“Promise yourself to be so strong that nothing can disturb your peace of mind. Look at the sunny side of everything and make your optimism come true.

Think only of the best, work only for the best, and expect only the best.

Forget the mistakes of the past and press on to the greater achievements of the future.

Give so much time to the improvement of yourself that you have no time to criticize others.

Live in the faith that the whole world is on your side so long as you are true to the best that is in you!”

– Christian D. Larson

Brianna, sent me a text message over the holiday, “I just read your OMR piece – very interesting.”

I responded, “Here’s the bottom line:

- We’ve saddled my generation and worse yours with too much debt.

- Because of the debt mess, governments around the world are trying to print, buy and sweep it under the carpet.

- Think “how the economic machine works.” The most important thing to understand is that we are at the end of a long-term credit expansion cycle and at the beginning of a deleveraging cycle.

- Many people can’t get credit anymore. Tapped out.

- We need to get out of this debt mess and reset the system somehow.

- It will take a dozen or so years. It has to break (default in some form) before it can reset.

- The question is whether governments soften the blow or not. A beautiful or ugly deleveraging?

- The U.S. has a better shot. Europe has bigger structural challenges. Japan and China?

- Can one do it? Can they all do it?

- We need to reset or the greater power of economic reality will do it for us.

- We’ll get through it but not without consequences. It will be bumpy.”

I concluded my text reply to Brie saying, “Maybe I need to take a happy pill, but I’m almost certain I’m right. No guarantees. We’ll see.”

And her text back to me made me smile, “Well, on the positive side — this too shall pass and we are fortunate to understand what is happening and can better prepare for it… AND it’s Christmas so let’s not worry and drink some of Rory’s yummy wine  .”

.”

How about that! “Promise – peace – optimism – think – best – future – faith – true – you.” Amen!

Brianna works in New York with a team of people lead by her boss Rory Riggs. Google him. He’s sharp and probably the brightest business mind I know. Rory sent Brie home with an outstanding bottle of red wine and, oh yes, we did drink it. Their firm, Syntax, has created a better way to index. Think owning the same stocks in the S&P 500 Index but weighted across the same constituents in a way that diversifies you better. Same with small caps, sectors, etc. The result is an improvement in returns and the numbers are compelling. You’ll want to learn more. Stay tuned.

By the way, if you are going to the Inside ETFs Conference in Florida later this month – you should take a minute to stop by their booth. No, I’m not on Rory’s payroll… just a big fan. And a special hat tip to the brilliant Mark Finn. A godfather behind the curtain and one of the smartest investors I know.

The Inside ETFs Conference is on January 22-25, 2017 at the Diplomat Beach Resort in Hollywood, Florida. I’ll be speaking at the event. You can learn more here. If you are attending, please send me a note… I hope to see you there.

Today, let’s take a look at the most current equity market valuations for they can tell us a great deal about future 7-year and 10-year annualized returns. We’ll also look at the bond market. Total U.S. credit market debt-to-GDP is nearly 355%. Global debt-to-GDP is 325%.

I hope you find the messaging in such a way that your retail client can better understand. I believe that the biggest bubble of all bubbles is in the bond market. If not tactical last quarter, that bond portion of a portfolio took a beating. What can you do? I share a few ideas. You’ll also find a great chart showing bond yields dating all the way back to the year 1285 (not a typo). It is a reminder that we sit at a very unusual period in time. The great bond bull market is behind us… not ahead of us. But let’s see opportunity… not despair.

And drink some yummy red wine! Hold the glass up high and “Promise yourself to be so strong that nothing can disturb your peace of mind. Look at the sunny side of everything and make your optimism come true. Think only of the best, work only for the best, and expect only the best.”

Not a bad way to begin the new year. I hope you find this week’s post helpful.

? If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ?

