its stock price oscillate between 11 dollars and almost 21 dollars. Specifically, its price plummeted almost 40% from the maximum of 2018, and then appreciated 80% from the minimum. Has its business really changed that much in the period, or is it short-term investor sentiment that caused these (huge) ups and downs?

Our understanding is that investor sentiment has been dancing to the tune of various misinterpreted events. On the one hand, Qiwi has opened different lines of business in the last two years that complement its current payments and transfers platform. Specifically, it launched Sovest (consumer finance cards), Tochka (a bank focused on SMEs) and Rocketbank (a bank focused on millennials: the youngest and most 'technological' demographic). These new lines have required significant investments and an increase in Qiwi's operating expenses, financed with the cash generation of the company's traditional operations. When this cash generation "disappeared", the market began to penalise the company on the stock exchange. This situation was aggravated by the announcement in August 2018 by Sergey Solonin, CEO of the company, of a nine-month trip around the world. For all these reasons, the stock continued correcting until it reached the 12 dollars level.

How did we respond to this important correction (remember that it was 40%)? By increasing our investment. At this point, it is very important to understand that we do not act against the market automatically, that is, we do not acquire more shares of a company by the simple fact that its price falls. What we do continually is review our investment thesis and assess why the market is penalising the company. If we think that this penalisation is unjustified, then we increase our position. This was the case with Qiwi.

On the one hand, we talked to the company on several occasions to find out more about the business strategy they were following and we thought it was the right one (something we corroborated in November 2018, when we attended the Investor's Day that Qiwi organised for its shareholders in London). In addition, Sergey Solonin acquired shares of the company for five million dollars. A not inconsiderable amount that demonstrated his commitment to the company's progress (the important concept of skin in the game we talked about here). On the other hand, in our opinion, the investment community was not adequately valuing Qiwi's business by focusing exclusively on its current cash generation (heavily weighed down by the investments and operating expenses discussed). By separating its lines of business into a valuation by sum of parts, the true cash generation capacity of Qiwi and its significant undervaluation were uncovered. We were convinced that, over time, as investments normalised and the new businesses scaled up (if they were to succeed or otherwise be liquidated), the market would once again reflect the cash generated by the company. In the end, this is what happened. Qiwi announced that, with its investment needs practically covered, it was resuming the dividend distribution and, additionally, the good performance of the business contributed to changing the investor sentiment, allowing a recovery of more than 80% in a few months, which has led us to reduce our investment in line with its current potential and increase our investment in other more penalised companies.

The second example we are going to present you with is Naspers, the South African holding company owner of global technology platforms. The company owns 31% of Tencent, the Chinese company that holds Wechat (a highly evolved platform of the Whatsapp that we use in the West), as well as being the world's largest video game distributor, owning Tencent Video (a mixture of Netflix and YouTube) and Wechat Pay (along with Alipay, the most widely used payment method in China). Therefore, it is a business of extraordinary quality that we can acquire at a discount through Naspers. Specifically, the current value of Tencent's stake is higher than Naspers' market cap, which means we get the rest of Naspers' platforms and investments for "free”, which conversely, are worth considerably more than zero. Several factors, which we are not going to delve into now, explain this inefficiency in the market. However, what you do need to know for what we will discuss below is that the progress of Naspers’ stock depends on two factors: the evolution of its business and investments (especially Tencent) and the increase or reduction of its stock discount. Why do we emphasise this? Because, this last year substantial changes in these two factors caused drastic variations in investor sentiment, increasing the volatility in Naspers’ share price (50% fall from 2018 highs and appreciation of more than 60% since October) and creating excellent opportunities to take advantage of it.

On the one hand, the Chinese regulator announced the prohibition of new video game licenses until companies in the sector, including Tencent, made sure to limit the number of hours of play, as well as to implement filters on the age of the players, after several reported cases of young people suffering significant vision loss after devoting endless number of hours to playing some of Tencent's popular games on their mobile phones. In addition, the regulator took the opportunity to pressure Tencent to modify the theme and content of its most successful (and quite violent) video games. This measure negatively impacted Tencent's business and, as a consequence, its stock price. However, while the impact on the business has been real, a cold analysis of the situation made us understand that the company would benefit in the long term or at least regain some of the lost ground.

