Dan Loeb’s letter to Third Point investors for the third quarter ended July 2021, discussing the top winners in Q3; Upstart Holdings Inc (NASDAQ:UPST) and SentinelOne Inc (NYSE:S).

Q3 2021 hedge fund letters, conferences and more

Dear Investor:

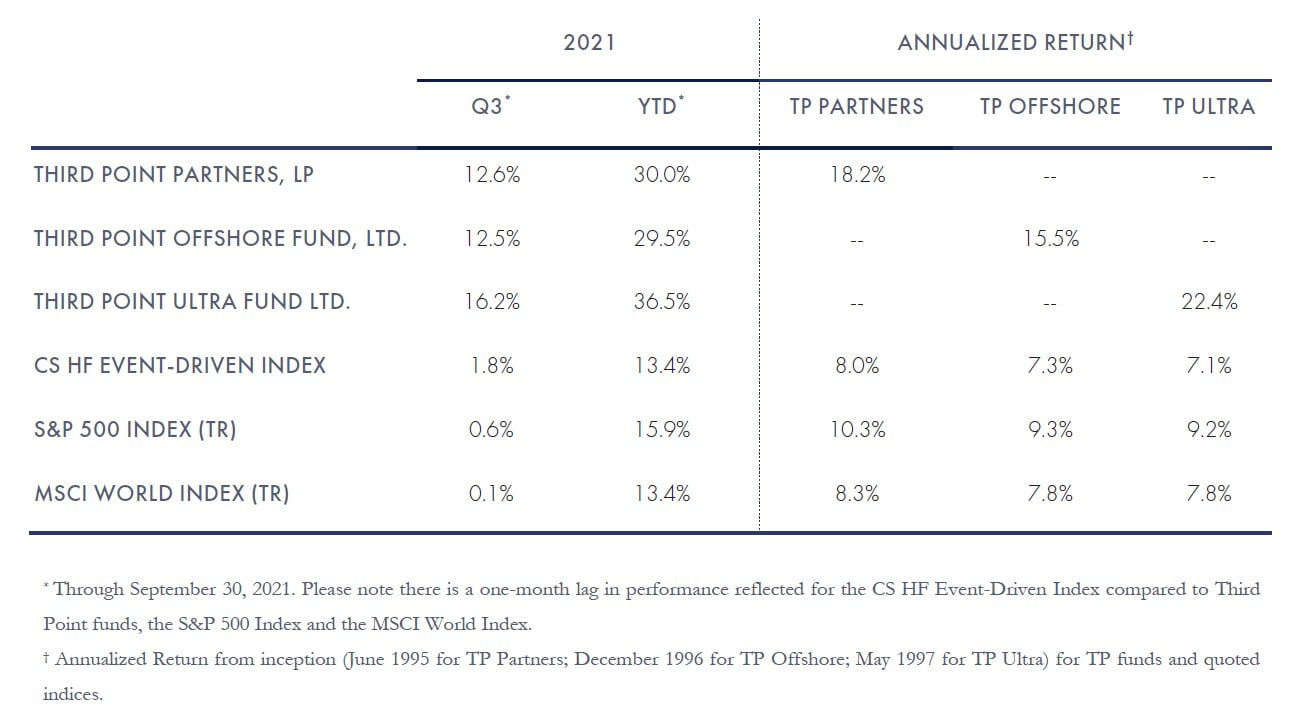

During the Third Quarter, Third Point returned +12.5% in the flagship Offshore Fund and +16.2% in the Ultra Fund, bringing year to date returns to +29.5% and +36.5%, respectively. Assets under management at September 30, 2021 were approximately $19.3 billion, including $863 million in the Third Point Structured Credit Opportunities Fund.1

The top five winners for the quarter were Upstart Holdings Inc (NASDAQ:UPST), SentinelOne Inc (NYSE:S), Prudential Financial Inc (NYSE:PRU), Danaher Corporation (NYSE:DHR), and Avantor Inc (NYSE:AVTR). The top five losers for the quarter were Paysafe Ltd (NYSE:PSFE), SoFi Technologies Inc (NASDAQ:SOFI), DiDi Global Inc (NYSE:DIDI), Uber Technologies Inc (NYSE:UBER), and Burlington Stores Inc (NYSE:BURL).

Our top winners on a percentage basis in Q3 were our two largest positions; Upstart, up 153%, and SentinelOne, up 26%, as public market investors rewarded both companies’ disruptive business models and high-growth trajectories. Upstart has started to upend the FICO-dependent, $84 billion unsecured personal loan market with its AI-driven underwriting approach and is ramping up its footprint in the $685 billion auto lending market. In its most recent earnings report, the company raised its full-year revenue estimates by 25%. We expect SentinelOne to grow rapidly and continue to gain market share over the next decade as flexible work patterns, cloud adoption, and IoT create more security vulnerabilities. This market is still dominated by legacy vendors whose solutions pale when compared to SentinelOne’s autonomous, machine-learning based security, which is taking share and helping the company grow annual recurring revenue by more than 100% year-over-year.

