Whitney Tilson’s email to investors discussing the case to buy Goldman Sachs, Facebook, Berkshire, Brexit, McKinsey, and China.

1) My favorite type of investment is buying great companies when they’re out of favor, suffering from temporary or solvable problems. One example today is Goldman Sachs, which is rightly getting blasted for its total greed and failure of risk control in the 1MDB scandal (here’s the latest story from the front page of today’s WSJ: Goldman Sachs Ignored 1MDB Warning Signs). But, as Bill Miller once said, “If it’s in the headlines, it’s in the stock price.” Now trading at a mere 0.87x book value, the stock is downright cheap. Here’s Doug Kass’s take:

Q3 hedge fund letters, conference, scoops etc

Dec 18, 2018 | 08:53 AM EST DOUG KASS

The Case to Buy Goldman Sachs

"Certain members of the former Malaysian government and 1MDB lied to Goldman Sachs, outside counsel and others about the use of proceeds from these transactions... 1MDB, whose CEO and Board reported directly to the prime minister at the time, also provided written assurances to Goldman Sachs for each transaction that no intermediaries were involved..." -- Michael DuVally, Goldman Sachs spokesman, on Monday

- Goldman Sachs remains "Best of Breed"

- Trading under $170 a share and down from $230 a share a month ago (and a one-year high of $275), Goldman Sachs shares have likely over-discounted the Malaysian problem

- We now face the unusual opportunity of becoming a GS "partner" at a discount to book value

- One of my 2019 Surprises is that GS management acts opportunistically and takes the company private at a premium

- I have placed GS on my Best Ideas List as a long

I have been a longtime bear on Goldman Sachs (GS) ; here was my thesis.

Several weeks ago, with GS trading more than $40 a share higher, I expressed concerns about Goldman's legal exposure to the capital raise of sovereign wealth fund 1MDB and that the media had been slow to highlight the potential liability to the brokerage, which is a holding of Jim "El Capitan" Cramer's Action Alerts PLUS charitable trust.

However, on Monday I moved GS off my Best Ideas List as a short to the Best Ideas List as a long as the market has fully -- and then some -- discounted the brokerage's Malaysian liabilities. Here was my post from Monday.

By means of background, back in 2009, the government of former Malaysian Prime Minister Najib Razak set up 1MDB. About $6.5 billion was raised through Goldman Sachs in three bond offerings. Subsequently, the U.S. Justice Department has estimated that a substantial portion of the capital raised was misappropriated by high-level fund officials and their associates.

GS shares are down by nearly 35% this year and have fallen from more than $250 to less than $170. As recently as mid-November GS shares traded at $235 a share!

Here is my investment rationale:

- For one of the few times since Goldman went public, investors can become a "partner" of Goldman Sachs at a discount to tangible book value. By my calculation, at the time its fourth-quarter results are reported, Goldman's book value will stand at about $187 a share compared to the current share price of $168 a share.

- Assuming a base case of $1.75 billion to $2.0 billion in reimbursement and fines for the Malaysian liability, the market has over-discounted its impact given Goldman's sizable capital base and strong earnings generation. The event likely does not pose an existential risk to the brokerage.

- On Monday Goldman Sachs fired back against the Malaysian government. I expect the litigation to be resolved sooner than later as both parties are incentivized, and there should be limited long-term impact on Goldman. Remember that the Malaysia government has a documented history of being notoriously corrupt.

- While Goldman's leverage has been administered lower by regulators, which has produced lower returns, the brokerage is still Best of Breed. Goldman's employee base is a talented and innovative pool. History has shown the brokerage's strong ability to strike a balance between risk and reward. The current management review of the company's operations (next year is Goldman's 150th birthday) will likely result in a thoughtful going-forward strategy that should improve current returns on invested capital.

- Goldman Sachs is a prime beneficiary of the business retrenchment of previously large, profitable, healthy and well-regarded but now-crippled European financial institutions (e.g., Credit Suisse (CS) and Deutsche Bank (DB) ).

- A reasonably high and sustainable profit growth picture lies ahead, absent the earnings volatility (from prop operations) of the past. Slower yet more stable and steady profit streams should be more valuable as the domestic economy matures.

- Goldman Sachs has beaten consensus EPS expectations over the last four quarters by 15.4%, 24.6%, 28.3% and 16.7%, respectively

- With a market capitalization of $62.5 billion, GS trades at only 1.7x sales, 0.85 of book value and 7.5x projected EPS of $25 a share. Goldman's return on equity (ROE) is about 13.2%. A rule of thumb I sometimes use in financials is that a 10% ROE justifies 1.0x book multiple, so a 13% ROE justifies a 1.3x book multiple, projecting to a value of $247 a share.

