As reported by Chain Reaction Research, written by Gabriel Thoumi, CFA, FRM, Tim Steinweg, and Barbara Kuepper, the economic links between deforestation and climate change are increasingly recognized in, for example, the 2015 Framework Convention on Climate Change’s Paris Agreement and elsewhere. This recognition is particularly important, as the planet has lost about 129 million hectares of forest since 1990. As deforestation is largely driven by specific economic activities and is thus a sector-specific risk, investors and banks must now pay far greater attention. Legend: Orange sectors are drivers of deforestation, red sectors are key drivers per country.

Key Sectors Causing deforestation:

- Agriculture: Palm oil, soy, rubber, cattle, and smallholder farming

- Forestry and extractives: Industrial logging, mining, oil and gas, and fuel wood

- Infrastructure: Urban expansion, energy, and transport

(click to enlarge)

Figure 1: Drivers of Deforestation in six Latin American and African Countries

Legend: Orange sectors are drivers of deforestation and red sectors are key drivers per country.

Figure 1 above shows the diverse economic drivers of deforestation in six key tropical countries. In four Latin American countries (Brazil, Colombia, Ecuador and Peru), over 70% of combined deforestation is linked to cattle ranching. In two African countries (Liberia and DRC), large-scale and subsistence agriculture are the primary drivers. Palm oil and other agricultural commodities, as well as mining and the exploitation of oil and gas are threatening forested areas in various countries. Logging is a recurrent factor in all forests, while infrastructure and hydropower contribute to deforestation in several countries.

Banks and investors can be exposed to deforestation risks directly by investing in (multinational) companies operating in the identified sectors in these countries. But they can also be exposed indirectly through downstream companies that buy commodities from these countries, or through governments and public banks that make infrastructure developments possible.

Deforestation related financial risks:

- Lost price premium when unable to sell higher-margin certified products.

- Loss of customers when producers are noncompliant with customers’ zero-deforestation procurement policies.

- Increase of costs of goods sold for sellers when they must find substitute buyers when sellers violate buyers’ zero deforestation policies.

- Loss of banking and investor relationships due to noncompliance with their sustainability policies.

- Fines and other costs due to noncompliance with government and buyers policies.

- Concessions being revoked for illegal deforestation and land grabbing

Direct and indirect exposure to deforestation risks could impact banks and investors in different ways:

- The reputation of financial institutions with sustainability policies is at risk if the companies they invest in do not comply with their policies.

- If deforestation is tackled more seriously on international and national levels, the profitability of companies active in these sectors – or their buyers – could be at stake. Their financial stakeholders could then experience lower returns on investments, higher risk profiles and even defaults.

Forests and Climate

When the December 2015 Paris Agreement explicitly mentioned REDD+ as an important instrument to fight climate change, the movement to halt deforestation entered a new era. The world is paying attention to the link between deforestation and greenhouse gas emissions, which means that more funding will become available in the future to halt deforestation. More and more companies will commit to ‘zero deforestation’ policies, and public monitoring of forest stocks will increase. These developments fundamentally alter the market conditions for those sectors that have contributed to deforestation in the past.

Examples of such changes can be found in SE Asia, where the large palm oil company IOI Corporation (IOI:MK) (IOIOF) was suspended from the Roundtable on Sustainable Palm Oil ((RSPO)) for not complying with its principles, and where palm oil company Felda Global Ventures (FGV:MK) voluntarily withdrew specific mills and concessions from the RSPO after it had been found to be deforesting valuable peatlands. In both cases, the financial implications for these firms were significant. IOI’s large customers suspended trading and Moody’s subsequently downgraded the company. FGV may potentially lose customers with ‘zero deforestation’ policies and is expected to lose an estimated US$6-12 million in 2016 cash flow from certification premiums.

