A quick update on this micro-cap data analytic software company.

Tangible YTD 2018 progress doesn’t reconcile with a -27% stock price decline. Over that time DWCH reported Q4 2017 YOY revenue increase of 19% for total revenue of 10.20M. License revenue was 5.90M or +32% YOY. Quarter 1 2018, 16% YOY increase or 9.60M in revenue with 5.6M in license revenue (28% YOY increase). Further, the launch of Monarch Swarm platform offers an enterprise solution for team driven data preparation. It offers a centralized data marketplace with improved governance. Monarch Swarm expects revenue recognition in the 2nd half of FY 2018.

January 31, 2018, Datawatch purchased Angoss Software for $24.5 Million. The Angoss acquisition adds predictive analytics software to its now complete enterprise offering for data intelligence; Swarm(team leverage), Monarch(data prep), Panopticon (real-time in motion data analysis). Immediate synergies exist for Datawatch purchase of Angoss. Datawatch shares many customers in the financial industry.

“Angoss Software Corporation, a privately-held data science platform provider based in Toronto, Canada. The acquisition will augment Datawatch’s Monarch data intelligence offering with expanded capabilities that enable data scientists to perform predictive and prescriptive analytics in a wide variety of enterprise applications. The transaction was completed today for US$24.5 million in an all-cash transaction, which was financed through a combination of Datawatch’s cash on hand and funding from a new credit facility with Silicon Valley Bank.”

Improved operations, double-digit top-line growth, near-term Swarm enterprise sales, and now Angoss offers strong upside synergies. Datawatch’s Panopticon real time in motion data visualization used at major financial institution can integrate with Angoss predictive analytics. They both share customers in the financial services /asset management industry.

The current corporate IT budget spend for the internet of things and real time is a fraction of the industry’s future. IOT is yet to be a factor for DWCH. But Panopticon and Angoss can become an important force. So now Datawatch offers a complete enterprise solution for an end-to-end solution for data preparation, predictive analytics, and machine learning. The initial stage of a more focused Datawatch is a real expectation for a company that’s made epic operational mistakes from 2012 to 2015. So, after the Angoss acquisition, Datawatch management published financial commentary. Based on the twelve-month results through December 31, 2017. The combined entity expects 48.20M in revenue and 2.3 Non GAAP net income of 2.3M.

Additional YTD news, Imagine Software incorporates Datawatch’s Panopticon into its Real-Time Portfolio, Risk and Compliance Management Solutions. Baker Tilly forms a strategic partnership with Datawatch. They use Datawatch’s Monarch preparation and automation in their Revenue Cycle Innovation Center. This is an end-to-end solution for healthcare organizations to maximize and manage revenues. Further, the average renewal maintenance spend per customer is up 5%.Partnership revenue is 15% for the recent quarter near an all-time high. The near-term future goal is 30%. On a fiscal year basis, the average license spent per customer, both perpetual and subscription is up around 10%. The operational goal of cash flow breakeven essentially realized 2 quarters ahead of internal forecast.

Consider the margin of safety not found in the financial statements. January 2018 Datawatch hired an adviser to handle acquisition approaches. There were several outside offers but nothing materialized. This news coupled with insiders owning ~15% of the company and a management team and board motivated and incentivized to sell the company at favorable prices.

Valuations and recent financial peformance.

Relative valuations:

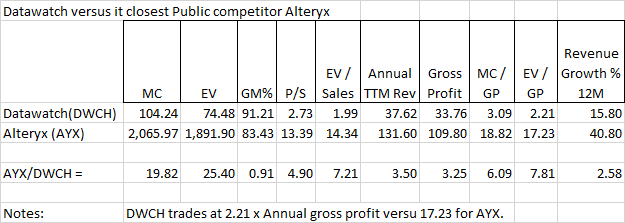

Datawatch closest public competitor is Alteryx. The table below compares both companies and highlights the large differences in valuation.