- With the share price so low, there is optionality that Goldman may go private. (See my 15 Surprises for 2019.)

Bottom Line

"Be fearful when others are greedy and greedy when others are fearful." - Warren Buffett

As described above, GS share are statistically inexpensive today. Trading at 0.85 tangible book value, the shares provide the unusual opportunity for investors to become a "partner" in Goldman Sachs at a discounted price.

While Goldman Sachs shares are not without risks, the market may have overly punished the brokerage's exposure to the 1MDB financing in 2009.

The Malaysian financing does not appear to pose an existential risk to Goldman Sachs.

In the fullness of time I expect that Goldman could be liable for the reimbursement of the approximate $650 million in fees earned on the Malaysian transaction. In addition, it is quite possible that a large fine may be imposed. The cumulative impact is likely to be under $2 billion, a manageable figure given Goldman's capital base. The key question is whether Goldman Sachs will be subject to criminal charges, which could jeopardize the company's franchise. Based on the information current available, it seems to me that GS partner Tim Leissner and members of the Malaysian government were likely rogue actors and that Goldman's exposure will be contained.

"Price is what you pay. Value is what you get." -- Warren Buffett

The Oracle of Omaha reminds us not to focus on short-term swings in price, but rather on the underlying value of our investments.

I value Goldman Sachs at about $245 a share; barring a going private transaction this is a reasonable two-year price target providing a compounded annual rate of return in excess of 20% a year.

Warren Buffett has taught us the value of being greedy when others are fearful. His stakes in American Express (AXP) (the olive oil controversy), Geico (near bankruptcy) and his numerous preferred investments during the Great Recession have proven to be enormously profitable investments and underscore the value of being an opportunistic long-term investor.

..........

Position: Long GS

2) I also agree with Doug’s view that Facebook is attractive here:

Dec 10, 2018 | 08:11 AM EST DOUG KASS

Trade of the Week: Buy Facebook ($137.42)

Facebook's (FB) fall from grace has been swift and sizeable -- perhaps too much so.

A number of strategic mistakes by senior management have served to reduce the share price from $210 in mid-July 2018 to only $137/share today.

I like FB both on a short- and intermediate-term basis. (I am adding under $138 in premarket trading this morning)

Briefly:

- The share price decline seems to have materially discounted the future of higher costs and regulations.

- Facebook's technical setup has been improving -- its shares have been relatively impervious to the market decline, in general, and to the schmeissing of the FANG space, in particular.

- On a valuation basis (particularly on a PEG analysis) FB's shares have rarely been as inexpensive.

- The company announced a $9 billion buyback late Friday.

On Nov. 19, 2018 I placed Facebook on my Best Ideas List (at exactly today's price).

Position: Long FB

3) The Brooklyn Investor blog with a nice pitch of Berkshire Hathaway: Why BRK? Here’s the conclusion:

I haven't even touched valuation here, but from all of the above, I like BRK a little more now than I have liked it in recent years.

I don't want to time the market and call a peak or anything. I have made it clear that even though we may enter a bear market or have a severe correction at any time, there doesn't seem to me to be a strong case to be made for an extended bear market in the U.S. at the moment (famous last words... I know!)

But the more frothy things seem (well, less so now with the October/November corrections), the more interesting BRK becomes for the above reasons.

AND, it is possible that you won't give up much in terms of performance to buy this 'optionality', with, of course, the greatest investor of all time ready to pounce if we have any big disruption in the market. And we can't forget that BRK has a lot more levers to pull than most conventional funds or even hedge funds; they can buy private businesses too, or do add-on deals to augment the many businesses they already own.

Plus, all that cash on the balance sheet doesn't mean it's as much a drag on BRK's performance as people make it out to be.

As for a post-Buffett world, I think what we need is intense rationality and discipline not to do stupid things. We know BRK is not going to jump into Bitcoin, or buy into bubble stocks (I fear we may find AMZN in the 13-F at an entry price of $3000 some day; that may be a sell signal!), panic and sell out stocks during a crisis or anything like that. And they will not be subject to quarter-to-quarter performance pressure in fear of redemptions. Many of these (and other) advantages are enough to keep me comfortable with BRK for a long time.

Also, even though BRK is not growing the way it used to, and it doesn't look like they are outperforming as much against the index, it looks like a lot of this is due to lower returns in the market in general as the rate of outperformance has been remarkably consistent even after 1998.

