In a previous article I discussed that I am on track to have my dividend income cover my expenses sometime around 2018. I received a few questions on how I am able to achieve that. I have mentioned before, that I do not like to talk about myself, because I personally find it a little tacky.

I think I have taken for granted certain topics such as saving, and the power of compounding. I always assumed that it was common sense that people who came to this site would not be interested in learning how I drive a 15 year old car, how I graduated college without any debt but $2,000 in the bank and no debt, and that my frugality has helped me save enough to build my portfolio since 2007.

I also naively assumed that everyone who already saves money sees dividend growth investing as a tool to achieve their financial goals and objectives, be that traditional retirement, early retirement, financial independence or something else. Based on many interactions I have had over the years, I think that I was wrong in my assumptions on what constitutes common sense and what doesn’t. Given the rapid growth of the site readership since its inception in 2008, it is reasonable to expect that not everyone will be on the same page when it comes to various topics.

The first thing about investing is that in order to invest, you need to have money. In order to obtain that money, you need to utilize your most important asset to either find a job, or start a business. You then have to make sure that your expenses are less than what you earn. This surplus cash is then invested every month in dividend growth stocks. The formula to achieve wealth is really simple:

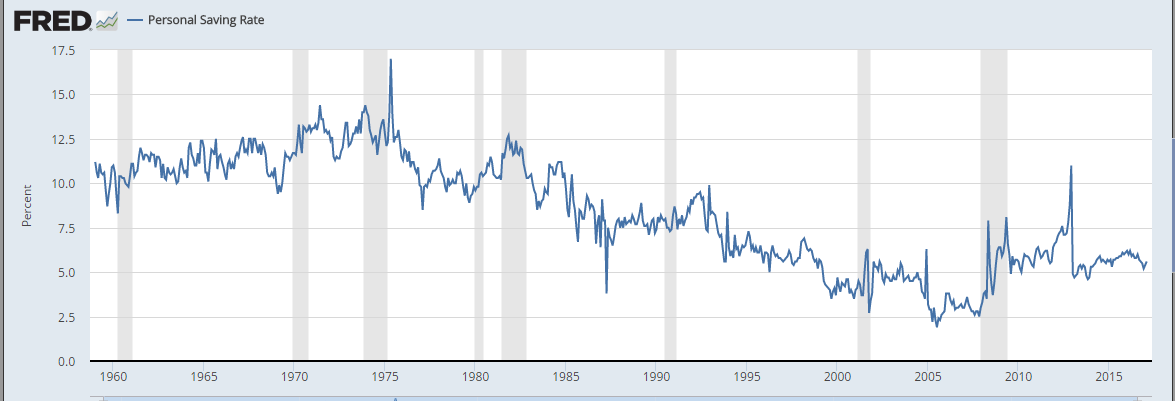

This is very simple, yet the low savings rate for the average household in the United States refutes my claim about what common sense on savings really is.

Source: Federal Reserve Bank of St. Louis Research

We can spin the above formula any way we want, but the basic truth still stands. In my situation, it has helped me that I invested my surplus in income generating assets. Therefore, the extra dividend income I received further increased my earnings power. In addition, going back to school increased my earnings power even further. The nice thing about earnings power is that having the flexibility to go to different states for jobs has definitely helped so far.

However, for someone who already saves money, their job is not done. This is because the more you save, the less time you need to spend accumulating your nest egg. In order to achieve that goal you either have to earn more, or spend less. In my case, I have managed to earn more through more salary income, dividend income and miscellaneous projects ( such as this site). I also managed to keep expenses low on things like transportation, taxes, housing. However, I do spend on things I value like education and learning, travel, quality entertainment ( I am a major supporter of Diageo (DEO) etc).

I do continuously try to streamline operations however, and cut expenses where I need to. My way of thinking is criticized sometimes, but it is my way of frugal thinking that has helped me get to where I am. For example, I have been criticized for using Interactive Brokers and bragging that I only pay 35 cents/trade, when I could have paid $5-$10/trade. Over a month, this sounds like a measly $10. I have learned one should never despise the days of small beginnings, and should allocate every single dollar as rationally as possible.

