This article is the accumulation of my thinking around the Digital Asset space as I have become more deeply involved and have begun to understand the different assets and narratives that drive them.

Q4 2020 hedge fund letters, conferences and more

My feeling is that the narratives in the space are behind the times, and stem from the world of 2017 when the adoption of bitcoin was just taking hold and every other digital asset was a threat. After 2017, we saw the crypto winter, where the entire space fell nearly 90%. People are scarred by those events. Many people made a lot of money and many people lost a lot of money in 2018 and 2019.

In this article, I’m trying to bring the narrative forward and bring some clarity on how to address the space that is based less on tribalism and emotion and more on a pragmatic approach to the entire subject.

There is complexity in this article which might be deemed unnecessary for GMI purposes, but my guess is that this article will becomes rather public as its conclusions are somewhat contentious for many people in the space. I’ve tried to clarify concepts where possible and have also enlisted some help for the more in-depth sections.

I hope you find it useful and interesting and that is widens your understanding of how to invest in the space more successfully.

Crypto Tribes

It might seem odd to a macro investor like you, but the crypto world is driven by deep tribalism.

As macro investors, yes, we have our favourite themes, but we always acknowledge the counter argument and other possible futures. We know there is no truth, just outcomes, and we place our bets accordingly and adjust the probabilities endlessly.

We are agnostic mercenaries, in search of optimal returns.

The Maximalist Tribe

In the bitcoin space, the tribalism is most fierce. It is so fierce that it has a name – Bitcoin Maximalism.

The beliefs of this group are that all other crypto assets are inferior to bitcoin and that bitcoin is the only possible winner in a winner-takes-all world. The end state is “hyperbitcoinization” where the entire global system of money, transfer of value and trusted ownership all occur on the bitcoin blockchain and its various layers.

The idea is that bitcoin is more than an asset, it is the only monetary asset that survives and thrives – the cockroach in the financial nuclear winter of money printing, societal collapse and government intrusion. It is a future world where inflation is not driven by central banks but just by cyclical demand and supply, and where you are your own bank, and the entire financial industry disappears as everything gets done with bitcoin and on the bitcoin blockchain in a decentralised world.

This is an alluring future for many. This is the chance to start a revolution. To get in on the ground floor and own something that is so scarce that early holders will become obscenely rich. It offers people the ability to control their own lives.

As you are aware from my writings in GMI, this is an addendum to the theme of societal discord driven by the massive relative wage deflation of the last forty years that led to massive debts, all driven by demographics, globalisation, fiat money and technology.

I get it.

I also share in some of that optimism. I also do assign a probability that hyperbitcoinization could happen in the next thirty years. I just don’t assign the same utopian outcomes or the libertarian philosophy in a world of no taxes – the sovereign individual, free of all claims on them.

This is why I don’t belong to this tribe, while I respect their desire for a better world. Bitcoin is a truly amazing breakthrough for the financial architecture of the world.

Everything is a scam

What I find strange however, is that this core group of bitcoin maximalists so strongly reject any other cryptocurrencies, protocol, digital asset or project that isn’t built on bitcoin. They generally refer to them all as scams and offer the advice of “Have fun staying poor” if you don’t agree. They think there is only one way to win and it’s bitcoin, shit or bust.

The attacks on social media really surprised me when I didn’t fully align myself with their philosophy. I shared their deep love of bitcoin, it is my biggest ever personal investment, but that wasn’t enough… Hilariously, I was deemed a scammer for even looking into or researching other opportunities in the space. The toxicity of the personal attacks is a tiresome hindrance and is off-putting to many. It would be so much better if they spent more time explaining why their ideas have strong merit (which the good guys in the space do tirelessly in order to help others).

Imagine in the macro world if you only believed in US bonds and that any other bond was a scam. You would thus ridicule anyone who owned anything else because only the US could pay its debts – as the only sovereign nation with the reserve currency status – and everything else was therefore deemed worthless.

Our world doesn’t work like that. Our world is about investing and what offers the best risk-adjusted returns at that point in the investment cycle.

