Stanley Black & Decker (SWK) has put together an amazing track record of dividends over time. The company says it has paid dividends for an almost unbelievable 141 consecutive years and the last 50 of those years have each seen increases in the payout.

Q1 hedge fund letters, conference, scoops etc

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Track records like this are almost unheard of and as such, Stanley Black & Decker is truly in a class of its own. It is now part of an ultra-exclusive club of Dividend Kings, a group of just 25 stocks that have increased their payouts for at least 50 consecutive years. You can see the full list of all 25 Dividend Kings here.

Click here to download my Dividend Kings Excel Spreadsheet now. Keep reading this article to learn more.

Dividend Kings are the best of the best when it comes to rewarding shareholders with cash, and this article will discuss Stanley Black & Decker’s qualities that have put it in such exclusive company.

Business Overview

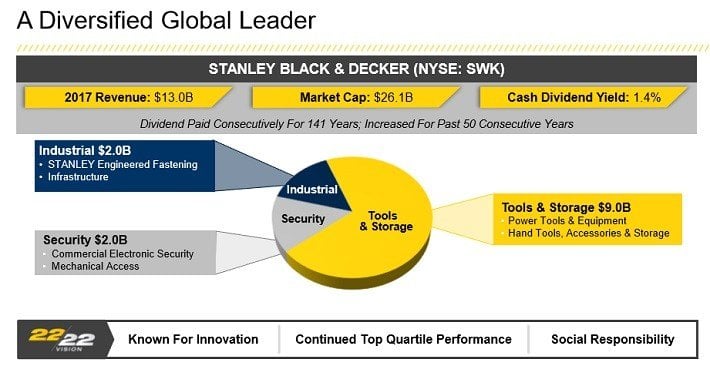

Stanley Black & Decker’s market cap stands right at $24B and the company is expected to do close to $14B of revenue this year. It operates in three separate business lines called Tools & Storage, Industrial, and Security.

Source: Investor presentation, page 4

The largest segment is the Tools & Storage business while the Industrial and Security businesses make up about 30% of total company sales combined. The company makes all kinds of things that a homeowner, contractor or professional laborer could need to make their lives a little easier, including its famous line of handheld power tools.

In fact, Stanley Black & Decker is #1 in market share in the Tools & Storage business as it dominates that particular niche in the construction, DIY, auto repair and industrial segments with its broad and deep assortment of brands that fit any budget and need. It has formed itself over the past 175 years since its founding in New Britain, CT into a global powerhouse of brands.

That stable of brands grew about a year ago when Stanley Black & Decker added Newell Brands as well as the Craftsman brand for a combined total of just under $3B. Stanley Black & Decker has always been acquisitive, pouncing when the opportunity strikes and growth-by-acquisition is a stated corporate goal.

It takes a measured approach to acquisitions and when great companies come up for sale – like Newell or Craftsman – it will get the deal done. Stanley Black & Decker has used this strategy to spend about $9B on acquisitions since 2002 and the results have been terrific to say the least.

Growth Prospects

That doesn’t mean that Stanley Black & Decker is done growing by any means and in fact, it has a number of strategic initiatives to ensure that it continues to grow in the years to come. Stanley Black & Decker’s acquisition strategy is key and will continue to be a focus for the long term as management has set expectations that roughly 50% of free cash flow is going to be used for acquisitions.

Free cash flow has been around $1 billion annually for the past four years, which leaves Stanley Black & Decker with plenty of dry powder to make targeted acquisitions where they make sense. The Newell buy was much larger than what Stanley Black & Decker normally does but when an opportunity arises, Stanley Black & Decker takes advantage.

Source: Investor presentation, page 12

Stanley Black & Decker’s five-year plan is to see revenue grow from $13 billion to $22 billion, representing a CAGR of about 12%. That is a steep hill to climb but Stanley Black & Decker’s strategic plan is to buy over half of that growth while organic sales increases make up the rest.

In addition, Stanley Black & Decker is looking to diversify away from its current revenue mix that is heavy in its core Tools & Storage products. That is Stanley Black & Decker’s bread and butter so there’s nothing wrong with this mix, but getting away from being so reliant upon it is prudent nonetheless.

The Industrial and Security businesses also offer more white space for growth than Tools & Storage, where Stanley Black & Decker is already dominant. This paints a picture of what investors can expect from Stanley Black & Decker going forward; lots of smaller acquisitions that will focus heavily on growing the Industrial and Security businesses and getting away from having quite so much emphasis on Tools & Storage.

In addition to that, Stanley Black & Decker is targeting emerging markets in order to strengthen its global footprint.

Source: Investor presentation, page 49

Stanley Black & Decker believes emerging markets are the key to organic growth as they offer up growing middle classes that are gradually seeing more and more disposable income, as well as large scale construction and rebuilding projects.

