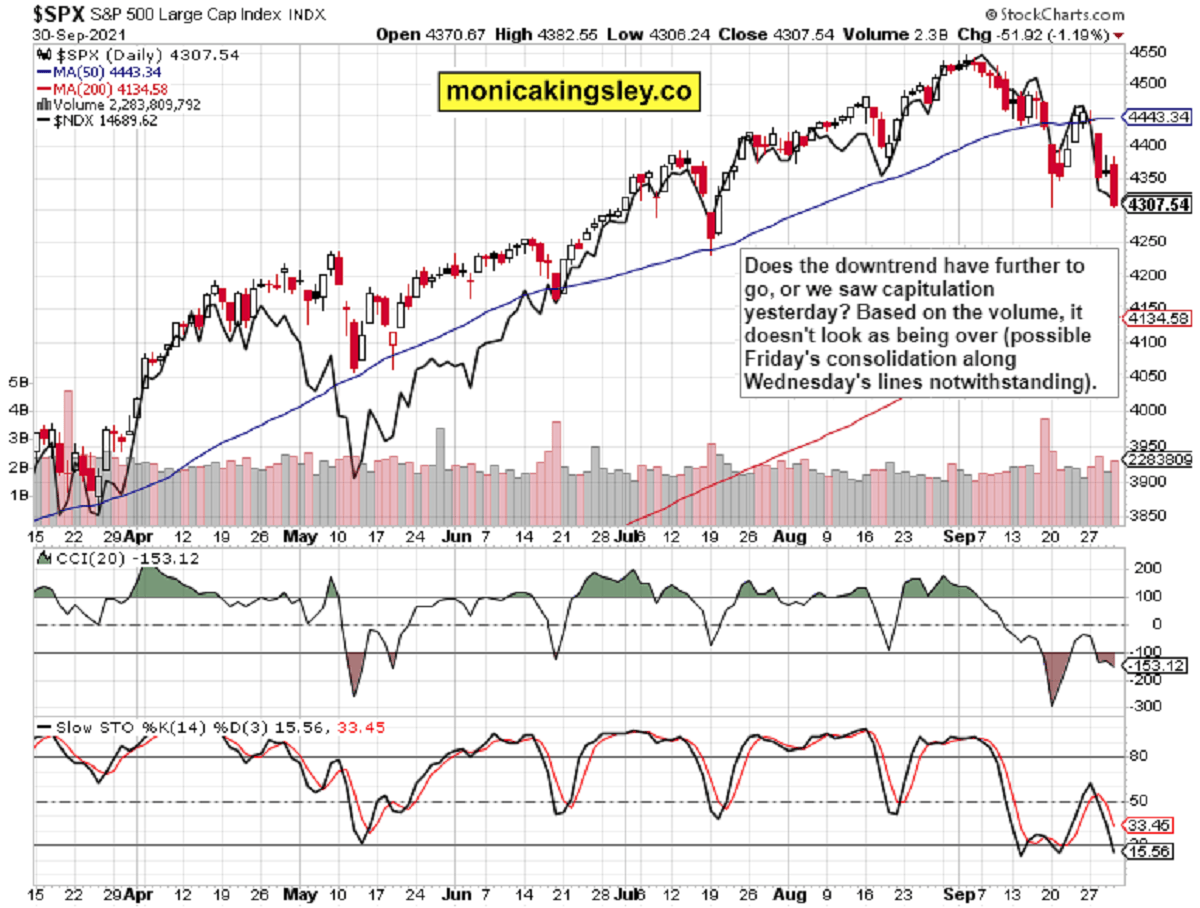

S&P 500 steeply declined, yet the credit markets offered a glimmer of hope to suck in the bulls – and thus far, the premarket bounce is sticking. The fact that buying the dip didn‘t work in the 4,350s area, needs some digesting today – the overnight stampede didn‘t develop. The sectoral view though doesn‘t allow to declare the bottom to be in just yet. The technical bounce would be probably led by value, with tech lagging behind regardless of the anticipated daily stabilization / retreat in yields.

Q2 2021 hedge fund letters, conferences and more

Neither the VIX has calmed down considerably yet. The bulls must be perplexed why buying the dip hasn‘t worked this time around (and before). The sizable open short profits can keep growing. As stated yesterday:

(…) VIX understandably calmed down [Wednesday], but doesn‘t give impression of yielding too much to the downside – on the contrary, it seems to be on a general uptrend since early Jul. Volatility is returning, and that‘s characteristic of the unfolding correction.

How far lower would it reach? The 4,340 followed by 4,300 and lower to mid 4,250 are the key supports. The bulls haven‘t (and face quite many headwinds from related markets, including the dollar) stepped in to close Tuesday‘s gap, which would be a game changer. For now, we‘re in a trading range where the bears have the advantage. The stock market bull hasn‘t topped, we‘re merely in an unpleasant correction, of which the daily upswing in utilities or consumer staples is a testament.

