Today, CoinDesk, the leading resource for crypto research & data, published their highly anticipated Q3 Market Report outlining the trends driving the digital asset markets, focusing on Bitcoin, Ethereum, DeFi, and more. In all, assets generally performed well, scaling projects on Bitcoin and Ethereum thrived, institutions started paying even more attention, and politicians flexed their regulatory muscle.

Q2 2021 hedge fund letters, conferences and more

Key Findings:

- $BTC became less correlated with other macro assets like gold, bonds, and the S&P 500. It could serve as an exciting tool to hedge a balanced portfolio.

- NFT trading dominated the market narrative as OpenSea’s volume topped $3.4 billion in August alone.

- Average CryptoPunk sales neared 120 $ETH, worth several hundred thousand dollars.

- Alternative layer one solutions and their governance tokens, like $BSC, $SOL, $LUNA, and $AVAX, grew in market capitalization and usage over the quarter.

- The demand for scalable access to blockchain protocols as users moved cross-chain and onto layer 2s.

- While the overall crypto market performed well in Q3, $ETH showed dominance and neared its May highs.

- $ETH outperformed primary DeFi tokens over the past several months, including $UNI, $SUSHI, $AAVE, and $COMP.

Executive Summary

In the following report, we aim to summarize some of the key themes and metrics that highlight the quarter’s progress in cryptocurrency markets.

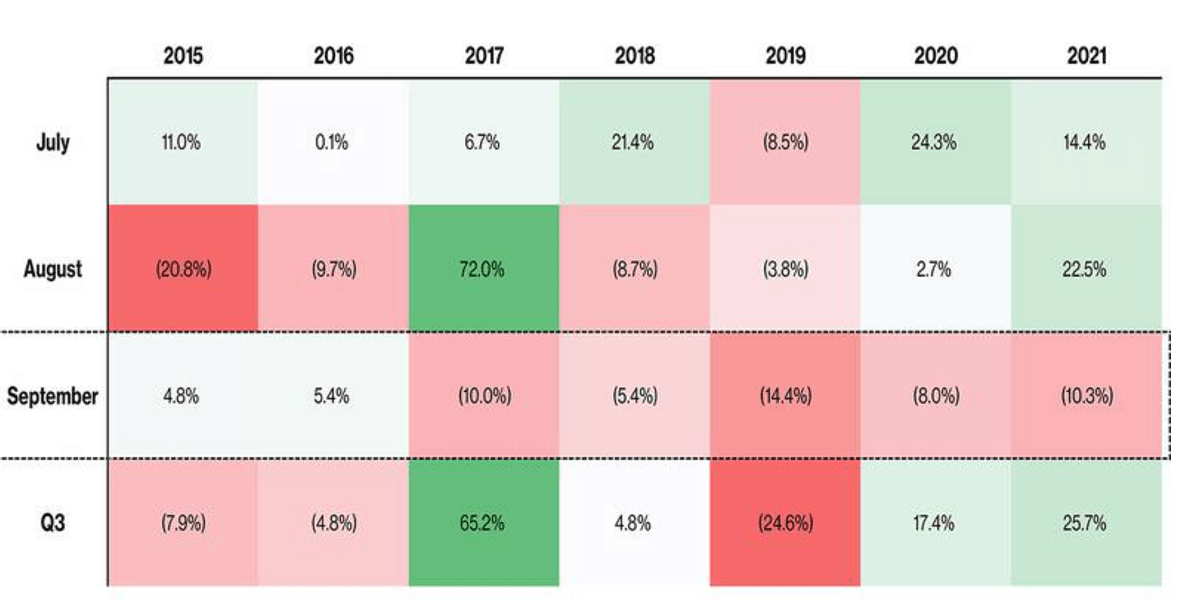

Q3 2021 was a welcome relief for the market after BTC and ETH hit all-time highs in early Q2 2021, only to come tumbling down. Both assets performed well from a price perspective, adding 25.0% and 31.8%, respectively. It felt as though the market was taking a breather, which revealed itself through lower volatility measures than in any other quarter this year, albeit with levels still far above established macro assets. On top of that, BTC proved mostly uncorrelated with gold, the S&P 500, bonds and the U.S. dollar, highlighting that BTC could have a unique place in portfolios.

We started Q3 still hanging on the words of Tesla CEO Elon Musk, which led to an ARK Invest-hosted event, dubbed “The B Word,” focused on explaining bitcoin to institutions. The event featured a keynote panel of Cathie Wood (ARK Invest), Jack Dorsey (Twitter, Square) and Musk. The topic of discussion was “Bitcoin as a Tool for Economic Empowerment.” The event was widely watched live across the industry.

Stablecoins reentered the spotlight when Circle, the issuer of stablecoin USDC, announced its intention to go public. This move sparked a wave of stablecoin issuers disclosing what exactly was backing their pegged coins. Those disclosures left some skeptics and investors unsatisfied.

Meanwhile, non-fungible tokens (NFT) exploded in popularity— even Visa bought a CryptoPunk. NFTs also paved the path to making Ethereum expensive for transactions, triggering extended discussions around scalability and accessibility which, in turn, led to the rise of alternative layer 1 and layer 2 smart contract blockchains. A similar story was played out in Q3 for bitcoin, which officially became legal tender in El Salvador. Salvadorans transacted bitcoin using the Lightning Network, an open-source, decentralized, rapidly growing layer 2 scaling system for Bitcoin, to mixed reviews.

All the while, regulators and politicians all over the world applied pressure to bitcoin and crypto: China doubled down on previous bans; Binance navigated regulations; and the U.S. proposed new crypto tax rules, which were met with heavy criticism from crypto supporters.