Since 2013, Chain Reaction Research ((CRR)) has uncovered the hidden financial risks associated with the sustainability performance of SE Asian companies such as IOI and FGV. However, deforestation and forest degradation are also major issues in the Congo and Amazon Basins. Similar hidden financial risks are therefore likely to be faced by firms active in these countries, particularly given the increasing level of global attention. This briefing provides a snapshot of the sectors that drive deforestation in six focus countries: Liberia, Democratic Republic of Congo, Colombia, Peru, Ecuador and Brazil, and that are therefore most susceptible to financial risks.

Deforestation Rates: Forests worldwide constitute large repositories of carbon pollution, provide a livelihood to millions of people worldwide – many of whom live in poverty – and contain some of the most varied biodiversity in the world. Despite the widely recognized global importance of forests, vast areas are still affected by deforestation and forest degradation. That leads to major carbon emissions, as well as loss of biodiversity, loss of livelihoods and other adverse sustainability impacts.

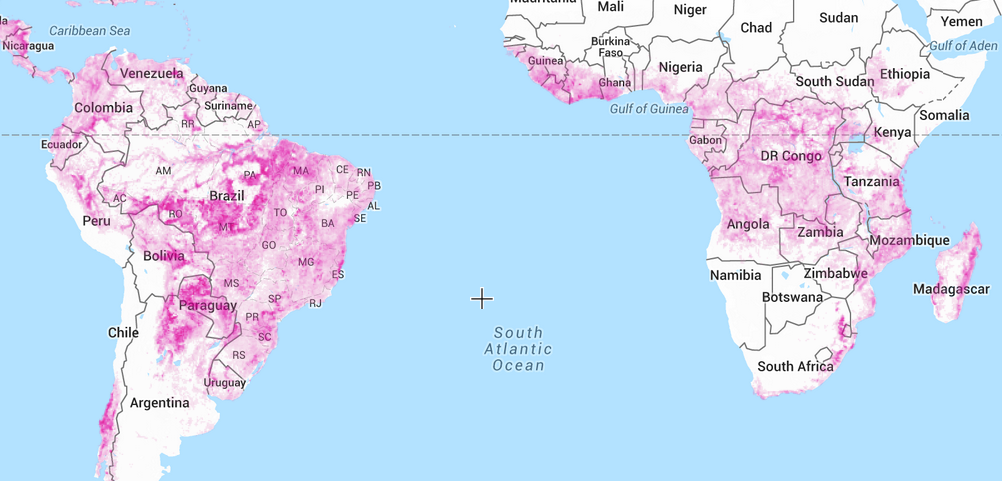

(click to enlarge)

Figure 2: Deforestation in South America and Central Africa

Source: Global Forest Watch.

As shown in Figure 2, deforestation hotspots in Latin America and Central Africa are highlighted. According to the Food and Agriculture Organization of the United Nations ((FAO)), approximately 129 million hectares of forests have been lost around the world since 1990. While the rate of global deforestation has slowed down in recent years, the world’s forests continue to shrink. Tree cover loss in the six focus countries is extensive and, despite a number of good efforts in different parts of the world, is expected to continue and to grow.

As shown in Figure 3, there are clear differences in the relative annual deforestation rates in each of these six countries, as well as in the absolute areas that are deforested every year. In terms of absolute values, deforestation is most pressing in Brazil, where almost one million hectares of forest are lost each year. The relative deforestation rates are much higher in the smaller countries, such as Liberia (0.7%) and Ecuador (0.6%).

The worldwide economic crisis starting in 2007 has had a major impact. Conservation programs have often been limited and governments have had to divert attention and resources to other issues. Liberia has suffered particularly heavily with the Ebola virus coming on top of the economic crisis.

| Country | Forested area in 2015 (in ha) | Deforestation | |

| Annual deforestation rate, as % of total forested area between 2010-2015 | Annual loss of total forested area in ha between 2010-2015 | ||

| DRC | 22,334,000 | 0.2 | 311,400 |

| Liberia | 4,179,000 | 0.7 | 630,000 |

| Brazil | 493,538,000 | 0.2 | 984,000 |

| Colombia | 58,502,000 | 0.0 | 26,700 |

| Ecuador | 12,548,000 | 0.6 | 78,900 |

| Peru | 73,973,000 | 0.2 | 167,600 |

Figure 3: Forested Area 2015 and Deforestation per Country 2010-2015

Source: FAO (2015) Global Forest Resources Assessment 2015

Main Economic Activities Driving Deforestation

Most deforestation is driven by the prospect of economic gains. Countries that have forests often look to develop their economy by exploiting their natural resources.

