Ben Graham, whom we consider the guru of most value investors advocated simple and effective strategies when it came to investing in the stock market. And perhaps, one of the most overlooked of Ben’s barrage of strategies is the net current asset value approach. I have been an investor for 15 years and have developed a few themes around the net current asset value approach which have worked well for me. I will describe some of these ideas in the paragraphs that follow.

Dividend Skipping

Value theorists claim that an important factor in investing is dividends. I totally agree with that. Where those views depart from mine is that the reduction and/or the skipping of dividends can be a good thing from a behavioral finance perspective. The market views the refusal to give dividend as a bad thing in general. As such, usually when one sees that dividends have been skipped or suspended, the consequence is a battered stock price.But at times like these, an investor really has to ask the question : Has the stock been overly punished?

Q3 hedge fund letters, conference, scoops etc

For a good many cases in my investing life, I opine that many such stocks have been overly punished. But incidentally, that is a good thing for investors who are able to set themselves apart from the crowd. And even better, if you can purchase some of these stocks at a price that is less than two-thirds of the liquidation value, you will find that baskets of such stocks will do very well over time.

In such instances to this theme of investing, you will find that the catalyst to an increasing stock price is the eventual resumption of dividends.

Incidentally, there is also an academic backing to this. It has been found that net nets that do not pay dividends have outperformed net nets that pay dividends. According to Henry Oppenheimer in Ben Graham's Net Current Asset Values : A Performance Update, it was found that securities with a positive earnings, but which do not pay a dividend tend to produce higher mean and risk-adjusted returns than companies that have positive earnings and pay dividends.

And Tobias Carlisle, Sunil Mohanty and Jeffrey Oxman in Ben Graham's Net Nets: Seventy-Five Years Old and Outperforming, have validated that very finding that Henry Oppenheimer made years ago.

"Our results, presented in Exhibit 4, support Oppenheimer’s conclusion. Firms with

positive earnings generated monthly returns of 1.96%. By contrast, firms with negative

earnings generated monthly returns of 3.38%. Firms with positive earnings paying dividends

in the preceding year provided monthly returns of 1.48%, a lower mean return than portfolios

of firms with positive earnings with no dividend paid in the preceding year (2.42%), but did

have a lower systematic risk. "

From a behavioural finance perspective, actors in a stock market are less than rational players in the stock market. These irrational actions play out in the markets as unwarranted overvaluation and undervaluation. And in instances of a dividend cut or skipping, this produces an overly dramatic fall in price which deep value investors can take advantage of to their benefit. My spin on dividend strategies is this. The company must have had an operating history of paying dividends and should have a propensity to pay dividends when normalized conditions of earning power resume.

So some of the net current asset value stocks that I invest in have a cycle that looks somewhat like this. 1. Pays dividends for a number of years 2. Cuts or skips paying dividend 3. pays dividends 4. Cuts or skips paying dividend

So we take advantage of overreactions to the stock price in this way. I have described this in vivid detail in some of the case studies that I have written about in my books.

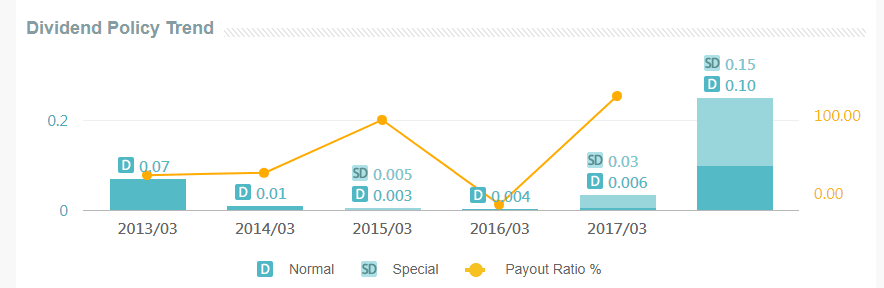

Oriental Watch Case Study

Oriental Watch Is a company that fits the dividend cycle as described above.

Source : http://www.aastocks.com

The bar graph above shows the dividend history or Oriental Watch. If we superimpose the dividend bar graph on the stock chart of Oriental Watch above, what you will see is striking example of how the dividends paid directly correlates with the stock price. The higher the dividends paid, the higher the stock price. The lower the dividends paid, the lower the stock price. The best time to buy in this example is in 2016 as you can see when dividends were cut from the previous years. In other words, fluctuating dividends paid out represent opportunity. Combined with a purchase price of less than two-thirds of the liquidation value, the payoff is in terms of capital appreciation to the upside.

Loss Making Companies

Loss making companies that happen to be net nets also perform extremely well as compared to the general market and to net nets which are profitable. Again, the paradoxes of behavioural finance plays out in the form of beaten, battered stock prices. If the company can prove to be profitable again, an investment at those prices driven by pessimism is the optimist's edge in the market.

