Farnam Street Investments commentary for the month of January 2022.

Q4 2021 hedge fund letters, conferences and more

Mea Culpas, Base Rates, And Hard Work

“If you took our top fifteen decisions out, we’d have a pretty average record.” – Charlie Munger

In 2015, Lonnie and I visited Google headquarters in Mountain View. There were some googlers who were fans of the author interview series I was doing called Five Good Questions. They invited me to give a talk. I dug up the presentation recently. It was titled “Blind Spots: The Hazards of Ignoring Macro Valuations and Dispersion.” There were lots of colorful charts showing how expensive the market was at that time. I made the argument that the value opportunity set was the worst in decades due to a lack of dispersion in valuations (no surprise to readers of these letters back then). Coincidentally, this prediction ended up being mostly right. Invesco’s Small Cap Value ETF (NYMARKET:RZV) went nowhere from 2015-2020. But as we’ll see, there was a pot of gold right in front of me if I’d had been using a better framing.

Everyone raves about the free food and campus amenities at Google, and those didn’t disappoint on our visit. But what really impressed me was how chock full the place was with smart people. I’m quite thankful many have become friends as I’ve made more trips to Mountain View over the years.

I had been using Google products for more than a decade at that point. I had recently read Steven Levy’s In the Plex, so I knew some of the backstory and how there was an engineering mentality permeating the culture. I even had a sense back then that Google’s search was one of the greatest businesses of all time. I’ve come to a greater appreciation as I’ve learned more about business, network effects, and data moats. 1

Had I let my wide-eyed enthusiasm take the wheel and bought a big slug of Google in 2015, it would have worked out quite well. It’s painful to report the numbers to you. From January 2015 to January 2022, Google’s stock was up 443%, equivalent to earning 27% per year for 7 years. Mea culpa.

“I like people admitting they were complete stupid horses’ asses. I know I’ll perform better if I rub my nose in my mistakes. This is a wonderful trick to learn.” – Charlie Munger

So how did I miss this one for us?

I don’t have investment journals from that time, but the first obvious mistake was letting the macro picture have too large an influence. Sure, if you know where rates are going, how corporate profit margins and valuations will change, what central banks are going to do, this game gets pretty easy. Each of those factors are impactful and drive outcomes. Access to an interest rate crystal ball would grant you a fortune.

The only problem is all those factors are largely unknowable. At least to me. (And everyone, I suspect.) It’s not even so much the what, it’s the when. And the when really matters. I still keep an eye on some top-down items, but I’ve learned to prioritize a bottom-up focus. Of course, Warren and Charlie adopted this philosophy decades ago:

“Forming macro opinions or listening to the macro or market predictions of others is a waste of time. Indeed, it is dangerous because it may blur your vision of the facts that are truly important.” – Warren Buffett

Good Businesses, Bought Cheap

My analysis skills in 2015 were less evolved than they are today. We were looking for good businesses that were selling cheap. Joel Greenblatt’s The Little Book That Beats the Market was a major influence.

“Good businesses” were defined as earning high returns on invested capital. How much money comes in, compared to how much was laid out.

On that score, Google put up 75% for 2015. Those numbers are slightly obscured for Google due to the way GAAP accounting treats intangible investments.3 But suffice it to say, Google qualified as a good business.

Selling cheap was defined by what’s known as “earnings yield.” Take EBIT and divide by Enterprise Value (EV).4 Google’s earnings yield in December 2015 was 4.2%. That would have felt expensive, and the likely reason I passed. Recall, you could still get 3% “risk free” in 30-year US Treasuries at that time. I didn’t have the confidence to trust a qualitative insight of an amazing culture that wasn’t reflected in Google’s current numbers.

What’s missing from my static analysis was that it was fairly obvious to anyone that Google was bound to grow. More money coming in, especially if you didn’t have to lay out a lot of money to make it happen, creates tremendous value over time.

Post-Mortem Recipe

“Skate to where the puck is going, not where it has been.” – Wayne Gretzky

We’re going to conduct a post-mortem for what I missed in analyzing Google in 2015. I’ll use a simple back-of-the-envelope approach that uses the following recipe.

Start with today’s revenue. Imagine how much it will grow every year.5 We’ll project out six years: 2015 to 2021.

Of the money that’s coming in, how much falls to the bottom line as earnings in Year 6? This percentage is called the Operating Margin. Revenue multiplied by operating margin gives us earnings.

