Crescat Capital’s commentary for the month of December 2021, discussing that software is the tell.

Q3 2021 hedge fund letters, conferences and more

Equity Market Warning

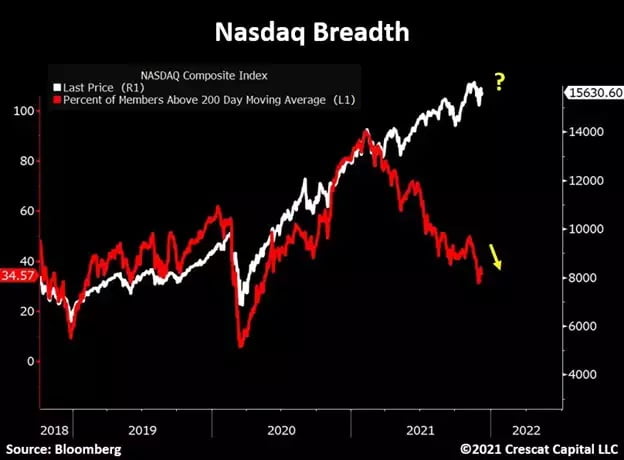

The recent weakness in the broad US equity market is being masked by the outperformance of mega-market cap companies that remain near record valuations. With that in mind, it is remarkable to us how the NASDAQ Composite is just 2.6% from all-time highs while only 35% of its members are above the 200-day moving average. Such a disconnect is corrosive. This backdrop of deteriorating market breadth is present at a time when significantly rising inflation is putting pressure on the Fed to accelerate its taper and begin raising rates sooner than it has signaled to date. With the Fed out of the liquidity pump game, weak stock market internals suggest that the long overdue reckoning of the most inflated financial asset bubble in US stock and bond history is close at hand. We believe there is substantial risk of a significant equity market selloff in the near term, even before year-end. We exclude the energy and materials sectors from this warning where equity fundamentals are driven much more by currently low valuations, scarce supplies, and robust demand.

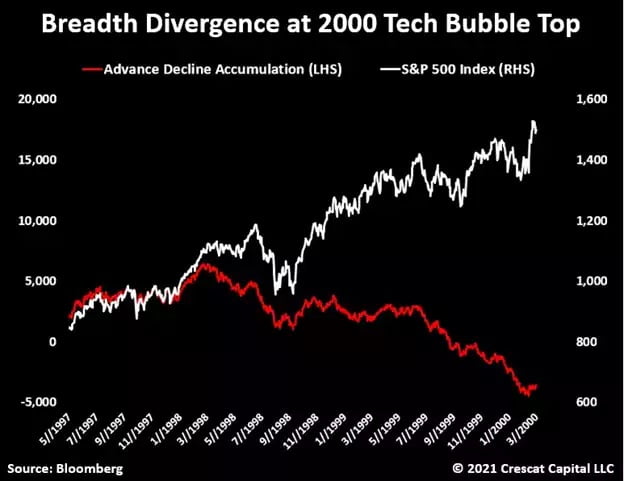

Similar Divergence Preceded the Tech Bust at the 2000 Top

We are wary of times when the generals lead but the soldiers don’t follow. It is reminiscent of the breadth deterioration at the peak of the tech bubble in March of 2000.

Most Extreme Asset Bubbles Yet

Our equity models continue to flash warning signs of excessive valuations among stocks at large. According to our research, on a median and aggregate basis, US equities are at their most expensive levels ever across a lengthy composite of underlying fundamental measures. Conventional wisdom today believes that mega-cap tech stocks are reasonably valued. However, as we showed in our August research letter, the top five market cap stocks in the US, all tech stocks, were 54% more over-valued relative to GDP than the top five market cap stocks at the peak of the tech bubble in 2000. The common refrain is that it is different this time, that P/E ratios are reasonable, that earnings are stronger, and that growth is more sustainable. P/Es had been the one area still not quite at 2000 top levels but that is not true anymore. It is true that earnings are strong, but they are anything but sustainable. There is a business cycle after all, and we are essentially at the peak of one that has been longest ever US expansion, twelve years now since the GFC. The March 2020 Covid recession was a mere blip, hardly a recession at all because there was no reconciliation of the imbalances, no creative destruction, just more inflating of the same bubbles. When it comes to P/E ratios, we believe most investors today are not even looking at them let alone factoring in the effect that sustainably rising inflation would likely have on compressing them going forward. The median P/E ratio of the top 10 largest stocks in the US is now as high as it was at the peak of the Tech Bubble, 37 times earnings.