Included in this week’s On My Radar:

- Year-End Valuations and Forward Equity Market Returns

- The Bond Market is Facing the “Perfect Storm”

- Trade Signals – Don’t Fight the Trend or the Tape… A Golden Rule

Year-End Valuations and Forward Equity Market Returns

Chart 1: My favorite – Median P/E. At 22.9 the market remains “Overvalued”

Here is how you read the chart:

- Median P/E is the P/E in the middle, meaning there are 250 companies out of 500 that have a higher P/E and 250 that have a lower P/E.

- The red line in the middle section shows you how P/Es have moved over time (updated monthly).

- The green dotted line is the 52.8 year median. So a Median P/E of 16.9 is the historical “fair value.” Simply a point of reference.

- You can see that over time the red line moves above and below the dotted green line.

- The future returns come when you buy at “bargains.” It also happens to be when risk is least.

- As you’ll see in Chart 2, the worst returns come when Median P/E is in the highest 20% of all readings. That is where it sits today. Expensive!

One last comment on the above chart. At the very bottom of the chart, NDR calculates just how far the market is from “Overvalued,” “Median Fair Value” and “Undervalued”. For example, Median Fair Value is determined by taking 16.9 (Median P/E) x 97.90 (Most recent 12-months earnings) or 1654.50. The S&P 500 Index closed the year at 2238.83 which is 26.1% above fair value. A correction of -26.1% would mark a point in time where you would get better bang for your money.

A correction to “Undervalued” would make for a great buying opportunity. Unless one is run over by the 48.7% decline it will take to get there. Such declines come in recession so we’ll keep close watch on the recession indicators (more on that next week). No sign of U.S. recession for now. I am on record predicting 2017 to be the year. I’m not so sure. We’ll watch the data and I have some pretty good recession indicators that have done a good job at calling them in advance. Again, no recession signs today.

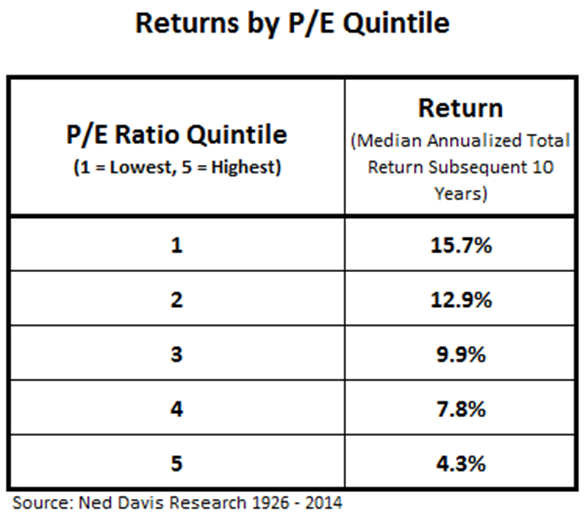

Chart 2: Median P/E and Forward 10-Year Returns

Median P/E can help us predict what is likely to be the coming 10-year annualized returns for the S&P 500 Index. Not perfect but a pretty good guide.

Here is how you read the data:

- A Median P/E of 22.9 puts us in the highest quintile.

- The overall idea is to determine if buying at bargains is better than paying up.

- In this way, looking at actual reported Median P/E every month back to 1921 we can then measure what the subsequent 10-year returns turned out to be.

- Then look at each month and see what the returns were 10 years later. Step forward a month, what were the returns 10 years later. And so on…

- Then group all of the month-end actual reported Median P/Es into five quintiles (not Wall Street’s future guesstimates… actual real numbers) and then evaluate what the subsequent 10-year average returns were by quintile and you get the following chart:

We sit today firmly in quintile 5. It is telling us to expect the low returns over the coming 10 years. We want to be aggressive buyers of equities when we get to quintile 3, 2 and 1. That’s how measuring valuations can help us. For now, patience.

As a forward guide, when I share the Median P/E with you at the beginning of each month, use this next chart as a guide to see which quintile we are in:

Chart 4: Shiller’s CAPE or Cyclically Adjusted P/E (a measurement process that smooths P/E over the last 10 years).

Current level is 28.26.

In simple terms… historically very high!

