Earnings season creates opportunities for investors. An overreaction due to one quarterly result can allow investors to purchase an otherwise strong firm at an undervalued price. With growing profitability, expansion into high margin segments, and a valuation implying permanent profit decline, this stock could significantly outperform moving forward. Spectrum Brands Holdings (SPB: $128/share) is this week’s Long Idea.

Spectrum Brands’ Impressive Profit Growth

Since 2011, Spectrum Brands has grown after-tax profit (NOPAT) by 25% compounded annually to $568 million in 2016. The company has grown revenue by 10% compounded annually to $5 billion over the same time. Per Figure 1, the company’s NOPAT margin has improved from 6% in 2011 to over 11% in 2016.

Figure 1: SPB Profitability Improvement Since 2011

Sources: New Constructs, LLC and company filings

In addition to NOPAT growth, Spectrum generated $711 million (10% of market cap) in free cash flow (FCF) in 2016 and $672 million over the last twelve months, which equates to a 6% FCF yield. Spectrum Brands has also exhibited good stewardship of capital amidst multiple acquisitions aimed at diversifying the business. Studies have shown that most acquisitions destroy shareholder value. Spectrum Brands’ management team has proven to be the outlier. Since 2011, SPB has improved its ROIC from 6% to 8%, per Figure 2.

Figure 2: Spectrum Brands’ Good Stewardship of Capital

Sources: New Constructs, LLC and company filings

Per Figure 3, ROIC explains 77% of the changes in valuation for the 17 Household Goods peers under coverage. Despite SPB’s 8% ROIC, in line with the 8% average of the peer group, the firm’s stock trades at a discount to peers as shown by its position below the trend line in Figure 3. If the stock were to trade at parity with its peers, it would be at $149/share – 16% above the current stock price. Given the firm’s rising ROIC and impressive profit growth, one would think the stock would garner a premium valuation.

Figure 3: ROIC Explains 77% Of Valuation for Household Goods Firms

Sources: New Constructs, LLC and company filings

SPB’s Profitability Helps Maintain Market Leading Positions

As a manufacturer of many household products with significant brand recognition, such as Rayovac, Remington, Black & Decker, George Foreman, Kwikset, Stanley, Eukanuba, Armor All, and Spectracide, among others, Spectrum Brands faces competition from many different firms. Competition includes Allegion PLC (ALLE), Energizer Holdings (ENR), Scotts Miracle-Gro (SMG), Newell Brands (NWL), Whirlpool Corporation (WHR), and Central Garden & Pet Company (CENT). Per Figure 4, SPB’s NOPAT margin ranks near the top of its competition.

High margins have allowed SPB to invest in product development initiatives, expand its global footprint, and build a strong brand presence across its many different markets. SPB’s profitability also allows it to weather economic downtimes and invest to prosper during economic growth. Most importantly, SPB is able to withstand pricing pressures from competition, or even provide products at a lower price to take market share while maintaining above average profitability.

Figure 4: SPB’s Profitability Among Peers

Sources: New Constructs, LLC and company filings.

Bear Concerns Assume Precipitous Decline In The Global Economy

Spectrum Brands’ segments are tied to many different aspects of the economy, including overall consumer spending, the global battery market, the housing market, and the automotive market. In order to buy-in to the bear case, one must not only ignore the positive domestic economic trends, but also Spectrum Brands’ diversification into higher margin business segments. Add in effective cost controls and the bear case seems even less likely.

A strong U.S. economy, where SPB generated 68% of 2016 revenues, bodes well for Spectrum Brands’ profit growth potential. Most importantly, personal consumption expenditures of durable goods, as measured by the U.S. Department of Commerce, have grown 4% compounded annually since 2014. The three-month moving average of wage growth has improved from 2.4% in March 2014 to 3.4% in March 2017. Lastly, consumer confidence, which measures the level of optimism regarding the economy, reached a 16 year high in March 2017.

In order to take advantage of the improving economy, Spectrum Brands has diversified its business away from its Global Batteries and Appliances segment (40% of 2016 revenue) into higher margin segments. The company expanded into the Global Auto Care segment in 2015, with the acquisition of Armored AutoGroup, maker of Armor All products. In 2014, Spectrum Brands acquired Tell Manufacturing, a lock manufacturer that expanded its Hardware & Home Improvement segment. Lastly, in 2014 the company expanded its Home & Garden lineup with the acquisition Liquid Fence. Per Figure 5, these three segments have greater margins than the Global Battery & Appliance segment and also grew revenues at a significantly higher rate.