Asset allocation

We look at the world in terms of:

Liquidity preference – how fast can I sell something to get me back to an asset that won’t lose money. In the global world that is cash and short-dated government bonds. But it could be the S&P 500 benchmark, if you are an equity investor. Or it could be A+ credit for a credit investor etc.

Time Preference – How much visibility and security do I have in the return profile of an investment that allows me the benefit of holding it for a longer duration i.e., can I buy and hold it, and will I get compensated for doing so? Different investors have different time preferences. Endowments tend to have the longest and day traders the shortest.

Risk Preference – If I have the visibility that an asset class will perform over a longer duration, can I juice the returns by taking on more risk? The great example of this is that when emerging markets outperform, I might eventually move out on the risk curve to frontier markets.

Or I might be a gold bull and eventually buy gold equities and then junior miners. All come with more risk. We spend our lives calculating that risk-adjusted return potential. High risk tends to come with lower holding periods too.

That is how asset allocation works.

But I feel like an alien when I talk about this in the crypto markets because so few people have come from traditional investing, so are learning over twelve years of asset price history only. Therefore, they suffer recency bias in what worked or didn’t work previously, and then construct narratives around it to give them comfort in their current investments. We all do that to some extent but not with such a short history.

The Behaviour Machine

But why the deep tribalism in bitcoin?

Simple.

If you were to design an experiment in creating optimal network effects, you could not create a more robust system that a network based around a new form of money.

The more the network grew, the more the participants would make money. If it’s a currency or a system of money itself, there is no price anchor, unlike a discounted cash flow etc.

Bitcoin is the greatest behavioural economics-based network of all time.

It has the best narrative – the world’s hardest money and a new system of finance that is fairer AND every time someone joins it and buys bitcoin, it goes up in value due to the restricted supply.

It is literally genius. It does actually work as superior money too. It is in fact a quantum leap in money.

All money is a trust-based system and this is no different, but it’s the supply dynamics and the narrative that makes it so compelling to humans. It plays to our basic behavioural instincts.

Metcalfe’s law

In that regard, bitcoin is a natural extension of the behavioural economics revolution that drove the network effects of the social networks – Metcalfe’s Law.

From Wikipedia:

Metcalfe’s law states the effect of a telecommunications network is proportional to the square of the number of connected users of the system (n2). First formulated in this form by George Gilder in 1993,[1] and attributed to Robert Metcalfe in regard to Ethernet, Metcalfe’s law was originally presented, c. 1980, not in terms of users, but rather of “compatible communicating devices” (e.g., fax machines, telephones). [2] Only later with the globalization of the Internet did this law carry over to users and networks as its original intent was to describe Ethernet purchases and connections.[3]

The big breakthrough in Silicon Valley came when Daniel Kahneman gave a now-famous lecture in 2007 to the leaders of the rising tech companies. In attendance were ALL of the Silicon Valley players.

Kahneman taught them the power of behavioural economics and how to effect behaviour via nudges and other tricks.

Directly out of this came the modified “like” buttons that allowed people to express the key emotions of anger, love, joy etc., creating further engagement. They literally began playing on emotions to drive engagement. Out of this also came the cognitive bias functions of YouTube algorithms and the sales techniques of Amazon’s marketplace.

It took the network effects and the power of Metcalfe’s Law to drive up share prices to a new equilibrium (and indeed a new method of valuation). The more people joined the networks and engaged in them, the more valuable the companies became. It was nothing short of a revolution that has now spun into politics and is spreading into finance with cryptocurrencies and the rise of central bank digital currencies. It is all about behavioural incentive systems. And if you can drive more incentive to your platform, you capture the value.

In Silicon Valley, Facebook et al created hyper engagement to drive up time-on-site to compete in the attention economy. Any network that managed to climb Metcalfe’s Law made the shareholders extremely rich: Facebook, Google, PayPal, LinkedIn, Amazon, Reddit, Twitter, Uber, AirBnB. Etsy, etc.

But in cryptocurrencies, the owners of the currencies are the ones that get rich in a distributed system. The owners and the network effects are one whereas in Facebook, they are two sets of players – the users and the shareholders.