Given that future level of earnings, what multiple might the market pay six years from now? This will give us an expected enterprise value.

We’ll also give some credit for the cash that is likely to build up, and arrive at a market capitalization six years from now.6 Compare today’s market cap to our projections to back into our expected return.

Time Machine

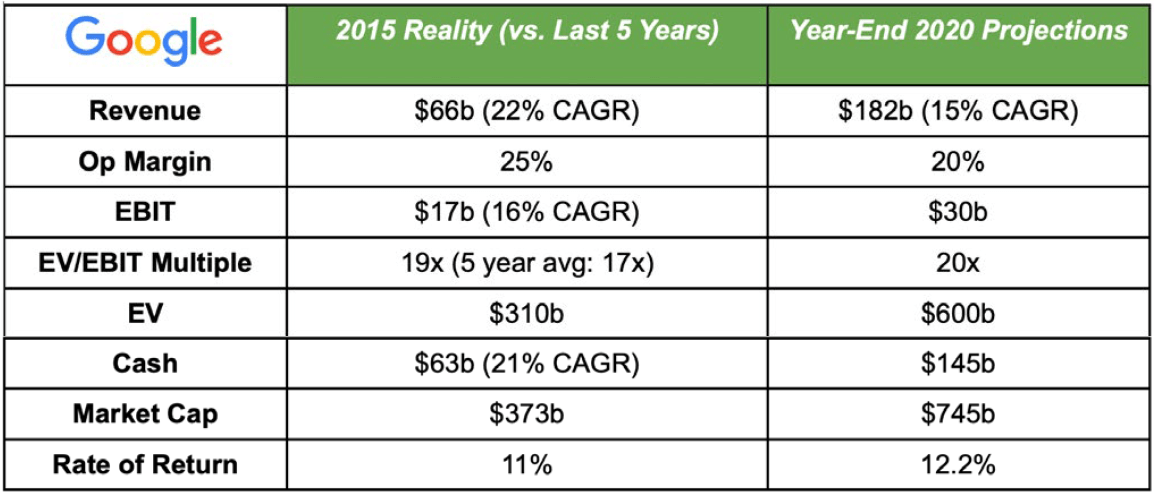

Let’s hop in our time machine and travel back to 2015. We’ll look at Google’s financials from 2010 to 2015 and use them to help us project forward through year-end 2020. We’ll be using very rough ballpark numbers.7

In 2010, Google’s revenue was $24 billion. It grew to $66 billion in 2015 for a 22% CAGR. Impressive feat.8 Operating margins were 35% in 2010 and dropped to 25% in 2015 (still very good). Earnings grew from $8 billion to $17 billion for a 15% CAGR. The average multiple of Enterprise Value/ EBIT was 17x from 2010 to 2015. It happened to be 19x in 2015 for our purposes. That gives us a 2015 EV of $323 billion. Add to that cash of $63 billion for a market cap of $386 billion.9

Using the above as our starting point, let’s project forward from 2015 to year-end 2020. We’ll assume that revenue will grow at 15% CAGR for the next 6 years (recall it was 22% the five previous years). Revenue of $66 billion therefore grows to $152 billion.

Next we’ll assume the operating margin falls to 20%. It had fallen from 35% in 2010 to 25% in 2015, so we’ll drop it a little to stay on trend. That gives us earnings growing from $17 billion to $30 billion.

We’ll assume a 20x EV/EBIT multiple. It had averaged 17x from 2010 to 2015, so we aren’t shortchanging the enthusiasm for the company by using 20x. We now have a projected EV of $600 billion at the end of 2020.

Assuming the cash balance grew at 15% CAGR (it was 21% for previous five years), that takes cash on the balance sheet from $63 billion to $145 billion.

Adding the cash, we get a market cap of $745 billion for where we think the puck will be.10

A 2015 starting market cap of $373 billion growing to $745 billion over 6 years equates to a 12.2% rate of return. Not too shabby. If we felt we were using conservative inputs, this would be an attractive set up. The range of future possible outcomes for disruption-prone industries like tech is wider than normal (“fatter tails” in stats parlance), but this is likely not a bad starting base case.