Chart 5: Shiller P/E 28.22 as of 1-5-17

John Hussman shared this next chart — it is similar in thinking to Chart #2 above except it looks at P/E by quartile not quintile. Same conclusions. Expect low coming returns.

Here’s how you read it:

- With a CAPE of 28.26 we sit firmly in the CAPE 20 to 48 quartile. Real returns (nominal returns less inflation) of less than 2% annualized are probable over the coming 10 years.

Chart 6: What about Drawdowns?

Here is a look at the downside risk by quintile. Remember, we sit in the most expensive quintile. The simple point is that risk is highest when valuations are highest.

Chart 7: Household Equity Percentage vs. Subsequent Rolling 10-Year Returns

This next chart is one of my all-time favorite charts. Here’s how you read it:

- The blue line tracks just how much households own in equities as a percentage of their total liquid net worth.

- The dotted black line is a plot of what the annualized 10-year return turned out to be.

- What it shows is that at points in time when households had a large percentage invested in stocks, the subsequent 10-year returns were lowest.

- Note late 1999 – early 2000. The blue line was at 62% (left hand column). It predicted a subsequent return of approximately -3% per year.

- The black line shows what actually happened.

- Also note how investors raced out of equities in 2008 and 2009. At the market low in early March 2009, the most recent household equity percentage ownership was at 33%. At that level, the data is projecting a 15% annualized return from 2009 to 2019.

- We don’t yet know the 10-year numbers but pretty safe to say that so far returns for equities since March 2009 have been good. Problem is, and I’m pretty sure you’ll agree, that most people were in a state of pure panic. They were selling when they should have been buying.

- Finally, where are we today? The blue line is at 53.1% as of September 2016 quarter-end suggesting a 2.75% coming 10-year annualized return (before inflation).

We can use this chart as a guide. I’ll share it with you from time to time. Point is that we want to get our clients prepared to overweight stocks when the getting gets good. The hard part is they’ll need to be a buyer when everyone around them is panicking. That’s when opportunity is always best.

Chart 8 – Price to Sales, Price to Operating Earnings, Etc.

Here’s how you read the chart:

Look to the far right – most valuation metrics are “Extremely Overvalued”

The Bond Market is Facing the “Perfect Storm”

I’ve been saying for some time that the biggest bubble of all bubbles is in the bond market. European sovereign debt might just be the first to crisis. Further, global debt has reached 325% of GDP. Academic studies show that economies get into trouble when debt-to-GDP exceeds 90%.

OK, in English for your clients who have other important things to focus their time on: If you earn $100k per year and borrow $10k per year, your spending power was $110,000 (before taxes, of course). That leveraging up fuels the economy. Another year passes, you earn more, your credit rating improves, and you can borrow more. Economies expand on income and credit (spend today is good for growth – pay off tomorrow is bad for growth). But how do we know when we’ve reached tomorrow?

Academic research shows that number to be about 90% debt-to-GDP. Think of GDP as a country’s gross income. So what if you earn $100k and borrowed and now owe $90k? Can you see it is now getting harder to borrow from a bank and that more of your income is required to pay the interest on the $90k debt? Your economy slows.

Expand that to the U.S. and you find a 105% debt-to-GDP number. Well, the number is actually much higher than that if you include Social Security and Medicare debts and several others government has creatively reworded, but they are debts to be paid and the total number is north of 250%.

The next chart shows the breakdown of that debt.

Global debt-to-GDP is now 325% of world GDP, rises to record $217 trillion. Europe and China are a mess. When I say “debt” is our single biggest global issue, debt here, there and everywhere, it is like you are earning $100k and owe $325k to the banks and credit card companies. Is it any wonder that global growth has slowed and limps along?

Every country is competing for growth. How? Lower currency in a way that puts your goods on sale. It gets dicey. All this leads to currency and trade wars. We are seeing this in China, Europe and in Trump tweets today.

As Hardy said to Laurel, “Well, here’s another fine mess you’ve gotten me into!”

