Whitney Tilson’s email to investors discussing Arne Alsin on his supersize position in Tesla Inc (NASDAQ:TSLA); Tesla’s declining market share; Mark Spiegel August letter; how Elon Musk’s Starlink satellite internet keeps Ukraine online, and the debate over FSD.

Arne Alsin’s Supersize Position In Tesla

My usual mix of bullish and bearish opinions on Tesla…

1) Here’s Arne Alsin explaining why it’s a super-size position in his fund:

A question from one of our investors: “I’m curious to know how things are looking for Arne deciding to invest in other things.

Q2 2022 hedge fund letters, conferences and more

Obviously Tesla is the big play, and he’s taken some Spotify and dabbled elsewhere, but no other big bets. Does he see anything brewing, or is this the way for now?”

Arne: Good question. Our goal is to construct the best performing, highest conviction portfolio we can. We’re always looking at new companies, new industries—so absolutely. For example, if you look back to the midpoint of our performance track record, the portfolio was dominated by Amazon, Netflix, and Facebook.

Now it is Tesla, Spotify, and Amazon. If we see something that’s worthy of our investment capital, we’re ready to size up new positions. As I always coach the team, ‘We only own #1.’

We don’t play around with second or third best companies in a category. We’re happy to be patient, too. If we get in at the second or third inning of a company’s growth, that’s fine. But they’ve got to be the #1, dominant winner. That’s what matters.

The concentration in Tesla is a unique situation, and it’s a reflection of my conviction in their market dominance relatively early in the cycle. I view owning Tesla in 2022 like owning Apple in 2007… or maybe even 2003… or maybe even earlier.

And this company is going to be much, much bigger than Apple, in my opinion. In my investing career, I have never come across a position that I not only thought had the potential for massive returns moving forward, but one that I had the utmost conviction in – even more so than Amazon.

I think we’ve barely scratched the surface of what this company can become. And so my view: We have to own it in size. My projections for Tesla’s growth are far, far beyond the consensus view right now.

I like to stay calm and dispassionate about these types of situations, but the truth is I’m giddy. I think we could be set up for a couple of years of strong growth, far beyond what Wall Street is expecting.

Over the next few quarters, I think we’re going to see a swell of activity around Tesla in the investment community and on Wall Street. In my mind, it’s not a question of if, it’s a question of when.

I know I’ve probably said this before in previous Q&As or letters or phone conversations, but I continue to think Tesla is destined to be Wall Street’s favorite stock.

It’s got all the right ingredients—fast growth into vast, global end markets, rapidly expanding gross and net margins, a wide moat, endless demand for the product, and crazy potential upside from energy storage FSD, bots, AI—none of which I think are priced into the stock.

I know it doesn’t look pretty to more conventional outsiders, and I know the stock is hated by some pockets of the investment community, but A) I don’t care about looking pretty and B) the best investments are almost always hated for a period of time before they become consensus.

Many of the so-called “smart money” on Wall Street wouldn’t touch Amazon in the 2010’s but had no problem buying it in the 2020s.

The best rewards come to those who wait, by the way. We just need to be in position—and we are.

2) A friend’s comments:

I’m looking at the real-time data from the four European countries that report daily sales data — Sweden, Norway, Netherlands and Spain. This is to assess how Tesla is doing this quarter, from where we have the very latest data, even if it’s only one piece of the puzzle.

In Q1, Tesla sold 10,165 vehicles in those countries for a 15% share. I am not sure what’s the definition of the base here — BEV only or EV as a whole (including PHEV). It doesn’t matter, as long as the definition is consistent in a comparison over time.

In Q2, Tesla sold 6,619 vehicles in those countries for a 9.0% share.

So far in Q3, with a couple of weeks left to go, Tesla has sold 5,223 vehicles for a 9.8% share.

As such, it looks like Q3 is going to end up similar to Q2 as far as these four countries are concerned. Remember, everyone blamed the huge drop-off in Q2 sales (compared to Q3) on Chinese lockdowns. Well, it doesn’t seem like there has been any meaningful improvement in Q3.