That's why we increased our investment in Naspers during that downturn phase. In our view, big players could quickly adapt to the new situation, while small players could even disappear, given the costs associated with adapting to the new regulatory environment. Besides, Tencent wasn't going to stand idly by in the face of these drastic changes. After a short time it announced the release of versions of its popular games catered more to the taste of the regulator. Within a few months, its share price recovered much of the lost ground, a recovery from which Naspers obviously also benefited.

On the other hand, the Naspers management team has been taking steps to try to reduce the discount on the company's stock against the value of its assets. Specifically, in early 2019, Naspers announced the IPO of MultiChoice, its South African pay television division, unlocking its value. In addition, in March of this year, Naspers announced its intention to list its international platforms, including its stake in Tencent, on the Amsterdam Stock Exchange, as a measure to reduce its discount on the stock against the value of its assets. This measure will contribute to reducing Naspers' weight in the South African index, which was strongly impacted by Tencent's good performance (its weight in the index rose from 5% in 2012 to 25% today) and may be influencing the company's discount, as South African investors are forced to reduce Naspers' weight in their portfolios, as this investment exceeds their legal concentration limits. Since the company announced this measure, it has outperformed Tencent's by 10%, so the discount has been somewhat narrowed and indicates that these actions are going in the right direction. After its recovery, we have been reducing, as we did with Qiwi, our position in Naspers, investing in businesses with greater potential.

These two examples clearly illustrate how we at Horos work to take advantage of market volatility. Today, we are faced with portfolio investments that have suffered price collapses due to the excessive negativism of the investment community regarding the industries in which they operate and the future performance of their businesses. Such is the case of Ensco and Borr Drilling (Oil platforms companies), the holding company Teekay Corp. and Meliá Hotels International, to name but a few. As we said at the beginning, we don't control when gravity returns the ball to the ground, but with time, the ball will fall. Obviously, the risk is that our investment thesis is wrong and the price is correctly reflecting the value of the company. That is why our continuous work of analysis and review of our investment thesis is so important.

Until now, we have focused the content of this letter on how there are factors outside our management that influence the evolution of our investments and how it is in our control to be able to benefit from them. However, there is another external factor that we do not control that impacts you directly as a co-investor: your behaviour in the face of these ups and downs. That is what the final part of this letter will be devoted to.

The confidence of the investor

I would rather lose half my shareholders than lose half my shareholders' money — Jean Marie Eveillard

Every value investor knows (and fears) the anecdote of the legendary investor Peter Lynch and his investors. Lynch led Fidelity's Magellan fund to one of the best returns in history, with 29% annual growth over a period of thirteen years. However, the average return for its investors was, according to some sources, only 7% per year. How is such a sizeable difference possible? Very simple. Just as equity investors are conditioned by their emotions, a fund investor inevitably suffers from the same problem. Getting carried away by emotions can force us to sell and buy at the worst possible time, whether we are talking about stocks or investment funds. That's why we spend so much time communicating with our stakeholders, explaining our investment decisions as transparently as possible. Without being a guarantee of success, we think it's the best way for you to understand what you can expect from your investments and our work. Therefore, to finish this letter, we are going to delve into two ideas that we would like you never to lose sight of on this journey you have chosen to embark on with the Horos team.

On the one hand, we must understand that the real risk of an investment is not the volatility of its price, but the possibility of suffering a permanent loss of capital. As we mentioned a moment ago, the companies' stock prices suffer great ups and downs on the stock market, often unjustified. However, what seems obvious after the fact, at the moment of greatest pessimism can make us doubt. The explanation is found in psychology and, specifically, in what is known as loss aversion. Studies show that human beings suffer the losses of an investment more than twice as much as they enjoy profits of an equal magnitude. Therefore, it is very common that, in the most difficult moments as investors, after a bad performance of the portfolio, our minds focus only on the negative, looking for causes for the fall that will justify selling the entire position. Unfortunately, it is precisely this way of acting that leads us to consolidating permanent losses of capital. If the fall in value has not been justified, one should wait or even, if possible, increase one's investment. We are aware that this is not an easy way to react, but it is the best way to guarantee satisfactory returns in the long term.

