Investors seeking floating interest-rate exposure and high yields are increasingly turning to credit risk–transfer securities (CRTs), a fairly new type of mortgage-backed bond. But could US tax-code changes hurt the housing market and, by extension, CRTs? We don’t think so.

[REITs]Government-sponsored housing agencies Fannie Mae and Freddie Mac began issuing CRTs in 2013. Like typical agency bonds, CRTs pool thousands of different mortgages into a single security, and investors receive regular payments based on the performance of the underlying loans. But there’s a key difference: CRTs carry no government guarantee. Investors could absorb losses if a large number of the loans default.

This hasn’t been much of an issue in recent years because the US housing market has been steadily recovering and borrower credit quality is much higher than it was before the 2008 housing crisis. For example, FICO scores, which measure the creditworthiness of individual homeowners, have greatly improved over the last 10 years, and debt-to-income ratios are also at very healthy levels. All of this has kept defaults low.

But is that about to change? The new tax laws that Congress passed in late 2017 include two big changes that many fear could affect the housing market: limits on the amount of mortgage interest and of state and local taxes that homeowners can deduct from their federal tax bill. We don’t think either change will have much impact on CRTs.

Mortgage Interest Deduction: CRTs Dodge a Bullet

Let’s start with mortgage interest deductibility. Previously, borrowers could write off a portion of the interest they pay on mortgages of up to $1 million. The new law lowers the threshold to $750,000.

While this change could have a modest impact on prices at the high end of the housing market, it’s not an issue for CRTs. That’s because loans above $630,000 are ineligible for inclusion in CRTs. In fact, the overwhelming majority of loans in CRT pools are valued at $500,000 or less.

This issue initially rattled investors because an early version of the tax reform bill proposed ending borrowers’ ability to write off interest on mortgages above $500,000. With the revised limit, the CRT market dodged a bullet.

Don’t Sweat the New SALT Rules

A bigger issue is the cap on state and local tax deductibility, also known as the SALT deduction. Under the new law, taxpayers can deduct $10,000 worth of state and local taxes from their federal tax bill. Previously, there was no limit.

The change is likely to make higher-priced homes in states with high property taxes—particularly California, New York and New Jersey—somewhat less affordable and could encourage buyers to spend less when purchasing a house.

Will this hurt home values enough to raise default levels? We doubt it. We anticipate a marginal and temporary price reduction—about 1% to 2%—for higher-priced homes in high-tax states. That won’t be enough, in our view, to have any material impact on default rates.

How Tax Reform Could Help Housing

To sum up, we don’t expect changes to the tax code to derail the US housing market. The US job market remains strong, wages and household net worth have been rising, and the economy is firing on all cylinders.

If tax reform helps to boost growth and the US stock market even further, high-income borrowers may actually benefit from a positive wealth effect that offsets a modest decline in home prices.

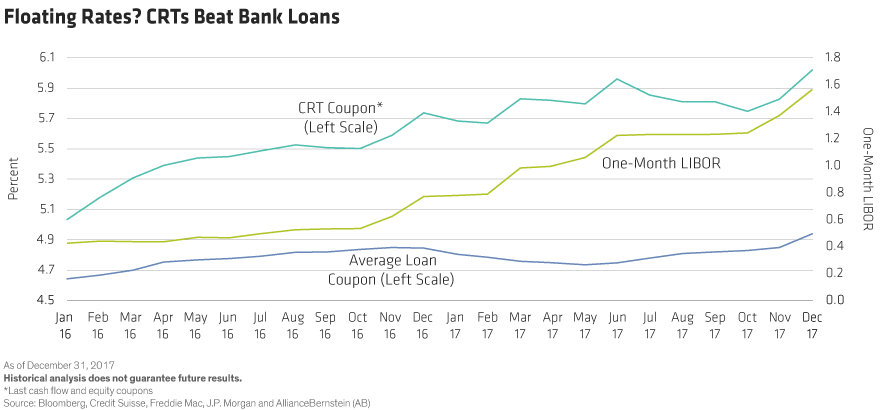

Investors have gravitated to CRTs in recent years for their relatively high yields and their floating interest rates, which are tied to the one-month LIBOR rate that banks charge one another for short-term loans and can provide protection when interest rates rise. As the Display shows, CRT rates have climbed higher and faster than those on floating-rate bank loans, which don’t behave like floating-rate notes because investors can call the loans at will with no prepayment penalty.

We don’t expect new tax laws to change that. CRTs should remain an attractive investment opportunity and a good way to gain exposure to an improving US housing market and economy.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Article by Michael S. Canter, Monika Carlson, Janaki Rao – Alliance Bernstein