This is super powerful and the result is that individuals become evangelical about their chosen cryptocurrency. Literally, if they can persuade people that only their system has value, then they capture ALL of the value. And humans being humans will always try to do that. That is the power of behavioural economics…

We then justify our actions with alluring narratives. Gold bugs show a similar disposition and for similar reasons, but technology allows bitcoin and others to be supercharged networks with instant, frictionless transfer of value.

As I mentioned before, there are some hypernarratives around bitcoin and then there are other more pragmatic narratives (which could also be right or wrong) and which use the commonly observable phenomenon that in a competitive technological complex arena such as blockchain, almost all solutions are suboptimal for varying reasons: speed, levels of trust, cost, flexibility etc., and therefore there will likely be multiple winners (and even more losers).

Also, different blockchain and crypto protocols serve different needs. Not everyone needs bitcoins’ level of trust, for example. Bitcoin works particularly well as a store of value but, as yet, less so as a payments network or a transfer network or smart contract network etc.

Some believe that all of this will be solved on the bitcoin blockchain as different layers are built out. Bitcoin WILL evolve in its different layers, it will offer competition to some elements of other digital assets, as will others. Bitcoin WILL be a huge part of the future. But will it be the entire future?

The rest of us own bitcoin and others because we don’t think it offers the right risk profile to make one choice this early in the game and, witnessing history that strongly suggests multiple outcomes are by far the highest probability.

My job here is not to suggest that anyone is right or wrong but to allow an understanding of the different points of view.

But this is where things get weird…

The key argument made by maximalists is that all other digital assets, aside anything on the bitcoin blockchain, will trend to zero in value and that only bitcoin will accrue value. The key paper on this was a dense and interesting piece of work by John Pfeffer, an ex-KKR partner entitled, “An (Institutional) Investor’s Take on Cryptoassets”.

https://medium.com/john-pfeffer/an-institutional-investors-take-on-cryptoassets-690421158904

In a long and complex discussion which is well worth reading, Pfeffer uses Monetary Theory to analyse the crypto space using the familiar equation MV=PQ.