On the other hand, and very relevant to the above, it is very important to understand that, in the investment the path followed to reach the goal should not condition our decisions. As Ryan Holiday comments in his wonderful book “The Obstacle is the Way8”: We are A-to-Z thinkers, fretting about A, obsessing over Z, yet forgetting all about B through Y. In the case of a fund investor, the “Z” can be the return expected by the fund's management team (e.g. 10% annually over 7 years or, equivalent, 100% over the same period). The “A” could be equivalent to the initial investment in the fund. The rest is the path followed by the net asset value (price) of the fund. This road is inevitably full of potholes, in which you will have years of good returns, years of bad returns and ”quieter” years. Forgetting that this path is necessary to reach “Z” can lead us to fall short of our goal. In the end, if one wishes to obtain annualised returns of, for example, 10%, one cannot expect the return to be 10% every year. No one said it was easy, but the investor's path will always be full of ups and downs. However, we are convinced that trusting and understanding this process will serve as an anchor in the stormiest times.

Current Affairs

Turning to the most significant news at Horos this quarter we would like to highlight our collaboration in the V Finance and Investment Conference of the Juan de Mariana Institute, where our investment director shared an agreeable round table discussion with Otto Kdolsky, manager of the management company Magallanes Value Investors (watch video).

Also, our manager Alejandro Martín participated in the "Conversations with" panel of the Zonavalue team (watch video), where, in addition to talking about his work at Horos, he shared some of his interests and experiences.

Finally, Alejandro and Javier had the pleasure of being interviewed by the team of the finance forum Más Dividendos, in a podcast of almost two hours, where they spoke at length and in detail about some of our investments, as well as other topics related to the industry and management (listen to the podcast).

Horos Value Iberia

The fund can invest up to 20% in holdings listed in Portugal and at least 80% in holdings listed in Spain. In addition, it can invest up to 10% in Spanish or Portuguese companies listed on other markets.