For example, MG — which is a Chinese brand these days, not British — in the same four countries sold 3,234 units in Q2 but in Q3 they sold 2,961 units thus far.

It would appear that MG is doing relatively similar to Tesla in terms of a comparison vs Q2, in terms of the growth rate — approximately flat.

MPG is now selling at least 50% of Tesla’s volumes in these four countries in Europe. As a result of that analogy, what kind of valuation should MG have? Half a trillion dollars?

Tesla needs to deliver at least 370,000 units this quarter, globally, in order to have a prayer to have a good full 2022 year with a monster fourth quarter needed at that point.

I think Tesla will come relatively close to the 370,000 units for Q3, but a 340,000 number is also in the zone, which would be a disappointment.

The thing is, demand for these cars are going down the toilet because of the economic recession right now. It’s really that simple. Would-be buyers are pulling in their horns. This will impact the whole industry, not just Tesla.

However, Tesla is extra sensitive because it’s considered a more risky luxury product, and is faced with a new set of risks and costs associated with higher electricity prices and outright shortages — real or perceived.

The pressure on Tesla’s sales may therefore be extraordinary, and if Tesla prints two quarters in a row around 340,000 units each, then Tesla’s multiple could collapse 50%, earnings also close to 50%, and then I would expect Tesla could fall from $300 a share to under $100 within about half a year.

His earlier comments along the same lines:

The month of July 2022 was the first month for which I have statistics, that Tesla’s global market share of BEVs — in other words EV excluding PHEVs — fell below 10%.

In July 2022, Tesla sold 52,000 cars globally, and the global BEV market was 550,000 cars.

EVs altogether — including PHEVs — were 778,000 cars, but that’s another story. Tesla’s 7% market share of all kinds of EVs was similar to April 2022 and July 2021, exactly one year prior.

I thought this was important because Tesla bulls tend to always claim that it is Tesla’s market share in BEVs only that is important, that that’s the trend to watch. In other words, exclude PHEVs for the relevant analysis.

Now this BEV-only number has fallen to a record-low 9%. It had reached 10% last October and 11% one year prior, in July 2021. Those were the lowest numbers on record before July 2022.

Obviously the third month in the quarter (September etc) is Tesla’s large market share month, and it was 23% of the global BEV market in June 2022 for example The average for the second quarter of 2022 was 18% as a percentage of the BEV-only market — and 12% of the total EV market.

Slice it anyway you want, and those numbers were also down from the prior year. The 18% BEV-only number was down from 21% a year prior, and the 12% PHEV-inclusive number was down from 14% a year prior.

The question for the bulls is: Tesla’s market share keeps falling. We can debate how quickly it is falling, but the big question is: Where will it stop?

In other words, what will be Tesla’s “terminal” market share among BEVs? (or for that matter EVs overall) One really can’t begin valuing Tesla without answering this question.

Will Tesla’s BEV-only global market share magically stop at 9% right now? Or will it, as I believe, continue to fall materially from here and land somewhere below half this level, before this decade is over?

If, a few years from now, Tesla ends up with no more than, say, 4% of the global BEV market, what should Tesla be worth? And if it’s not 4%, what are the bull assumptions for Tesla’s terminal market share?

To be even more clear about my question: Tesla’s BEV (and EV) market share keeps falling, year after year. Are you assuming that this market share decline will suddenly stop? Or that it will reverse? What is the case for it reversing?

3) Mark Spiegel’s usual bearish take – see his August letter.

4) Kudos to Musk – another reason humanity owes him a debt of gratitude: How Elon Musk’s Starlink satellite internet keeps Ukraine online

5) In response to this tweet:

A friend writes:

Let’s calculate the total amount (it’s all 100% gross margin) from FSD payments since that October 2016 day when he said that all Teslas built starting at that point were capable of Level 5 autonomy.

That would be driverless (Level 5 means ability to drive anywhere, everywhere, just like a human, with no human in the car).

