Crescat Capital’s commentary for the month ended December 2021, the year of the great rotation.

Q3 2021 hedge fund letters, conferences and more

The Year Of The Great Rotation

Welcome to 2022. More than ever, we believe it is time to get out with the old and in with the new.

At Crescat, we believe investors today face a twofold problem:

- The imperative to not get sucked into a financial asset bubble destined to implode.

- The need to outpace structurally rising inflation.

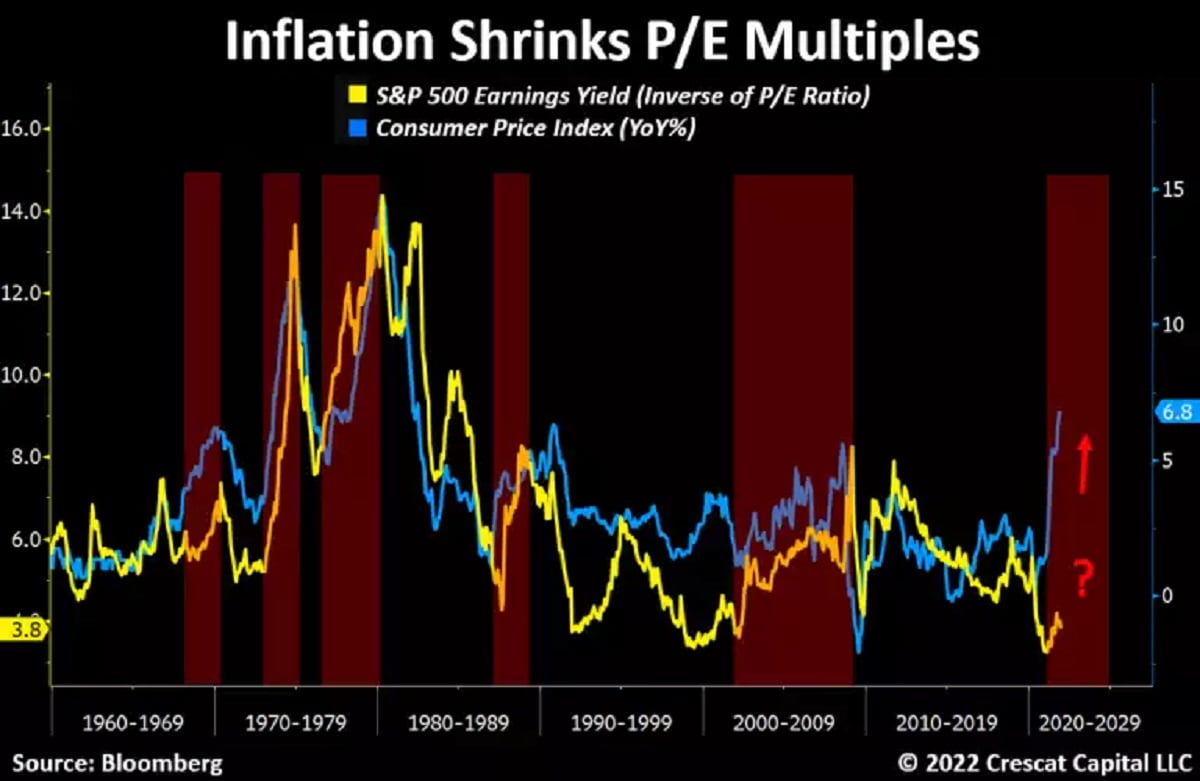

Starting from historically stretched valuations, inflation is the catalyst that can and should both crush price-to-earnings multiples and lead to rising interest rates. It can be especially destructive to overpriced large cap growth and mega-cap tech stocks.

As an overarching macro investment theme at Crescat today, we have been preparing for the Great Rotation. We believe this theme is a tectonic shift out of hyper-overvalued, long-duration financial assets and into a narrower undervalued segment of the market that is focused on the tangible assets at the core of the global economy. It is a collision of macro worldviews and investment flows with one much larger crowded pool of assets ready to swamp the other tiny one to only further ignite the inflationary catalyst, a feedback loop of monumental proportion.

2021 was a year where we saw glimpses under the surface of this transition beginning. But overall, the imbalances only grew more extreme. The economy is not on sound footing for a new economic expansion because there has been no purging of the valuation excesses from the last cycle.

At Crescat, we remain dedicated to applying macro and value investing principles to growing and protecting wealth for our clients over the long term. We have honestly never been more excited about our positioning and the opportunity to deliver solid inflation beating returns on both the long and short side of our portfolios in the coming months and years.

A Change Already Underway In 2022

Right from the starting gun of 2022, the US 10-year yield broke out to the upside from a 3-year resistance. Multiple macro forces are behind this rise in nominal rates. Among the most important ones, the flood of long-dated Treasury issuances is what truly concerns us. As we have explained in prior letters, this dynamic is part of a transition that the US government is undertaking by rolling maturing short-term Treasuries into long term debt instruments as it prepares to inflate out of an unsustainable debt problem. Just in the last 3 months, we saw almost $600 billion of Treasury bonds and notes being issued. Meanwhile, as inflation continues to prove to be more persistent than it initially expected, the financier to the current fiscal imprudence aims to tighten the reins. The Fed has been responsible for about 35 to 40% of new Treasury issuances in the last months. Without them as the lender of last resort, we believe the Treasury market will be facing a major supply-demand mismatch.