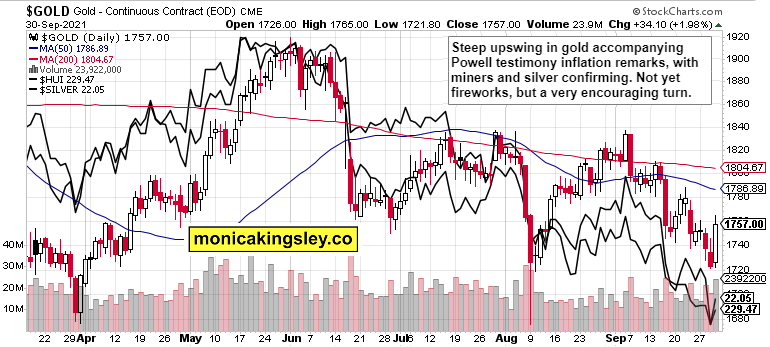

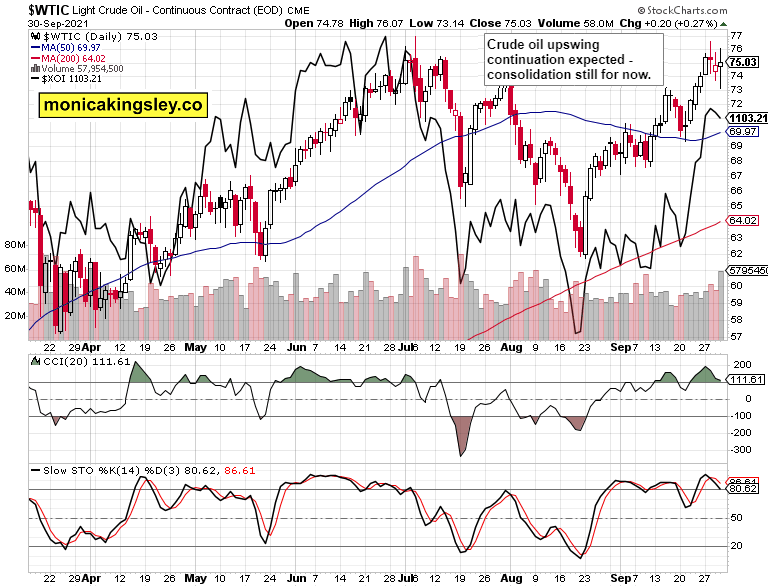

The key fundamental events Thursday were Powell acknowledging that pesky inflation and China ordering its state-owned enterprises to secure oil supplies for the coming winter at any cost. The former finally lit the fuse behind precious metals (did you see how profoundly silver recovered from that $8bn futures contract drop representing 40% of worldwide mining output before Powell spoke on Wednesday?), the latter keeps crude oil prices underpinned.

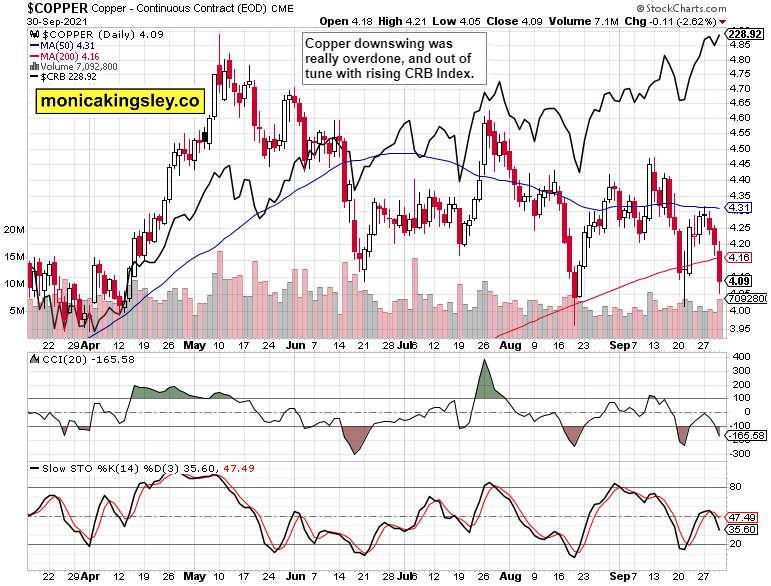

That‘s why I wasn‘t spooked by the copper plunge yesterday (really out of tune with the commodities sentiment and CRB Index performance) – the commodities superbull is merely getting started. Bringing up the key inflation thoughts of yesterday:

(…) The slowly but surely acknowledged inflation surprise will come back to bite the central bank as inflation expectations are finally surging again, reflecting the cost-push inflation (hello commodities superbull), job market challenges and increasingly strained supply chains characterized by order cuts, delays, shortages and general issues in getting merchandise where it‘s awaited (hello port congestion, docking plus trucking staff shortages and full container ships anchored and awaiting unloading). And I‘m not even talking record drought through the West Coast stretching into Rockies and Midwest, or China electricity rationing. Precious metals seem to be the most undervalued asset class these weeks really.

