The Broad Market Index was down 1.94% last week and 54% of stocks out-performed the index.

Q3 2021 hedge fund letters, conferences and more

With most U.S. companies now having reported their 3rd quarter financial statements, it shapes up to be another astonishing jump in corporate growth. Sales growth is up again with the average American company reporting 25% jump in sales over last year. This means 75% of all stock market companies are achieving an improvement in topline corporate growth.

Pent up desire to spend by consumers, rising wealth and savings, low interest rates, easy access to credit and now the fear of missing out on rising asset prices has produced an overheated corporate economy. Add to that the recently legislated federal infrastructure spending action and there are all the conditions for rising commodity prices and inflation.

Inflation Directly Impacts Corporate Growth

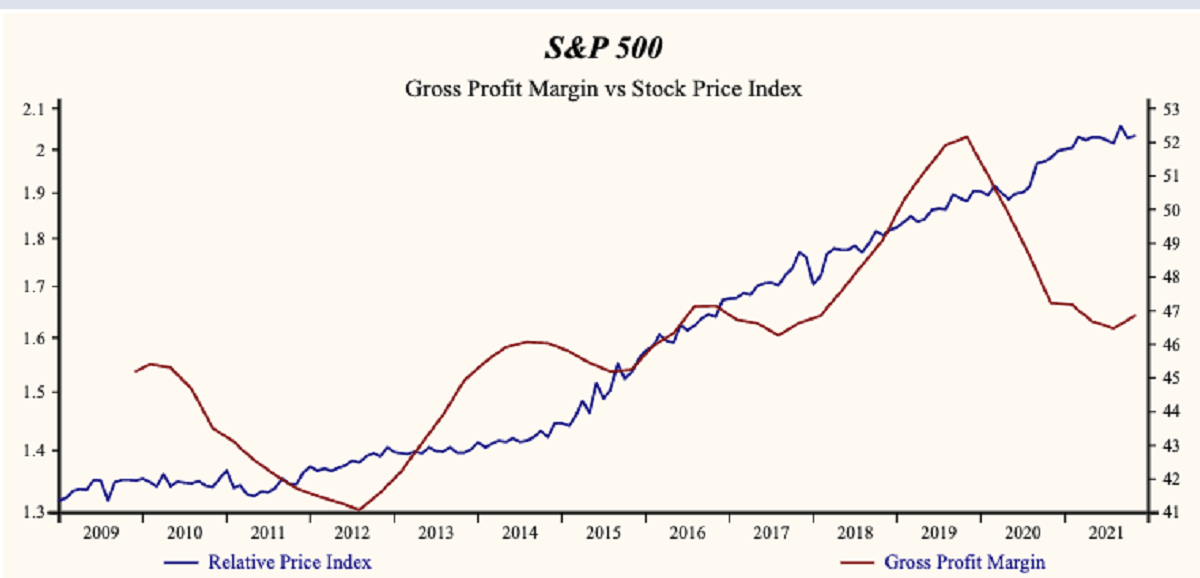

Commodity and labor costs are rising at a faster rate than product prices so the only direction for the gross profit margin is down. Evidence accumulated during the recent financial statement update shows that companies are in fact passing on rising costs as higher product and service prices. This is seen (graph below) by both the S&P 500 Index and the Otos Total Market Index gross profit margin rising. A soldi rebound after a 4-year almost steady decline and marks the 1st increase since 2019.

Your Portfolio Attributes Speak Numbers

It is important to be scrupulous around growth attributes of your portfolio of companies. With share-price indexes back to all-time highs it is important to sell stocks of companies with falling growth. Review your portfolio (your Otos MoneyTrees) and sell stocks of companies with lower sales growth (Red MoneyTree Trunk) and falling profit margins (Red MoneyTree Pot).

The broad market index was down slightly in November while long treasury bond yields dropped to 1.7% lifting long treasury bond prices. Stocks have been flat relative-to-bonds this year and the gap between corporate growth and inflation has never been higher.

Historically, in periods of rising growth, shares of stable growth companies perform poorly even with a high growth rate. In the recent 3rd quarter, the gross profit margin was up on average but with a smaller proportion of companies achieving this improvement. So, make sure all your stocks have rising profit margins (a golden pot).

Some of the remarkable improvement in growth attributes is the result of the virus impact that makes an easy comparison and maybe some pent-up demand as people postponed purchases during the lockdown. These attractive growth stocks will dissipate in coming quarters.

FED’s Response

Evidence emerged recently that U.S. policy makers will go to even more extraordinary lengths to sustain the value of assets. The unusual gap between bond yields and inflation must fall. The proper policy response now would be to increase interest rates and restrict lending to cool an overheated economy and prevent evident rising inflation from becoming rising inflation expectations.

However, no such policy can emerge before the mid-term U.S. elections. That makes for another year of fuelling inflation.

That translates into a portfolio strategy for a more volatile market. With the stock market still near all-time high. You must focus on sell decisions and particularly of companies with stable or falling growth.

Average Sales Growth Is Over 25%

In coming quarters, it will be difficult to sustain the rising-sales-growth attribute among our portfolio of companies. Sales growth is over 25% now, the highest we have ever measured from U.S. companies. Sales growth must fall in the future. As stated above, in the recent period, 3/4 of U.S. companies recorded an improvement. That is still a large majority of companies but down from 83% in the prior period.

That is why, at least for as long as the acceleration persists, your portfolio of companies should also have leverage. With overall growth high and rising, it is important for portfolio companies to accelerate faster. That requires operating and/or financial leverage.

Sell Bonds

It is the bond market that faces a sustained decline. Review your retirement accounts now and sell all fixed income investments. It is rising inflation expectations that cause the wage-price spiral that has been so difficult to control.

It has been decades since markets have experienced anything resembling tight money policy. The Long Treasury Bond yield, now 1.7%, peaked at 17.2% in March 1983. At the time evident consumer-price inflation was 15% (up 5 percentage points in the prior 9 months) and the real interest rate of 2.2% predicted that inflation would fall.

CPI Is Now 6.2%

Furthermore, consumer price inflation is 6.2%; up 5 percentage points in the past 9 months but real interest rates are an all-time low of -4.5%. This simply predicts that inflation will rise.

Despite All Those Distortions…

Corporate growth has never been higher or rising at a faster rate than it is now. The challenge is to manage portfolios through falling growth and rising interests that is now undoubtedly ahead. Make sure that the attributes of your portfolio are at least as good as the market average.

Capital markets are likely to become more volatile but a sustained stock-market decline is unlikely. Our best strategy response now is to sell all bonds and insure an equity portfolio of companies with rising growth attributes.