An example of an instance like this that I can think of is perhaps Emerson Radio.

Emerson's stock price fell to lows of less than $0.70 per share, at which price, it was trading at around 36% of the net current asset value.

Market Underestimates Mean Reversion

What I have experienced so far as a deep value investor is no different from the experiences of other deep value investors. But perhaps, I am saying and framing it a little differently so that I can accept the essence of it. But by and large, I am of the opinion that the market generally underestimates the power of mean reversion when it comes to beaten and battered stocks. The reversion to mean is a very powerful mental model to adopt in one's framework for deep value success. If a company can survive the current economic conditions, there is a good chance that it will thrive again. Multibaggers in deep value stocks are not uncommon as I have shown in my case studies within the books I have written.

Framed another way, the markets think that permanence is the innate nature of a pessimistic industry or stock. And there are one too many examples to disprove that notion. Consider the subprime financial crisis where many banks were thought to have a bleak future due to increased capital requirements and regulatory tightening. Some failed while many banks today rose from the depths of pessimism to become market darlings once again.

A more recent example of mean reversion is the recent declines in oil prices to less than $30 per barrel. Not long after, oil prices have recovered the $70 per barrel since. While many oil and gas companies which had heavy debt loads went under, those that survived started on a path towards redemption.

Impermanence is a law of nature and in the markets, it is a force to be reckoned with. Mean reversion is thus a natural extension of the law of impermanence. When it comes to net nets, investors as a whole also shun such companies due to uncertainty within the industry or the company. But by and large, investors often underestimate the returns that accompanies uncertainty with regard to net net investing.

Capital Structure Issues

Another net current asset value theme which I gave appropriate case studies of in my book is the theme of deleveraging. When a company embarks on a deliberate and purposeful attempt to reduce debt, the effect can be measured in several ways. The company eventually pays less in interest expenses which can increase after tax profit and the company's equity on the balance sheet encounters a natural expansion.

For companies trading at a low price to the earnings, book value or the net current assets, it would be an understatement to state that baskets of such stocks, implemented on a 'law of large numbers' approach, tend to do quite well.

So with such companies, what you would really want to do is to look at managements which are capital structure conscious. You don't want to invest in an equity stub where the ratio of debt to equity is 5 : 1. Cases like that present too much risk in my opinion. Instead, be open to companies where the ratio of debt to equity is less than 2 to 3 : 1 and where the company has some valuable and possibly hidden assets in the balance sheet, with a decent earning power. Cases like the latter present themselves occasionally and the investor could be well prepared to pounce on such opportunities.

A recent case,but not the best example, comes to mind. We have all heard of Valeant Pharmaceuticals and the saga it was embroiled in. To cut the long story short, Valeant's management was intent on acquiring companies and with the use of non-GAAP metrics such as adjusted earnings and adjusted revenues to inflate the true performance of the company. We know what happened thereafter. But things have changed since and the new managers have tried to make things right. Joseph Papa, the current CEO of Valeant, which has since changed its name to Bausch Health Companies to distance itself from its past, has embarked on an attempt to pare down the debt within the company's capital structure. The company's debt per share fell from $90 per share in 2015 to $86 and $73 in 2016 and 2017 respectively. And the markets have rewarded their efforts with the company's price rising from around $10 per share to around $25 per share over the last 12 months.

In all honesty, I have just skimmed the surface of things. There is a lot more I could talk about but I will perhaps leave that to another article. I would like to take this opportunity to thank Jacob Wolinsky for putting up this article on ValueWalk. If you are interested in my thoughts on deep value investing, I have written several books which I will leave the link to below.

As always, may all be blessed with prosperity, health and happiness!

Books Written By Kingsley

The $20 Million Investor Blueprint: How Amateur Investors Can Build Their Portfolio To $20 Million

The $20 Million Investor Blueprint: Net Current Asset Value Stocks In The USA

The $20 Million Investor Blueprint: Deep Value Net Current Asset Value Stocks In Japan

The Billionaire Investor Blueprint: Low Price To Book Stocks For Tremendous Wealth

Dear friends, I hope this article finds you well.

I have written a number of books about the net current asset value theme. The value of these books, which I set out to achieve is to create a sort of an imprint within me and also to help the general investor rewire their minds. There is such a tremendous amount of information on investing in the stock market but nothing stirs me up quite like Ben Graham’s ideas. I have taken on these ideas and have made some money in the stock market. I think these ideas will help you too, if you are willing to see the logic of it and not be a blind herd follower.

These books are available on Amazon Kindle and if you wish to know more about net current asset value investing, head on over to my blog at www.theholyfinancier.com.

All the best in your investing life and may you be prosperous, healthy and happy!

{kind=link}