A variety of proximate human actions at a local level and underlying factors – both fundamental social processes – contribute to deforestation. Proximate causes are defined as immediate human actions at the local level, originating from intended land use and directly impacting forest cover, encompassing agricultural expansion, infrastructure extension and wood extraction. Underlying causes refer to fundamental social processes, such as demographic developments or policy changes, which underpin the proximate causes. Underlying causes can operate at the local level or indirectly impact from a national or global level.

This analysis focuses on the proximate economic causes of human land use. As of 2014, 71% of global forest destruction is driven by agriculture – with timber, cattle, palm oil and soy being most important. Mining and infrastructure development also play significant roles. Underlying national contexts, determined by factors such as public policies, corruption, public management, law enforcement and geographical factors can differ greatly.

Many of the economic drivers of deforestation are closely interrelated. Roads to access mines or dams in remote areas lay protected forests open to new uses. Soy expansion in South America drives cattle farmers to seek new pastures. Improved enforcement in Brazil has limited deforestation in recent years, but is also shifting activities to neighboring countries, such as Peru and Paraguay. New rubber and palm oil concessions in Liberia force local communities to relocate and source their firewood from primary forests.

Agriculture

- Palm oil, soy, and rubber: Size and scale means these pose potential threats of rapid, large-scale deforestation. These sectors can impact forests both directly and indirectly, as concessions granted to commercial firms might force displacement of subsistence farmers to as yet undeveloped lands.

- Livestock: Cattle herding is often the first economic activity that takes place in newly deforested areas. In particular in South America, pasture for livestock has been the primary driver of forest area loss. Previously cleared land gains value and is often sold on to soy farmers. This results in new forest clearing for cattle as livestock farmers seek new pastures.

- Smallholder farming: After frontier areas are opened up by infrastructure development, small farms can fragment forests. Crops are grown for subsistence, for sale in local markets or sold in aggregate to larger players in the sector.

Forestry and extractive industries

- Industrial logging: Timber resources are an important source of employment and trade. Legitimate timber firms and illegal logging activities greatly contribute to deforestation and forest degradation through selective logging.

- Mining, oil and gas: Mineral resources often overlap with intact forest areas including protected areas. Whereas the mining activities themselves may only have limited impacts on tree cover loss, related environmental pollution can degrade ecosystem, while associated infrastructure can open up new regions for economic exploitation.

- Fuel wood: In some of the focus countries, a large percentage of the population is dependent on firewood for their own energy purposes.

Infrastructure

- Urban expansion: The distant demands of a growing urban population for food and other products lead to big block clearings of forests. However, in South America, urban developments and other infrastructure contributed much less to deforestation than pasture and commercial cropland.

- Energy: The construction of large dams used to generate hydropower requires infrastructure to access the forest frontiers, and can lead to the flooding of large forested areas. Furthermore, large-scale dams can severely interfere with the hydrological and biological characteristics of previously free-flowing rivers.

- Transport: While the roads themselves result in relatively little forest loss, they do ‘open up’ the interior for many other activities, both legal and illegal.

Democratic Republic of the Congo

Main drivers of deforestation

- Mining

- Small-scale subsistence agriculture

- Charcoal

- Fuel wood

- Urban expansion

The Democratic Republic of the Congo ((DRC)) is among the least developed nations in the world. Measuring roughly the size of Western Europe, most of the country lacks basic infrastructure such as electricity or roads. Since gaining independence from Belgium in 1960, the DRC has seen continuous internal wars and conflicts, corruption and extreme poverty. Its eastern provinces continue to experience violent uprisings.