Back to the Future

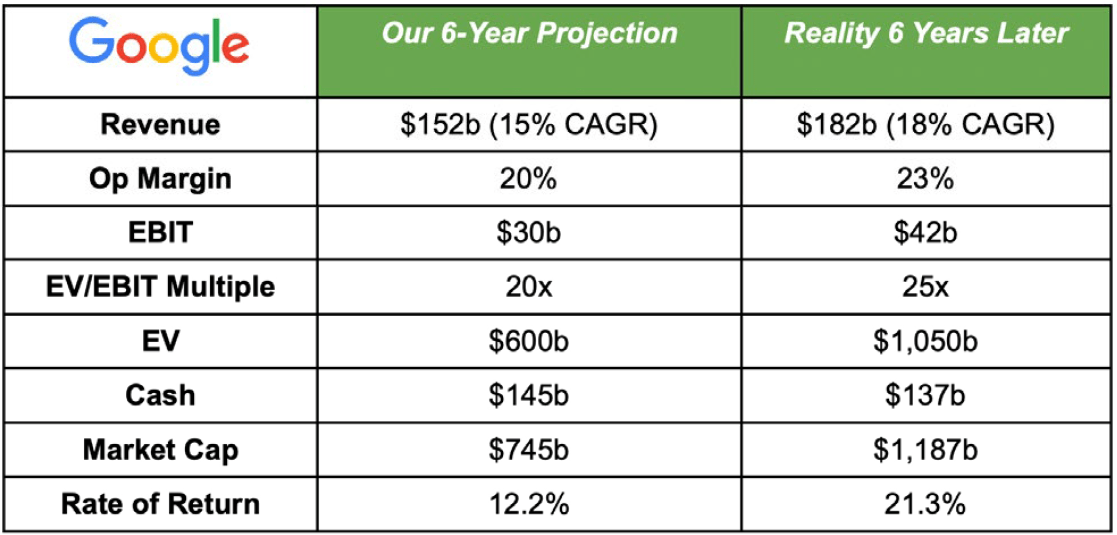

Let’s compare our projections to what really happened to see what we missed. Surprise is our brain’s way of telling us we’ve been using a faulty model and need to adjust.

Revenue in 2020 came in at $182 billion, equaling an 18% CAGR. We were off by 3%.11 Operating margin came in at 23%. Off by 3% again. Makes sense. Economies of scale can kick in–more money coming in can lead to a greater percentage falling to the bottom line. EBIT was then $42 billion versus our $30 billion projection. The business grew more and was more profitable than we anticipated.

Here’s the surprise: the EV/EBIT multiple late in 2020 was 25x. The market was quite a bit more enthusiastic for the business than our projected 20x. Which also makes sense–higher growth and better margins are worthy of more excitement. You can get a sense of how markets can psychologically overshoot any company with dramatic revenue growth. You project out increasing earnings and a bigger multiple and your projected returns explode higher. You can then pay too much for a rosy future. $42b * a 25x multiple gives us a 2020 EV of $1,050 billion. Cash was $137 billion, which was less than our $145 billion projection. Perhaps moonshots absorbed that money? That gives us a market cap of $1,187 billion. (That’s a trillion dollar company, by the way!) Market cap growing from $373 billion to $1,187 billion is a 21.3% annual rate of return.

We missed a home run.

“Sometimes in life, you will make mistakes. And when you think back on those mistakes, you may feel embarrassed. That’s a normal feeling… However, if you do not take responsibility for the mistake and do your best to correct it, then you are committing a second mistake. Do the right thing, even though you may feel embarrassed by your previous actions. Don’t compound the error.” – James Clear

Getting On Base

One of the keys to successful investing is to get out of your own head. Psychologist Daniel Kahneman would call this “finding the outside view.” An outside view can come from a variety of sources. Getting the perspectives of other people is one method for removing blindspots. It’s not without its perils of biasing you away from a good projection though, so choose your sources carefully.

Another outside view technique is asking yourself, “in situations like the one I’m examining, what’s been the typical outcome based on historical statistics?” This is called using base rates. The closer your unique situation is to reflecting the population for which you have existing statistics, the better you can feel about using that base rate. This is basic Bayesian probability.

For a silly yet relatable example, researchers have found that 60-70% of all dogs will bark aggressively at strangers. We have a base rate for all dogs we can use for predicting our next dog encounter. Researchers also found that small dogs are roughly 50% more likely to show aggressive behavior than large dogs. We now have an updated base rate for the likelihood of a small dog compared to dogs in general. This is how our brains work–continually making Bayesian predictions and comparing them to experience. It’s how we learn. Reading widely helps you weave a tapestry of diverse base rates outside of your basic daily existence.