Let’s say that the FTC would have dealt with Tesla regarding charging for a nonexistent product (FSD) the way they would have normally dealt with every other company operating in the US…

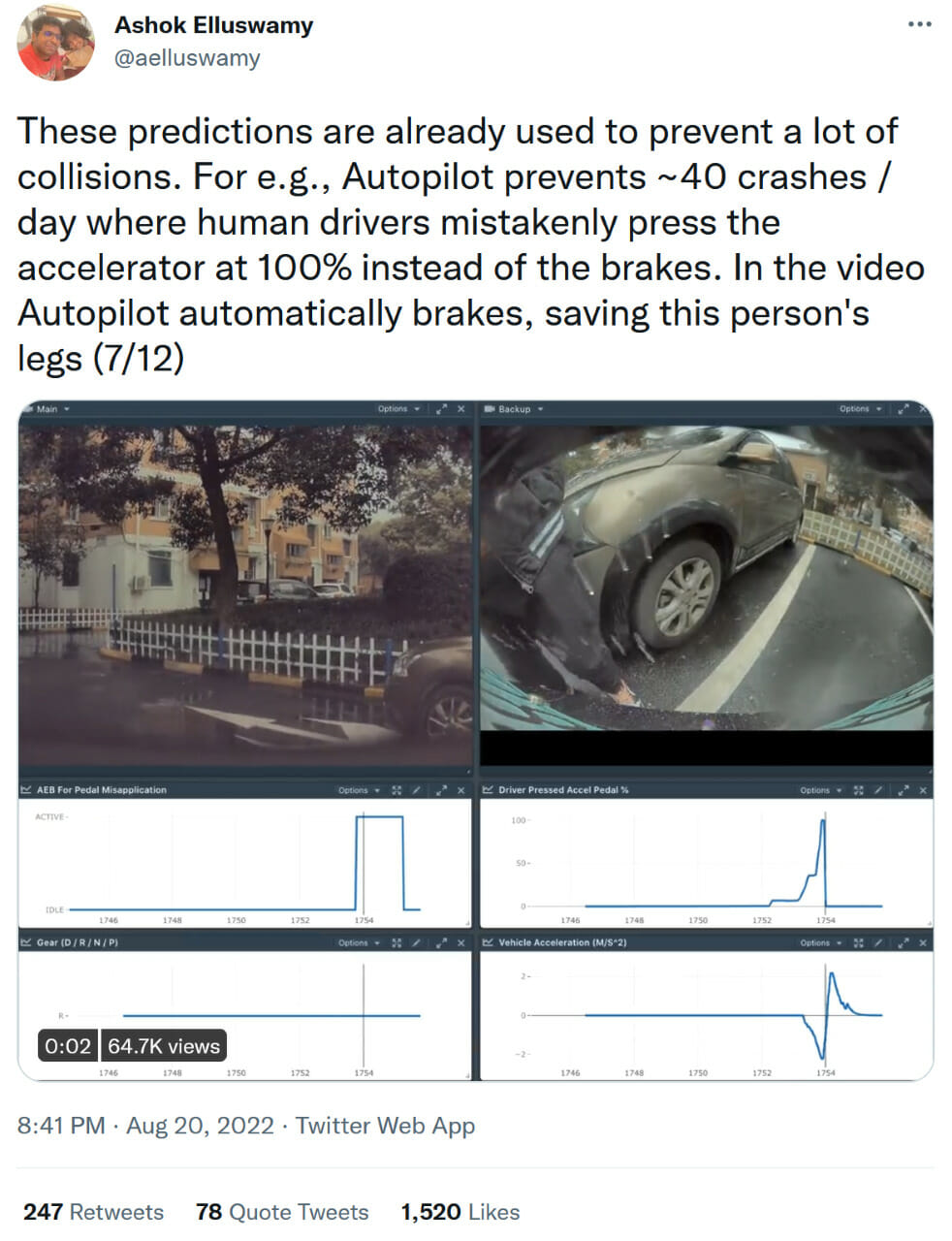

6) A thread on FSD reducing accidents:

7) Tesla demands removal of video of cars hitting child-size mannequins