The debt ceiling is dominating headlines as we narrow in on the potential X-date—at which time the U.S. Treasury will have insufficient cash to pay interest on the debt along with its other obligations. That date may arrive in early June, or potentially even sooner. While the likelihood of a U.S. government default is very low, the chance that this will be an issue until the very last minute is high.

What Is The Debt Ceiling?

There are two ways the US government pays its existing bills: tax revenue and proceeds from debt. Its bills include Social Security, Medicare, Medicaid, military expenditures, and interest payments on existing debt. If the government runs short of funds and chooses not to prioritize interest payments, then the country could go into default.

The US hit the debt ceiling on January 19. Since then, the Treasury department has relied upon “extraordinary measures” to meet the government’s debt obligations. Treasury Secretary Janet Yellen estimates the viability of using “extraordinary measures” will expire about June 1.

Earlier this year, observers expected the debt ceiling topic to become prominent later in the year—probably in the third quarter. But a bigger than expected federal deficit has made it a more immediate problem.

The deficit is larger than anticipated as government receipts (tax revenue) have declined, and outlays (bills) have increased over the past twelve months. Increased spending has mainly been driven by higher interest rates.

Only Congress can raise the debt ceiling, which means the House and Senate must agree on a bill—and the President must sign the bill into law—in order to do so. Otherwise, the Treasury department cannot take on more debt and the government will run out of cash.

Potential Implications

Typically, US treasury bonds are viewed as a safe haven asset for global investors and a virtually risk-free investment (in terms of full and timely payment). A failure to pay bondholders their interest due would have large implications.

