Del Principe O’Brien Financial Advisors commentary for the month ended October 2020, discussing their portfolio holdings and their recent investment in Intercontinental Exchange.

Q3 2020 hedge fund letters, conferences and more

Dear Fellow Investors,

“Just keep in mind: the more we value things outside our control, the less control we have.” - Epictetus

In times like these, it’s easy to let volatility and uncertainty get the best of us. It’s tempting to look for ways to make short-term gains in order to take the sting out of previous losses.

But this kind of thinking pulls us away from our value investing fundamentals and distracts us with shiny objects. What kind of shiny objects? How about the top 5 largest stocks in the S&P 500.

The top 5 – Apple, Microsoft, Amazon.com, Alphabet (Google), and Facebook – account for approximately 23% of the index’s market value. That leaves 495 or so other companies in the index, many of which are worthy of investment based not on their index position but on other analyzable criteria. Let’s not forget that the S&P 500 is weighted by float-adjusted market capitalization, which is why the top 5 stocks affect the index so profoundly and are watched and talked about like they are the only players in the game.

We value investors shouldn’t fall for the trap of index funds. We know to avoid the pitfall of correlating the weighted index position of a stock with the quality of the business behind it. We know that largest does not always mean strongest or best value.

In this letter, you can read about companies in our portfolio that are demonstrating their strength and intrinsic value. Companies that have actively cultivated strength and resilience will be better able to weather uncertainty and volatility. They will come out of these uncertain times even stronger – and so will we.

News from Our Portfolio: Acquisitions

“Know the difference between those who stay to feed the soil and those who come to grab the fruit.” - Unknown

Our equity portfolio is full of companies we would consider “serial acquirers,” and that is no accident. Merging with or acquiring other companies is an effective capital allocation strategy, and the move often raises the intrinsic value of a company.

See below for how our companies have been using acquisitions to strengthen their positions:

Berkshire Hathaway Inc. (BRK-B) | Ownership: 2% – 10%

Warren Buffett is, of course, the king of serial acquirers. He has grown his massive holding company, Berkshire Hathaway, by relentlessly deploying capital toward strategic acquisitions. In July, Berkshire entered an agreement to buy all of Dominion Energy’s Gas Transmission & Storage segment. The nearly all-cash deal, which is set to close in Q4 2020, is valued at close to $10 billion, including $5.7 billion of existing debt. Being so over-levered, Dominion was on the verge of filing for bankruptcy. That Berkshire had the cash and was able to make the purchase is what we call “good mojo” and a true win-win: Dominion was not forced to enter into bankruptcy, and the acquisition of Dominion’s business makes Berkshire one of the largest energy companies in the world.

According to its second quarter report, Berkshire realized $15.7 billion in proceeds from equity sales for a total of $146.6 billion in cash and equivalents on hand. That was in spite of the $5.1 billion worth of stock the company repurchased in May and June (the largest ever repurchase in a single time period for Buffett) . In the second quarter alone, Berkshire reported $26.3 billion in net earnings. The company is strong and getting stronger.

Roper Technologies, Inc. (ROP) | Ownership: 1% – 10%

Diversified technology company Roper is another serial acquirer. In August 2019, Roper acquired iPipeline, provider of cloud-based software solutions for the life insurance and financial services industry, in an all-cash transaction valued at $1.625 billion.

This August, Roper reached a definitive agreement to acquire Vertafore, provider of cloud-based software that simplifies and automates processes around property and casualty (“P&C”) insurance. The all-cash transaction is valued at about $5.35 billion. A move like this is what we have come to expect from Roper. The company tends to target niche industries with a zealous focus on each business executing a long-term, sustainable, and asset-light organic growth strategy. This move is the reason we added to our existing investment following the market pullback in the spring. It has proven to be a great growth opportunity for us.

Danaher (DHR) | Ownership: 1% – 5%

Danaher, which designs, manufactures, and markets life science, diagnostics, dental, environmental, and applied solutions, is a prime example of how to use the business strategy of “bolt-on” acquisitions. Led by capital allocation experts the Rales brothers, Danaher will purchase a company in a fragmented industry, create a strategic platform for providing a unique service, and then spin off the company when it can create even more value as an independent entity.

Since Danaher’s bolt-on acquisition of the biopharma business of General Electric’s Life Sciences division for $21.4 billion in March 2019, we have realized a gain of well over 100%. The move boosted Danaher’s stock from around $90 (our purchase price) to the $210s. A gain like this is one of the big upsides of investing in a serial acquirer.

Mastercard Inc. (MC) | Ownership 2 % –9 %

The market pullback in the spring gave us a chance to become owners of Mastercard, one of the biggest players in the global payments industry. In fiscal year 2019, the company processed almost $5 trillion in purchase transactions and holds 29% of the global market share for credit cards and 24% of the global market for debit cards.

In June, Mastercard entered into an agreement to acquire Finicity, a financial data and insight provider, for a purchase price of $825 million. The move is meant to strengthen Mastercard’s existing open banking platform. Open banking is a system that gives third parties, including other banks and tech start-ups that provide financial services (think budgeting apps), digital access to financial data. A user-focused innovation in the banking industry, open banking is thought to be the future of banking. We see an active investment in its open banking platform as a good move for Mastercard toward maintaining its leadership in the global market.

