Kerrisdale Capital is short shares of C3.ai Inc (NYSE:AI), a $4 billion market capitalization enterprise software company that has risen from the ashes of its busted IPO based on the misconception that its self-proclaimed “AI leadership” somehow positions it to benefit from Silicon Valley’s current tech theme du jour: generative AI as represented by media obsession ChatGPT.

We believe these speculative flames won’t burn bright much longer, as the realities of C3’s poor customer traction, failing sales partnerships, and financial pressures will catalyze what is likely to be a painful reality check.

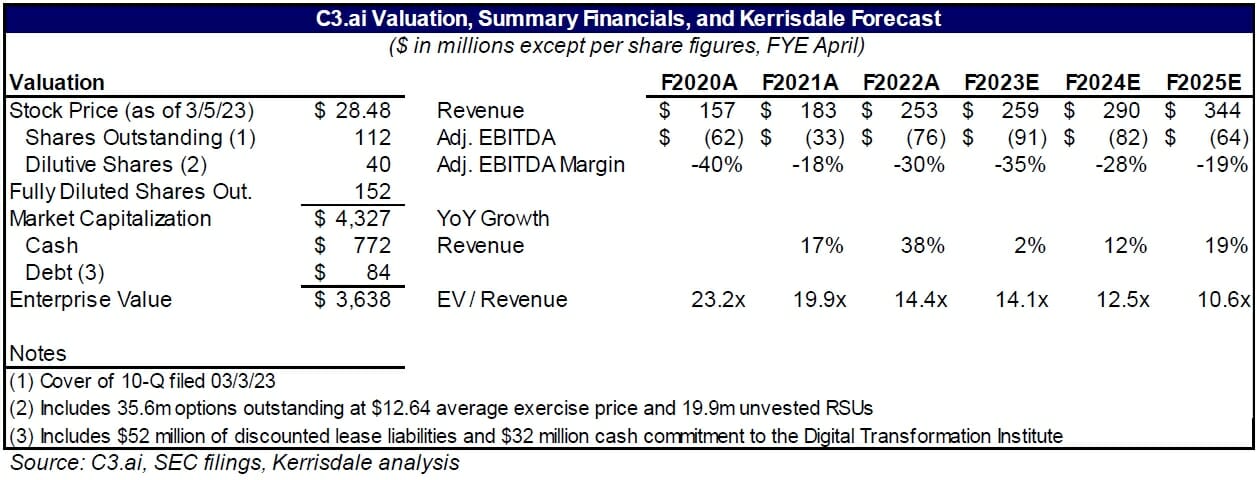

Q4 2022 hedge fund letters, conferences and more

This isn’t the first time C3 has sought to ride a hot investment theme. The company was originally founded as C3 Energy to develop analytics solutions for public utilities preparing for the emergence of cap-and-trade and smart grids. C3 pivoted in 2016, renaming the company C3 IoT to capitalize on that buzzy opportunity.

But management’s master stroke was rebranding operations as C3.ai in 2019 and going public with the “AI” stock ticker, thus securing its place as the default artificial intelligence stock play for the undiscriminating investor despite the bulk of its business coming from relatively dated analytics models built for a very small number of utility, energy, and government customers.

C3 is a minor, cash-burning consulting and services business masquerading as a software company, and its true value is a fraction of its current market capitalization.

Generative AI will do nothing to change the business or financial trajectory of C3 any time soon, yet C3 faces numerous, more serious near-term challenges. The company sells an expensive, trailing edge, and difficult to implement solution that is losing out to a plethora of alternative solutions. To make matters worse, C3’s go-to-market motion seems to be completely broken.

Excessive salesforce turnover suggests fundamental leadership issues, and the company’s marquee sales partnership, with energy services giant Baker Hughes, seems to be falling apart. Furthermore, we believe C3’s cloud partners, Microsoft, AWS, and Google, are more foe than friend.

Thus, while C3 has done its best to obfuscate the facts, the company’s track record of new customer acquisition is shockingly poor. Management has used recent pricing changes and accounting tricks to distract the market from the company’s deteriorating results, but all signs point to a further weakening of fundamentals ahead.

C3 was egregiously overvalued even before its shares caught the generative AI hype wave, which added an unjustified $2 billion to its market capitalization in just a few short weeks. Shares should return from whence they came, approximately $12 per share, or almost 60% below current levels.

The company’s high mix of lower margin professional services, challenged growth, and industry worst cash flow profile suggests the downside could be even greater. We find little about C3.ai intelligent, but plenty artificial.

Company Background

Originally founded as C3 Energy in 2009 by software entrepreneur Tom Siebel, the company’s original focus was on data analytics for public utilities to capitalize on emerging themes such as smart grid, demand management, and cap-and-trade.