Figure 5: Expanding Higher Margin Business Segments

*Net margin provided by Spectrum Brands Holdings in its 2016 10-K. Not enough disclosure to calculate NOPAT margins for each segment.

Sources: New Constructs, LLC and company filings

It’s important to note that sales growth, whether organic or via acquisition, is meaningless without prudent cost management. Through operating efficiencies, maximizing manufacturing capabilities, or running plants at full capacity, Spectrum has been able to improve its operating profitability. Per Figure 6, SPB’s cost of goods sold, selling, and general & administrative expenses have fallen as a percent of revenue since 2010. Furthermore, COGS, selling, general & administrative, and research & development costs have each grown less than revenue, which grew 12% compounded annually from 2010-2016.

Figure 6: Spectrum Brands’ Falling Operating Expenses

Sources: New Constructs, LLC and company filings

Bears will also raise concerns about Spectrum Brands’ revenue concentration. In 2016, Wal-Mart (WMT) represented 15% of sales and was the firm’s largest customer. Such concentration would be more concerning if it were based on one individual product. However, Spectrum Brands’ Wal-Mart concentration is spread across numerous products. Despite the Amazon (AMZN) threat, Wal-Mart has still grown sales 2% compounded annually over the past five years and represents a strong retail channel for Spectrum Brands. More importantly, Spectrum Brands’ products are also sold at Amazon, Lowe’s, Home Depot, Target, and others. Sales concentration is less of an issue when the same product can still be purchased at another retailer.

Lastly, SPB’s low valuation also undermines many bear arguments. Despite improving profitability, strong economic trends, and effective cost management, SPB’s current valuation implies a permanent decline in profits, as we’ll show below.

Spectrum Brands’ Cheap Valuation Implies Immediate Drop in Profits

Over the past two years, SPB is up 36% while the S&P is up 14%. However, over the past month, SPB has fallen 9%, after quarterly earnings missed expectations, while the S&P is up 2%. This price decline reflects investor overreaction to short-term events instead of a change in the fundamentals of the business and presents a buying opportunity. At its current price of $128/share, SPB has a price-to-economic book value (PEBV) ratio of 0.9. This ratio means the market expects Spectrum Brands’ NOPAT to permanently decline by 10%. This expectation seems overly pessimistic for a firm that has grown NOPAT by 25% compounded annually since 2011.

Even if SPB were to never again grow profits from current levels, the economic book value, or no growth value of the firm is $138/share – an 8% upside from the current valuation.

However, if SPB can maintain 2016 NOPAT margins (11%) and grow NOPAT by just 3% compounded annually for the next decade, the stock is worth $182/share today – a 42% upside. This scenario assumes SPB can grow revenue by consensus estimates in 2017 (1%) and 2018 (4%), and 4% each year thereafter, which is consistent with consumer spending growth in recent years. With an improving global economy, new product launches, and expanded manufacturing capacity, SPB could easily meet or surpass these expectations. Add in the potential yield detailed below and its clear why SPB could be a great portfolio addition.

Buy Backs Plus Dividend Could Yield Over 2%

In fiscal 2016, which ended September 2016 for Spectrum Brands, the company repurchased $43 million worth of stock. Through the first two quarters of 2017, SPB has repurchased $99 million. In January 2017, the company authorized $500 million in repurchases over the next three years. Going forward, if SPB were to average its 2016 and 2017 repurchase activity ($71 million per year), the firm would not exhaust its current authorization before expiration. A repurchase of this size is 1% of the current market cap. When combined, Spectrum’s 1% repurchase yield and 1.3% dividend yield offer investors a total potential yield of 2.3%.

New Product Introductions Could Create Earnings Beat

In order to grow revenues faster than the economy, consumer goods manufacturers can either spend on marketing, acquire growth, or introduce new products. Spectrum Brands has excelled in all three of these endeavors. At the same time, the firm must continue to control costs in order to maximize the value of revenue growth to shareholders.

In 2Q17, Spectrum Brands announced it was expanding capacity at its alkaline battery factory in Europe as demand exceeds capacity. The firm will be releasing new products in its high margin Global Auto Care segment, including new Armor All cleaning wipes, complete with TV marketing campaign, and new fuel system cleaners. To propel revenue growth in the Hardware & Home Improvement segment, SPB recently introduced new Kwikset smart locks. In Home & Garden, SPB is introducing new aerosol and liquid pest management products and a new weed-stop formula. In its Pet segment, SPB announced the acquisition of Petmatrix, a maker of rawhide-free dog chews. Lastly, in the Global Batteries & Appliance segment, SPB plans on releasing new Remington shavers and trimmers in the U.S. and a new Flex360 shaver along with hair care products in Europe.