2021 has been a good year for our portfolio and markets. Risk assets have climbed a wall of worry as easy financial conditions and post-vaccine enthusiasm created a favorable market backdrop. Looking ahead to 2022, we remain constructive but increasingly cautious, as the tapering of fiscal and monetary stimulus should reduce support for asset prices. On the positive side, consumer balance sheets remain robust and inventories low, allowing for sell-in, and transitory supply shocks should resolve over the next few quarters.

We expect uneven results in the near-term as companies contend with supply, labor, and logistical headwinds. The retail holiday season looks challenging, and notions of what constitutes pricing power at the micro level will show through results as we monitor the path of PPI versus CPI. We are looking for market shifts based on recent actions in China and watching how the path of interest rates and the dollar may impact financial conditions. We have increased the number of single name shorts in our portfolio and expect to take advantage of dislocations in quality and compounder equities.

Q3 2021 hedge fund letters, conferences and more

Return of “Event-Driven” Investing

In our Second Quarter letter, we wrote that event-driven situations looked interesting again, and our portfolio now reflects this view. Four positions are worth highlighting:

Vivendi

Third Point made an investment in Q1 in shares of Vivendi SE (OTCMKTS:VIVHY), the European media conglomerate. We were attracted by the industry-leading position of its crown jewel asset, Universal Music Group, and the announced separation of that asset as a standalone entity. Our upside calculation was underpinned by a sum-of-the parts analysis and an understanding of the company’s disparate assets. Third Point’s involvement was rumored in the press but in deference to our engagement with the company during a delicate time this Spring, we chose to keep our conversations about tax structure and corporate governance surrounding the spin private. We were pleased that Vivendi’s controlling shareholder, Vincent Bolloré, chose to take meaningful steps forward on governance for the new UMG entity, including commitments for an independent board and the equal treatment of shareholders. We believe these steps eased investor concerns about UMG’s corporate governance that may otherwise have created an overhang in the stock, contributing to UMG’s successful listing in late September.

Dell

Michael Dell has created substantial value for shareholders since re-listing the company several years ago. Earlier this year, Dell Technologies Inc (NYSE:DELL) announced that it would be spinning its $50 billion stake in VMWare, which we believe will unlock the underappreciated value of the Dell server and PC businesses. Dell’s best attribute has been strong free cash flow generation, which the company has used to de-lever and create significant latent value for equity holders. Looking ahead, we believe this core Dell business, which still trades at a discount to its hardware peer group, should instead command a premium multiple thanks to its leading market share, profitability, and impressive execution. There are few large cap companies which possess a nearly 10% FCF yield, 2.5% dividend yield and 1.5x leverage ratio; Dell is one of them.

Entain

MGM’s failed approach to acquire Entain PLC (LON:ENT) in January gave us the opportunity to study this iGaming leader ahead of the July expiry of the U.K.’s six month “cooling off” window. We gained an appreciation for the valuable BetMGM JV stake as well as Entain’s vertically integrated tech stack. The shares appeared to offer attractive value without pricing in the prospect for a bid; in short, we thought there was cheap optionality. Entain’s shares rose after DraftKings approached the company in September and remain above pre-offer levels, despite the recent withdrawal of interest, validating the company’s standalone value. It is uncommon to see one company receive two unique bids in the same calendar year, and we think this bodes favorably for Entain’s business and strategic value.

Q3 2021 hedge fund letters, conferences and more

Prudential PLC

During the quarter, Prudential successfully completed its previously announced spin-off of Jackson National and raised additional equity in Asia for the remaining Pru-Asia business. We are pleased to see the value gap begin to close but see considerable additional appreciation potential as Asian-domiciled and other global investors begin to fully appreciate its significant discount to its peers, excellent franchise, and growth potential.

New Position: Royal Dutch Shell

Third Point initiated a position in Royal Dutch Shell plc (NYSE:RDS.A) (NYSE:RDS.B) (“Shell”) during the second and third quarters. The past two years have been especially challenging for Shell shareholders due to a major dividend cut and well-publicized court case that ordered changes to Shell’s business model. Stepping back further, it has been a difficult two decades for shareholders, with annualized stock returns of just 3% and decreasing returns on invested capital. However, despite the current sour sentiment, we see opportunity for improvement across the board at Shell.