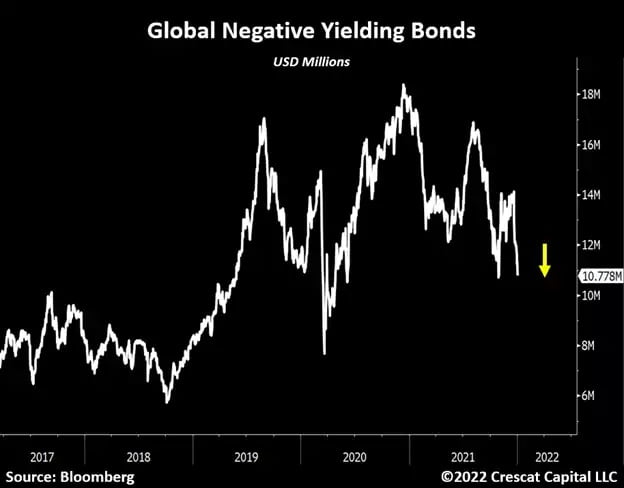

For the first time in a very long-time we are seeing a significant increase in cost of capital unfolding across developed economies. The outstanding value of negative yielding bonds has drastically decreased worldwide, peaking in December 2020 at $18.3 trillion. It is now in free-fall, back to $10.7 trillion.

This is an important part of the macro regime change that we have been calling for. It is a hostile market environment for long-duration assets that currently trade at historical multiples, i.e., tech stocks. These companies have rejoiced from a disinflationary setup for decades and are ripe to be re-rated at significantly lower prices in our view.

Software companies, for instance, have already started to price in this market risk. As part of Russell 3000 index, the median performance for software and technology services is now down 27% from its 52-week moving average. Outside of the technology sector, non-profitable businesses like biotechnology companies are also suffering tremendously from this major rotation out of long-duration assets. In fact, the SPDR S&P Biotech ETF, XBI, is now down 36% since February 2021. The underperformance of software and biotechnology stocks explains why the over-hyped growth investments like the ARK ETF have done so poorly in the last months. These are all strong signs that a reckoning moment for the stock and bond markets at large is upon us.

Still, there is a narrower value-oriented segment of the stock market that will thrive in this rotation. We believe unloved yet highly profitable energy and materials-oriented businesses with strong balance sheets, low fundamental multiples, and high intermediate-term growth rates will benefit from the inflationary environment that is already under development. That is precisely the reason why our hedge funds remain heavily exposed on the long side to natural resource industries. We think commodity-related stocks will continue to outperform relative to the current speculatively overvalued parts of the market.

For further analysis and discussion, please see our recent research letter.

December and Full-Year 2021 Net Return Estimates

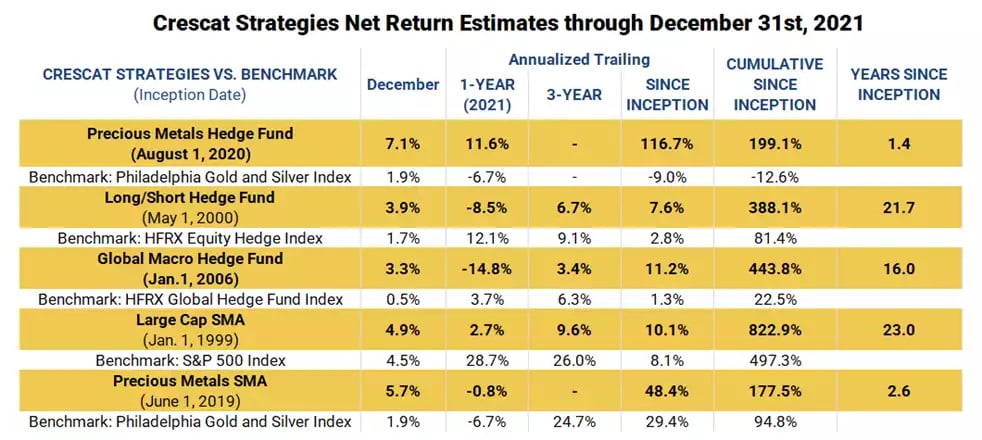

December was a positive month for all Crescat’s strategies. January is off to an auspicious start, especially for our Global Macro and Long/Short hedge funds which actively employ shorting in addition to our current long energy and materials themes. Those two funds have an abundance of software shorts. We are encouraged by their major breakdown today.

The Crescat Precious Metals Fund was the strongest performer in December and finished the year up an estimated 11.6%. Since inception in August 2020, the fund is up an estimated net 199.1% versus its benchmark the Philadelphia Gold and Silver Index which had a return of -12.6% during the same period. We are excited about the macro setup for a new leg of the secular precious metals bull market and look forward to realizing the full value of our activist portfolio.

Crescat Capital is a global macro asset management firm. Our mission is to grow and protect wealth over the long term. Our goal is industry leading absolute and risk-adjusted returns over complete business cycles with low correlation to common benchmarks. We encourage you to reach out to a Crescat representative to learn more about any of our five strategies. You can find both Marek Iwahashi and Cassie Fischer’s contact information below.

Sincerely,

Kevin C. Smith, CFA

Member & Chief Investment Officer

Tavi Costa

Member & Portfolio Manager

For more information including how to invest, please contact:

Marek Iwahashi

Client Service Associate

Cassie Fischer

Client Service Associate

Linda Carleu Smith, CPA

Member & COO

© 2021 Crescat Capital LLC