New Purchase

“You acquire companies at moments in time when there’s an inflection point and you can change the trajectory of the company and the industry.” - Jeffrey Sprecher

Intercontinental Exchange (ICE) | Ownership: 1% – 5%

As the above quote suggests, Jeffrey Sprecher, founder, chairman, and CEO of our most recent investment, Intercontinental Exchange (ICE), knows something about making the right acquisitions, at the right time, for the right reasons. ICE began as an online marketplace for energy trading in the late 1990s before electronic trading was a common practice. In 2000, Sprecher and his colleagues launched their company under “Intercontinental Exchange,” a name suggesting that their innovative brokerage was not bound by national borders and could serve a global market. In the last twenty years, Intercontinental Exchange has done just that by making several bold acquisitions of global brokerages and clearing agencies, including the International Petroleum Exchange, the New York Board of Trade, Creditex, and NYSE Euronext (otherwise known as the New York Stock Exchange).

Intercontinental Exchange’s acquisition of NYSE Euronext in a cash-and-stock deal valued at about $11 billion in November 2013 is particularly notable because it signifies how technology in the trading industry was changing. The days of blazer-wearing brokers calling out bids in the pit were about to give way to the era of high-speed computerized trading. In the last decade, we’ve seen how electronic trading has reduced the cost of buying and selling stocks and has made trading more accessible to your average investor.

Sprecher has had tremendous success growing Intercontinental Exchange by changing and adapting to the rapidly evolving global exchange industry. By doing so, ICE has positioned itself as (in Sprecher’s words) “a diverse operator” in the industry, which includes being a player in global financial and commodity markets, clearing and technology infrastructure, and data services. In September, ICE further expanded its capabilities by acquiring digital lending platform provider Ellie Mae for $11 billion from private equity firm Thoma Bravo. With this move, ICE aims to accelerate the automation of mortgage origination in the trillion-dollar residential mortgage industry. This acquisition also demonstrates how adept ICE is at anticipating changes in financial technology and how it pushes to make them happen.

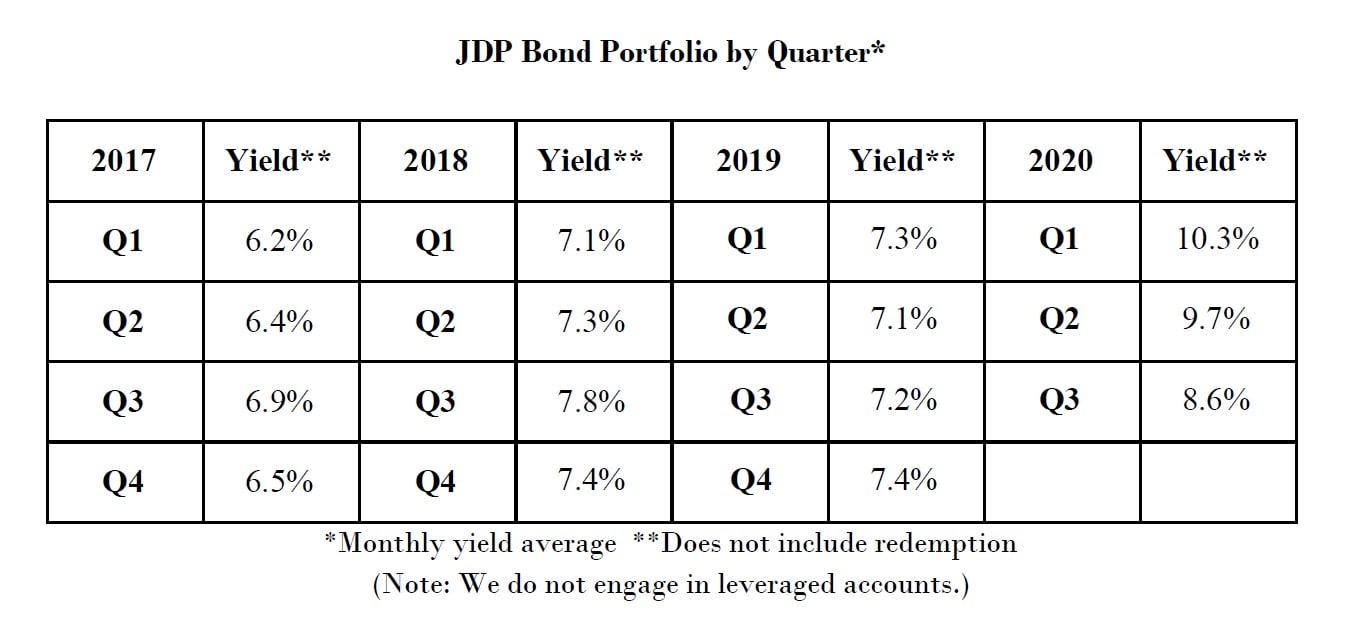

JDP Bond Portfolio

The following table provides a brief summary of how the JDP Bond Portfolio has performed on average over the last three years:

Staying Strong

“You have power over your mind, not outside events. Realize this, and you will find strength.” - Marcus Aurelius

Grappling with ongoing uncertainty and volatility isn’t the most comfortable thing. However, it helps me to remember that adversity cultivates resilience, and resilience only makes us stronger.

Rest assured that we are your true partners in this; we are investing our capital right alongside yours. Thank you for trusting the process and for trusting us. We will always work hard to remain worthy of your trust.

Cordially,

Joseph Del Principe