C3 won business at a handful of major utilities, but the prospects for growth in the notoriously slow-moving sector didn’t match Siebel’s ambitions.

As the Internet of Things (IoT) became a dominant, yet somewhat amorphous, investment theme in the tech sector, Siebel pivoted, renamed the company C3 IoT, and pitched its data collection and analysis capabilities as a key enabler for the deployment of industrial sensors and other connected devices.

Alas, this market too was slow to develop due to a jumble of tech standards, implementation complexity, and high costs. With the IoT fad subsiding, Siebel took his most ambitious leap, rebranding the C3 product as “artificial intelligence” and changing the company’s name to C3.ai in hopes of capitalizing on the investment theme de jour.

Once again targeting a nascent, ill-defined market, C3 firmly planted its flag as “the” enterprise AI company and fortuitously snagged the stock ticker “AI”. C3 went public in December 2020, and with limited AI investment vehicles available in a frothy market for SaaS names, investors bid up its shares from the $42 offer price to a high of $177, equating to a market cap exceeding $20 billion.

However, despite its claims of enterprise AI leadership, most of C3’s business came from predictive maintenance models for energy companies and the Department of Defense (DoD) and legacy data analysis tools sold to utilities.

A bloated pretender with stagnating revenue growth, C3’s shares quickly fell back to earth. Having achieved fallen angel status, management recently pounced on yet another opportunity to pump C3 shares: generative AI, a flavor of the technology that seemingly has little relevance to C3 products and will do little to address the shortcomings that have limited their adoption.

In addition, C3 announced a transition from subscription to consumption pricing, which we believe is designed to serve as an excuse for the company’s poor financial performance, as well as facilitating a shameless plug that C3 should now be valued in line with richly-priced SaaS consumption pricing players like Datadog and MongoDB. We believe the market is due to for yet another C3 wake-up call.

C3’s Product Offering is a Hard Sell

Tom Siebel suffers from many shortcomings, but selling a vision is not one of them. With a deep rolodex of CEO relationships and a sales pitch that resonates with CEOs seeking to embrace technology, Siebel sells a vision that C3 is a tool for corporate “Digital Transformation”, the process by which companies leverage new technologies and associated analytics to transform operations and improve decision-making.

We heard from both former sales employees and C3 customers that Siebel’s top-down pitch sold CEOs on his grand vision, even if it meant undermining CTOs and CIOs who foresaw some of the practical limitations of the C3 offering. Not surprisingly, the sales cycle for such a solution ranges from 6-18 months or more.

The C3 sales pitch also takes aim at the easiest of targets: IT consultants. Most strategic enterprise technology redesigns are still conducted by outside consultants such as Accenture, Deloitte, McKinsey, and Boston Consulting Group, who have well-deserved reputations for difficult and expensive bespoke IT implementations.

Noting the high failure rates of such projects, C3 positions itself as the savior with an all-encompassing platform that can cure the gamut of IT ills. However, the practical reality is that, despite its pitch, the C3 solution is difficult and expensive to implement, has been operationalized to address a fairly limited set of applications, and is likewise prone to failure.

There are two core elements of the C3 offering: an application platform and a portfolio of applications.

The C3 Application Platform: Onerous Data Plumbing

C3’s “application platform” attempts to access, integrate, and manage the vast array of data sources resident within a large company by leveraging an array of building blocks and domain-specific languages to create a system that provides data programmers a simpler way to integrate and access data from traditional databases, industrial sensors, and alternative data sets.

Yet, there is no escaping the inherent complexity of such a task. C3’s platform implementation largely mirrors that of a traditional IT consulting project: time-consuming, resource-intensive customization work requiring extensive use of C3 professional services personnel. In short, C3 customers incur all the brain damage associated with traditional “visionary” IT projects.

While the C3 platform cannot be classified as “AI”, most customers we surveyed actually considered it the most valuable component of the offering, as it solves known data collection and integration challenges that can plague enterprise analytics.

Of course, the extent to which the C3 platform adds value will be directly correlated to the complexity of the organization’s data architecture and requirements, which probably explains why various DoD entities are oft-mentioned customers.

However, we believe investors should be alarmed that there are numerous alternative solutions in the market. Most notably, Snowflake offers a multi-cluster, cross-cloud unified data platform that is comparatively easy to implement and operates at a materially lower cost. A simple comparison highlights the difference.

Only 6% of Snowflake’s LTM revenue comes from professional services, while that figure has historically ranged from 14%-18% for C3, and, as discussed below, we believe this figure is dramatically understated.

Read the full report here by Kerrisdale Capital