For weekend reading, while discussing the the bullish case for the Russell 2000, Louis Navellier offers the following commentary:

Q3 2021 hedge fund letters, conferences and more

The Bullish Case For The Russell 2000

In September, I highlighted how it might be time to consider going long the Russell 2000 and upping exposure to the small-cap stocks that, as a whole, had lagged the year-to-date performance of the Dow Industrials, S&P 500, and Nasdaq Composite. Smaller companies have been harder hit by the Covid-19 Delta strain, mandates, labor shortages, supply chain disruptions, and the rising costs of inputs and shipping from third-party providers crushed by demand and severe wait times.

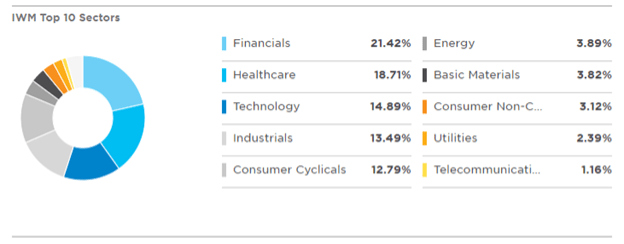

Being such a broad-based index, the distribution of assets in the Russell index is pretty attractive against the current market landscape, which has been rewarding the top-weighted stocks and sectors.

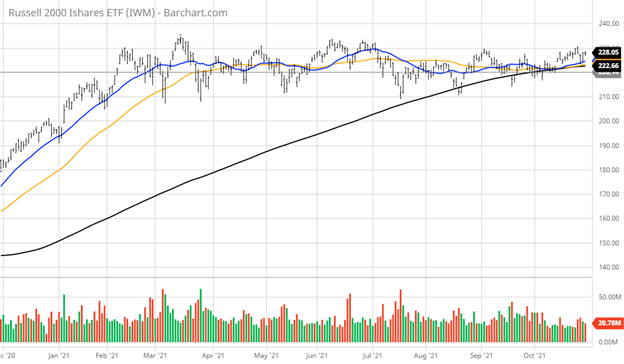

Six weeks later, the chart of the iShares Russell 2000 ETF (IWM) is trading at about the same level, but with the 20 and 50-day moving averages beginning to lift off of the 200-day moving average (black line).

The basing formation is getting longer, and investors haven’t missed out if the small-cap train does in fact leave the station. Unlike the ETFs for the big-cap stock indexes, such as SPY and QQQ, where there is a very high concentration of total asset weighting (of 27.5% and 55.6%, respectively) that accounts for the top ten holdings of each ETF, the top ten holdings in IWM represent only 2.9% of its total assets – since there are 2,026 total stocks held in IWM and they are by definition all smaller than the top 1,000 stocks.

Investing In The Small-Cap Arena

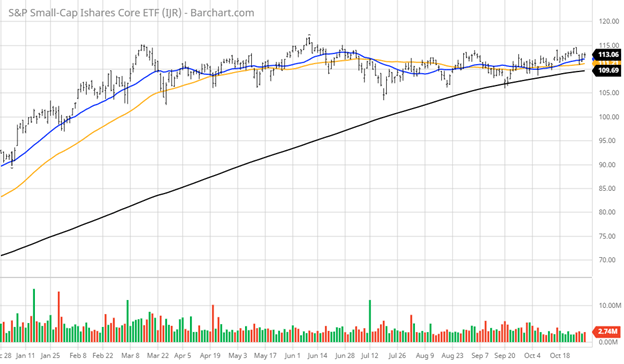

There are a couple of other ways to invest in the small-cap arena that can be considered for investors seeking exposure here. The iShares Core S&P Small Cap ETF (IJR) holds 603 stocks and has Assets Under Management (AUM) of $70.2 billion. With fewer stocks than IWM, IJR has more AUM than IWM, indicating to me that institutional money prefers a smaller number of positions on a select basis.

The chart of IJR is very similar to IWM, so owning either seems to work given the high price correlation, at least for now, but I prefer the blend of the top holdings in IJR over that of IWM. (That’s just a personal choice.) In any event, as capital flows continue to find their way into the stock market, it stands to reason that the small-cap sector will have its day in the sun soon, especially with the Dow, S&P, and Nasdaq all being technically overbought heading into this week.

Small caps have lagged, being the ultimate growth stocks, since they are viewed as the most vulnerable to inflation, and to date, that has been a legitimate concern. However, the Conference Board just released its latest forecast for U.S. GDP, showing a notable slowing in 2022 and again in 2023. If GDP does decline from 5.7% to 3.5%, then bond yields won’t likely climb much higher than where they currently stand.

It’s still too early to make this call, but any relief in energy prices and the supply chain backups will bring down the leading inflation indexes (CPI, PPI, and PCE), and that should translate into a higher level of confidence for small-cap investing. We’ll know more about how this scenario could unfold after the Fed made public their thoughts and plans for the economy at their FOMC meeting this week, as well as having a chance to digest wage inflation with the next set of labor statistics later in the month.

The Potential To Outperform The Other Indices

I’m bringing the Russell 2000 to light again because it has the most potential as an index to outperform the other indexes going forward, and the next five months are the best period for being long stocks in general. The technical term for this potential gain is, “The bigger the base, the higher the space.”

What I also like about this investment proposition is that most of the companies in the Russell 2000 are domestic businesses, where the U.S. seems to be on much better economic footing than the European, Asian, or Latin American economies. If there is a global small-cap rally, it will likely catch fire here first.

This is one area of the market that is not extended – when so much of everything else is.

Chasing stocks higher that have already had stellar year-to-date gains can be hazardous to one’s portfolio. For many hundreds of leading big-cap and mid-cap stocks, the easy money has been made. Such is not the case for the small-cap world of equities, and if the Russell does break out to the upside by year-end, it will have the potential to outperform the other major averages over a much shorter period of time.

The Russell 2000 Index needs to clear 2,360 on big volume to break free of its current 9-month trading range. If so, there’s excellent potential to ring up some fat holiday season profits.