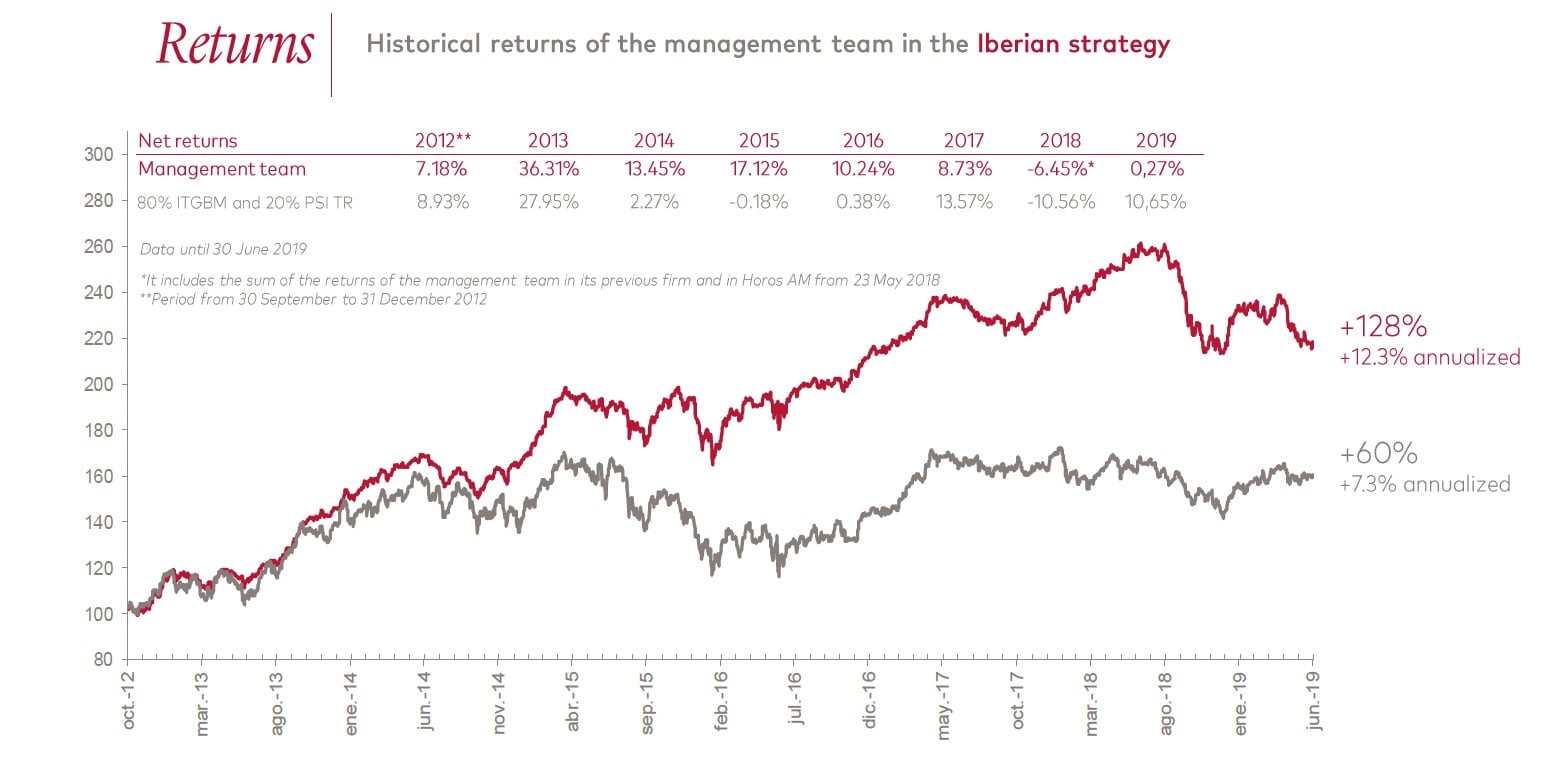

Horos Value Iberia returned -4.4% in the second quarter, compared to its benchmark index, which returned 1.5%. Since its inception on the 21st of May of last year to 30th June, the fund's cumulative return has been -12.8%. In the same period, its benchmark performance was -4.4%. The results achieved in such a short period of time are merely anecdotal and should be considered as such. As an indication of the importance of long-term investment, the annualised return obtained by an investor who has accompanied this management team since its inception would be 12.3% compared to 7.3% for its benchmark (for more information, see the appendix at the end of this document).

In this quarter, the investments with the most positive contribution are Renta Corporación and Aperam. For Renta Corporación, the good performance is owed to the announcement of the launch of two new SOCIMIs, which will join Vivenio, the vehicle managed by the company for the Dutch pension fund APG. These new companies will increase Renta Corporación's cash flows, further lowering its valuation and increasing the visibility of its results, thus counteracting the inherent cyclical nature of its traditional real estate purchase/sale business. Aperam has, as has the entire stainless steel sector, maintained high volatility during these months affected by the tariff wars between the United States and the rest of the world economies. Without denying the impact of these factors, we believe that current prices provide a high margin of safety, so we have increased our position in the company with the best financial profile and cash generation capacity in its sector .

On the negative side, Ercros and Sonae Capital stand out. The chemical company Ercros is suffering the impact of the fall in the price of soda and the rise in the price of EDC (the main raw material), which has hampered the group's profitability in the period and, possibly, for the coming months. In addition, the remuneration program carried out by the company, obliging it to repurchase its own shares at any price, has led to a significant destruction of value for its shareholders. Current prices, after a fall of more than 60% from highs, discount a very negative scenario and, for this reason, we are keeping a significant percentage of the fund invested in the company. As for Sonae Capital, we believe that the bad performance of the period does not correspond to the reality of the business operation, so we have increased our investment in the company.

The fund portfolio had no new stakes or disposals in the quarter.