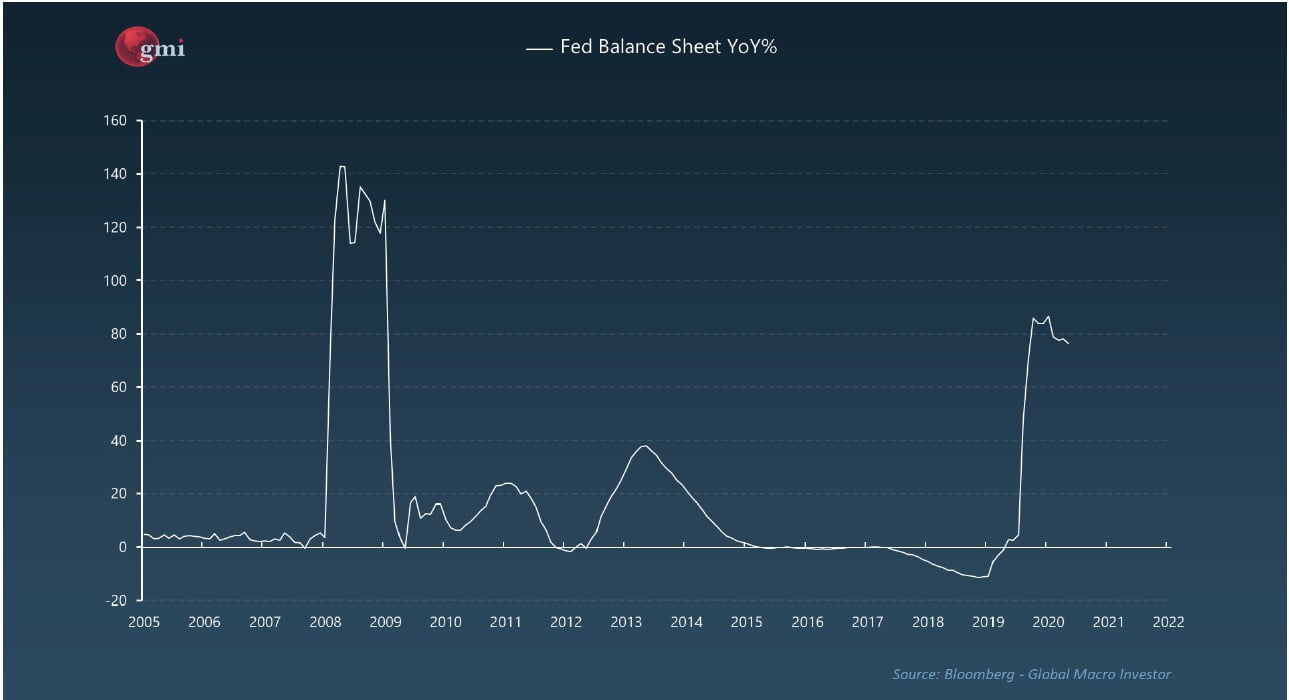

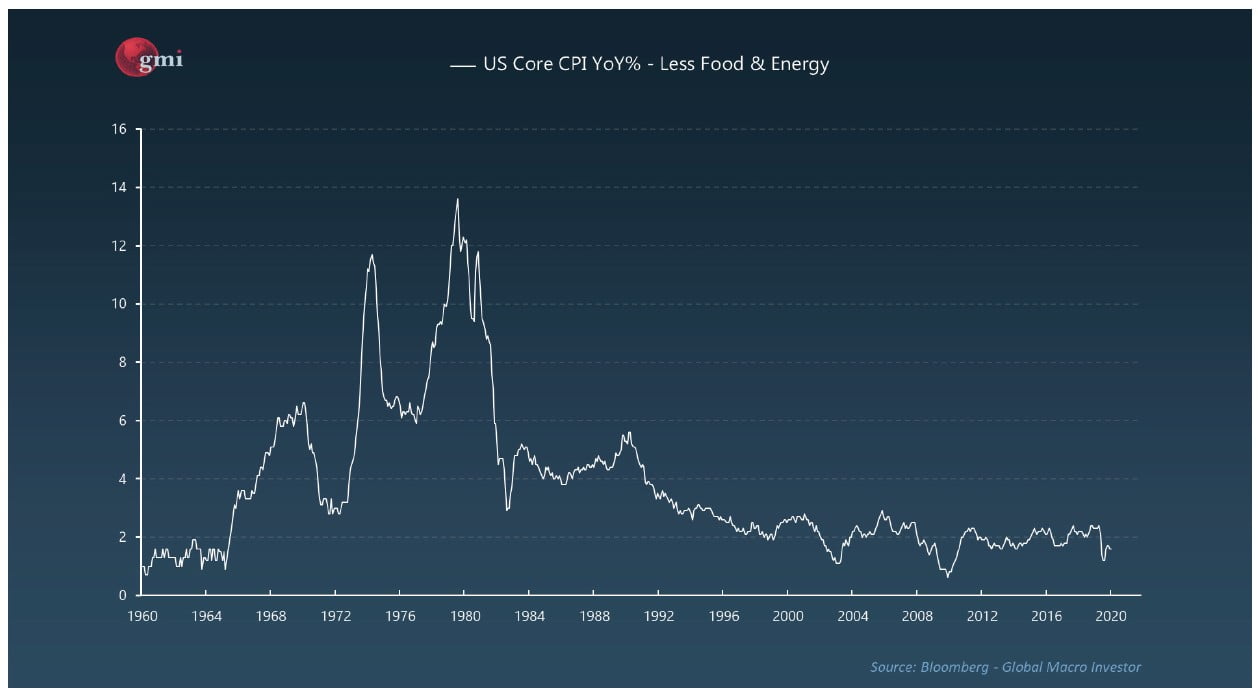

I am no fan of Monetary Theory; it has failed to describe the modern world we live in, whether it is due to velocity of money or of the assumptions it is based upon. The core assumption is that the key driver is supply. It is 100% clear to me that the growth in the Fed Balance Sheet…

