Horizon Kinetics portfolio update for the fourth quarter ended December 31, 207.

An Overview

Part 1: The CalPERS Return Problem and its Contribution to the Bubble.

Part 2: Our Allocation to Inflation Beneficiaries and Other Diversifiers

Part 3: Marine Drilling & Shipping Holdings

Part 4: Our Precious Metals Exposure

Part 5: Revisiting Consensus Money and Blockchain Discussions

The CalPERS Conundrum

Some Background Facts

A few notable facts:

- AUM: $356B* (2ndlargest in the US, 7thworldwide)

- 194 managers in private equity alone; paid $234M in management fees and $455 in incentive fees

- Paid $33.6B of stock trading commission on ~18B shares, translating to ~0.2¢ per share.

- CalPERS serves almost 2 million public employee members, over one-third of whom are already retirees and beneficiaries. It paid out an average of about $33,000 each last year. And the number of members increased by 3% during the year.**

- In 2016, The Fund lowered its expected rate of return from 7.5% to 7.0%.

- Expected 2017 funded ratio: 68% (it was 86% funded in 2006).

Positions (as of 12/31/2016), to name a few:

- ~2000 separate corporate bonds (aside from MBS, Treasuries, ABS)

- 4000 domestic publicly traded stocks

They seem exposed to the very same securities at the center of the indexation fund flows as a retail investor directed by an online robo-advisor.

And Its Contribution to the Bubble

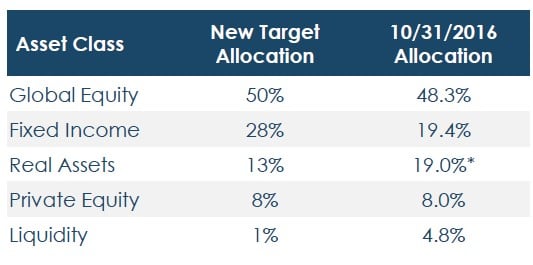

In December 2016, the Board voted for a change in its allocation to support the existing plan to reach as even percent discount rate.

In a low-growth, record-high-valuation environment, a major risk to bond prices in particular is an increase in inflation or interest rates. Yet, not only did CalPERS increase its weighting to below-required-return bonds as well as stocks, but in order to increase those weightings, it reduced its allocation to Inflation Assets and Real Assets by 6% points; the Fund also reduced cash, which provides flexibility in the event of sudden, large price changes, to almost zero.

And this is only one of the innumerable vectors of buying demand that help perpetuate bubbles.

The Sacramento Bee

(Dec 20, 2016) CalPERS moves to slash investment forecast. That means higher pension contributions are coming.

- CalPERS has spoken. Its ominous message is reverberating through government buildings and employee cubicles all over

- The move, closely watched in the pension industry, reflects an acknowledgment that investment returns are softening. “This is very monumental for the organization,” said board member Richard Costigan moments before the vote.

- The state says its CalPERS bill will increase by $2 billion a year, including a $1 billion-a-year hit to the general fund [almost a 20% increase]. Representatives of California’s school districts said they’ll have to shell out another $500 million a

- “It is possible that we could see some bankruptcies,” said Dane Hutchings of the League of California Cities in an interview

