Lumina Gold: A Rare Opportunity In A Fully Valued Gold Market? – A Stock Research Report

Q2 2020 hedge fund letters, conferences and more

Introduction

In a world of $1,900 gold, it is becoming difficult to find opportunities that are not fully valued on a reasonable long-term gold price assumption. Investors who were not positioned for the move in gold are left with the unenviable decision of buying into fully valued companies, in hopes of further gold price appreciation, and thus making a directional bet on the price action of gold, or investing in junior miners.

Juniors can be excellent investments, but they are challenging and require domain-specific due diligence. For those not capable of such work, we have a suggestion: a gold firm that, although a junior, does not have many of the same due diligence challenges of a junior, has an excellent management team, and a built-in catalyst for appreciation in the form of management’s desire to sell.

Lumina Gold Corporation, a Canadian listed junior, is an explorer and developer, not a builder and operator. The firm’s goal is to find assets and de-risk them until they are confident that they can sell them. With this strategy, the Lumina team, through seven different entities, has raised a combined $274 million in equity since the early 2000s and generated $1.6 billion in value through asset sales. In its eighth iteration, the Lumina Gold team is set to do it again in Ecuador, where they have discovered and de-risked a 10.4-million-ounce gold deposit.

Lumina Gold: What’s Going on Here?

Lumina Gold Corporation is a Ross Beatty-backed prospect generator that owns the Cangrejos gold deposit in Ecuador. The Cangrejos deposit is the world’s 37th largest primary gold asset by resource and the 14th largest undeveloped primary gold deposit by production capacity. It has a measured and indicated resource of 10.4 million ounces of gold and 1.4 billion pounds of copper at a grade of 0.73 grams per ton of gold or a 0.50% copper equivalent grade. The management team has recently completed a preliminary economic assessment (PEA) on the asset, in preparation for a sale, which proposes a bulk tonnage open-pit mine with expected capital expenditure requirements of roughly $1.0 billion.

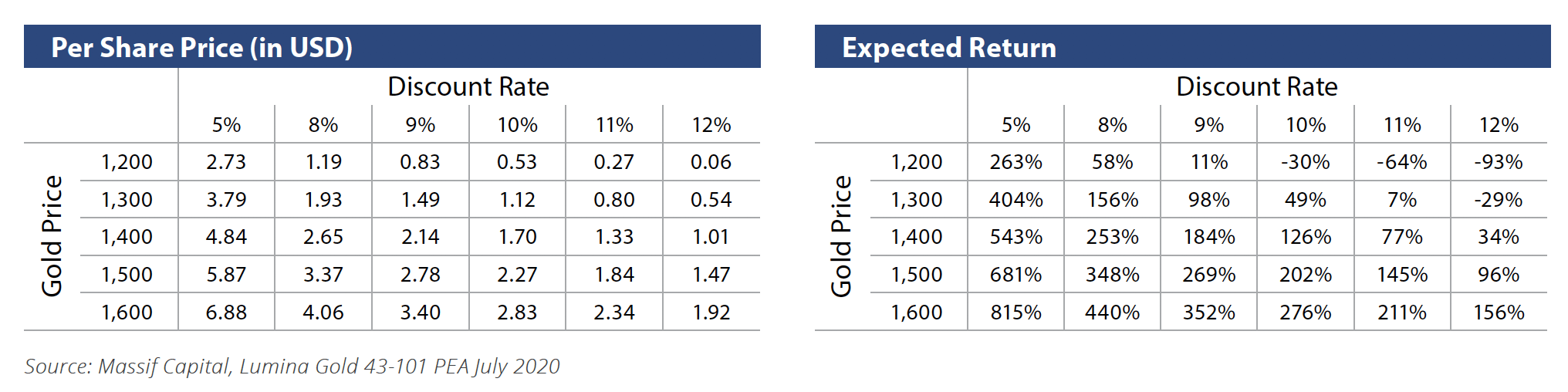

The PEA envisions a 25-year mine life, with an average annual production of 366 thousand ounces of gold per year at an all-in-sustaining-cost of $604 per ounce, net of copper byproduct credits. At a long-term gold price of $1,500 and a long-term copper price of $3.00, assuming a 10% discount rate, the value of the asset developed as per the PEA is worth $2.27 (2.99 CAD) per share, producing an expected return from the current price of roughly 200%. If this were a development project with a management team looking to build the mine , we would likely look for a more significant return.

