S&P 500 gave up opening gains, a bit too easily. The 3,880s didn‘t hold, and bonds lost their risk-on posture. Yields rose, but the dollar declined – and the greenback doesn‘t look to be out of the woods even though I‘m looking for it to top out and roll over later than in July still. Apart from bonds, one good reason why stocks bulls aren‘t yet done, is the good performance of value (in spite of the darkening clouds in financials). More thoughts regarding the immediate stock market are reserved for premium subscribers.

Q2 2022 hedge fund letters, conferences and more

Keeping in mind the key macro thoughts from yesterday‘s extensive analysis:

(…) Wednesday‘s very hot CPI print means that the pressure on the Fed to keep hiking aggressively, is on. Indeed no pause in inflation, and if PPI is anything to go by (it is) then there is a lot more in the pipeline – and I‘m not bringing up owners‘ equivalent rent, which would continue driving inflation ahead (it‘ll be now service driven as opposed to goods driven). With 50bp obviously not being enough to recoup some of the Fed‘s badly damaged credibility, the question is by how much they hike actually. There is chatter about a full 1%, but another 75bp one looks most probable to me. And should we see signs of inflation moderating (gasoline and heating oil topped in June, which would help the July figures, and with inflation expectations pointing lower now, odds are that we would then get 25bp in September, and that‘s it – midterms next, justifying Fed‘s wait and see posture.

True, economic growth is slowing, and we are likely to get a slightly negative Q2 GDP reading, but given the way GDP is constructed (this setback would be driven by inventories and trade balance), I don‘t see NBER as likely to declare the U.S. to be in a recession. Europe, that‘s another story entirely – in the worst case that the Fed doesn‘t succeed in its soft landing, we‘re looking at an early 2023 U.S. recession – regardless of the housing turmoil gathering steam, the States are largely insulated from the darkening clouds worldwide. I‘m looking for a quite good Q4 of S&P 500 gains, but at the same time, remember that the current bottoming is a process, and I view the approaching washout (give it 2 weeks to start roughly) as the likeliest scenario still. So, enjoy the positive seasonality of a few good weeks of July still ahead.

Let‘s move right into the charts (all courtesy of www.stockcharts.com) – today‘s full scale article features good 6 ones..

S&P 500 and Nasdaq Outlook

S&P 500 is at a crossroads, the fate of which would be decided in the first half of today‘s session. I‘m looking for moderate degree of optimism, paring back a great deal of yesterday‘s setback. It would be highly encouraging should value again do better than tech.