Of course, emerging markets are heavy into opening price point tools that generally carry lower margins but over time, the growing middle class not only creates more potential customers but also more that can afford a mid-price point or even high price point product.

Stanley Black & Decker has a truly global footprint as the US is only about 54% of total revenues. Emerging markets are only 14% of total revenue and in the Security business in particular, represent just 4% of that segment’s revenue. The opportunities for Stanley Black & Decker to grow its emerging markets business are vast and while this is a long term story, it is certainly one to focus on.

Competitive Advantages & Recession Performance

Stanley Black & Decker certainly has advantages over its competitors in that it is in a number one or two position in all of its markets and has a truly global reach. These things afford Stanley Black & Decker not only scale advantages in terms of distribution but in pricing as well, both of which lead to higher margins.

In addition, the dominant position Stanley Black & Decker enjoys in its core products affords it the ability to purchase competitors like it did with Craftsman and the Newell business, eliminating potential threats before they become a problem.

That said, Stanley Black & Decker does rely upon discretionary spending and in particular, things like residential construction spending and automotive production. Over half of Stanley Black & Decker’s Industrial revenue comes from automotive production alone, an area that is highly sensitive to recessions.

In addition, residential and non-residential construction make up a whopping 60% of Stanley Black & Decker’s total revenue across all categories as the Tools & Storage business derives most of its revenue from those categories. Again, these are categories that are highly sensitive to recessions.

That said, Stanley Black & Decker is not immune from recessions. Earnings declined significantly in 2008 and 2009. As an industrial manufacturer, Stanley Black & Decker is reliant on a strong economy and a financially-healthy consumer.

Stanley Black & Decker’s earnings-per-share during the Great Recession are below:

- 2007 earnings-per-share of $4.00

- 2008 earnings-per-share of $3.41 (15% decline)

- 2009 earnings-per-share of $2.72 (20% decline)

- 2010 earnings-per-share of $3.96 (46% increase)

There’s no indication a recession is imminent but it will occur at some point and these distribution points are highly likely to experience potentially significant revenue and earnings declines when it does. History suggests such a time would be a terrific buying opportunity for Stanley Black & Decker, but it would be painful in the interim.

Valuation & Expected Returns

Stanley Black & Decker expects to generate earnings-per-share of $8.25 for 2018. Based on this, the stock has a price-to-earnings ratio of 18.7. In the past 10 years, the stock has held an average price-to-earnings ratio of 15.6. As a result, the stock seems slightly overvalued.

Source: Value Line

Stanley Black & Decker is a high-quality business and a Dividend King, so it could be argued the stock deserves a premium valuation. As a result, it seems the stock isn’t overpriced, but it also means it isn’t particularly cheap, either.

This implies that the multiple is likely to remain right around where it is today unless something changes drastically positively or negatively. That seems unlikely given the steady results we’ve seen from the company over its long history.

If we assume that the multiple won’t change, Stanley Black & Decker’s expected EPS growth in the low teens should be plenty good enough to provide shareholders with strong total returns. After all, if the multiple doesn’t change but EPS rises by 12%, for instance, the stock should rise by 12%, all else equal. That’s been the company’s playbook for a very long time and it has worked so there is no reason to think it won’t continue to work.

In addition, Stanley Black & Decker’s stated target payout ratio is 30% to 35% of earnings, which equates to about the same amount in free cash flow given its virtually one-for-one relationship between earnings and free cash flow conversion. That implies the dividend should rise at roughly the same rate as EPS in the coming years and apart from that, it means that the dividend is ultra-safe.

With the company targeting such a low payout ratio – allowing for R&D, acquisitions and buybacks – it means there’s no reasonable scenario where the payout would be at risk. It would take a complete disaster and an enormous decline in earnings such that if such a scenario were to occur, you’d want to be out of the stock anyway for other reasons.

Putting all of this together, with the current yield in the 1.5% area and expected EPS growth of 12%+ in the coming years, Stanley Black & Decker could fairly easily provide shareholders with total returns in the mid-teens. This company’s track record of excellent management provides the roadmap; all we have to do as investors is trust that it will continue to work.

Final Thoughts

Stanley Black & Decker is certainly not a high-yield, income-focused stock and it never will be. The company’s strategy of growth-by-acquisition conflicts with paying out a high percentage of free cash flow in dividends. However, it is that strategy that has allowed Stanley Black & Decker to produce astronomical total returns in the past two decades against the broader market so it is clear that changing its tilt towards a higher yield would be imprudent. The company continues to strengthen its hold on its core markets and as those advantages continue to grow, it will only become a more attractive stock to own.

The stock doesn’t look cheap but it doesn’t look expensive, either, and given the clear and achievable road map management has laid out, shares look attractive here for a long term buy. Stanley Black & Decker’s dividend also has one of the longest track records in the US and will almost undoubtedly continue to rise in the years to come.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

{kind=link}