Additional examples of relative acquisition value are below. It’s not a perfect comparison but close. Examples are in the same data analytics software space.

February 2015, Hitachi Data Systems acquired open source business intelligence and analytics specialist Pentaho. The acquisition value was not disclosed. It’s estimated between $500 and $600 million or 7 times Pentaho’s annual revenue of 85M. HDS motivation is to gain same market access as the much smaller Datawatch.

Spring 2016, Qlik goes private by a private equity firm for 3.40B with an annual revenue of 3B, ~3.40 times sales. Fall 2014, Open Text buys struggling Actuate for $330 Million or 2.6 times annual revenue. TIBCO goes private for approximately $4.3 billion or ~4 times sales. It’s worth noting. Tibco uses Datawatch’s panopticon for in motion real time analysis. Tibco white label’s Panopticon and integrate into their software.

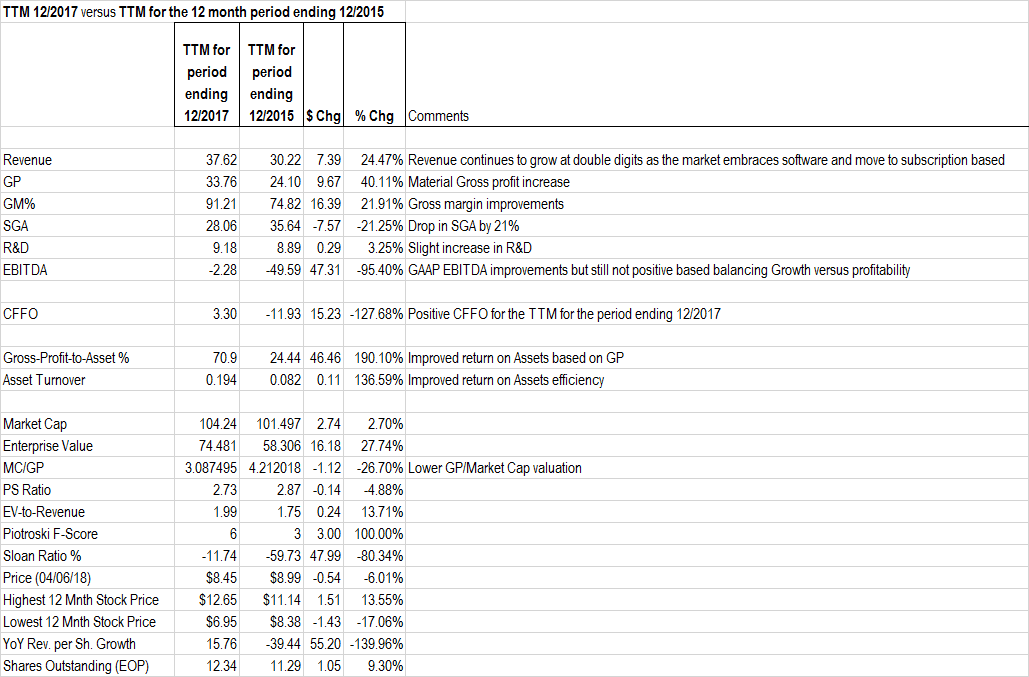

The simplest and direct method to derive today’s intrinsic value. Take DWCH’s TTM gross profit of 33.72M and multiply by a conservative number of 4 to arrive at a value of 135.048M. This is ~ 45% greater than the current DWCH enterprise value. But if things keep improving and Swarm and Angoss perform as expected. DWCH valuation goes much higher.

Risk:

Risks to the company’s financial future are real. The recent 24M Angoss acquisition uses 15M of the current 30M cash balance with the remaining in debt. Their prior acquisition of Panopticon was a disaster. Its destroyed shareholder value and a wasteful distraction from their core competency for several years. But, I believe the recent outside interest in the company provides a margin of safety. Datawatch is still a speculative micro-cap. I’m willing to take the risk.

Long: DWCH

Article by ShadowStock