There are several reasons why we would look for a higher return in the case of development. First, although Ecuador is an increasingly popular destination for mining firms looking to conduct greenfield expansion, it is not without its risks. Second, as a low-grade bulk tonnage asset, minority equity investors may experience significant equity dilution or balance sheet erosion due to mine development costs, not to mention a minimum build time of three years following at least one more year of development drilling and project planning. Luckily, management is focused on selling the asset and, importantly, focused on selling the asset within the next twelve to twenty-four months.

Going-Concern vs. Resource Conversion

As some readers will already know, we tend to think about companies in terms of their ability to generate value as going-concern or as resource conversion.1 From our perspective, valuation always starts with the balance sheet. Does the company have a balance sheet and a business model that supports value creation via the flow of cash through the operations, or does the firm have a balance sheet that is asset rich and supports value creation via the conversion of assets into cash via a sale? In short, should the business be valued as a flow or a stock?

Given the prospect generator model, in which a management team rich in exploration and development expertise finds, de-risks, and sells an asset to someone interested in becoming a producer, Lumina Gold is a resource conversion play. This is important to recognize as it focuses our attention on the essential questions: will it get sold, what is the downside in a sale, and what is the potential upside?

What is the Downside in a Sale?

We first must ask; will this asset be developed into a mine? To answer this question, it is helpful to compare the asset to other recently developed assets.

- Cobre de Panama: 0.43% Cu Eq

- Mount Milligan: 0.39% Cu Eq

- Red Chris: 0.55% Cu Eq

The fact that other similar or lower-grade comparable projects have been developed in recent years is by no means evidence that the asset will be developed. Still, it is supportive of our contention that, at the very least, the asset is potentially attractive to would-be producers.

A second question to ask is whether the potential Capex of ~ $1 billion makes this project a non-starter? Comparables again, in this case, both in Ecuador, can help assuage concerns:

- Fruta del Norte: Completed in 2019 at the cost of $700 million.

- Mirador: Completed in 2019 at the cost of more than $1 billion.

At worst, Cangrejos is an attractive target for potential development; more likely, it is a mine in waiting. Next, we turn to what the value of the asset is in its undeveloped state. Here we have a useful comparison to help us put a lower bound on the value in Lundin Gold’s Fruta del Norte mine.

Fruta del Norte is a sizeable high-grade gold deposit in Ecuador acquired by the Lundin family in 2014. The asset has different operational characteristics then Cangrejos (14 mine life years, reserves of 5.02 million ounces grading 8.74 grams per tonne, and a resource at the time of purchase of 25 million ounces), but both projects have a similar all-in-sustaining-cost: $621 per oz vs. $604 per oz and initial build costs that are of a similar scale, ~$700 million vs. $1.0 billion. Despite some differences, the circumstances around its acquisitions by the Lundin family make it an interesting comparison.

The Fruta Del Norte deposit has a long history. Gold mining in and around the deposit dates to the Spanish conquistadors with evidence of both hard rock and alluvial deposit mining starting in the 1500s. The deposit in its current iteration began to take shape when it was being explored and developed by Aurelian Resources between 2003 and 2008. Aurelian sold the asset to Kinross in 2008 for $1.2 billion (additional assets were included in the acquisition, but the Fruta Del Norte asset was the primary asset acquired).2 At the time of the purchase, the asset had a 13 million ounce resource, comparable in size to Cangrejos. Everything went wrong immediately following the acquisition, resulting in Kinross eventually writing down the value of the investment by $720 million in 2013.