After Brazil, the DRC is home to the largest contiguous expanse of tropical forest in the world. The DRC accounts for two-thirds of the Congo Basin forest, which represents 10% of all tropical forests of the world and more than 47% of those of Africa. The overall annual net deforestation rate has been estimated at 0.2% from 1990 onwards, a net loss of about 300,000 km each year.

Deforestation in the Congo Basin is linked to population density and expansion of associated subsistence activities (e.g. agriculture and energy needs). Poor forest governance has been identified as a key underlying driver in the country. Under formal law, the state owns the forests in DRC, but corruption, a lack of effective governance, weak institutional capacity, weak law enforcement and insecure land and resource tenure contribute to ongoing forest degradation and deforestation. The biggest economic drivers are small-scale subsistence agriculture, clearing for charcoal and fuel wood, urban expansion and mining. Industrial logging is also expected to gain in importance.

DRC Subsistence Farming: Most deforestation in the DRC is driven by local subsistence farming. However, few quantitative figures are available. Once an exporter of food, the DRC now grows too little to meet the basic food needs of its 80 million people. Up to 60% of the population have no choice but to undertake some form of subsistence farming on a micro level to meet their basic food and energy needs.

DRC Timber and Mining: The timber industry is a major employer in DRC; thousands of workers rely on logging companies for basic healthcare and other services. At present, industrial timber exploitation is not a major factor in deforestation, but its role is expected to increase. Logging in the Congo Basin has increased significantly as peace has returned to the region. In 2011, most timber production in the DRC (around 90%) was illegal and/or informal for domestic and regional markets. Artisanal logging of roundwood, estimated at 3.4 million m3 per year in 2011, is 13 times greater than formal production of timber in areas where official statistics are reliable.

DRC is one of the most mineral-rich countries in the world, with the Katanga province in the south of the country one of the richest copper and cobalt regions on the planet. In 2010, the contribution of the mining sector was 12% of the GDP and 50% of export earnings. The government intends to increase substantially the contribution of the mining sector to the state budget, from 9% in 2010 to 25% in 2016. Industrial mining competes with other land use, including forestry: in 2011, 629 mining permits were identified as overlapping with protected areas. In addition to industrial mining, in 2008 approximately 16% of DRC’s inhabitants (about 10 million people) derived their livelihoods from artisanal and small-scale mining.

Liberia

Main drivers of deforestation:

- Palm oil and rubber

- Timber and mining

Liberia is a low-income country that relies heavily on foreign assistance. After long periods of civic unrest ended in 2003, its government looked to rebuild the country’s economy by attracting foreign direct investment and exploiting its rich natural resources. Multinational mining and agriculture companies were awarded large concessions, leading to growing exports of iron ore, rubber, gold and timber. Such companies now lay claim to more than 50% of Liberia’s total land area through government leases and concessions. This has created conflict with local communities, some of which have turned violent. The 2014-2015 outbreak of the Ebola epidemic led to the withdrawal of many foreign investors. It slowed down ongoing operations and diverted already scarce resources to combat the spread of the virus, reducing funds available for much needed public investment.

Liberia’s forest has significantly declined – from 4.9 million hectares in 1990 to 4.2 million hectares in 2015. Around 15% of the country’s forest was lost between 1979 and 2004, and since then deforestation has continued at a rate of approximately 0.7% per year (around 30,000 ha). Large-scale industrial palm oil and rubber plantations, and gold, diamond and iron ore mining are the main economic drivers for deforestation. While Liberia has a number of progressive laws governing forests and use of land, effective enforcement remains an issue. Furthermore, Liberia’s forests are owned by the state. This makes forest development susceptible to company lobbyists trying to target political forces in order to obtain concessions.

Liberian Palm Oil and Rubber: Palm oil development is one of the major drivers for deforestation in the country. The area under palm oil concessions was estimated to cover 19% of Liberia’s land area in 2014. The government has issued leases to foreign palm oil companies, often without obtaining prior consent of communities who customarily own and use the land. Exports of palm oil are expected to increase rapidly. Rubber is the most dominant cash crop produced in Liberia, both on large agricultural concessions as well as smallholder farms. The development and expansion of large-scale rubber and palm oil plantations in Liberia have increased in recent years. Related sustainability issues in these sectors include forced displacement, intimidation and harassment by security services, environmental damage such as water pollution and loss of livelihoods due to loss of traditional farmlands.