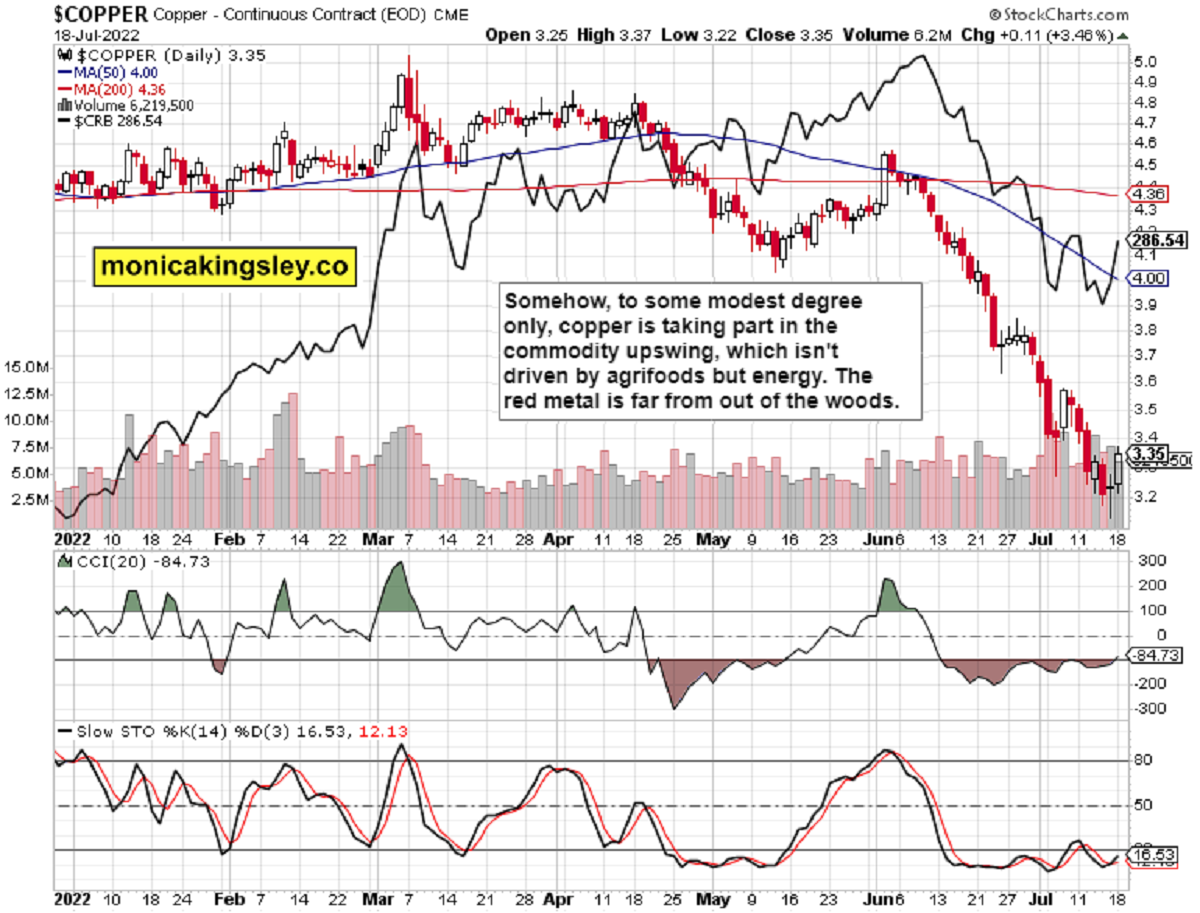

Copper

Copper isn‘t surprising on the upside, and little wonder – I would personally wait for the dust to settle, and load up the truck on the next wave of capitulation.

Bitcoin and Ethereum

Cryptos aren‘t looking bad at all – we are likely to see increased volume with downswing rejection aka indecision today. So far so good.

Thank you for having read today‘s free analysis, which is a small part of the premium Monica’s Trading Signals covering all the markets you’re used to (stocks, bonds, gold, silver, oil, copper, cryptos), and of the premium Monica’s Stock Signals presenting stocks and bonds only. Both publications feature real-time trade calls and intraday updates. While at my homesite, you can subscribe to the free Monica‘s Insider Club for instant publishing notifications and other content useful for making your own trade moves. Thanks for subscribing & all your support that makes this endeavor possible!

Thank you,

Monica Kingsley

Stock Trading Signals

Gold Trading Signals

Oil Trading Signals

Copper Trading Signals

Bitcoin Trading Signals

All essays, research and information represent analyses and opinions of Monica Kingsley that are based on available and latest data. Despite careful research and best efforts, it may prove wrong and be subject to change with or without notice. Monica Kingsley does not guarantee the accuracy or thoroughness of the data or information reported. Her content serves educational purposes and should not be relied upon as advice or construed as providing recommendations of any kind. Futures, stocks and options are financial instruments not suitable for every investor. Please be advised that you invest at your own risk. Monica Kingsley is not a Registered Securities Advisor. By reading her writings, you agree that she will not be held responsible or liable for any decisions you make. Investing, trading and speculating in financial markets may involve high risk of loss. Monica Kingsley may have a short or long position in any securities, including those mentioned in her writings, and may make additional purchases and/or sales of those securities without notice.