Anchors Away

“Size is the anchor of performance.” – Warren Buffett

In 2015, Google was already a big company, doing $66 billion in business. What were the odds that a company that big could keep growing at a needle-moving rate?

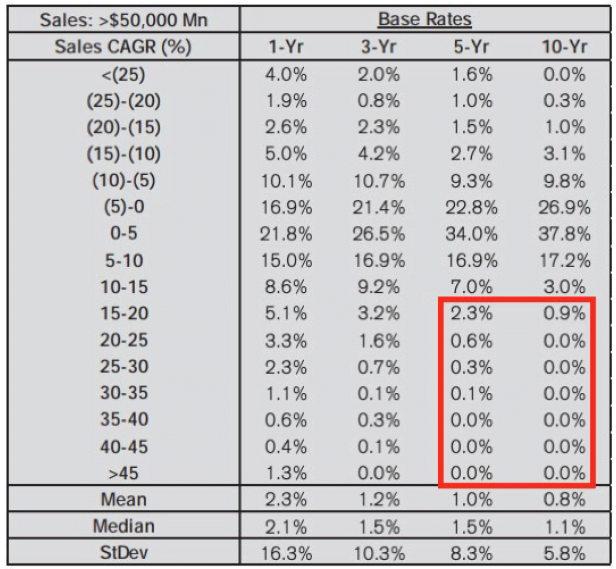

In 2016, one of my heroes, Michael Mauboussin, released an enlightening white paper on using base rates in the investment process. In the paper, he looks at all businesses from 1950-2015 and examines the prevalence of various growth patterns. If you dig into the report, you’ll find a table specific to our “How much do big companies typically grow?” scenario. Of all the companies with sales greater than $50 billion, how many grew at a rate higher than 15% over five years and ten years?

I’ve highlighted in red where to look on the table. Using a little addition, the answer is 3.3% for five years and just 0.9% for ten years. Therefore, the onus would be on us to justify why Google had a better than 33- in-1,000 chance at defying the adage that “trees don’t grow to the sky.” Sure, Google is a remarkable business, but any organization doing more than $50 billion in sales has something cooking.

I did a mini-version of this Google post-mortem on Twitter in an effort to learn in public. Michael Mauboussin reached out to me with an update to his canonical 2016 base rate paper. I’ll save the gory details for another letter, but the punchline is companies which invest in intangibles (like computer code at Google), have different base rate growth profiles. When it works, they can grow in ways that a “brick-and-mortar” business with tangible capital investments like factories simply can’t. Even when they’re already big.

But when it stops working, say due to technological obsolescence (think: Blackberry), the declines are equally breath-taking. So you end up with a much wider standard deviation of growth base rates. This reflects our gut intuition that it seems like technology widens the gulf between winners and losers.

What Does Hard Work Look Like?

“It is good for a professional to be reminded that his professionalism is only a husk, that the real person must remain an amateur, a lover of the work.” – May Sarton

I worked at a grocery store in high school all the way through college. For much of that time, I stacked cans on shelves from 11pm to 7am. After clocking out, I’d splash some cold water on my face and go to class until the early afternoon. I’d come home, sleep for a bit, wake up, eat “dinner,” tackle my homework, shower, and do it all over again. That was hard work. The upside was I’ve never taken a student loan.

But what does hard work look like in an investment context?

Is it returns? No, you can’t just create returns out of thin air, no matter how hard you work. But there are actions upstream from returns you can focus on. I’ve started measuring these precursor inputs to focus myself on key efforts. As Peter Drucker said, “You can’t improve what you don’t measure.”

For me, the ingredients are keeping a thorough investment journal to see what I was thinking in real time and to help organize my research. I also want to record my decisions and reasoning so I can later analyze the data for error patterns (like missing Google). It’s also important to nurture my network of other smart investors to find fresh ideas and gain new understandings about businesses and industries (remember back to courting the “outside view.”)

I’ve been working on a software project with a few awesome co-founders called Journalytic (Journaling + Analytics). We’ve been at it for a few years. The software helps me more easily capture my investment process and track these contributors of success. I can feel myself improving the longer I use it.

Below is a table Journalytic helped me assemble of the work I put in for 2021.

I feel pretty good about my 2021 efforts. If I can keep grinding out relentless process improvements, tracking new important measurables, we’ve got a good shot at satisfactory results over the long haul. Eventually, hard work becomes skill and the vagaries of luck fade.

As always, we’re thankful to have such great partners in this wealth creation journey.

Jake