The term “network effect” gets too often ascribed to businesses that don’t truly possess one, but a true network effect is one of the most valuable advantages in business, and something I always watch for when studying companies. When combined with a marketplace business model, the result can be a toll road, taking a high margin royalty on the commerce that happens on its platform. They usually have very attractive economics with low capital requirements and often little to no marginal costs, which means expanding profitability as the business grows. But the most important feature of a true network is that it gets stronger as the business grows. Network effects defy the nature of capitalism — profit margins expand while simultaneously becoming harder to competitors to attack.

Q1 2021 hedge fund letters, conferences and more

Metcalfe’s Law says the value of a network is the square of the number of participants on the network. This is of course a loose approximation but one that is directionally correct. If a telephone network has 10 customers, Metcalfe’s Law says value of the network is “100” (i.e. 10×10). If this network adds a phone, going from 10 to 11, the value is now 121 (i.e. 11×11). The size of the telephone network grew 10% but the value rose by 21%. If this network goes from 10 users to 20, the value is now 400. The size doubled but the value quadrupled. Each new user that purchased a telephone in the early years exponentially enhanced the value for each existing customer. And with each new customer, the network became both more valuable and more difficult to attack. The biggest network effects trend toward becoming monopolies, which of course happened eventually with AT&T, one of the first modern network effects. The internet has significantly improved the economics of the best network effects by removing a lot of variable costs to serve new customers and eliminating much of the capital required for growth, and this expedites this path toward monopoly. Of course, not every true network effect gets to the legal definition of monopoly status, but they all enjoy monopoly-like profits.

Growth in Etsy’s Network

Etsy Inc (NASDAQ:ETSY)’s network has grown from 2.7 million sellers and 46 million buyers at the end of 2019 to 4.7 million sellers and 91 million buyers today. Also, each member of the network is more engaged, and spending more money on average. This network is exponentially more valuable than it was pre-pandemic, and the future cash flow is in my view going to be much larger and also more predictable.

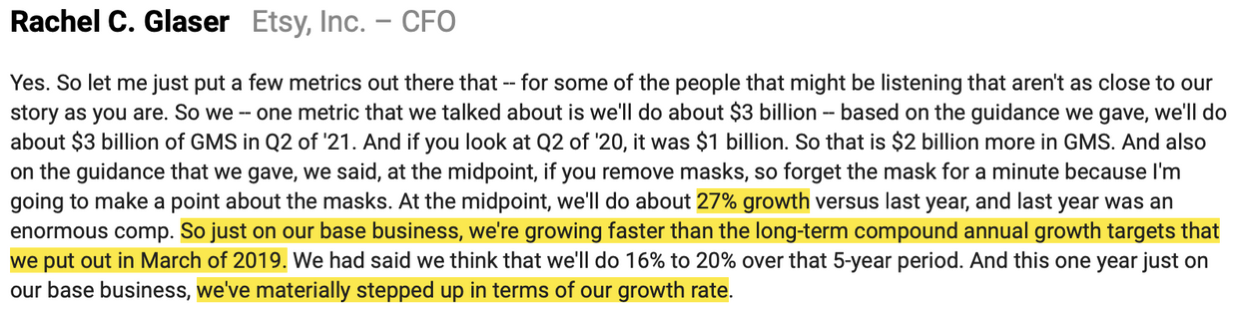

The company recently participated in a conference and I wanted to highlight two points. First, the company is still growing fast:

So Etsy’s core business is growing 27% in Q2 off of last year’s incredible Q2 2020 when the overall business grew 145%. “Mostly Borrowed Ideas”, an investment analyst who does outstanding research (highly recommend is newsletter, which I am a happy subscriber to) shared this same point regarding the Q1 numbers:

It’s the same point I have been making after Q1. Post-pandemic, Etsy seems to be decidedly a better business.https://t.co/VHHHy9Kfws

— Mostly Borrowed Ideas (@borrowed_ideas) June 10, 2021

Etsy’s core (ex-masks) business grew 32% in Q1 over last year’s number, significantly faster than historical growth rates.

The business is bigger, more profitable, and growing faster than it was pre-pandemic. Metcalfe’s Law in action.

Habitual Buyers

Another datapoint that demonstrates network effect strength is the growth in what Etsy calls “habitual buyers” — buyers who shop at least 6 times per year on Etsy or who spend $200+ per year. This cohort is Etsy’s most valuable group, and it is also growing the fastest, up 205% in Q1:

So Etsy is still growing near 30% in the core business and its most valuable customer segment is accelerating their shopping frequency. The network has gotten bigger, the users are participating more often, and the profitability has exploded higher with operating margins going from 11% to 27% in just a year, even as the company continues to invest heavily in marketing and product development. Etsy did $2 billion in revenue over the last year, of which $700 million turned into cash flow.

A $25 billion market cap for this level of production wouldn’t normally get me excited, but for a network that is exponentially stronger and more profitable than it was a year ago and the very long runway for the ecommerce industry, I think this could prove to be a bargain.

Related: I discussed Etsy in more detail in an interview with Columbia’s Graham and Doddsville, and also in a recent podcast with Matt Samuels that I linked to in the last post.

Thanks for reading!

Article by John Huber, Saber Capital Management