I recently wrote an article for Sure Dividend entitled “Consider Equity REITs for Your Next Investment“. In that article, I listed nine equity REITs (eREITs) for dividend investors to consider in light of the drubbing that eREIT valuations have recently taken due to fear of rising interest rates and to capitalize on the pass-through provision for REIT income included in the new tax legislation. Both of these topics are covered in some detail in the previous article. This article provides a more complete investment thesis for STAG Industrial (STAG), one of the nine eREITs highlighted in the previous article.

STAG Industrial, Inc.

STAG Industrial invests in single tenant warehouses, distribution centers, and light industrial buildings in secondary markets around the country. STAG Industrial has an enterprise value of roughly $4.1B owning 356 buildings in 37 states in the US. STAG Industrial was established as a public company in July 2010 and is headquartered in Boston, MA.

Readers interested in the difference between primary and secondary industrial building markets should understand that primary markets (cities) are those with total industrial real estate space greater than 200M square feet while secondary markets typically include total industrial real estate space of 25M – 200M square feet. In short, primary markets are larger while secondary markets are smaller.

STAG Industrial sees advantages to investing in the secondary market with few disadvantages. The secondary market is significantly smaller but tends to offer lower acquisition costs.

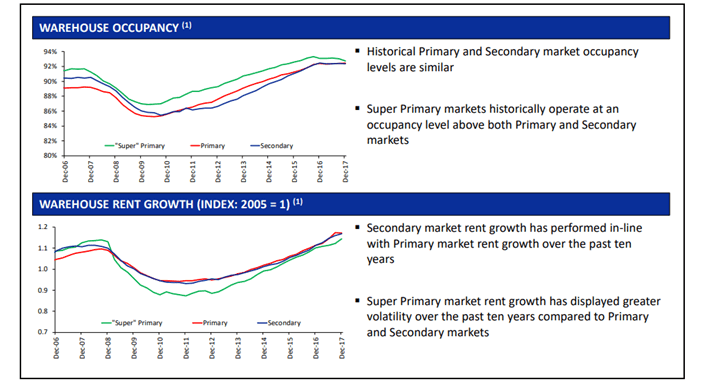

The secondary market occupancy and rent growth track closely together with the primary markets. The charts below show that relationship.

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Source: STAG Website

With the cost advantages that the secondary market buildings have with essentially the same occupancy and rent growth as in primary markets, STAG management believes they are in a sweet spot with respect to industrial real estate.

Focusing on the secondary market also helps STAG achieve tenant diversification. The charts below show the diversification that STAG has achieved to date.

Source: STAG Website

In addition to tenant and industry diversification, STAG has been able to achieve geographical diversification across 37 states.

Source: STAG Website

STAG’s level of diversification in industries, tenants, and geography help STAG achieve a high degree of stability in total cash flow; clearly an important trait for a income investment. STAG has also been busy growing their asset base. The chart below provides a summary of growth in square feet under lease.

Source: STAG Website

This chart is significant as it shows STAG growing at an exponential rate from 1,944,000 square feet in 2011 to 33,488,000 square feet by the end of 2017. The compound annual growth rate of square footage leased is just a bit over 60%. That is tremendous growth in leased space in a relatively short time.

STAG Industrial, Inc. Recent Financial Performance

Not only has STAG been successful at growing its leased space, it has also been growing its adjusted funds from operations (AFFO). STAG Industrial’s past financial performance has been steady and predictable. A short note here for investors not fully versed in eREIT financial metrics. Because eREITs have very high depreciation write-offs which are tax accounting entries that do not affect cash flow, the usual metrics of earnings per share (EPS) and price earnings ratios (P/E) are not meaningful for eREIT financial reporting. The accepted metric for eREIT financial reporting is FFO and AFFO which are cash flow metrics. The following charts show STAG’s near term financial performance in those accepted metrics.

Source: Author

The charts above show STAG’s AFFO/share and cash dividend distribution growth over the last 5 years and estimated for 2018 and 2019. It is obvious from the second chart that STAG has been less generous with dividend growth than its AFFO growth would allow. This is because STAG has been prudently bringing its dividend payout ratio down from 90% to an estimated 78% for 2018. The dividend payout ratio is also presented for eREITs in terms of AFFO. The chart below shows STAG’s payout ratio over the last 5 years and estimated for the next two.

Source: Author

For an eREIT, anything less than 90% payout ratio is acceptable and less than 80% is good. STAG’s estimated payout ratio of 78% is conservative and would allow STAG to begin growing their dividend distribution at a clip closer to their growth in AFFO.

STAG Investment Thesis

With the general market currently experiencing a mild correction and eREIT valuations suffering further from fear of rising interest rates, why would I be considering an investment in STAG at this time?

For the last three months, STAG has been pummeled by the market’s fear of rising interest rates and has fallen more than 17%. While the market has pushed eREIT valuations down over the last quarter, and particularly the past three weeks, due to fears of rising rates, history tells us that eREITs generally do well during periods of slowly rising rates and some eREITs will even beat the big market indexes under these conditions.

This is particularly true for REITs like STAG because the economic conditions that are causing the Fed to tighten monetary policy also increase demand for STAG’s industrial buildings. In addition to the increasing demand for STAG’s properties, the recent tax legislation included a 20% deduction for pass-through income from partnerships, MLPs, and REITs. This makes STAG’s current 6% dividend yield all that much more enticing. For a more complete discussion of the impact of rising rates on REIT financial performance as well as a more detail on the new pass-through provision, readers should see my earlier article “Consider Equity REITs for Your Next Investment“.

In Conclusion

STAG is a well established and well run industrial REIT with a history of steady and conservative growth. With economic growth picking up (GDP estimated between 3% – 4% for 2018), demand for industrial warehouse and light industrial building space should grow as well. This should provide STAG with the opportunity for continued growth in leased space as well as rent receipts.

Recent investor jitters over rising interest rates has pushed STAG’s stock price into bargain territory and its dividend yield up to 6%. The partnership and REIT pass-through provision in the recently passed tax legislation will shield 20% of STAG’s dividend from Federal income taxes. An investment in STAG at its current valuation should reward investors well in future years.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

Article by Dirk S. Leach, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

{kind=link}