By EconMatters

Steve Jobs is really gone forever this time. Many questions surrounding where Apple as a company would be headed without Jobs. Jobs has such a rare combination of artistry, business savvy, and salesmanship that the void left by his untimely death probably will never be filled.

While the current executive team at Apple is no doubt quite capable of running the company, but gone are the days of the continued stellar AAPL stock returns and the pace of new product introductions could slow considerably vs. the iSteve era, and investors are now looking for the next Apple. (See graphic below) .

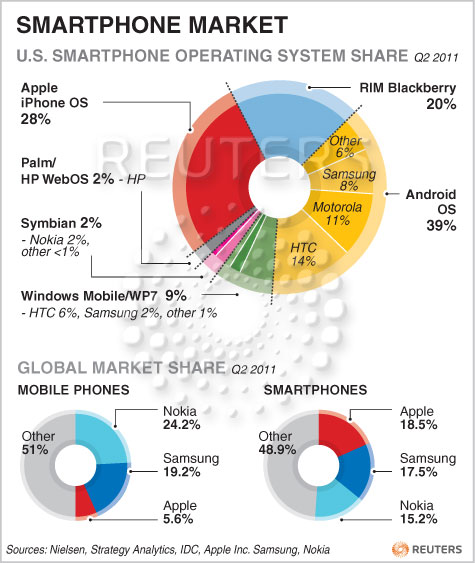

The mobile phone market is very competitive particularly with Google Android gaining market share among cell phone manufacturers (See Chart Below). And signs of vulnerability of an Apple without Jobs is already emerging upon the release of the iPhone 4S, the first new product launch under the new CEO Tim Cook.

From Digitimes:

“The newly released iPhone 4S lags behind some mainstream smartphones as far as specifications are concerned, giving rival companies in either the Android or Windows Phone camps, including HTC, Samsung Electronics and Nokia more chance to expand their market shares with innovative models, according to industry sources…..

…Although Apple also launched an entry-level 8GB iPhone 4 and cut the price of its iPhone 3GS, the effectiveness of such tactics will be limited as iPhone fans will still prefer to buy new models and the low-priced iPhones will not be able to compete with Google Android phones in the entry-level segment, commented the sources.”

On the positives, in addition to iPhone 4S with a new iOS 5 operating system, so far, Apple also has the following new products:

- New iPods (iPod Nano, white iPod Touch) available on Oct. 12

- Siri voice-recognition-based assistant (which allows one to control the iPhone with one’s voice)

- iTunes Match ($25/yr service that scans one’s music collection and creates an identical version in iCloud platform, but rivals like Amazon also has a 5-GB free Cloud Drive for music).

Moreover, Wedbush Research estimated that Apple has only 228 operators distributing the iPhone and only 68 countries for the iPad, vs. an estimated 600 operators distribution channel for RIM and Nokia. So tremendous market growth potential for both iPhone and iPad remains even in the face of fierce competitions.

Another potential niche growth market for Apple TV is the content streaming service for movies and TV shows, etc. which lacks a clear market leader. However, the marketing and vision of that entry is where Jobs’ creativity and leadership would be sorely missed.

Bottom line: We remain neutral on AAPL. We do think Jobs most likely has left a rich approved product development pipeline that Apple could be expected to still deliver above expectation performance in the next 3-5 years. But the downside risk increases on a longer time horizon as Tim Cook’s is mainly an operations/numbers guy, so the creative course of Apple without Jobs is hard to chart.

We also think the delay of iPhone 5 opens the door for others such as Samsung and Motorola to gain on Apple, and there’s a risk (similar to RIM) of consumers becoming disenchanted if Apple fails to keep pace with the new products by competitors. Furthermore, the global macroeconomic uncertainty would be an even greater downside risk as AAPL would not be spared in the case of a market sell-off en masse.

Near term, although investors reacted negatively to iPhone 4S and Jobs death, Apple should have good earnings in this holiday season (Christmas Rally) with the iPad, iPhones (4, 4S, 3GS) among the popular devices along with Samsung Galaxy S II, as well as the Motorola DROID BIONIC and HTC Rhyme.

From a technical perspective, AAPL is now trading in the bear territory, and has broken below the 50-day moving average of $383.42. The next support level would be around $$350 to $360 levels and the next support at around $340. (See Chart Above)

A break below $320 (which we think is fairly easy based on AAPL historical movement) would be an extremely bearish sign, which could be an attractive entry point. However, we caution investors to do some root cause analysis before rushing in to buy on the dip.

In the case of a broad market sell-off (a la 2008), Apple stocks would most likely hold up better due to its high branding, customer loyalty, and could find major support at $250 with $200 as the next major support level.

Apple’s Sept. earnings release is scheduled on Oct. 17, AAPL by and large should have blow-out results rallying into earnings, and would find strong upside resistance around $400 levels.

On a side note, although AT&T lost its exclusive iPhone contract, but since the new iPhone 4S includes AT&T’s 4G technology (HSPA+), vs. only 3G for the others, AT&T could have a significant marketing advantage over Verizon and Sprint. We also like AT&T as an attractive alternative to CDs in the new normal of negative real interest rate (Read our complete analysis on AT&T Here)

{kind=link}

{kind=link}

{kind=link}