Given the decade-long performance leadership of large, growth-oriented companies, Sapience like many others in the investment world are expecting better relative returns for value stocks in the near to medium term. We believe the odds, given the equity market scenario today, favor a rebalancing between growth and value exposures.

Q3 2021 hedge fund letters, conferences and more

We are ardent believers in David Swensen’s quote from his epic book, Pioneering Portfolio Management:

”Casual commitments invite casual reversal, exposing portfolio managers to the damaging whipsaw of buying high and selling low. Only with the confidence created by a strong decision-making process can investors sell mania-induced excess and buy despair-driven value.”

Mr. Swensen targeted his comment at two audiences—investment managers who may be tempted to deviate from their disciplines based on current poor relative recent results, and Investment Committee members who may jettison effective long-term asset categories and manager talent based on recent shortfalls.

The markets over the last five years can be characterized by an increasingly fervent zeal to invest in growth stocks with minimal regard for prices paid and downside risk. Many investment firms have begun to actually take pride in deemphasizing valuation—read their letters or listen to their podcasts. As multiples have risen, many such investors are now using non-objective measures of quality to defend their holdings at lofty valuations. We believe many mistakes are being made based on investors’ desire to expand exposure to quality growth—overpaying for growth and quality businesses doesn’t protect against losses and downside risks. The environment is shifting but these investors and their allocators are caught in a cognitive trap of rear-view framing. As Buffett has said, “only when the tide goes out, do you discover who’s been swimming naked”.

How Value Can Regain Leadership

Given our expectation for a style reversal, we must acknowledge that value can regain leadership in three ways:

- Growth multiples can come under attack as the rose-colored glasses come off allowing value to lead by default, which would result in a somewhat muted victory.

- The marketplace begins to recognize the merits of some neglected or out of favor value-oriented companies and sectors, leading to re-rating and increases in prices.

- Both of the above scenarios occur simultaneously. Recall the three years following the Dot Com correction:

Intuitively, the simultaneous scenario seems the most likely. Investors are usually more policy driven, meaning they remain in stocks and choose to make intra-market shifts between styles, sectors, and geographies.

Factors Of Cyclical Shifts In Style Leadership

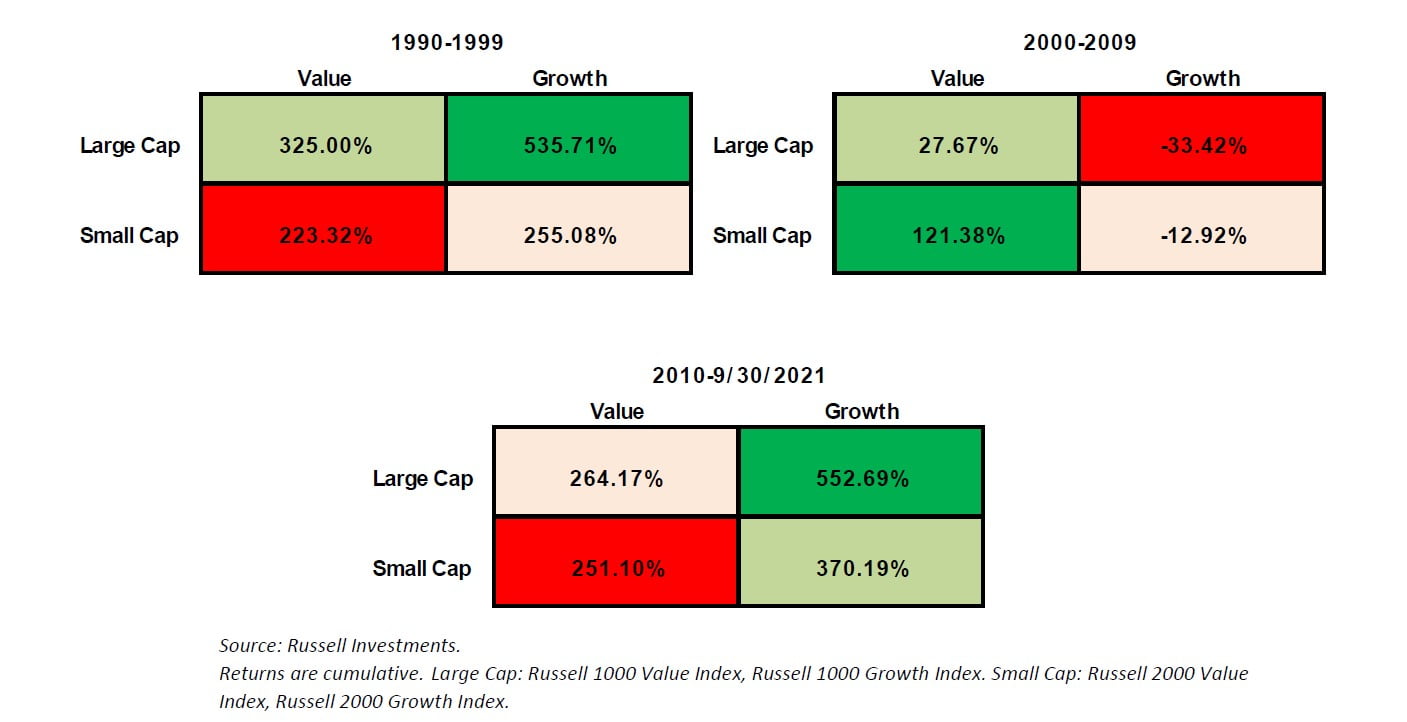

There are macro and valuation drivers that are causal factors of cyclical shifts in style leadership. The technology-media-telecoms (TMT) bubble in the late 1990s was a period where the spread between growth and value reached a record. In March of 2020, the same spread reached close to that all-time record. We are not far from that valuation spread today. The following tables illustrate the dramatically divergent performance for value and growth styles over three (almost equal) time periods during the last 31 years:

No “category” of investor is free from periodic guilt. Those of us in the value camp might be quick to suggest that since the growth managers failed to recognize the massive bubble in 2000, we should not count on them to recognize the current vulnerabilities. If we do that, then we must acknowledge that when facing the greatest credit excess in history, many value managers maintained their substantial exposure to Financials (in keeping with their benchmarks), which were decimated in the GFC. The growth dynamic is currently stretched to an extreme.

Looking out over the near to medium term, we remain constructive but more cautious, as the reduction of fiscal and monetary stimulus should lead to a less favorable backdrop for equities. On the other hand, consumer balance sheets remain sturdy and transitory supply shocks should abate over the next few quarters. The economy should post a strong recovery over the next 12-18 months. A significant turning point in U.S. monetary policy is at hand. However, the consensus view among market participants is still that the FOMC won’t be able to lift rates as postulated and if they do, it would be a policy mistake. In last few weeks, the elevated inflation levels is causing a rethink of this consensus view.

Riding The Popular Stocks Upward

In the last five years, riding the popular stocks upward has been a winning game plan. Simple strategies—passive or momentum based—relying on multiple expansion in the name of growth/quality, have all led to unprecedented gains. The fear of missing out on further gains, and the institutional imperative of keeping up with the benchmarks and peer groups has led to an adjournment of healthy skepticism and a dissipation of discipline. Trends usually go too far, and speculation always leads to rational thinking—the voting machine cedes to the weighing machine. Regime shifts in the markets, after long periods of speculative excesses, are seldom orderly and often violent. In the aftermath of the TMT bubble, retail investors swore off hot IPOs and several growth firms shriveled or were shuttered. In our view, the odds now point towards a shift in the equity markets toward the favoring of skill-based investing or alpha over beta.