Each of these new products expand SPB’s footprint in retail channels while also creating revenue growth opportunities. With improving margins and revenue, beating both top and bottom line expectations could prove an effective catalyst to send shares higher. When SPB reported 1Q17 results above consensus, the stock rose 8% the following day. In 3Q16, when SPB again beat bottom line expectations, the stock rose 12% in the following two weeks.

SPB could be poised for another beat and subsequent increase in valuation. In the meantime, investors in this stock carry very low valuation risk and are rewarded with a potential 2% total yield given SPB’s history of dividends and share repurchases.

Executive Compensation Plan Could Be Improved But Raises No Alarms

Spectrum Brands’ executive compensation plan, which includes base salary, annual incentives, and long-term incentives, is largely tied to two metrics. Both annual bonuses and equity incentives are tied to the achievement of EBITDA and free cash flow goals. A two-year equity incentive program is tied to the achievement of EPS and return on asset goals. We would prefer to see executive compensation tied to ROIC, since there is a strong correlation between ROIC and shareholder value. However, SPB’s current exec comp plan has not led to executives getting paid while destroying shareholder value. In fact, since 2010, Spectrum Brands’ economic earnings, the true cash flows of the business, have grown from $135 million to $260 million TTM, a clear creation of shareholder value.

Insider Trends Are Minimal While Short Interest Highlights Market Pessimism

Over the past 12 months, there have been 49 thousand insider shares purchased and 91 thousand insider shares sold for a net effect of 41 thousand insider shares sold. These sales represent less than 1% of shares outstanding. Additionally, short interest sits at 5.9 million shares, or 10% of shares outstanding. It would appear the market is ignoring Spectrum’s track record of profitability.

Impact of Footnotes Adjustments and Forensic Accounting

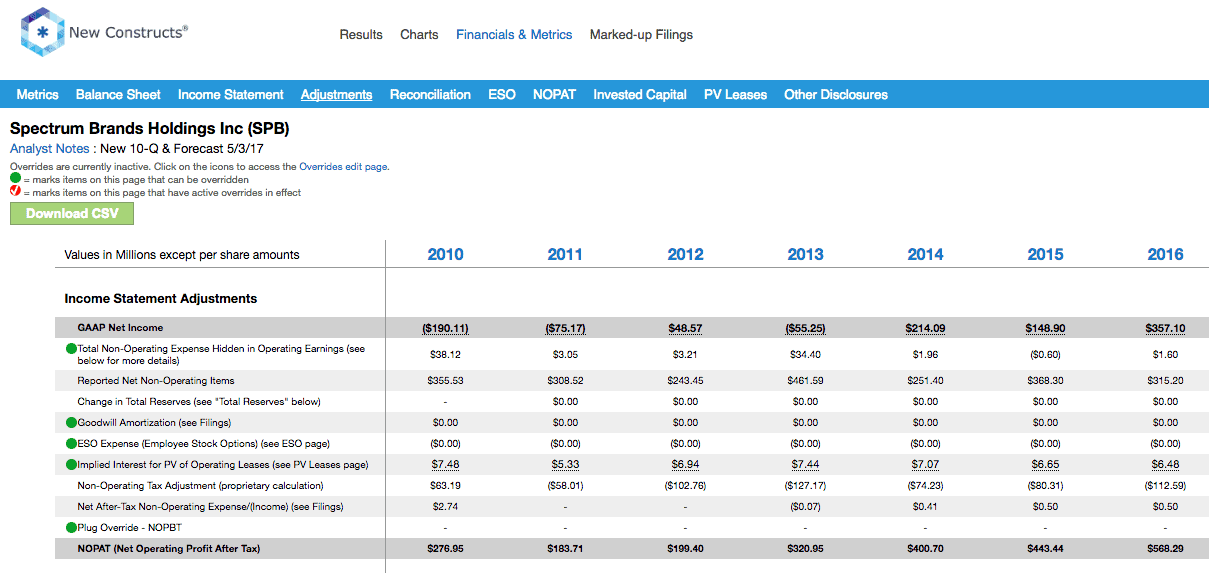

Our Robo-Analyst technology enables us to perform forensic accounting with scale and provide the research needed to fulfill fiduciary duties. In order to derive the true recurring cash flows, an accurate invested capital, and an accurate shareholder value, we made the following adjustments to Spectrum Brand’s 2016 10-K:

Income Statement: we made $453 million of adjustments, with a net effect of removing $211 million in non-operating expense (4% of revenue). We removed $121 million in non-operating income and $332 million in non-operating expenses. You can see all the adjustments made to SPB’s income statement here.