Liberian Timber and Mining: Liberia is rich in mineral resources – including gold, diamond and iron ore. In 2015, the mining sector accounted for about 17% of GDP and received the highest inflow of foreign development. Iron ore is one of the country’s main export products, and is primarily exploited in large-scale industrial mines. Due to the sharp decline in prices for iron ore on the international market, existing mining operators have put planned investments in the mining sector on halt. Gold and diamond mining in Liberia consists largely of alluvial and small-scale operations, many of them without a mining license as the government lacks the capacity to regulate these activities. However, recent discoveries hold the potential for future large commercial development. International gold mining companies have been granted concessions in areas where artisanal mining was common. This has led to local conflicts and may be indirectly contributing to deforestation as artisanal miners are forced to move elsewhere. Mining activities are known to have caused pollution of surface and ground water, affected the water quality of watersheds and contributed to forest fragmentation.

Liberia’s logging industry is known for its corruption and mismanagement. More recently, large commercial logging companies controlled by political elites and foreign investors have abused ‘private use permits.’

Brazil

Main drivers of deforestation:

- Cattle and soy

- Timber, oil, and mining

- Hydroelectric dams and roads

Characterized by large and well-developed agricultural, mining, manufacturing and service sectors, and a rapidly expanding middle class, Brazil’s economy outweighs that of all other South American countries. The country is in the middle of turbulent political times, with corruption scandals leading to a series of high-profile criminal investigations and the impeachment of President Dilma Rousseff.

Brazil holds about one-third of the world’s remaining rainforests, including a majority of the Amazon rainforest. The Brazilian Amazon has experienced enormous forest loss over the past two generations-an area exceeding 760,000 km, or about 19% of the country since 1970.

Recent years have seen a significant reduction in deforestation rates in the Amazon, primarily because of a government push to protect more areas from logging and burning, and self-imposed moratoria by the soy and cattle industry. However, other ecologically sensitive biomes, most notable the Cerrado savannah, are under increased pressure from expanding monoculture agribusinesses. Deforestation might have also shifted from the Brazilian Amazon to the Amazon regions of neighboring countries. The most significant economic drivers of deforestation in Brazil are cattle and soybean production. Due to Brazil’s size and its dominant economic position, smaller Brazilian sectors may also contribute significantly to deforestation.

Brazilian Cattle and Soy: Brazil has the largest commercial cattle herd in the world and the highest beef production of the Amazon countries. Beef production is forecast to increase in 2016 – driven by higher export demand and depreciation of the Brazilian currency. In 2015, beef production reached 9.4 million metric tons, having grown significantly during the previous decade. Of that total, 21% was destined for exports. Cattle herding accounted for more than 80% of deforestation in Brazil between 1990 and 2005.

Soybean production rose quickly in the early 2000s due to increased global demand, with the area under cultivation tripling between 1995 and 2015, up to 33 million hectares. This increase took place on land directly or indirectly converted from natural ecosystems. Soy farmers regularly move into (already cleared) cattle grazing land, pushing up land prices. Such monoculture expansion, especially in the Cerrado, is displacing the cattle industry into still forested areas.

Brazilian Timber, Oil and Mining: There is significant evidence that illegal logging is widespread in Brazil. Huge discrepancies have been found between volumes harvested and authorized, and widespread fraud has been documented. The country is also the world’s third largest producer of both iron ore and bauxite. Brazil promotes mining exploration in the Amazon Biome on a large scale, and is considering permitting mining surveys and extractive activities in Indigenous territories. Oil access roads are seen as a key driver of deforestation and a threat to Indigenous Peoples. Although only 3% of the Brazilian Amazon has hydrocarbon blocks, this occupies an area of more than 12 million hectares. This is the third largest surface area after Peru and Colombia. An oil exploration block is a large area of land that is awarded to oil drilling and exploration companies by a country’s government.