At the end of the quarter, the fund's potential for the next three years was around 74%, equivalent to a theoretical annualised return of 20.3%. For the calculation of this potential, we performed an individual study of each holding that makes up the portfolio. These theoretical returns are no guarantee that the fund will perform well over the next three years, but they do give an idea of how attractive the current time is for investing in Horos Value Iberia.

Portfolio Structure

At the end of June, the portfolio of Horos Value Iberia comprised 26 holdings and was concentrated in two important blocks. One block, almost 75% of the invested part of the portfolio is made up of companies that we have known for years, managed by families with an important presence in the shareholding (which guarantees an alignment of interests with their shareholders).

The second block (12%) is made up of companies that have been forgotten or even "hated" by the investment community, because they have historically been unfulfilling for shareholders, but that are very attractive to invest in today.

Horos Value Iberia also invests in Horos Value Internacional (4.6%). In this way, the potential of the Iberian fund is increased, increasing the quality of the portfolio and generating greater value for our co-investors in the long-term. Of course, NO commission is charged on that percentage invested in the house funds.

Finally, the cash position of the fund at the end of the quarter was below 2%.

Main Positions

Meliá Hoteles (7.6%, family-owned): hotel group with a presence in over 40 countries, of which the Escarrer family controls 52% and has been a shareholder for over 60 years. The company is the leading hotel chain in Latin America and the Caribbean and is the largest global player in resorts and “bleisure” (a combination of business and leisure). Meliá's objective is to migrate to an asset-light business model, which focusses on the management of hotels without owning them. Currently, hotel management accounts for nearly 30% of EBITDA and they expect to reach 50% in seven years. The interesting thing about this investment lies in the valuation of its hotel assets, (much higher than its current market capitalisation, which allows us to take the hotel management business “for free”) and what this business can contribute to the company in the future.

Ercros (6.0%, forgotten): company forgotten by analysts due to the complicated situation it experienced a few years ago. It is an industrial group dedicated to the production of chlorine derivatives (necessary, for example, for the manufacture of PVC), intermediate chemicals (formaldehydes, glues and resins, etc.) and pharmaceuticals (raw materials and intermediary products). After almost ten years of continuous decline in demand for PVC, the capacity shut-downs of the sector in recent years, together with the additional restriction of supply that is taking place, following the ban by the European regulator on the use of mercury technology in chlorine production processes, gives us reasonable expectations for a good evolution of this industry in the coming years.

Catalana Occidente (5.6%, family-owned): This insurance company has an excellent history of creating value for its shareholders, thanks to the attractive acquisitions they make on a regular basis. Its management team manages the business very conservatively, operating with combined ratios lower than those of the industry, as well as of the balance sheet, and always has a significant excess of reserves. We believe that the current prices at which the company trades do not reflect the profitability of the business or its good capital management.

Renta Corporación (5.6%, forgotten): the company, focussed on acquiring real estate assets for transformation and sale, has gone through a restructuring process, both financial and business (they use options to purchase the properties to be reformed), which avoids risks to the balance sheet that are typical of this industry. In addition, it has reached an agreement with the Dutch pension fund APG to manage its SOCIMI specialised in residential assets. This SOCIMI has the goal of reaching 1,500 million euros in assets and Renta Corporación, in addition to owning 3% of the SOCIMI, charges a 1.5% fee for its management. In 2019, Renta Corporación has announced its intention to launch two more similar vehicles, which will contribute to increasing the cash generation capacity and visibility of the company's results. Finally, it should be noted that we are working hand in hand with a professional and highly experienced management team, which has been able to restructure its business toward a model of high returns on capital employed.

Ibersol (5.1%, family-owned): Portuguese multi-brand catering company operating restaurants and franchises in Portugal, Spain and Angola. Its best-known brands include Pizza Hut, Burger King, KFC and Pans & Company. This is a business of relative stability and significant capacity to generate free cash flows. Finally, close to 55% of the shareholding is in the hands of the management team, which aligns its incentives with those of the rest of the shareholders.