Shell is one of the cheapest large cap stocks in the world, trading at under 4x next year’s EBITDA and ~8x earnings at “strip” prices. It also trades at a ~35% discount on most metrics to peers ExxonMobil and Chevron despite Shell’s higher quality and more sustainable business mix. Compared to its peers, Shell generates a much larger percentage of its cash flow and earnings from stable businesses that have a major role to play in the energy transition. For example, Shell is the largest global player in liquified natural gas (“LNG”), which is a critical transition fuel to move off carbon intensive coal-fired power generation. In 2022, we expect the company’s energy transition businesses (LNG, Renewables and Marketing) to generate EBITDA of over $25 billion with sustaining capex of only $5 billion. These businesses account for just over 40% of Shell’s EBITDA but would likely support Shell’s entire enterprise value if they were a standalone company. At the current share price, we believe investors are getting the remaining ~60% of EBITDA (upstream, refining and chemicals) for free.

Q3 2021 hedge fund letters, conferences and more

Management has been gradually divesting assets that are not aligned with a low-carbon future such as upstream and refining. This is perhaps most evident in Shell’s refining business where the company went from owning 54 refineries in 2004 to only five (by year-end.) This is a remarkable accomplishment. Shell’s massive dividend cut and other asset sales (e.g. Permian) have left it with an under-levered balance sheet with year-end 2021 net debt to EBITDA of well below 1x. This positions Shell to return capital earlier and more aggressively than peers.

Given all these positive attributes, why can’t Shell attract investor interest? In our view, Shell has too many competing stakeholders pushing it in too many different directions, resulting in an incoherent, conflicting set of strategies attempting to appease multiple interests but satisfying none. Some shareholders want Shell to invest aggressively in renewable energy. Other shareholders want it to prioritize return of capital and enjoy the exposure to legacy oil and gas. Some investors think Shell should shrink to grow, while we suspect some within Shell seem sentimentally attached to its “super major” legacy. Some governments want Shell to decarbonize as rapidly as possible. Other governments want it to continue to invest in oil and gas to keep energy prices affordable for consumers. Europe paradoxically wants both!

Shell’s board and management have responded to this with incrementalism and attempts to “do it all.” As the saying goes, you can’t be all things to all people. In trying to do so, Shell has ended up with unhappy shareholders who have been starved of returns and an unhappy society that wants to see Shell do more to decarbonize.

Shell’s board can and must move faster. We believe all stakeholders would benefit from a plan to:

- Optimize Shell’s corporate structure to reduce cost of capital and allow it to more aggressively invest in decarbonization;

- Match its business units with unique shareholder constituencies who may be interested in different things (return of capital vs. growth; legacy energy vs. energy transition);

- Allow each of its business units to more nimbly and effectively react to market and environmental policy developments.

Q3 2021 hedge fund letters, conferences and more

This should involve the creation of multiple standalone companies. For example, a standalone legacy energy business (upstream, refining and chemicals) could slow capex beyond what it has already promised, sell assets, and prioritize return of cash to shareholders (which can be reallocated by the market into low-carbon areas of the economy). A standalone LNG/Renewables/Marketing business could combine modest cash returns with aggressive investment in renewables and other carbon reduction technologies (and this business would benefit from a much lower cost of capital). Pursuing a bold strategy like this would likely lead to an acceleration of CO2 reduction as well as significantly increased returns for shareholders, a win for all stakeholders.

Many ESG investors employ a strategy of buying companies that already have a clean bill of health. A lesson from our prior engagements is that it is often most impactful to invest in companies where the opportunity for positive change is the greatest. While daunting, there is perhaps no bigger ESG opportunity than in “Big Oil”, and specifically, at Royal Dutch Shell. We are early in our engagement with the company but are confident that Shell’s board and management can formulate a plan to accelerate decarbonization while simultaneously improving returns for its long-suffering shareholders.

UnitedHealth

UnitedHealth Group Inc (NYSE:UNH) is one of the largest healthcare companies in the world and a market leader in both its insurance and healthcare services (Optum) businesses. We initiated our position during the 2020 Presidential election at a time of heightened political and regulatory uncertainty.

We believe under its new CEO, Andrew Witty, UnitedHealth can not only preserve its market dominance and sustain industry-leading growth rates across most of its key segments but also enter new healthcare services markets. Witty is known as a mission-driven CEO who clearly articulates his view that providing high-quality, affordable health care services is a social good. He receives consistently high marks from former colleagues, and we believe that his leadership approach will ballast and even strengthen UNH’s already impressive management and employee ranks. The insurance and services businesses are synergistic and complementary, which entrenches United’s critical role in care financing, access, and management. This dynamic gives us confidence in the durability of United’s market leadership.