Brazilian Hydroelectric Dams and Roads: Brazil generates 80% of its electricity from hydropower plants and intends to further increase that capacity. In 2012, Brazil had 138 hydro-plants of different sizes (> 2 MW) installed in the Amazon, 16 under construction and another 221 under planning – the largest number of all Amazon countries. According to Brazil’s ‘Ten-year Energy Expansion Plan’ (PDE-2023), published in September 2014, 44% of the new energy demand will be fulfilled by large hydroelectric dams.

In addition, the largest part of the Amazon’s road infrastructure is in Brazil (71.4%). In the Amazon, the presence of roads is primarily associated with the expansion of new cattle ranching, agriculture and deforestation. There is also a rapidly expanding network of unofficial or illegal (logging) roads linking major highways and cutting into the surrounding areas.

Colombia

Main drivers of deforestation:

- Cattle and palm oil

- Mining

Despite its relatively small size, Colombia is the second most biologically diverse country on Earth, home to about 14% of the world’s biodiversity. This is due to Colombia’s varied ecosystems, from the rich tropical rainforest to coastal cloud forests to open savannas and the high Andes. Today, about 53% of the country is forested. Colombia has seen decades of armed internal conflict, with left-wing insurgency groups and right-wing paramilitary groups conducting armed violence. The Colombian government has held peace negotiations with the FARC since 2012 and is pursuing an economic agenda that aggressively promotes international trade. It is slowly regaining control of most of the country.

Since 1990, Colombia has lost 9% of its forests (5.9 million hectares). After high annual deforestation rates in the period 1990-2010, the FAO reports a drop to an average annual loss rate of about 27,000 hectares since 2010.

These statistics seem too optimistic, however. The country’s meteorological institute, IDEAM, found that 140,000 hectares were destroyed in 2014 alone – a 16% increase year over year. Half of this deforestation took place in the Amazon forest, while deforestation rates were highest in the coca-growing provinces of Putumayo and Norte de Santander.

The forests in Colombia are largely privately owned (around 67%) by local, Indigenous and tribal communities. In 2014, the Colombian government took far-reaching measures to strengthen the rights of Indigenous Peoples and established legal mechanisms to secure their ancestral lands.

The Colombian government has identified its main drivers of deforestation as cattle, palm oil, and mining.

Colombian Cattle and Palm Oil: The Colombian cattle herd is the third largest in South America, after Brazil and Argentina, and the 12th largest in the world. Small and mid-sized producers dominate the sector as more than two-thirds of all cattle farms have less than 25 cows. FEDEGAN, the national cattle association, aims for Colombia to become one of the world’s leading cattle producers, projecting an increase in the size of the national herd from 22 million in 2005 to approximately 48 million head by 2019. Expansion of cattle pastures has also been driven by armed conflict.

Colombia has the third largest forest area potentially suitable for palm oil among the Amazon countries. It is the world’s fifth largest palm oil producer and aims to rapidly increase production of crude palm oil for export – a six-fold increase in production by 2020. Production centers currently are located largely outside of forest frontier regions and the overall impact on the Amazon is so far limited; however, palm oil could become a direct driver of deforestation in the near future as companies explore greater investment near the forest frontier.

Colombian Mining: Gold and other mineral mining contributes to forest clearing and contamination of soils and water sources. Deforestation from mining is currently predominantly linked to the proliferation of illegal artisanal mining in the Colombian Amazon. Around 182,000 people work in gold mining, with small-scale mining accounting for about 70% of national gold production. There is no detailed data on the contribution of these activities to deforestation; however, it is seen as an important driver especially in the Pacific area of the country.

Colombia sees itself as a “mining country” and larger-scale activities may increase in the future. Further developments also depend on the implementation of a Constitutional Court ruling from June 2016 that revoked a 2012 government decree legalizing mining in strategic mining zones but ignoring the rights of indigenous communities.