… has ZERO correlation with CPI…

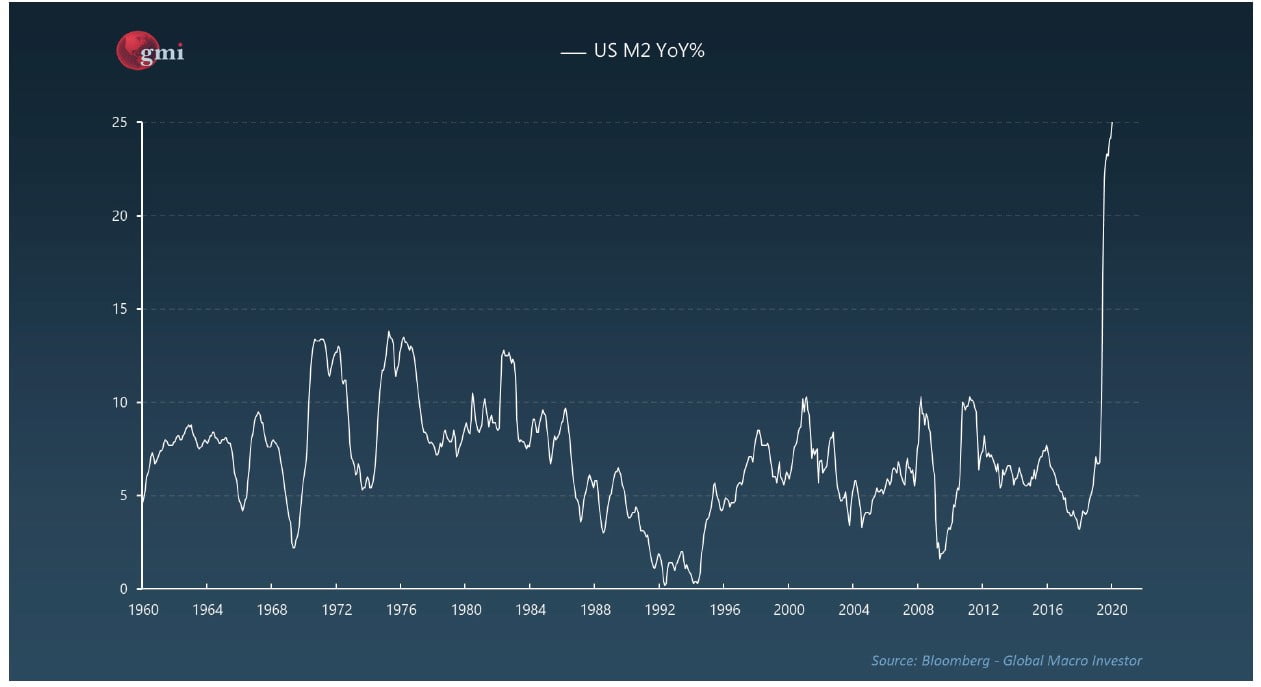

Or we could use M2, if that is your favoured way to measure money supply. Again, zero point zero correlation in the real world…

Read the full article here by Raoul Pal, Real Vision.

About Raoul Pal

Raoul Pal is also the founder and CEO of Real Vision, a digital media group. Previously he co-managed the GLG Global Macro Fund in London for GLG Partners, one of the largest hedge fund groups in the world. Raoul moved to GLG from Goldman Sachs where he co-managed the hedge fund sales business in Equities and Equity Derivatives in Europe. In this role, Raoul established strong relationships with many of the world’s pre-eminent hedge funds, learning from their styles and experiences. Other stop-off points on the way were NatWest Markets and HSBC, although he began his career by training traders in technical analysis.

Raoul also publishes Global Macro Investor (since January 2005) providing original, high quality,

quantifiable and easily readable research for the global macro investment community hedge funds, family offices, pension funds and sovereign wealth funds. GMI draws on his considerable 30 years of experience in advising hedge funds and managing a global macro hedge fund. Global Macro Investor has one of the very best, proven track records of any newsletter in the industry, producing extremely positive returns since inception: www.globalmacroinvestor.com.