Euclidean Technologies letter to investors for the fourth quarter ended December 31, 2017; titled, “Predicting Future Earnings.”

In October, Jim Cramer shared his new rules for the bull market. These rules included rethink discipline and ignore valuation. [1] Following this advice could have helped you realize very good recent returns. Then, in late November, the WSJ reported that the U.S. stock market was showing the biggest divergence between cheap and pricey stocks since the aftermath of the dot-com bubble. [2]

In this context, the stars of the moment include a money manager at Fidelity who, in a recent Bloomberg profile, was heralded as an investor who flouts Warren Buffett, thinks valuation is overrated, and says most other rules of investing are “total baloney.” [3]

What to make of this?

Presumably, when an investor says to ignore or think less about valuation, he is suggesting that certain companies will eventually deliver such substantial cash flow that it makes no difference that they are priced high in relation to their existing bodies of work.

This is a reasonable view. After all, a good equity investment is made when a company is purchased at a low price in the context not of its current cash flows but of its future ones. And, if an innovative company that has yet to generate much cash ultimately delivers an extraordinary future bounty, it may eventually prove to have been a very good investment even when initially purchased at a high price.

But how easy is it to repeatedly and successfully invest this way? Doing so requires that you identify in advance those companies whose financial results will vastly improve over time. Put another way, you have to successfully predict future earnings.

During bull markets, it certainly feels possible to make these predictions and identify future winners. Investors wear rose-colored glasses, anticipate good developments, and bid up shares in exciting, innovative companies, often until their prices become disconnected from current earnings. As investors’ paper wealth grows in this context, they get welcome but potentially misleading feedback regarding their prescient abilities. The test eventually comes when others’ willingness to bet on the future wanes. Then, one of two scenarios ensues. Either a company begins to generate enough cash to bolster a valuation that may have previously been built on hope, or a company’s financial results are too slow to emerge, causing its shares to decline as it is exposed as having been the object of unfruitful speculation.

So what does it take to successfully predict future earnings and end up on the better side of this spectrum? It is a timely question, given that many now view valuation as a tired touchstone to be ignored or deemphasized. To explore the extent of the challenge posed by this question, we will look at investors’ track record of predicting earnings. Then, we will introduce the opportunity to use modern analysis (e.g., machine learning) to improve these predictions.

How Well Do Investors Predict the Future?

More than ten years ago, we encountered David Dreman via his book, Contrarian Investment Strategies. We were on our own journey, looking at the data on public companies and their investment outcomes, and becoming convinced that there were systematic structural and human biases that impacted equity prices. His book was a revelation and encouraged us to keep looking for ways to identify the blind spots in investing’s accepted wisdom. One subject Dreman documented in that book was the extreme error, and optimistic bias, characterizing analyst predictions of future earnings.

Dreman analyzed over 500,000 earnings forecasts from Wall Street analysts, stretching across 25 years and 1,500 public companies. He found that, even with forecasts made only three months in advance, the average analyst forecast error was in excess of 40%. He also found that analysts had a strong optimistic bias, or tendency to overestimate future earnings. More recently, StarCapital extended Dreman’s research by looking at more than 1.7 million documented forecasts over a period of 33 years. [4] They found that, when predicting earnings a year in advance, the average analyst error was greater than 30%. Significant rates of analyst forecast error are evident regardless of how you control for outliers and whether you analyze results by industry or market environment.

Thus, accurately predicting earnings seems to be a pretty tall order. If the best minds, with deep industry expertise and access to management, are generally wildly off in their predictions of future earnings, should you expect your own predictions to be especially reliable? Instead, you might reasonably conclude that earnings are too difficult to accurately predict. It would naturally follow that you would question the basis for different companies’ shares being offered at wide-ranging valuation multiples on current earnings.

You see, investors’ predictions for future earnings growth are reflected in the relative valuation multiples they are willing to pay for different companies’ shares. Companies that are expected to grow earnings generally earn higher multiples, and companies whose financial results are expected to decline endure lower multiples. But, since investors are not good at accurately predicting future earnings, you should not expect companies’ relative valuation multiples to tell you much about the different rates at which those companies will actually grow earnings! [5]

Accepting that the future is difficult to predict logically leads you toward betting against extreme investor predictions. You would seek to purchase the companies priced lowest in relation to current earnings and avoid those companies trading at the most expensive valuations.

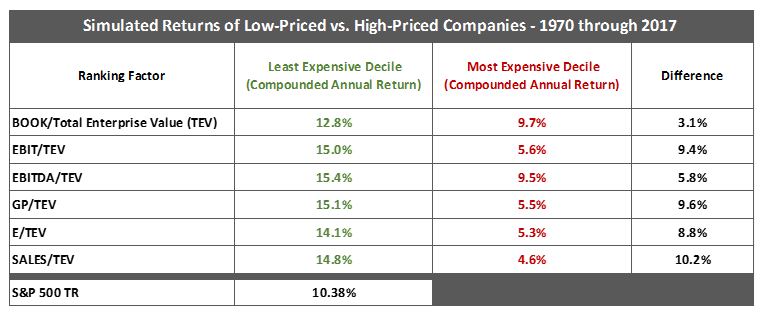

Interestingly, it seems that such a conclusion would have positioned you for very good long-term investment returns. The chart below shows simulated results realized from 1970 through 2017 from owning companies that were priced low and high in relation to current financial results.