Ecuador

Main drivers of deforestation:

- Cattle and palm oil

- Mining, oil, and gas

- Hydroelectric dams and roads

Ecuador is considered one of the world’s megadiverse countries, owing to its geographical landscapes. Forest covers about 51% of the country’s surface area. Ecuador is significantly dependent on its oil resources. These account for more than half of the country’s export earnings and approximately 25% of public sector revenues in recent years. The country faces significant risks as both export and fiscal revenues are falling due to lower oil prices and appreciation of the US Dollar. In 2015, Ecuador experienced a meager economic growth of +0.6%, and analysts expect a downturn in the coming years. Foreign investment levels in Ecuador continue to be the lowest in the region as a result of an unstable regulatory environment, weak rule of law and the crowding-out effect of public investments.

Official data on deforestation rates varies. Between 2010 and 2015, the average rate of deforestation in Ecuador was 78,700 hectares per year. While almost all of Ecuador’s forests are held in private or communal possession, an estimated 50% of these lands have unresolved land tenure issues. On paper, Ecuador’s constitution covers topics such as climate change and mitigation measures (including deforestation), community and tenure rights and even bestows rights to nature. But corruption threatens the implementation of these constitutional rights.

In the Amazon region, where the majority of Ecuador’s forest biomass is located, agriculture (cattle and palm oil), mining, and infrastructure development and human settlements linked to hydrocarbon block development are among the main economic drivers of deforestation.

Ecuadorean Cattle and Palm Oil: Agriculture has been identified as the main driver of deforestation in Ecuador. In the Northern Amazon region, agricultural expansion accounted for 78% of deforestation between 1990 and 2000, and 56% between 2000 and 2008. It has also contributed considerably to deforestation and forest fragmentation in the biodiverse forests in the south of the country. Cattle is the most extensive driver of land use change in recent years. While dominated by hundreds of thousands of smallholders, large-scale landowners also contribute significantly. Agriculture accounts for 57% of income-generating activities in the Amazon region – of which cattle farming accounts for 10% and mixed farming for 30%. Future growth is expected in the palm oil industry.

Ecuadorean Mining, Oil, and Gas: The only large-scale mining projects in Ecuador are still under development. Industrial gold and copper mines are considered as potential future drivers of deforestation. Small-scale gold mining often takes place in remote and forested areas that overlap with natural and Indigenous territories. Ecuador is the country with the largest area of hydrocarbon blocks under production in the Amazon Biome (21%), many of them overlapping with Indigenous territories. Road building within or outside of oil concessions opened up much of the Ecuadorian Amazon, attracting settlers that may engage in slash and burn activities and logging.

Ecuadorean Hydroelectric Dams and Roads: Construction of hydropower dams and additional infrastructure such as roads and transmissions lines drive deforestation in Ecuador. Besides road construction tied to extractive activities, several planned or already started projects within the “Initiative for the Integration of Regional Infrastructure in South America” (IIRSA) are located in the Ecuadorian Amazon. This includes a planned connection between Brazilian and Ecuadorian ports, comprising ports, roads, airports and a waterway.

Peru

Main drivers of deforestation:

- Palm oil

- Mining

Peru has a varied topography – an arid lowland coastal region, the central high sierra of the Andes, the dense forest of the Amazon and tropical lands bordering Colombia and Brazil. Peru’s Amazon forest covered almost 74 million hectares in 2015. Peru lost around 5% of its forests since 1990 (3.9 million hectares). According to most recent FAO statistics, the deforestation rate between 2000 and 2010 averaged 133,600 hectares per year, but grew to an annual rate of 167,600 hectares between 2010 and 2015. Preliminary data from the agriculture ministry suggests that forest loss in Peru will continue to expand through 2017.

As deforestation in the Brazilian Amazon decreased in recent years, it has risen in Peru. This resulted partially from activities moving there from neighboring Brazil, as forest enforcement and monitoring in that country has strengthened, in addition to economic development and recently developed infrastructure access in Peru. These factors, combined with high prices for palm oil and weak governance enforcement, will continue to encourage forest conversion in the Peruvian Amazon.