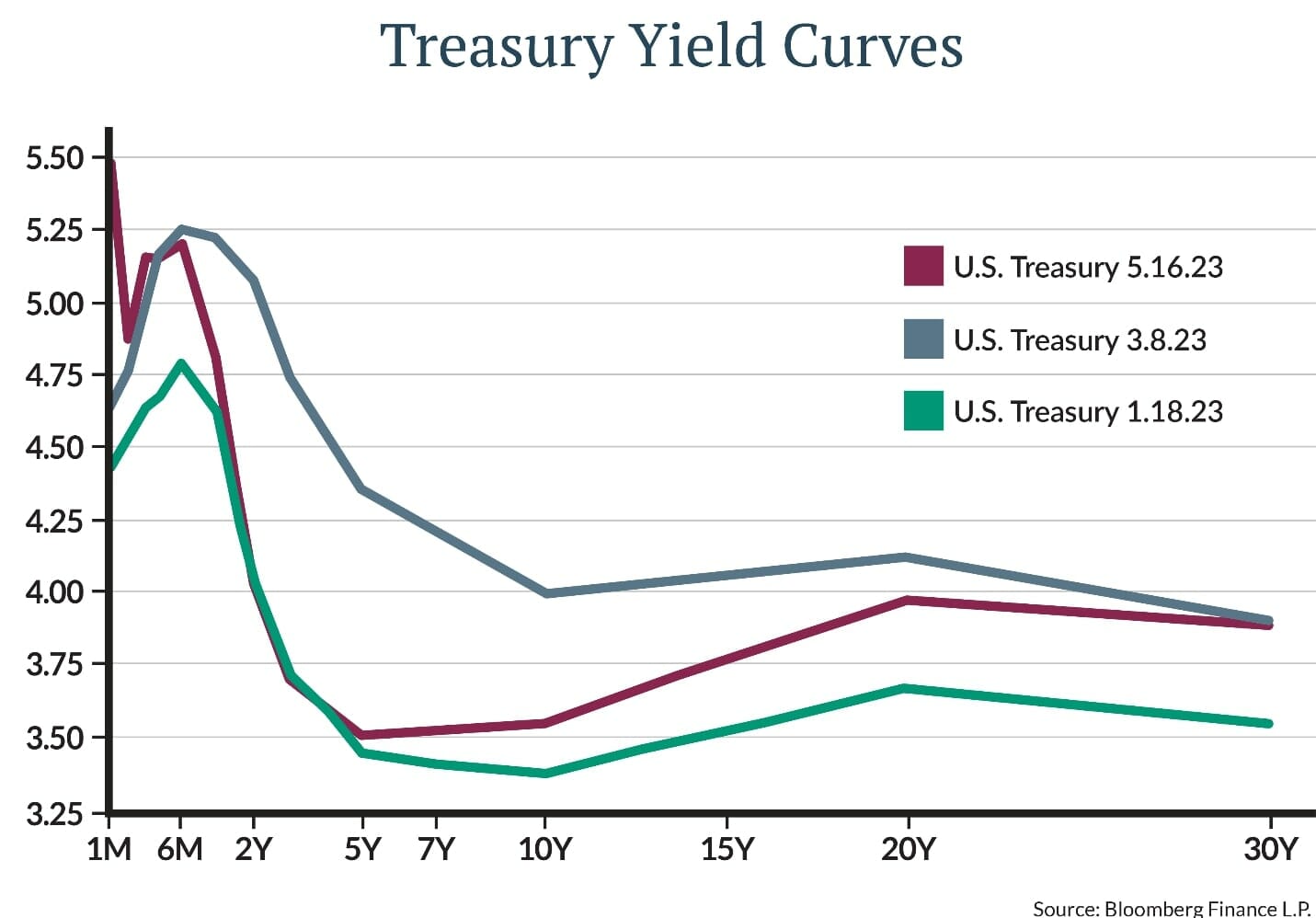

Treasury debt would potentially be downgraded from its current Aaa rating (AA+ by S&P) which would lead to higher interest rates or borrowing costs. This would cause stocks, bond prices, and the US dollar to decline. The current Treasury yield curve demonstrates this uncertainty as 1-month Treasury bills have spiked to nearly 5.5% over the past few months.

Timing of the current debt ceiling impasse is especially concerning as the US economy already faces a potential recession after five percentage points worth of Fed rate hikes. In 2011, the US got very close to the debt limit and US treasuries were downgraded from AAA to AA+ by S&P. At that time, the VIX, or volatility index, spiked from 18 to 50 (with values over 20 indicating increased volatility). The S&P 500 was down 17 percent over one month.

There is a chance that the debt ceiling constraint may be harder to resolve now than in 2011. The Republicans’ narrow margin in the House will make it harder to separate raising the debt ceiling from budget spending. If the government focuses on just paying the existing debt and forgoing all the other programs, the economy could still suffer a mild recession.

If and when a deal comes to fruition, it is likely to include permitting reform, recissions of COVID spending, and a short-term agreement on spending caps. Volatility may increase temporarily even if a deal is struck before the X-date, due to pent-up Treasury issuance and a drain on liquidity.

Portfolio Positioning

According to Bloomberg, money managers seem relatively unfazed. A Bank of America survey released this week indicates that 71 percent say they expect a resolution before the deadline.

Western Asset, one of our fixed-income managers, states that they have been increasing both quality and collateral in their portfolios. They believe that should a default occur, longer-dated Treasuries would likely rally while the shorter end of the treasury yield curve would likely take the brunt of the rate increases.

Baird, another of our fixed-income managers, believes the debt ceiling will be raised and default taken off the table. They reference a clever comparison: the process of resolving the debt ceiling has been likened to passing a kidney stone—it will pass, it’s just a question of how long it will take and how painful it will be.

They expect more clarity over the next week but expect volatility ahead. Their portfolio positioning has not changed as they are already well diversified with ample layers of liquidity to weather the storm.

Here at Johnson Financial Group, we feel we are already appropriately positioned within portfolios and are ready to weather potential volatile times ahead. As chief investment officer Brian Andrew emphasized in his commentary last week, we’ve continued to be more defensively positioned in both equity and fixed income portfolios. History shows whatever impact that debt ceiling chaos brought to the markets back in 2011 got erased eventually. After 2011, the S&P 500 fully recovered six months later.

So, while the debt ceiling debate may lead to temporary pain, we trust it will pass and remain focused on long-term goals.