Kinross had made a calculated bet when it acquired Aurelian because the Ecuador government had suspended mining projects across the country while it rewrote the country’s mining legislation. Kinross figured they could navigate those waters. It turned out they were not up to the challenge, and the Ecuadorian government imposed a 70% windfall profits tax on all mining projects. Kinross worked with the government for two years, trying to negotiate a rewrite of the mining code, or at the very least, a more appealing tax regime. Kinross eventually succeeded in negotiating a deal that was more acceptable to the firm’s management, but it still included the 70% windfall profits tax, which was not appealing to shareholders. Kinross CEO Tye Burt lost his job, and the new CEO wanted nothing to do with the disaster, selling it in 2014 to Fortess, soon to be renamed Lundin Gold, for $240 million in cash and stock.

Lundin Gold paid $240 million for a mothballed Ecuadorian gold project that a large, sophisticated mining firm had failed to develop due to political risk. Fast forward to the present, the political situation is entirely different, with dozens of western mining firms crawling over every inch of Ecuador in search of copper and gold deposits. As previously noted, Fruta Del Norte and Cangrejos are different assets. One is a high-grade underground deposit, the other a low-grade open pit deposit, and Fruta Del Norte had a larger resource at the time of the Lundin acquisition. Still, Cangrejos does not have the same troubled political history.

At the time of the Lundin Gold acquisition, according to the first 43-101 filed by Lundin Gold on the Fruta Del Norte asset, the deposit had an indicated mineral resource of 7.26 million ounces of gold and 9.73 million ounces of silver.3 At the current time, Cangrejos has 10.4 million indicated ounces of gold and 1.4 billion pounds of copper. On a gold equivalent basis, Fruta Del Norte had an indicated resource of 7.4 million ounces at average gold and silver prices during 2014, implying that the Lundin’s paid roughly $32 per ounce of political troubled gold in the ground. Cangrejos has approximately 12.6 million gold equivalent ounces in the ground. At $32 per ounce in the ground, this implies that Cangrejos is worth $402 million under circumstances like those in which the Lundin’s purchased Fruta del Norte or roughly 63% more than Lumina Gold’s current market cap. The political situation is entirely different though.

Comparable low-grade bulk tonnage mines in South America have been built recently, comparable assets have been developed in Ecuador recently, and troubled but comparable assets in Ecuador have been sold for more than the firm is worth recently. The downside price risk for this investment appears to be roughly the firm’s current market capitalization, which is about what Lundin Gold purchased Fruta del Norte for under a political cloud and when the gold price was approximately 33% lower. The idea that the worst you can do allocating capital to Lumina Gold is to receive your invested capital back within 24 months appears reasonable and well supported.

What is the Upside in a Sale?

Determining the upside of an investment in Lumina Gold at the current time is more complicated than thinking through the downside. Sensitivities above suggest the NAV per share of the asset is between $1.70 and $2.27. Should you be inclined to discount the cash flows at 5%, which is typical for feasibility studies, while still assuming a long-term gold price of $1,500, the NAV per share is closer to $5.87. Given the history of gold miners and troubled acquisitions at times of high gold prices, we feel comfortable asserting that this investment has a ceiling in a sale of $1.51 (2.00 CAD) per share or roughly a double from here. Although higher valuations fall within our expected NAV ranges, it seems unlikely that a publicly-traded gold miner, other than perhaps a few Chinese firms, will open themselves up to the shareholder ridicule that comes with paying a ~100% premium to the current market value of a single asset. A more reasonable premium to the current market price would be 30% to 50%, a still healthy return in twelve to twenty-four months.

Simultaneously, we can comfortably assert that management will seek the best offer possible, which, given the downside discussion above, is around the current market cap. We can approach a theoretical valuation in a sale from another direction. Over the last ten years, gold mine mergers have closed at a price of roughly $202 per ounce of reserves, and in 2019 firms paid approximately $191 per ounce of reserves.4 At the moment, Lumina Gold does not have any reserves, only resources. If we assume that only 25% of the gold resource converts to reserves, a conservative and risk-averse assumption, the value of the asset in a sale is between $435 million and $460 million, an expected return of between 76% and 86%. This outcome is still high in our opinion but provides further evidence supporting a significantly higher price in sale for Lumina than the market is currently awarding the firm.