In Peru, all natural resources, including forests, are owned by the state as a part of the national wealth. Despite attempts to reform the forest sector, forest tenure and use rights for Indigenous Peoples in Peru remain unclear. The lack of locally perceived legitimacy is one of the most important underlying reasons for the troublesome implementation of the recent forest sector reforms in Peru.

The Peruvian economy grew by an average of 5.6% from 2009-13 with a stable exchange rate and low inflation. This growth was due partly to high international prices for Peru’s metals and minerals exports, which account for almost 60% of the country’s total exports. Peru is the world’s second largest producer of silver and third largest producer of copper. Growth slipped in 2014, due to weaker global commodity prices. Palm oil production and the mining sector are the main economic drivers of deforestation in Peru.

Peruvian Palm Oil: The area under palm oil cultivation has expanded rapidly in recent years, from approximately 9,000 hectares in 2003 to 36,000 hectares in 2015. Of the total area, about 40% is owned by corporations and the rest by smallholders. The sector is expanding for food and other industrial uses. Low-yield plantations accounted for most of the expansion (80%), of which 30% came from forest conversion. In contrast, 75% of the high-yield expansion was conversion of old-growth forest. Global demand and national political support encourage further growth. Incentives include tax exemptions and a mandate to mix 5% biodiesel in diesel fuel. This resulted in the clearance of 30,000 hectares of primary forest for large-scale plantations and around 575 hectares for small-scale palm oil plantations.

Peruvian Mining: Gold mining, both large- and small-scale, is found in remote forested areas of Peru. From 1999 to 2012, there was a 400% increase in mining area, driven by the rising global price of gold. Much of this gold mining is illegal, taking place in and around protected areas. In 2010, more than 5,000 – mostly small-scale – mining blocks had been designated in the Peruvian Amazon forest, covering 3% of its total area. Data suggest that mining contributed to clearing of at least 53,750 hectares of forestland since 2000. Most of the clearing took place in the southern Peruvian Amazon, in the regions of Madre de Dios and Cusco.

About Chain Reaction Research: Chain Reaction Research is a consortium of Aidenvironment, Profundo and Climate Advisers. CRR conducts sustainability risk analysis for financial analysts and investors, with a special focus on sectors that deal with environmentally intensive commodities in tropical countries. Since 2012, CRR has provided in-depth and reliable analysis to investors about the financial risks inherent in the activities of palm oil and pulp and paper companies in Indonesia. These reports have proven to be a driver for change; investors have used their financial leverage to stimulate companies to adopt No Deforestation policies. The reports have also highlighted the financial risks associated to non-compliance of sustainability standards.

Through a new NORAD-NICFI-funded program, CRR is now expanding the scope of its work to include six additional countries in Africa and Latin America; Brazil, Colombia, Ecuador, Peru, the Democratic Republic of Congo and Liberia. These are all REDD+ priority countries. Green Century Capital Management, a responsible asset manager, has also teamed up with CRR as part of this program.

Disclaimer: This report and the information therein is derived from selected public sources. Chain Reaction Research is an unincorporated project of Climate Advisers, Profundo, and Aidenvironment (individually and together, the “Sponsors”). The Sponsors believe the information in this report comes from reliable sources, but they do not guarantee the accuracy or completeness of this information, which is subject to change without notice, and nothing in this document shall be construed as such a guarantee. The statements reflect the current judgment of the authors of the relevant articles or features, and do not necessarily reflect the opinion of the Sponsors. The Sponsors disclaim any liability, joint or severable, arising from use of this document and its contents. Nothing herein shall constitute or be construed as an offering of financial instruments or as investment advice or recommendations by the Sponsors of an investment or other strategy (e.g., whether or not to “buy”, “sell”, or “hold” an investment). Employees of the Sponsors may hold positions in the companies, projects or investments covered by this report. No aspect of this report is based on the consideration of an investor or potential investor’s individual circumstances. You should determine on your own whether you agree with the content of this document and any information or data provided by the Sponsors.

{kind=link}