United’s core capabilities across insurance underwriting, cost and clinical datasets, provider care management, and PBM assets – undergirded by an advanced IT infrastructure – bolster their competitive advantage in providing the most robust insurance benefits at the lowest cost. United is also an early adopter of the technology across a variety of care settings such as telemedicine, digital therapeutics, and continuous glucose monitoring technology for their diabetic type 2 population. This provides better tools and care to patients and gives United better visibility on patient health, which leads to better cost control via early intervention. Driven by UNH’s higher-growth businesses like Medicare Advantage (MA) and value-based care MA clinics, as well as strong visibility on growth acceleration post-Covid, we expect the company’s multiple to rise significantly as investors see a path to sustained mid-teens earnings growth. We believe the stock can double in the next three to four years as we see durability of EPS in the mid-teens supported by a high single digit FCF yield while trading in-line with the market.

Q3 2021 hedge fund letters, conferences and more

Private Investment: Rivian

We first took notice of Rivian after its spectacular launch at the L.A. Auto Show in 2018 when it announced two beautifully designed electric off-road vehicles: the R1T truck and the R1S SUV. Rivian is the brainchild of RJ Scaringe, an engineer with a master’s and a doctorate from MIT. We had the opportunity to meet RJ in early 2020 and were deeply impressed by his charismatic vision and approach to designing a new type of automotive company.

A car enthusiast with a passion to conserve the environment for future generations, RJ has built a company that is shifting consumer mindsets about what battery electric vehicles can be. The R1T, which officially launched in September 2021, has received rave reviews, with Motor Trend calling it the “future of the pickup truck.” The clean sheet, technology-focused vehicle eliminated long-accepted compromises and delivers an experience that harnesses humanity’s innate adventurous spirit in an environmentally friendly way.

Recognizing that personal ownership of vehicles will give way to ride-sharing in the future, Rivian also has the ambition to be major solutions provider to centrally managed fleets. They prudently initiated a relationship with Amazon to develop a range of commercial delivery vans that leverages the same core electric skateboard platform as the R1S/R1T. Amazon has an initial 100,000 vehicle order with Rivian (the largest backlog/order for any electric vehicle company ever at the time) and is also a major investor in Rivian. As Amazon seeks to become a dominant player in logistics while being carbon neutral, we believe that Rivian will be their end-to-end fleet provider of choice.

When we learned that Rivian was doing a fund-raising round in late 2020, we expressed our interest and secured a small investment. More importantly, we spent time with RJ and his team. When Rivian did a pre-IPO convert round in July 2021, we were able to participate in a more meaningful way. Rivian recently filed its S-1 and is on track to go public by year-end.

Rivian stands out with a compelling brand, an excellent first vehicle, and a unique partnership with Amazon that allows them to scale quickly. They are taking full advantage of the direct-to-consumer model/digital ecosystem to attack the full lifetime revenue potential from vehicles rather than simply an upfront sale. After recently spending a full day with RJ and his team in Normal, Illinois and driving the R1T, we are confident that they are best in class in every way: vision, strategy, talent, execution, partnerships and amount/quality of capital raised so far. The R1T knocked it out of the park, and we are excited to invest with Rivian to support its mission to keep the world adventurous forever.

Q3 2021 hedge fund letters, conferences and more

Business Updates

We recently welcomed three new investment professionals to the team. Their biographies are below:

Robert Hou joined our team as Head of Insurance Solutions to develop investment strategies and manage portfolios for our insurance clients. Prior to joining Third Point, Mr. Hou was a portfolio manager at Blackstone in the Insurance Solutions business. His background includes FIG Investment Banking and Corporate Development at BlackRock, Deutsche Bank and Merrill Lynch. Mr. Hou graduated from Stanford University with a B.A. in Economics.

Daniel Lee joined our Structured Credit group. Prior to joining Third Point, Mr. Lee was in-house counsel at Nomura Securities International, Inc. covering securitized products. Mr. Lee spent five years as a structured finance associate at Weil, Gotshal & Manges LLP and four years as an associate at Cadwalader, Wickersham & Taft LLP. Mr. Lee graduated with a J.D. from Washington & Lee School of Law and holds a B.A. from Binghamton University.

Luana Majdalani joined our equity team as an analyst. Prior to joining Third Point, she worked at Blackstone in private equity. She started her career at Evercore Partners in its merger & acquisitions advisory group. Ms. Majdalani graduated with a Master in Financial Mathematics from Princeton University and holds a BSc in Economics from the University College London (UCL).

Q3 2021 hedge fund letters, conferences and more

Sincerely,

Daniel S. Loeb