Horos Value Internacional

Our international portfolio can invest without geographical restrictions in most of the world's stock exchanges, including the Iberian market. Therefore, Horos Value Internacional can count on the best investment ideas that this management team currently finds available.

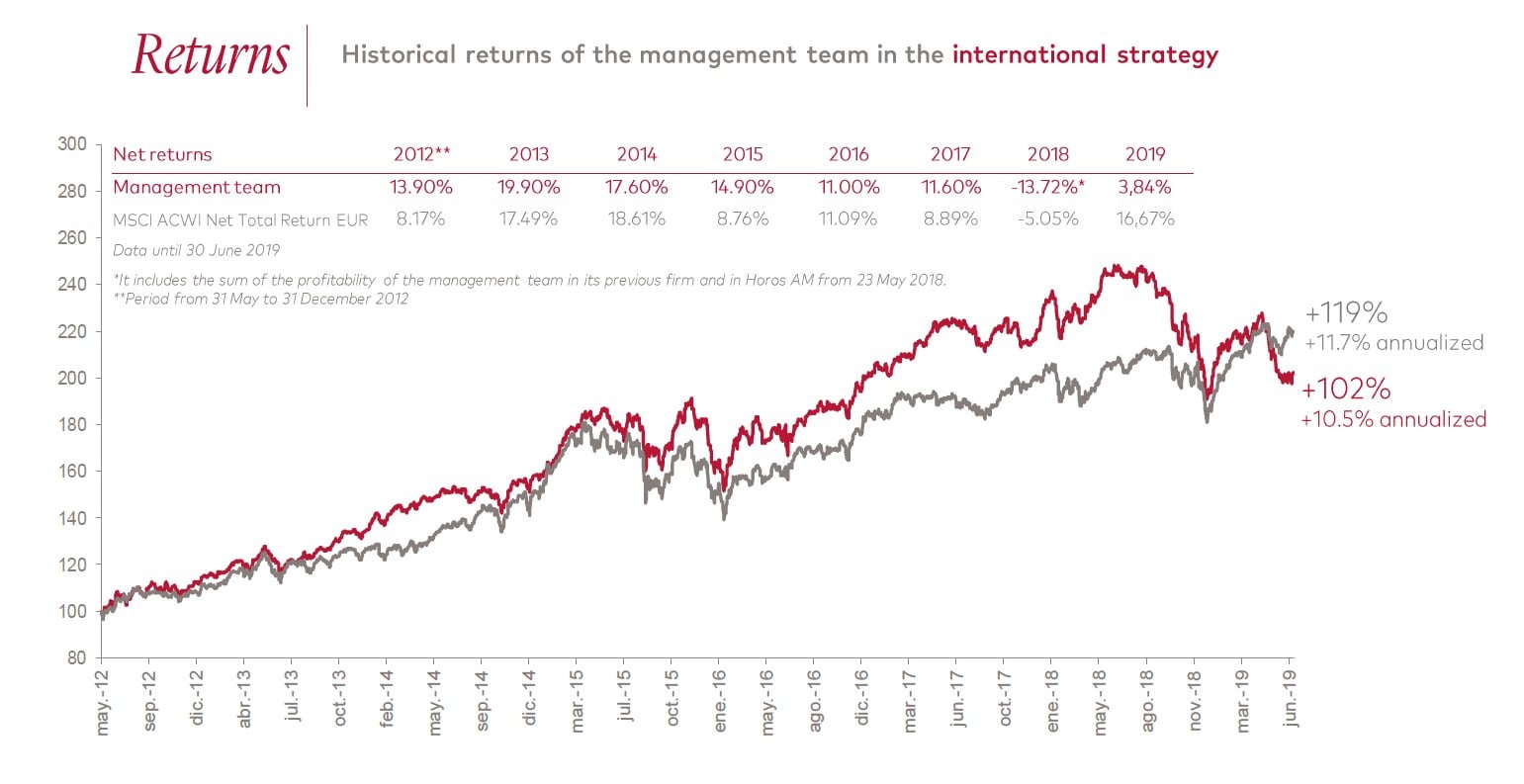

Horos Value Internacional returned -7.1% in the fourth quarter, compared to its benchmark index, which returned 2.2%. Since its inception on the 21st of May of last year to 31st June, the fund's cumulative return has been -17.3%. In the same period, its benchmark performance was 6.7%. The results obtained in such a short period of time are merely anecdotal and should be considered as such. As an indication of the importance of long-term investment, the annualised return obtained by an investor who has accompanied this management team since its inception would be 10.5% compared to 11.7% for its benchmark (for more information, see the appendix at the end of this document).

