The EUR/USD index edged up to 1.2533 on Wednesday, U.S. 4th of July holiday Wednesday in subdued markets ahead of the ECB rate decision to be announced on Thursday. It is widely expected that ECB officials meeting in Frankfurt will cut benchmark interest rate by between 25bps to 50 bps to a record low of below 1% for the first time, and deposit rate to zero, according to Bloomberg News surveys.

|

| Chart Source: Yahoo Finance, July 4, 2012 |

Call for ECB to reduce interest reate has increased with a deteriorating Euro economy in recent months. Uunemployment rate rose to a record high of 11.1% in May. Confidence level also dropped to the lowest in more than two and half years in June, while services and manufacturing contracted for a fifth month. The European Commission now expects the euro economy will shrink 0.3% this year.

Some believe rate cuts may lower money-market rates and encourage banks to lend, instead of hoarding cash, Bloomberg reported that almost 800 billion euros is currently being deposited with the ECB each day.

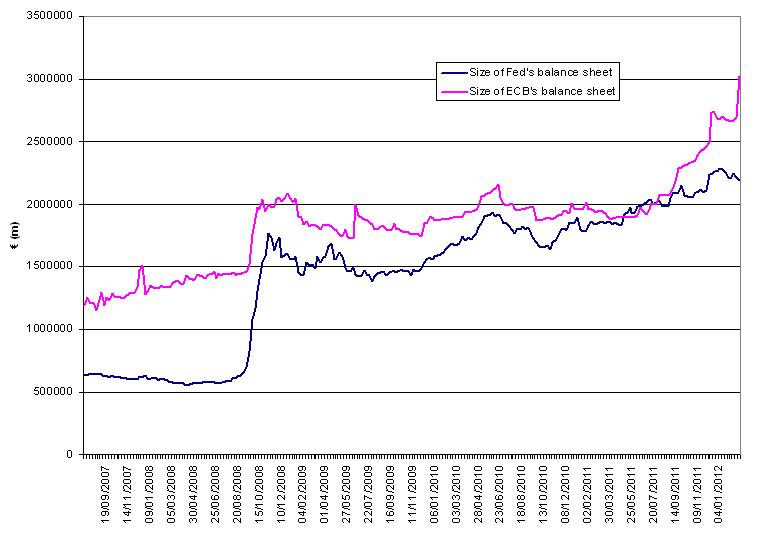

The ECB actually has lent banks over 1 trillion euros ($1.26 trillion) through its LTRO (Longer Term Refinancing Operations) program earlier this year–basically banks get a free ride on ultra cheap cash for three years.

|

| Chart Source: Money Supply-blogs.FT.com, March 6, 2012 |

The problem is that the massive liquidity injection by the ECB does not seem to have trickled down to business and consumers as intended. The latest ECB data shows lending to households and businesses in the euro zone as a whole turned negative in May, while lending also declined further in the Euro member countries that need it the most–Spain, Ireland, Portugal, Greece and Italy.

At the same time, Societe Generale SA estimates that cutting the key rate by 50bps would save banks 5 billion euros a year. So further ECB rate cuts and the resulted lower borrowing costs most likely will only help pad the wallets of European banks, rather than stimulating consumer demand and the broader Euro economy.

More importantly, ECB will not be much room to maneuver with an already below-one-percent benchmark rate, and LTRO 2 is unlikely to accomplish what the first round of LTRO has failed. Furthermore, this crisis seems to have finally spilled over to the German Economy, which could have serious implication as to the country’s future capacity to support more bailouts.

From that perspective, we think Euro is overvalued compared to the dollar. The only thing keeping the single currency afloat is the carry trade. Depending on ECB policy implementation and market reactions, barring any crazy unexpected surprises, Euro should continue to weaken against the Dollar after the ECB rate cut announcement. EUR/USD could hit 1.15 mark in Q3 this year, and parity in the next six to seven months.

By: Econmatters