With a firm looking to sell itself, we are not only concerned with the sale price. We are also concerned with the timeline. Just as the downside in valuation appears limited, the downside with timing may also be limited. In January, Ross Beaty, the Chairman of the Board of Lumina, said at the Vancouver Resource Investment Conference that 2020 was the year the firm was going to sell the asset. In a subsequent conversation with management, we have been told that they have a slate of interested parties they are currently talking with that are capable of closing the deal this year. Given all that has happened in the world since January, extending this timeline by a year may be more realistic. Having potential buyers assessing the asset is no guarantee of a sale, but it is a favorable situation for investors.

Appendix: Political Risk

Note: Readers interested in learning more about how we approach political risk are encouraged to visit the thought leadership section of our website or download our white paper: “How to Think About Political & Social Risk in Equity Investing.”

Political risk is an issue that all investors should think about. Political risk is of particular importance in countries with a history of creating political risk issues for investors like Ecuador. As a reminder to readers who may have read our white paper on the topic, and as an introduction to some of the ideas discussed in that paper to those who have not, we view political risk through the following framework:

- Political/social risk is idiosyncratic to a business model, its operations, and how a company engages with its operating environment.

- An investor’s goal in assessing political/social risk is not to forecast events that may occur but rather to achieve a high conviction that management can deal with political/social events when they do occur.

- Political/social risks are hard to understand because they are people risks. As such, risk management by a corporation is about managing an ongoing bargaining relationship between the company and stakeholders.

- Political mastery by management can be a source of competitive advantage.

To this list, we add a definition of political risk: Political risk is the probability that political/social events could significantly affect a company’s business over a defined period. To expand the utility of the definition, there are a few specific variables to help us understand and think through how that definition applies to a particular asset: likelihood, magnitude, timing and the nature of a potential event. There is little in the way of surety or conviction that an equity investor can generate around the occurrence of events. So some may find the definition presented above problematic. That concern should be put to the side though. As equity investors, our goal is not to calculate the probability of an event but rather to generate high conviction that a company’s management team can deal with political/social events when they occur.