In this period, the holdings that have contributed most to the fund's portfolio are IWG, Qiwi and AerCap. IWG, the English company that manages work centres, announced in the period the sale of its Japanese business to TKP Corp. for 320 million pounds, also communicating its intention to make more future sales, to start a migration towards a franchise model. For its part, Qiwi surprised the market with higher-than-expected revenue growth and results, also announcing an increase in the expected earnings guidance for the year as a whole. AerCap, the aircraft leasing company, continues to demonstrate the strength of its business and its management team continues to take advantage of the current price discount against its book value to aggressively repurchase shares.

On the negative side, Ensco Rowan (soon to be renamed Valaris), Ercros and Baidu stand out. The American oil platform company, like the rest of the sector, has continued its own stock price ordeal, with very heavy falls in the period. The fear that the sector will not recover quickly enough in the coming years and put future refinancing at risk explains this performance. Without knowing if the recovery of platform contracting will be more or less imminent, it is clear that the company is taking measures to create value for its shareholders. Specifically, Ensco announced at the end of June the launch of a bond repurchase offer amounting to 600 million dollars, thus reducing its debt and taking advantage of the attractive purchase price (finally, the company announced in July that it raised the offer above 724 million dollars, with a purchase price that yields a discount of 24%, that is to say, it redeemed almost 1,000 million dollars of debt by paying just over 700 million dollars).

The chemical company Ercros is suffering the impact of the fall in the price of soda and the rise in the price of EDC (the main raw material), which has hampered the group's profitability in the period and possibly for the coming months. In addition, the remuneration program carried out by the company, obliging it to repurchase its own shares at any price, has led to a significant destruction of value for its shareholders. Current prices, after a fall of more than 60% from highs, discount a very negative scenario and, for this reason we are maintaining a position of the fund invested in the company.

Finally, Baidu is suffering a double impact on its business at this time, which has contributed to a notable deterioration in the company's current profitability. On the revenue side, it continues to suffer regulatory consequences in its management of health-related advertising (remember the scandal of a few years ago of fraudulent drug advertising, with disastrous consequences, on Baidu platforms), which has caused it to lose customers along the way and slow down its growth (this is the industry with the greatest historical weight in the company's revenue). In addition, regulatory changes in the video game industry and the economic slowdown have played a role. We think that these are circumstantial factors that will be normalised in the coming quarters. On the other hand, Baidu is promoting a “super app” for mobile phones that includes all its services, in order to be able to compete with other technological players, especially Tencent. To generate direct traffic to this application, Baidu needs to make significant investments that it will not be able to monetise until some time later, which negatively impacts the profitability of the business. For now, Baidu is constantly increasing the number of users of its application (almost 190 million DAU in the last update), but it is a structural impact on its business and, of course, contributes to a lower visibility of its future cash flows. That said, we think it is the right strategy to follow, given the current competitive environment.

The international portfolio had two entries (KKR and Infotel) in the period and no disposals.

KKR is one of the largest and oldest alternative investment managers. In recent years, with more than 200 billion dollars under management, the entity has been reducing its historical dependence on the private equity business, to invest in new lines, either directly (real estate or infrastructure, for example) or through agreements with third parties (hedge funds). KKR uses its balance sheet to invest in the products it manages, giving them scale while achieving profitability and generating value for its shareholders. This balance represents more than 60% of KKR's current market value, which gives the investment a high safety margin. In our opinion, current prices imply that the balance sheet will not generate more returns in the future and, in addition, they give no value to the revenue from variable incentives (carry) that KKR may obtain. Both scenarios seem unreal to us, given the historical double-digit returns of the company's balance sheet investments and KKR's important carry yet to be untapped, largely linked to new products that require time and larger scale.