Software Is the Tell

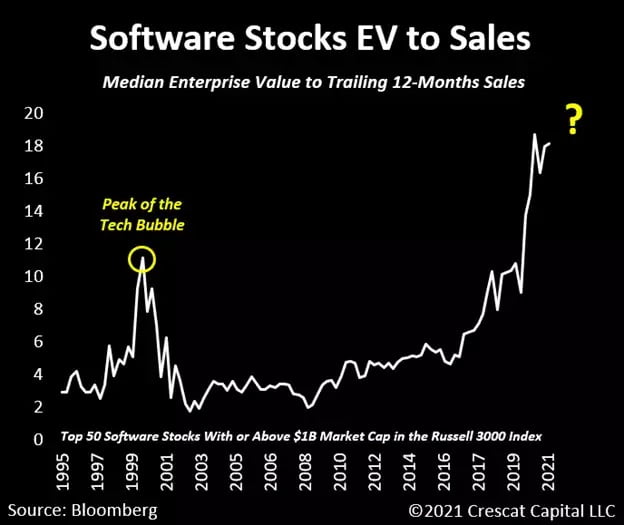

In our analysis, the software industry is the most speculative and concerning segment of the stock market. It has been the best performing broad industry group since the 2008-9 Global Financial Crisis and is more than 50% more overvalued than it was at the peak of the dotcom bubble in 2000 based on median enterprise value to sales.

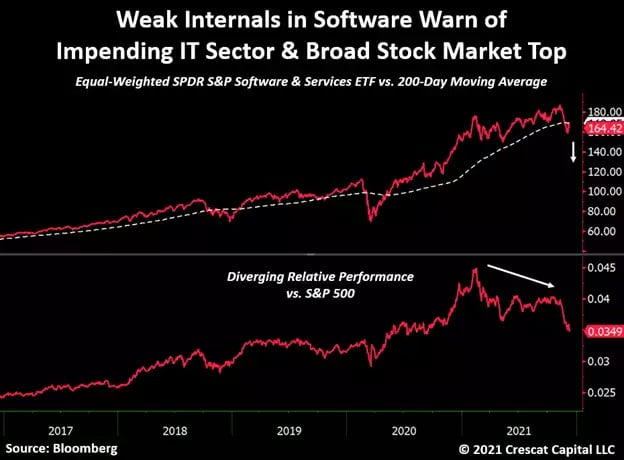

We believe most software companies have already begun a major downturn. In fact, if we look at a list of all the US-listed software companies with a market cap greater than $1 billion, the median stock is down 34% from its 52-week highs. The performance of the equal-weighted SPDR S&P Software and Services ETF has just broken below its 200-day moving average. This broad software index shows sharply negative relative performance compared to the S&P 500 since February.

Inflationary Pressure is Real

The Fed was overly optimistic in its inflation forecasting this year and has been proven horribly wrong. With CPI just clocking in at 6.8% year over year for November, inflation is already much higher than the central bank forecasted four months ago when it sold itself and the world on the idea that inflation would be “transitory”. To maintain its credibility, the Fed must now lay out a path to tighten monetary policy at a more aggressive pace.

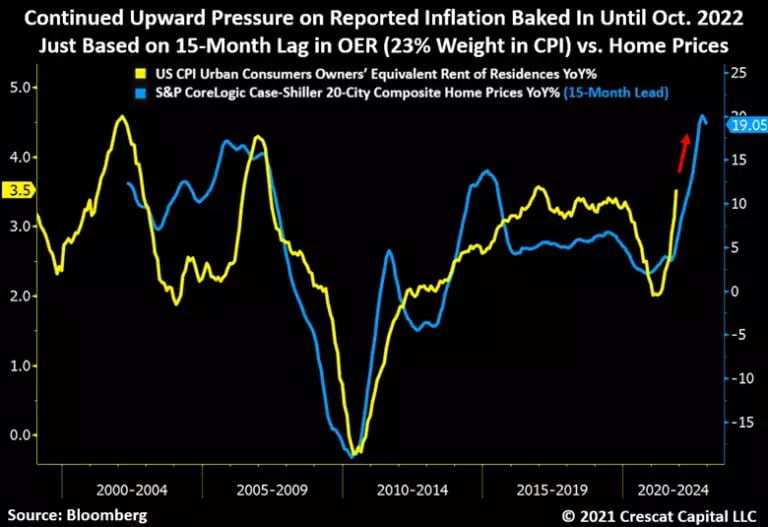

Inflationary forces in the real world and inside the CPI data are not likely to ease up soon. Based on what home prices have already signaled, and the fact that there is a fifteen-month lag in Owner’s Equivalent Rent, the 23%-weighted OER component of CPI appears poised to keep going higher until at least October 2022.