Harvard Academic Sees Debt Rout Worse Than 1994 ‘Bond Massacre’

The current bond market is facing the “perfect storm” of potential steepening of the bond yield curve, monetary policy tightening and a multi-year period of sustained losses due to a “structural” return of inflation resembling that of 1967. (Source: Bloomberg)

If you thought you had already read the gloomiest possible prognosis for bonds, wait until you read this one.

Paul Schmelzing, a Ph.D. candidate at Harvard University and a visiting scholar at the Bank of England, said if the latest bond market bubble bursts, it will be worse than in 1994 when global government bonds suffered the biggest annual loss on record.

“Looking back over eight centuries of data, I find that the 2016 bull market was indeed one of the largest ever recorded,” wrote Schmelzing in an article posted on Bank Underground, which is a blog run by Bank of England staff. “History suggests this reversal will be driven by inflation fundamentals and leave investors worse off than the 1994 ‘bond massacre’”.

The gist of his message is this:

- Schmelzing research focuses on the history of international financial systems.

- He divided modern-day bond bear markets into three major types:

- inflation reversal of 1967-1971,

- the sharp reversal of 1994 and

- the value at risk shock in Japan in 2003.

- The Bank of America Merrill Lynch Global Government Index of bonds fell 3.1 percent in its worst-ever annual loss in 1994 as then-Fed Chairman Alan Greenspan surprised investors by almost doubling the benchmark rate.

- Treasury 10-year yields surged from 5.6 percent in January to 8 percent in November.

- Schmelzing said, “The current bond market is facing the “perfect storm” of potential steepening of the bond yield curve, monetary policy tightening and a multi-year period of sustained losses due to a “structural” return of inflation resembling that of 1967.”

- Last quarter was the worst for government bonds since 1987, according to data compiled by Bloomberg.

I bet you’re sitting there wondering what bond yields look like today vs. the year 1285. Here you go:

Not your father’s bond market. Interest rates move higher and the squeeze gets tighter.

But, fear not! Just think about your bond allocations differently.

Here’s what you can do:

Diversify the bond portion of your portfolio to several tactical bond trading strategies. If we are heading for a reset, which I believe may take several years, then you’ll want to find ways that gets you to that higher interest rate opportunity with capital intact. It won’t be straight up; it will be bumpy. Protect and grow, protect and grow.

Trend following trading strategies can help:

- Tactically trade the trends in high yield. Non-emotional. Easy to implement but requires an ability to religiously stick to the process. A high percentage of profitable trades with downside risk protection.

- Take a look at the Zweig Bond Model signal… I post the chart each week in Trade Signals.

- Tactical Fixed Income – take a look at our Tactical Fixed Income Index. It looks at nine fixed income ETFs and allocates to the top two showing the strongest positive price trends. It lost 1.08% last quarter vs. a decline of 7% in the Barclays Global Bond Index. A 6% beat. It gained 11% for the full year 2016 vs. a gain of just 2% in the Barclays Index. Email me if you’d like to learn more about how it works.

- Diversify to several tactical fixed income trading strategies. No guarantees — all investments involve risk; however, each of the above three processes came through the recent spike in interest rates (loss in bonds) quite well.

The point is that now is not the time to buy-and-hold bond funds and ETFs; however, bonds can still play an important role in your portfolio(s).

You’ll find several bond signal updates weekly in the Trade Signals blog (link below). Email me if you have any questions.

Trade Signals – Don’t Fight the Trend or the Tape… A Golden Rule

S&P 500 Index — 2,270 (1-4-2017)

Posted each Wednesday, Trade Signals looks at several of my favorite stock, investor sentiment and bond market indicators. It is my weekly risk management dashboard, designed to keep me better in sync with the major technical trends. I hope you find the information helpful in your work.