I do not believe I should be paying $10 more per month than I have to for a commodity service that stock trading is these days. To me the above objection sounds like slippery slope – if I view $10 in monthly savings as measly, then the next stop is upgrading my deal from getting only internet to getting cable and internet from my local cable company. After all, what is the difference between $50/month and $100/month, right? Since I hate spending more than I have to, I analyze my major ticket items. I believe that frugality is a frame of mind, and extends to every activity you spend money on. This is why you see business owners who are worth millions, who will drive around looking for a parking meter with money for it. This is why you would also see successful executives who are detail oriented about every single aspect of their business – and may even collect some trash from their business parking lot. When you have frugality as a frame of mind, this influences everything you do. The frugality helps you get the capital, that will compound and pay dividends to you for decades to come. But it never leaves you.

I realize not everyone is frugal. For people who are not naturally frugal, it is helpful to focus on the biggest expenses. For example, the largest expenses for households include housing, transportation, food and taxes. I will discuss below how I tackled most of those.

My largest expense over the past decade has been taxes. Using tax-deferred accounts however, I have managed to cut this expenditure to the bone. Unfortunately, wage income is heavily taxed. This is where it has helped me to max out every single tax-deferred account I am eligible for. This reduced my tax liabilities today, and ensures tax-deferred growth of investments. With some planning, it is possible to get a tax break upfront, and not pay any taxes when I would spend the money.

The other major item is transportation. Lifestyle design can help in tackling this expense. I have tried to design my lifestyle around reducing this expense. It has helped me that I have always lived close to work, which makes driving an old car easier. It has also helped to live in an area, which is close to grocery, entertainment, etc.

The third major expense is food. Naturally, cooking for your family and brown bagging lunch to work saves a lot of funds. In my opinion, eating out is expensive, and generally unhealthy. I can easily make a sandwich for a lower price than what I can buy at a restaurant. It is cheaper and more entertaining to host a party for your friends at your home, rather than go out to an overcrowded and noisy place.

The one area where I have failed so far is capitalizing rent expenses, aka buying an affordable house. Unfortunately, I have two left hands, so home ownership looks like money and time pit to me. Not having a house has worked well actually, since I have frequently moved around every few years or so, in order to get better paying jobs. Given the fact that house prices where I live are so low relative to rent, I have most probably thrown out tens of thousands of dollars in rent that could have been home equity sitting on my net worth statement. I may be able to rectify this deficiency at some point in the future. If you plan to stay at a location for less than a decade, it is generally advisable to rent.

The one expense I have never had is long-term debt. I graduated college not only debt-free, but with $2,000 in the bank. I received support for the first year of college only. I achieved the rest by picking a school which was a great value for my money. I also picked a major that offered real marketable skills. During college, I worked throughout the year to pay for school. I minimized costs by living cheaply off campus, studying all the time, earning scholarships, getting involved etc. Unfortunately, without effort, there is no success in anything. I try to be practical, in order to avoid bad scenarios in life. I believe that not paying interest, but earning interest and dividends have been instrumental tools in my quest towards financial independence.

Of course, frugality only goes so far. You need to have a decent amount of income, in order to pay for expenses and get the capital to invest productively. The main thing that helped me is the fact that I received decent education in a field that is marketable, and which always seems to be in demand, even for someone like myself. Your biggest asset is your earnings potential, so you need to make sure you treat it with respect. Going back to school in my case was helpful for earning more money. When your income increases, but your spending remains the same, your investable savings increase rapidly. The other thing that has helped me in my quest is any side income I receive beyond the job. The first line that was scalable were dividends. But to get more capital to put to work, I opened bank and broker accounts for their bonuses. I also opened up this site, and earned some cash in the process.

Having a decent income, and having a high savings rate are not enough either. You need to learn how to invest that money intelligently for the long term. There are a variety of strategies involving dividend growth stocks, real estate or index funds. The strategy of your choice should be something that makes sense for you, something you are comfortable with, and something that you will stick to through thick or thin.

Too often new investors come out and are told to do this, and only this method, but they don’t understand why they should do it. When things get difficult, these new investors abandon the strategy that they never really understood in the first place, and lose money. I see it in indexing today, though new dividend investors are not immune to behavior pitfalls either.

I developed my method of selecting dividend growth stocks, in order to accomplish my goal of generating enough stable passive income by a certain timeframe. The truth is that others might have different goals and objectives. The important thing is to understand your goals, the time you have to achieve those goals, and then find the method that work best for you, given your own shortcomings.