But inflation is also likely to be around for longer and at a higher rate due to structural shortages in the commodity and natural resources sectors of the economy based on years of deteriorating capital investment trends. Meanwhile, tightness in the labor market is also portending a future wage-price spiral that could continue for years. Because of these factors, we think investors are poised to rotate out of the bubble in large cap growth, mega-cap tech, uber-low yielding long duration fixed income, and into stocks and commodities that offer high intermediate-term growth, low valuations, and inflation protection. At Crescat, we refer to this broad macro theme as the Great Rotation.

Crescat Embraces Moderate Volatility in Pursuit of Superior Value-Driven Returns

At Crescat, we are macro and value investors. The Great Rotation has hardly even begun, but we believe it is poised to start playing out soon in a big way. We are positioned for it in various ways across the firm. We believe natural resource industries, specifically precious metals’ companies are true deep-value opportunities that should benefit tremendously from the current economic imbalances in the world today. Additionally, gold and silver stocks look exceptionally oversold and ripe for a major reversal to the upside in our strong opinion. Conversely, as we laid out our fundamental case for being short overall US stocks in our Global Macro and Long/Short funds, we think the recent weakness in market internals is an incredibly bearish sign that we are in the process of a major speculative top. Our Global Macro fund has additional important exposures supported by our macro research including put options on the Chinese yuan and Hong Kong dollar and a carefully crafted sleeve of fixed income short positions. We will be elaborating more on these positions in our next research letter that will be out before year end.

While much of the hedge fund industry has attempted to sell low volatility as an attribute, many of those funds have fallen short on delivering performance. Our funds are quite unique in that sense. For the last 22 years of company history, Crescat has embraced a moderate level of volatility as part of our investment process in our efforts to deliver outstanding long-term returns. After having two of the top 10 hedge funds according to Bloomberg in 2020 and delivering over 235% in the first year our recently launched Precious Metals fund, in a down year for gold and silver, it is only natural that we are experiencing a pullback. We believe that such retracements are great opportunities for new and existing clients to add capital. We feel more confident than ever in the underlying value and future appreciation potential of our portfolio.

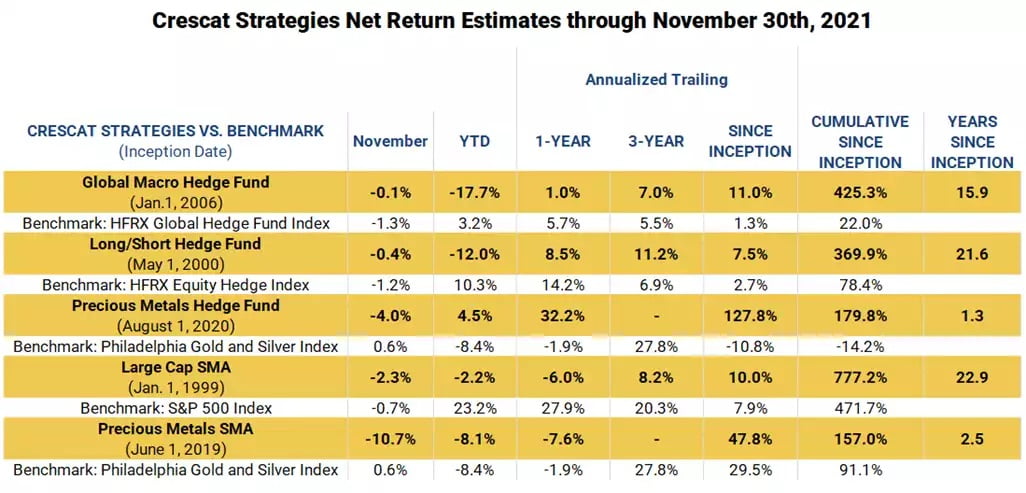

November Performance Update

Sincerely,

Kevin C. Smith, CFA

Member & Chief Investment Officer

Tavi Costa

Member & Portfolio Manager

For more information including how to invest, please contact:

Marek Iwahashi

Client Service Associate

Cassie Fischer

Client Service Associate

Linda Carleu Smith, CPA

Member & COO

© 2021 Crescat Capital LLC

Article by Crescat Capital