See Euclidean’s Q2 2017 letter for factor definitions and simulation assumptions. Historical simulated results presented herein are for illustrative purposes only and are not based on actual performance results. Historical simulated results are not indicative of future performance. Please see important disclosures at the end of this document.

As you can see, it would have been fruitful to own portfolios of companies that are priced low, and not high, in relation to current earnings. This supports a conclusion that valuation multiples are not good indicators of future cash flows. If they were, you would not expect to see such a big difference in returns between cheap and expensive companies. Indeed, there has been a very substantial cost to investing based on the belief you can predict which companies will deliver better results in the future. There has also been a great reward for simply abstaining from earnings predictions and buying shares in companies where other investors’ pessimistic predictions create opportunities to buy companies at low-prices.

Commitment to Our Craft: Machine Learning and Earnings Predictions

Following these lessons, which have persisted across most of investing history, has not been especially rewarding during recent years. Rather, it has been more lucrative to own “growth” stocks, which are expensive in relation to current (or nonexistent) earnings. So has something changed such that a valuation focus is now in fact overrated? Are yesterday’s rules of investing total baloney?

We do not think so. Instead, our sense is that we are in the midst of one of those times required to shake out weak hands and create the wide dispersion in company valuations necessary for disciplined, value-minded investors to generate good long-term returns. There is, after all, plenty of financial history that rhymes with what is going on nowadays. For example, we lived through the late 1990s, when people last questioned whether valuation mattered and if the value paradigm had gone the way of the dinosaurs. Following that time, and subsequent to other exuberant times in the past, the capitulation of value investing in favor of “betting on the come” has preceded periods when value stocks delivered some of their best absolute and relative returns.

This is a big reason we are not tempted to deviate from our approach. Rather, we are encouraged to use these times to further hone our craft. There is a great renaissance going on with the machine learning technologies that we use to find meaning in the vast body of corporate and stock market history. These tools are behind improvements in self-driving cars, computers that can teach themselves how to master various games, and machines that have achieved better-than-human skill at image recognition. Thus, we devote our energy to exploring how the technologies and practices behind these developments might add to our investment process.

Along these lines, given that investors have proven to be especially bad at predicting earnings, we became interested in seeing how well machine learning could do with this task. Maybe investors have a variety of human biases that make earnings prediction difficult, whereas an unbiased application of historical, quantifiable experience could do a better job?

To this end, in November, Euclidean published a paper in partnership with Zachary Lipton—a friend, researcher at Amazon AI, and professor at Carnegie Mellon—to show how machine learning can be applied to predicting future company fundamental data, such as earnings, from past fundamental data. Specifically, we trained deep neural networks to forecast future fundamentals based on a trailing five-year window.

We showed that these neural networks do a pretty good job. For example, they are good enough at predicting future earnings to meaningfully improve the simulated investment performance of widely researched and commercially applied quantitative investment strategies that use valuation ratios. If you are interested, you can see the results in the paper here and also listen to a Bloomberg podcast where John and Zack discuss the results.

The paper’s results raise interesting questions. First, to what degree might future earnings be more predictable than one might assume based on the poor record of Wall Street consensus earnings forecasts? Second, what is it that so severely impedes investors’ abilities to rationally assess companies’ future prospects?

With regard to this second question, our hunch is that various human behavioral biases limit people’s ability to process large amounts of information and make good decisions. People tend to put too much weight on recent experience and, often wrongly, expect recent trends to continue into the future. People also tend to treat each situation as unique, and underweight historical outcomes associated with similar situations.

This is why, in many fields characterized by high degrees of uncertainty, statistical formulas based on past experience have been shown to provide better predictions than not only people in general, but also better than collections of experts. Daniel Kahnemans’ book, Thinking Fast and Slow, explains how this has been true in a wide range of fields, from estimating the likelihood that a convict will violate parole all the way to whether a candidate will have success in pilot training. We believe that this is also true in the realm of company valuation and earnings prediction.

Thus, our conviction is high regarding the merits of a systematic approach to long-term investing, especially one formed from the lessons of history and focused on undervalued opportunities. We will to adhere to—and seek opportunities to refine—our process through the market’s ebbs and flows.

Best regards,

John & Mike

The opinions expressed herein are those of Euclidean Technologies Management, LLC (“Euclidean”) and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Euclidean reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Euclidean Technologies Management, LLC is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Euclidean including our investment strategies, fees and objectives can be found in our ADV Part 2, which is available upon request.

[1] CNBC | Cramer’s 6 Rules for Investing in a Raging Bull Market [2] WSJ | Investors Finding Little Value in Value Stocks [3] Bloomberg | Fidelity Manager Buys Everything Crypto [4] Star Capital | EPS Forecasts [5] For some good research demonstrating that this is in fact the case, see this paper from LSV Asset Management.

{kind=link}