http://www.sacbee.com/news/business/article122088759.html

Practical Questions about Real Risks

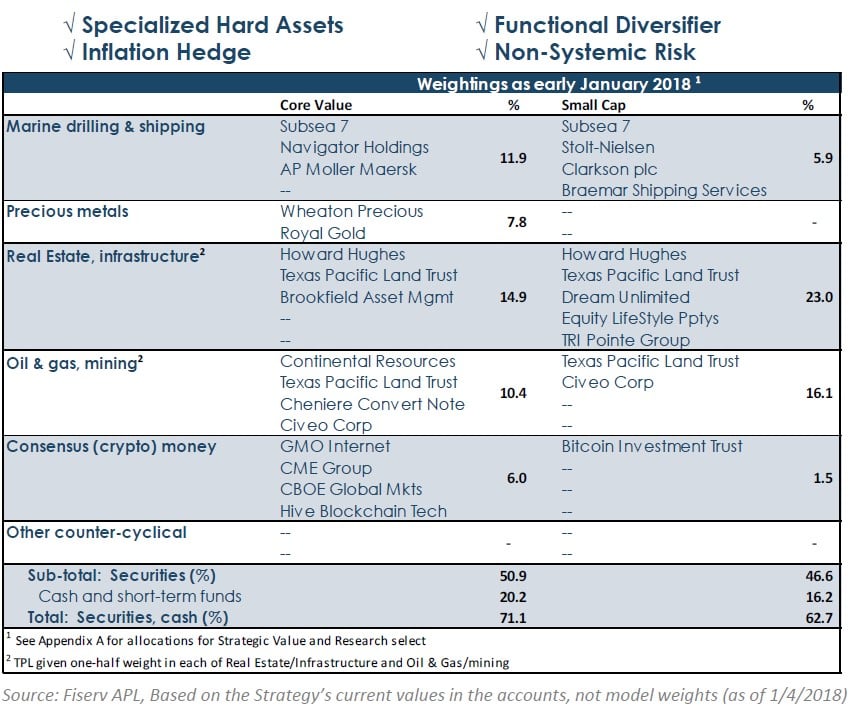

Inflation Beneficiaries and other Diversifying or Counter-Cyclical Holdings

The businesses identified on the right are not only markedly different than the broad stock market –information technology and finance being the two largest sectors – they differ markedly from ea ch other: in their business models, the way they derive their revenues and customers, and the factors that may cause them to do well or to recover if they happen to be depressed . They comprise between about 35% and 55% of ea ch strategy.

And if we include the 15% to 25% cash balance – a value-elastic asset – in ea ch strategy, the differentiable chara cter of these portfolios is even more substantial.

The first questions were: do the portfolios have any inflation-beneficiaries?

Having shown you, the next question might be: why do you have so much? And what about timing?

We’ve been preparing our portfolios for preservation of purchasing power :

- Bond yields are so low, even junk bonds, that they just about guarantee a negative after -tax, after – inflation return . That’s losing money, not making money, not so different than

- And the S&P 500 is at an all-time high P/E. Recall from prior reviews that whatever figure you see when you look at that S&P 500 number, it doesn’t include the companies with very high P/E’s – like Amazon, with its year-forward P/E of

Timing? The only time to get a good price in a tourist shop is when the season is over, the tourists have left, and the shopkeeper has a long winter ahead.

One reason for so many counter -cyclic als is pure investing opportunism : the best time to buy, say, an inflation -beneficiary security is precisely when no one is concerned about inflation. That’s when they sell at deep discounts, and you don’t pay a premium for the characteristic you want. The prices tell you all on their own . That’s usually when no one wants them or expects a recovery or is willing to wait for a recovery, i.e. pre-position yourself in securities that already provide alluring safety and return characteristics

Some Diversifying Industries and Companies

Marine Drilling and Shipping

These are among the most depressed industries in the world. A couple of examples will illustrate:

- The lease rates for transporting various raw materials – the Baltic Dry Index – is down 41% from its high at year- end 2013; it declined 87% to its low in

- The number of offshore drilling rigs has declined by 82% since

Diamond Offshore

This off-shore drilling rig operator had 56% lower revenue in 2016 than in 2009. But it still generates substantial free c ash flow, and has no debt maturing until November 2023. Controlled by the Tisch family, it has a certain staying power and therefore represents a long -term call option on higher oil prices. How much optionality? The c ompany trades at only 3.4x its average earnings since 2004. If a recovery P/E ratio is only 12x, the shares would appreciate by 3.5x. Even if that were to take 5 years to accomplish, it would be 28% per year.

Maersk

This largest container shipping company in the world does not depend on a recovery in oil prices . It is a family – controlled business, is also profitable, has repurchased substantial quantities of shares, has recently acquired a significant failed competitor, and simply requires a normalized rebalancing of the excess supply of ships with demand from the persistent rise in from global trade, in order to provide a very robust rate of return . It trades at about 1.1x book value .

Clarkson and Braemar

Clarkson and Braemar fall into the croupier c ategory of business model — intermediaries who don’t risk any serious amount of c apital, but take their fair share of the a ctivity of other participants . These are shipping brokers which are asset -light businesses . They don’t own ships; they provide information about ships. Moreover, they are diversified a cross the spectrum of shipping sectors, so their exposure is to tankers, container ships, bulk carriers, and so forth. They are profitable, despite the market depression .

And they also have an additional form of earnings leverage in that a portion of their fees are a function of the vessel lease rates . Ergo, if container shipping rates rise sharply, that will be reflected to a degree in revenues, separate from increased transa ction activity . The investment return will be lower than in a recovering direct and asset -intensive operator, but it should be high nevertheless.

See the full PDF below.

{kind=link}