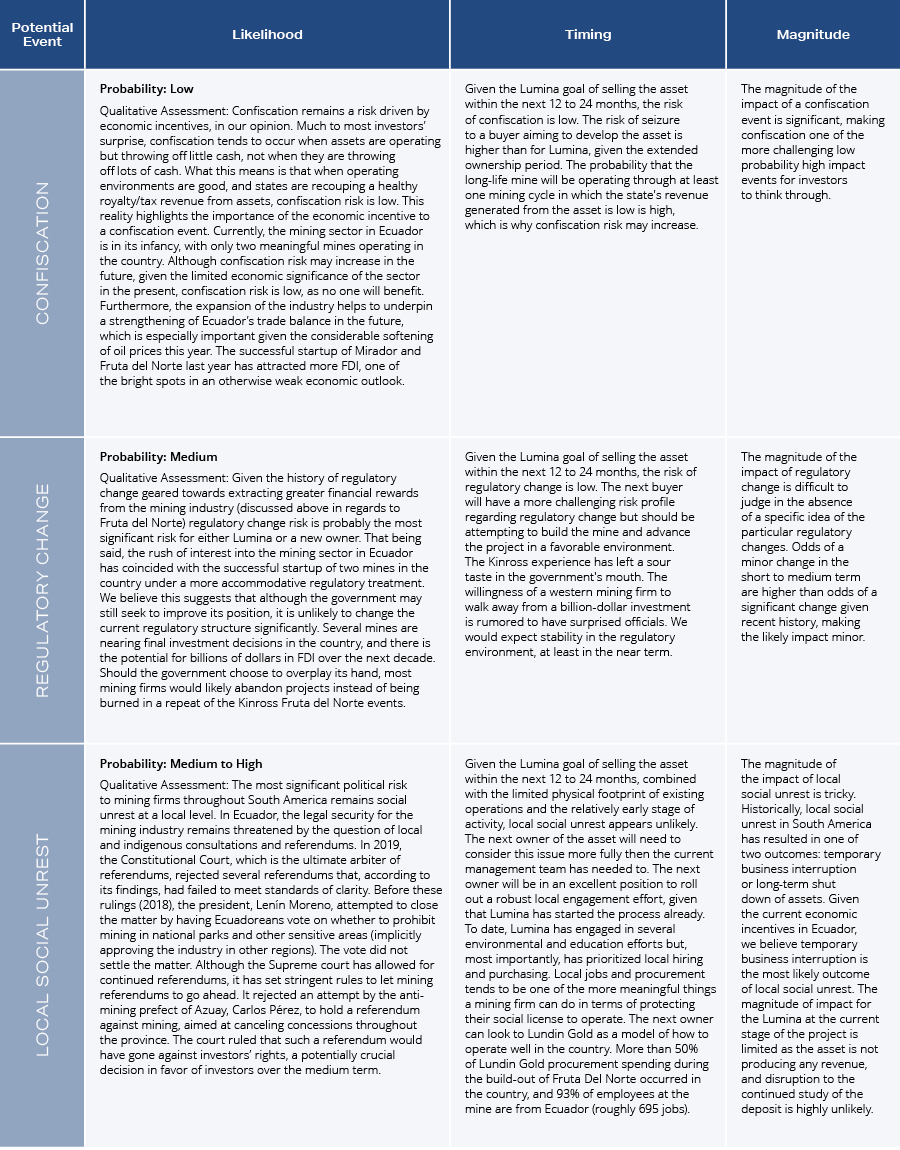

In the case of Lumina, we are principally concerned with the potential occurrence of the following three events:

- Regulatory Change

- Confiscation of Assets

- Local Social Unrest

All the above risks to Lumina Gold investors are limited in part due to the time associated with a potential sale of the asset. Furthermore, the management team and the firm’s largest owner, Ross Beaty, have extensive experience operating in South America. Mr. Beaty has demonstrated himself countless times to be an executive with the ability to navigate tricky operating environments and has, throughout his career, worked hard to maintain good working relationships with local and national governments. The recent purchase of Tahoe Silver by Pan American Silver, a firm started by Mr. Beaty and for which he is the Chairman of the Board, was mostly a purchase of a single asset, the Escobal mine in Guatemala, which has been shut down for three years as a result of local unrest. The mine is not yet operating, in part due to COVID and a change in government, which slowed regulatory approvals. Still, Pan American’s success in advancing towards a restart, when Tahoe management had none, is a prime example of Mr. Beaty’s skill at navigating troubled waters.

For Lumina Gold investors, the political risk does not appear significant enough to warrant an adjustment to our price in sale expectations articulated above.

See Political Risk Table below.

Footnotes

1See our 2019 Year End Letter to Investors

2Kinross Announces Friendly Combination With Aurelian

3Fortress Minerals Corp Fruta Del Norte Project Technical Report 43-101

4Gold M&A Is Heating Up, Mining Journal

Opinions expressed herein by Massif Capital, LLC (Massif Capital) are not an investment recommendation and are not meant to be relied upon in investment decisions. Massif Capital’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is limited in scope, based on an incomplete set of information, and has limitations to its accuracy. Massif Capital recommends that potential and existing investors conduct thorough investment research of their own, including a detailed review of the companies’ regulatory filings, public statements, and competitors. Consulting a qualified investment adviser may be prudent. The information upon which this material is based and was obtained from sources believed to be reliable but has not been independently verified. Therefore, Massif Capital cannot guarantee its accuracy. Any opinions or estimates constitute Massif Capital’s best judgment as of the date of publication and are subject to change without notice. Massif Capital explicitly disclaims any liability that may arise from the use of this material; reliance upon information in this publication is at the sole discretion of the reader. Furthermore, under no circumstances is this publication an offer to sell or a solicitation to buy securities or services discussed herein