Following is a summary of what I am seeing this week:

Each week I post a chart called “Don’t Fight the Tape or the Fed.” This simply means that the Tape (or the trend of the market) and the Fed are important considerations to your financial health. Combined together, they produce a historically strong timing indicator. It looks like this:

Source: Ned Davis Research (NDR)

The above chart shows the annualized gains per annum based on the reading of the model. The current score is highlighted in yellow. In short:

- You want to be bullish when the trend is positive and the Fed is lowering interest rates – Readings of +1 and +2.

- You want to be neutral and more cautious (long but hedged) when the indicators are mixed – Readings of 0 and -1.

- And most importantly, you want to “watch out for -2.”

The current reading is -1. You want to be neutral and more cautious. Have equity exposure (but hedged). Keep the 200-day moving average stop-loss rule in mind.

Equity Markets: The overall trend remains bullish as measured by the CMG NDR Large Cap Momentum Index (a trend-based indicator), the 13/34-Week Moving Average Trend and Volume Demand (more buyers than sellers). Don’t Fight the Fed or the Tape (Trend) is neutral. The weight of evidence for the equity market remains bullish.

Fixed Income: Our fixed income trend indicators have done a great job at avoiding the large declines that have hit the bond market. Rates moved even higher and bond values lower over the last week.

- Zweig Bond Model(ZBM) moved to a sell signal on October 12, 2016 and remains in a sell today. Chart below. We favor holding “BIL” over longer-dated fixed income ETFs, such as BND or TLT. The short-term trend for high quality fixed income remains bearish.

- CMG Managed High Yield Bond Program remains in a buy signal. The trends in HY funds and ETFs are bullish.

- CMG Tactical Fixed Income Index. Currently positioned: 50% in JNK (SPDR Barclays High Yield Bond ETF) and 50% in CWB (SPDR® Bloomberg Barclays Convertible Securities ETF). Both fixed income asset categories have been trending higher. The index is up 2.25% in the last month and up 11.80% over the last year. You can track the CMG Tactical Fixed Income Index here. See important index disclosures below.

Tactical All Asset and Liquid Alternatives:

CMG Opportunistic All Asset Strategy:

The Index is up 2.77% in the last month and up 7.91% over the last year. You can follow the daily, weekly, monthly and annual performance of the CMG Tactical All Asset Index here. See important index disclosures below.

Click here for the most recent Trade Signals blog.

Concluding Thought and Personal Note

Put this next chart in the “food for thought” category. Look at those bond returns from 1950 up to 1980. Just saying…