Infotel is a French company that designs, develops and maintains IT systems for multi-sector customers. Infotel has a very solid balance sheet (the current cash represents 30% of its market capitalisation), which gives it great flexibility to continue with its organic growth, while allowing it to make specific acquisitions to complement its business.

At the end of the quarter, the fund's potential for the next three years was around 143%, equivalent to a theoretical annualised return of 34.5%. For the calculation of this potential, we performed an individual study of each holding that makes up the portfolio. These theoretical returns are no guarantee that the fund will perform well over the next three years, but they do give an idea of how attractive the current time is for investing in Horos Value Internacional.

Portfolio Structure

The portfolio has 34 holdings and four blocks that account for the bulk of it. The main one is made up of companies linked to raw materials (33%), especially uranium, stainless steel and oil. Another important block is the one that includes forgotten emerging stocks (18%) or stocks scarcely followed by the investment community, mainly from Asia. Investment in technology platforms (14%) with powerful network effects that are still trading at very attractive prices and in UK companies (9%), impacted by the Brexit, would be the other two important investment blocks.

Lastly, the cash position of the portfolio at the end of the quarter stood at 4.4%.

Main Positions

Uranium Participation Corporation (5.8%, raw materials): The investment vehicle that buys and stores uranium for later sale. Given our positive outlook for uranium prices and the limited cost structure of this vehicle, we have decided to concentrate our investment in this type of company (we are also shareholders in Yellow Cake, a similar vehicle listed in London) and renounce, at these prices, exposure via mining companies, where we would have to assume a greater risk of loss in an adverse scenario, as well as operational risks linked to the management and development of projects and mines.

Teekay Corp. (5.7%, raw materials): is a holding company that owns shipping companies that use methane carriers (Teekay LNG), tankers (Teekay Tankers). Teekay Corporation owns approx. 33% of Teekay LNG, the world's largest liquified natural gas shipping company by fleet size. Teekay Corporation, for the management of Teekay LNG, charges a fee that increases depending on the distribution of cash that Teekay LNG makes. Today, Teekay LNG's cash distribution is low (although it has risen 36% by 2019) due to the objective of deleveraging the company, which hides from the market the value of the increase in distributions we expect for the coming years.

Aperam (5.4%, family-owned): one of the world's leading stainless-steel producers, with strong exposure to Europe and Latin America. After a couple of years of good stock performance, as a result of the rationalisation of the sector's supply and the anti-dumping measures imposed by Europe against Asian producers, the fear of the impact of US President Trump's tariffs on this metal have, in our opinion, had an excessively negative impact on the stock.

Keck Seng Investments (5.3%, forgotten emerging company): is a Hong Kong family company founded in the early 1940s by the Ho family, owner of 75% of the vehicle, so its interests are aligned with those of its shareholders. The holding company specialises in the ownership and management of hotels in the United States, China, Japan, Vietnam and Canada. Keck Seng also has an important residential portfolio in Macao that we expect will benefit from the recent opening of the bridge that connects Hong Kong with this city. The poor liquidity of the share or the fact that the assets are valued at acquisition cost on the balance sheet have contributed to a market inefficiency, which in our opinion is unjustified.

Aercap Holdings (4.8%, others): one of the world's leading aircraft leasing companies. This is a business with a high recurring revenues and good future prospects, given the expected growth in aircraft production and demand for aircraft in the coming years, mainly derived from the needs of developed economies and the expected growth of emerging economies. Although this is a business with significant financial leverage, we believe that the stability of the revenue streams generated by the business, as well as the correct capital allocation in recent years, acquiring ILFC at very attractive prices in 2013 or repurchasing shares at a significant discount, justify investing in a company that achieves historical ROEs of 12% and is trading today with a discount on its book value and at less than 10x earnings.

{kind=link}

{kind=link}