Most investors, knowingly or not, rely on long-only, passive strategies. They may shift holdings between stocks, bonds, and cash at various intervals, but generally, their portfolio returns mimic those of well-known stock and bond indices.

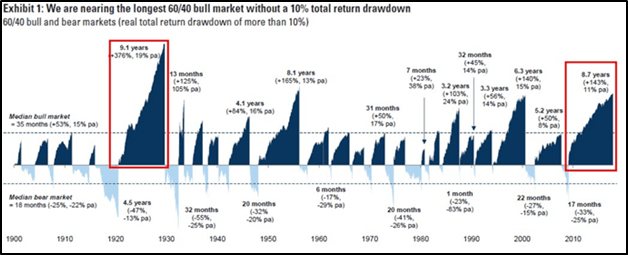

A recent graph from Goldman Sachs, as shown below, serves as a prescient reminder that this popular portfolio strategy may be worth reconsidering in the current environment.

The graph shows bull and bear market periods based on a portfolio comprised of 60% equities and 40% bonds. This graph uniquely allows the reader to simultaneously visualize both returns and the duration of the respective bullish or bearish periods. Focusing on the current bullish period, here are two important takeaways that investors must consider:

- The current bull market in stocks and bonds is 8.7 years old and only about five months shorter than the longest bullish period since at least 1900. That period, the “roaring twenties” preceded the Great Depression.

- Total returns for the current recovery are the third highest over the past 118 years, eclipsing both 2008 and 1999, which both resulted in significant (over 50%) drawdowns.

This chart should give investors pause. While it does not necessarily imply the bottom will fall out as it did in the 1930’s, or even 1999 and 2008, it does suggest that asset markets are historically stretched when measured in both return and the duration. Over the coming years, it is highly likely that a sizeable portion of those returns will be lost.

The graph above fails to factor in one consideration that may make the next correction different from the last four. During the last four recessions and related equity market corrections, a balanced portfolio (60/40) benefited greatly from gains in fixed income assets. The graph below compares total returns during those periods of a portfolio that is 100% invested in the S&P 500 versus one that is allocated to the S&P 500 and U.S. 10 year Treasury notes in a 60:40 ratio.

As shown, the addition of bonds and reduction of equities resulted in positive returns during the recessions of 1981 and 1991. During the last two recessions, bonds helped to cut the portfolio’s losses in half.

Looking forward, an important question we must consider is will bonds help minimize losses as they have done in the past. In the prior two recessions, the ten year U.S. Treasury note yields were greater than 4% and nearly double those of today. The significance is that a higher yield provides more room for yields to decline and thus bond prices to increase. Further, the higher yield provides more coupon income to help offset equity losses.

Investors relying on gains on bond holdings to offset losses on stock holdings should consider that while bonds may produce gains, said gains are likely more limited than at any time in the past.

What’s an Investor to do?

Given the historical precedence, we think it is appropriate for investors to consider alternative wealth management strategies. Below, we describe a few strategies that are not dependent upon positive stock and bond market direction to generate positive returns.

Global macro – By far the most complex and difficult of strategies, managers use a fundamental assessment of global economic dynamics to establish long or short positions in every asset class available to them.

Deep value – This strategy seeks to limit investments to those securities that are heavily discounted and/or extremely out of favor and thus appear to have very limited downside risk. This strategy tends to have longer holding periods than most.

Option strategy – Managers employing this strategy predominately engage in the exchange-traded options market (put/calls) and/or over-the-counter options (swaptions). At times, options are combined with long or short positions in the underlying securities to create the desired profile.

Event-driven – This is a strategy focused on identifying specific catalysts related to a company, a sector or an economy and positioning for the ultimate realization of that event.

Arbitrage – In this approach, managers look for pricing anomalies among related instruments and seek to extract risk-free profits by being long or short those instruments at the same time.

Volatility – Now viewed as an asset class like stocks, bonds and commodities, this strategy uses long or short positions and options to produce returns through low (and rising) or high (and falling) price swings in those instruments.

Long/Short – Predominantly used by managers in the equity markets to pair a long position in one stock against a short position in another with the intent of limiting market risk while taking advantage of perceived richness and cheapness in selected securities.

Trend Following – This strategy is generally a technical approach which relies upon the momentum of price action in a security or an index to generate profits. Managers use long or short positions as a trend establishes itself, then take profits and reverse positions as the trend weakens or reverses.

Fund of Funds – Firms with expertise in identifying talented investment managers look to diversify investment dollars among many managers and strategies, including some of the strategies listed above.

The strategies listed above represent a subset of strategies commonly used by those seeking returns that are not highly correlated with market returns. Like any strategy, those summarized above tend to cycle through periods where they are effective and times when they are less so. Thus, like any strategy, timing is important.

The overly simplistic approach of buy-and-hold fails to acknowledge that given a deep enough correction, most investors will eventually react by selling to stop the mental anguish. This usually occurs very near the worst possible time – at the bottom. To continually build wealth through good and bad markets, investors require a diverse, alternative set of strategic tools. Further, traditional bond/stock strategies of yesterday had the benefit of a cushion provided by fixed income assets. Given the low level of rates, we must question the validity of relying on bonds to hedge a portfolio in the next turndown.

By ignoring history and shunning alternative strategies, investors will, in time, lose much of the wealth they have accumulated over the prior years. Compounding wealth does not require keeping up with high-flying markets in good times, it demands prudent decision-making to avoid large losses when markets sour.

It is important to stress that the strategies detailed above are typically beyond the scope of amateurs and do contain substantial risks of loss. We highly recommend speaking with a knowledgeable investment manager, and conducting extensive due diligence, before investing in such strategies.

Michael Lebowitz, CFA

Investment Analyst and Portfolio Manager for Clarity Financial, LLC. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis.

Article by The Real Investment Advice

{kind=link}