Source

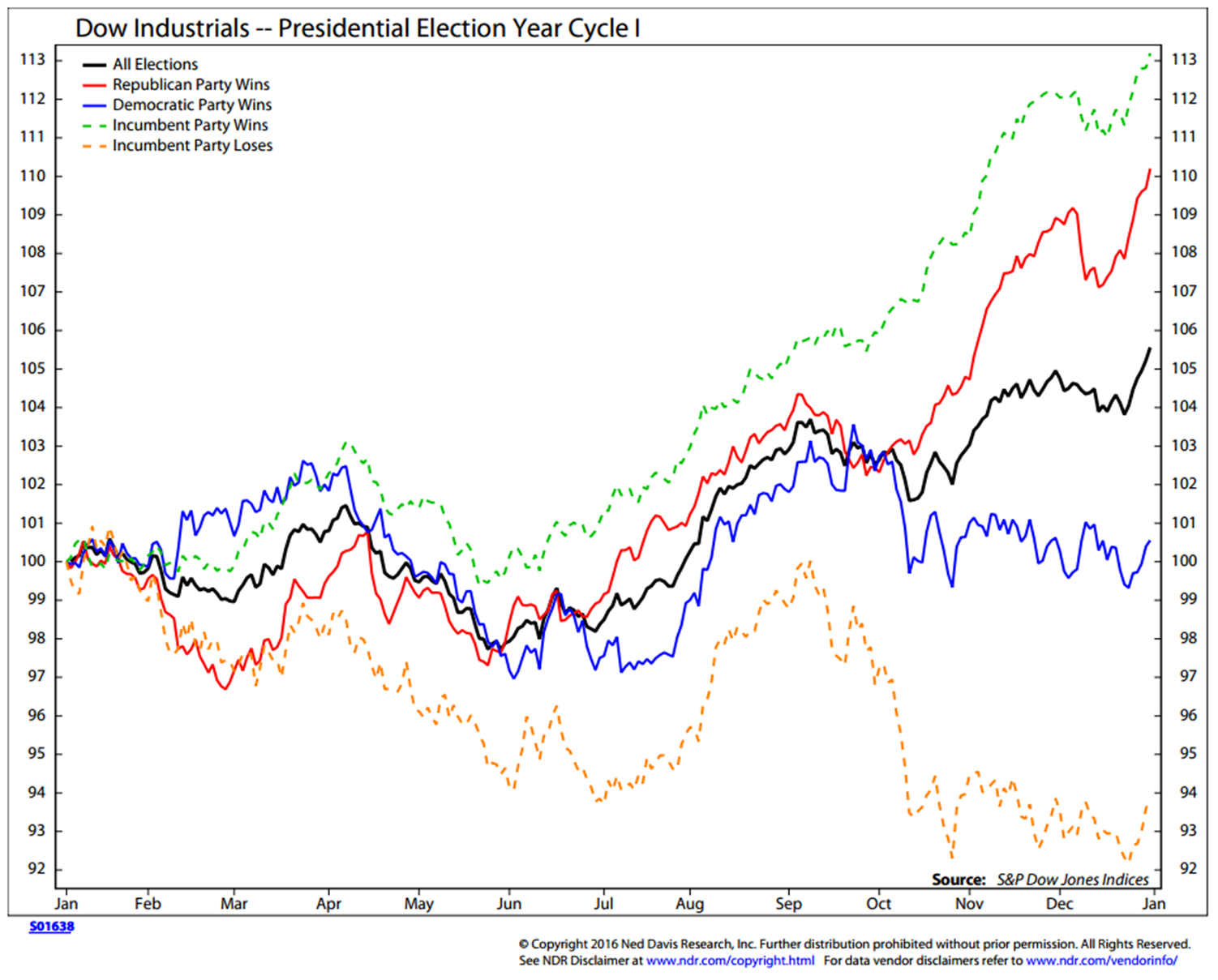

Put this last and final chart in the “fun” category:

- This chart shows what the Dow Industrial average did in prior election cycles – year one.

- The orange dotted line shows what the market did the first year when the incumbent party lost.

If this chart is to be any guide to 2017 (and there is most certainly no guarantee), then expect a market top in January followed by a retest of the high in September and a sell-off into year end. It suggests a negative return year for equities. Of course, no guarantees and data set is fairly small.

Keep in mind that if you gained 1% in 2015 and 10% in 2016 and the market corrects 6% to 10% in 2017, then your equity gains for the full three years will be close to 0%. Overall, high valuations and high debt and low growth are the culprits. We remain in a low coming 10-year return world.

The S&P was up just 3% going into the election. The prior two years of gains stood near that same number — up 3% over 24 months. Frustrating. To the surprise of all of us (certainly me), the market gained 7% from the election into year-end. So far, 2017 is off to a pretty good start.

As you saw in Trade Signals, the trend remains bullish for equities and we’re riding the trend. But keep risk in mind. As the great Art Cashin reminded me again this morning, “Stay wary, alert and very, very nimble.”

The travel schedule is picking up. Early Sunday morning I’m boarding a plane for a three-day business meeting in Vail. I know. Poor Steve… I’m really excited and the forecast is for up to 40 inches of snow. If you are a skier, you know how much fun it is to float on top of deep powder snow. Wish we could bottle that feeling and sell it to the world.

I’m in Dallas on January 16-17 for several fund-related meetings. The Inside ETFs conference in Hollywood, Florida follows on January 22-25. I know… poor Steve again. Lucky and grateful! February 1 finds me back in Dallas for an S&P Index conference. I’ll send more information on that conference to you next week.

Wishing you a wonderful weekend!