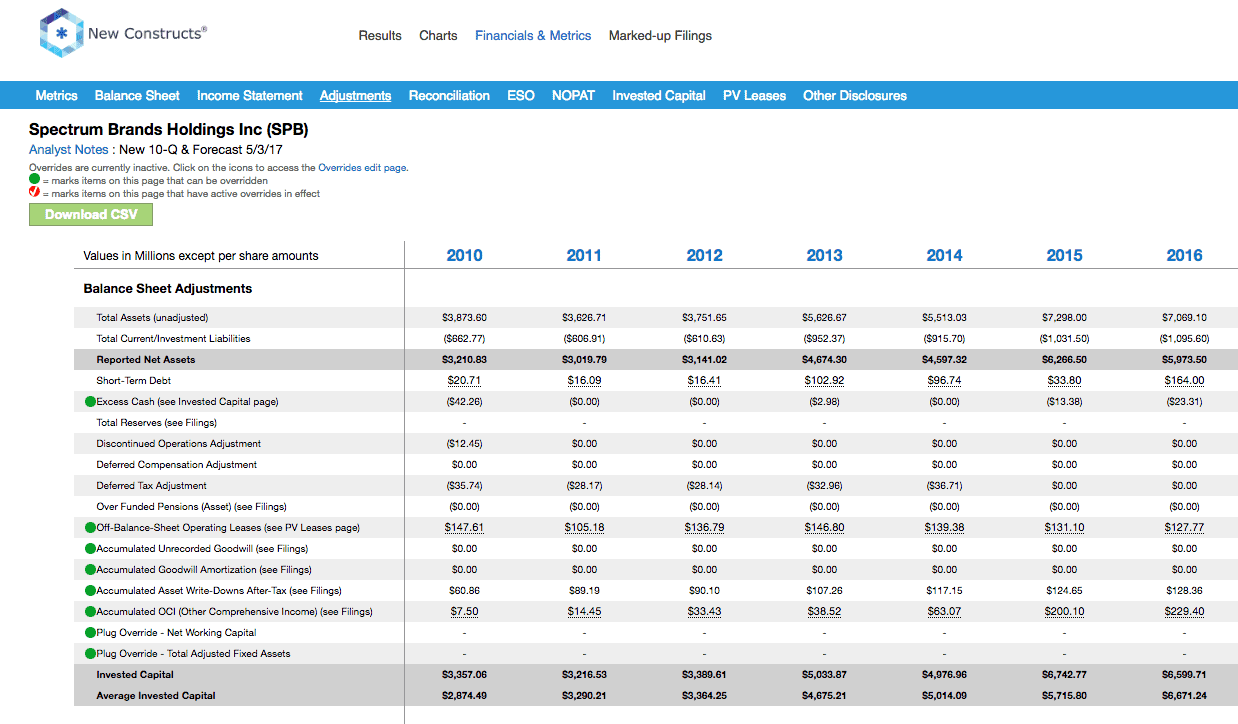

Balance Sheet: we made $750 million of adjustments to calculate invested capital with a net increase of $698 million. The largest adjustment was $236 million due to other comprehensive income. This adjustment represented 4% of reported net assets. You can see all the adjustments made to SPB’s balance sheet here.

Valuation: we made $4.6 billion of adjustments with a net effect of decreasing shareholder value by $4.6 billion. There were no adjustments that increased shareholder value. Apart from total debt, which includes $128 million in operating leases, one of the most notable adjustments was $578 million in net deferred tax liabilities. This adjustment represents 8% of SPB’s market cap. Despite the net decrease in shareholder value, SPB remains undervalued.

Attractive Funds That Hold SPB

The following funds receive our Attractive-or-better rating and allocate significantly to SPB.

- Blue Chip Investor Fund (BCIFX) – 4.2% allocation and Very Attractive rating.

- WBI Tactical SMV Shares (WBIB) – 2.5% allocation and Very Attractive rating.

This article originally published on May 15, 2017.

Disclosure: David Trainer and Kyle Guske II receive no compensation to write about any specific stock, style, or theme.

Article by Kyle Guske II, New Constructs

{kind=link}

{kind=link}

{kind=link}

{kind=link}