By owning BRK, you sort of get paid at least market performance while you wait for the optionality to be exercised!

4) I think it’s now likely that Brexit won’t happen for the simple reason that it was always a dumb idea that would hurt the UK a lot and therefore there is no deal that could pass Parliament. Consequently, there will eventually be a re-vote against it. Brexit Revote? Calls for a Second Referendum Grow Louder. Excerpt:

More than two years after Britons voted to leave the European Union, the U.K.’s politicians still can’t agree on what kind of Brexit they want. Now more lawmakers are calling for a do-over, a second referendum that could potentially reverse the results of the first.

“This is becoming more of a potential outcome,” says Mr. Grieve.

5) Here’s McKinsey’s response to the NY Times article I linked to in my last email.

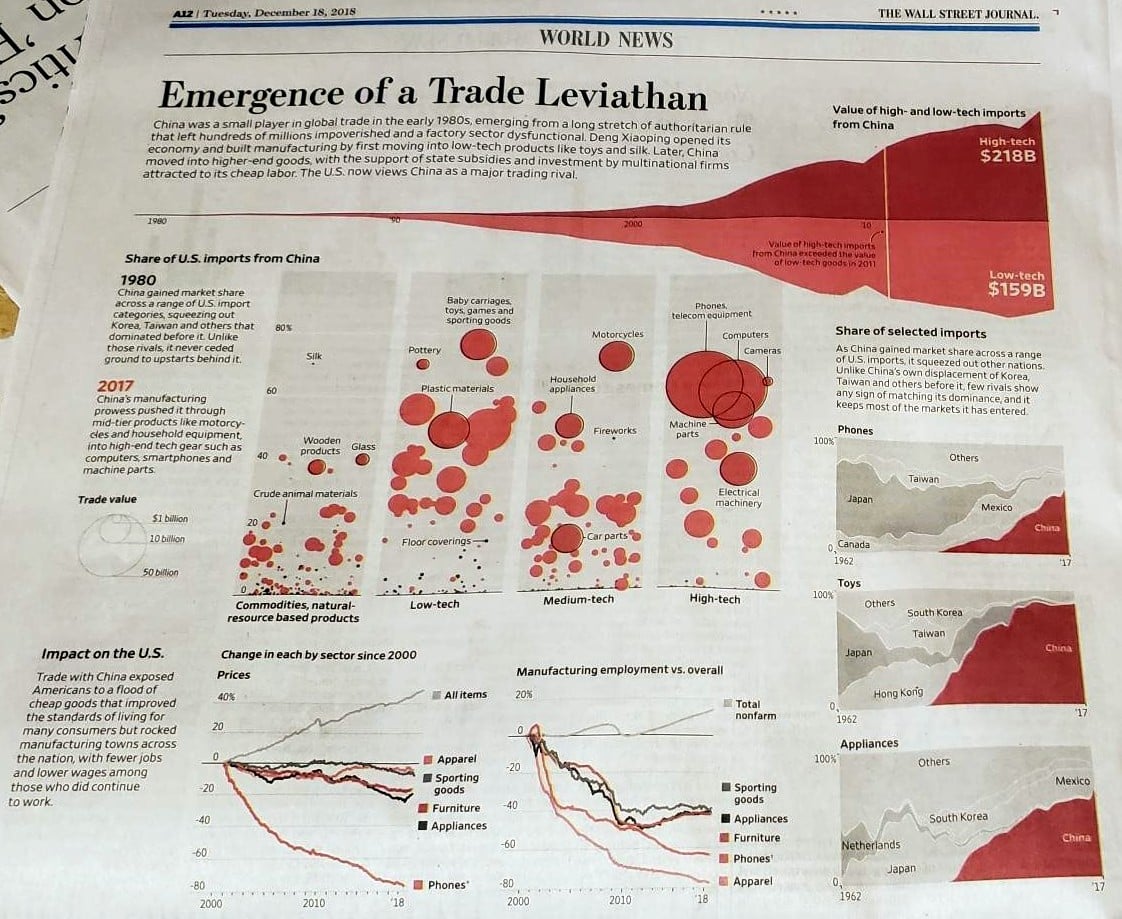

6) The WSJ web site has a fascinating (and sobering) analysis of the parabolic rise of China’s exports to the U.S. since 1980 and the impact it’s had on us: China: Emergence of a Trade Leviathan. It’s really jaw-dropping – well worth five minutes to zip through it. Here are some of the most interesting graphics, as printed in the WSJ today:

{kind=link}