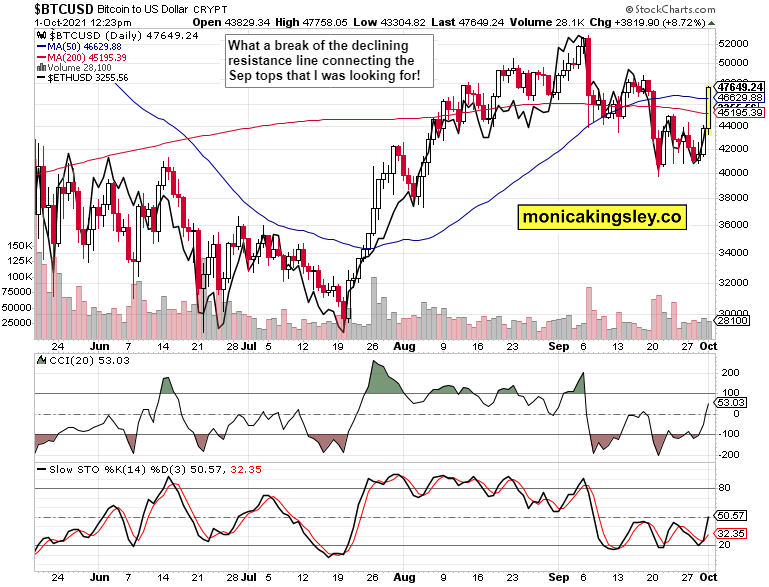

Once we look back at autumn 2021 a few short years down the road, we would all say that precious metals have been outrageously undervalued indeed. And have you seen the great crypto breakout that‘s making bulls such as myself very happy…

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

S&P 500 and Nasdaq Outlook

S&P 500 pause is very clearly over, and the bears keep having the upper hand.

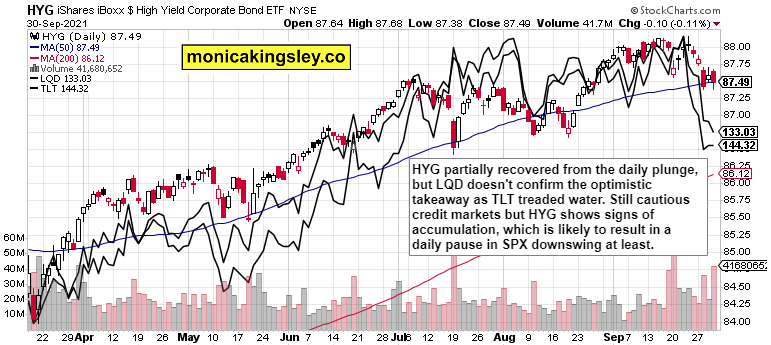

Credit Markets

Credit markets let the bulls have second thoughts, and the high HYG volume indicates a brief pause in the stock market selling.

Gold, Silver and Miners

Precious metals sprang to life – first swallow of a turnaround. The bottom looks to be in, and would be confirmed by silver increasing in price faster than gold in order to bring the gold to silver ratio back down from its 80 local top. Reinforcing that move would be copper catching up and outperforming the CRB Index too.

Crude Oil

Crude oil consolidation continues, and every dip is being bought. Upswing continuation appears a question of time only.

Copper

Copper downswing could have attracted higher volume but that doesn‘t detract from a vigorous response of the bulls coming most likely next. The pattern of lower highs is likely to be broken to the upside the cryptos way (discussed next), in due time.

Bitcoin and Ethereum

Bitcoin and Ethereum bulls confirmed they were on the move, and the early Sep highs are next in their sights. The chart is very bullish, and the daily indicators have plenty of room to go before reaching overbought levels.

Summary

Stocks aren‘t out of the woods yet, but the bears are likely to take a daily pause today. Inflation is coming back into focus, today‘s core PCE price index confirms it isn‘t going away any time soon, and Treasury yield spreads (10-year over 2-year) are coming back from the false breakdown earlier in Sep, which would feed into the hunger for commodities.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for all the five publications: Stock Trading Signals, Gold Trading Signals, Oil Trading Signals, Copper Trading Signals and Bitcoin Trading Signals.

Thank you,

Monica Kingsley

Stock Trading Signals

Gold Trading Signals

Oil Trading Signals

Copper Trading Signals

Bitcoin Trading Signals

All essays, research and information represent analyses and opinions of Monica Kingsley that are based on available and latest data. Despite careful research and best efforts, it may prove wrong and be subject to change with or without notice. Monica Kingsley does not guarantee the accuracy or thoroughness of the data or information reported. Her content serves educational purposes and should not be relied upon as advice or construed as providing recommendations of any kind. Futures, stocks and options are financial instruments not suitable for every investor. Please be advised that you invest at your own risk. Monica Kingsley is not a Registered Securities Advisor. By reading her writings, you agree that she will not be held responsible or liable for any decisions you make. Investing, trading and speculating in financial markets may involve high risk of loss. Monica Kingsley may have a short or long position in any securities, including those mentioned in her writings, and may make additional purchases and/or sales of those securities without notice.