insights from Jay Younger, Investment Analyst at Aubrey Capital Management. Recently, Germany has been taking over the headlines as it was reported that it is likely to generate more than 50% of its power from renewable energy this year.

Mixed Reaction For Q2 Results

Q2 company results have seen a mixed reaction. Despite the average H1 sales and earnings per share (‘EPS’) growth being 21% and 35%, respectively, share prices have not necessarily followed. Rather, anticipation of further inflation and interest rate rises continues to impact share price performance. Several of our holdings have, however, had excellent results despite these headwinds and we believe that the portfolio is currently undervalued based on the potential for earnings growth to beat forecasts.

The most notable results in the portfolio during Q2 were from a German solar company which saw its H1 sales increase 65% year-on-year (YoY), its EBITDA improve 688% YoY and the margin expand by 12.8 percentage points. Management also confirmed that the company has upgraded its guidance for the full year, and the share price rose by 10% on the announcement. Despite this level of earnings growth, the shares trade on an FY23 PE of 15x which is significantly below their 5-year average, as well as their six-month average of 34x. This shows that there is still potential for a re-rating.

Another set of results that stood out was from a UK company specialising in road safety barriers and galvanising. This company generates 73% of its profits from the US meaning that the company is well positioned to benefit from increased onshoring and the Infrastructure Investments and Jobs Act (IIJA). The company reported 20% YoY sales growth, an operating margin expansion of 2.4 percentage points and earnings per share growth of 39% YoY. The shares increased 8% as management guided that year-end operating profit will most likely be ahead of current market expectations. The valuation is compelling with the shares trading on a FY23 PE of 20x with an expected EPS growth of 24%, placing the company on a price-to-earnings ratio to earnings growth (‘PEG’) of 0.8x.

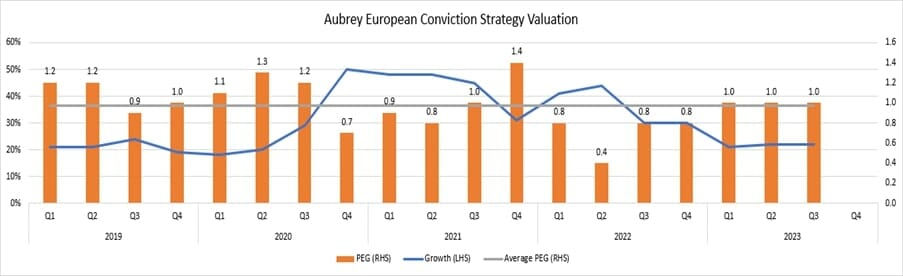

The portfolio’s earnings growth has averaged well above our 15% minimum, and the valuation is still very attractive. Despite the expansion in the earnings growth (denominator of the PE multiple), the increase in price (numerator of the ratio) has yet to follow. The portfolio is trading on an average PE of 21x with an expected two-year average earnings per share growth of 21%. This values the portfolio on a PEG of 1x.

As shown in the chart below, the portfolio’s average 5-year PEG is 1x so, at a glance, the portfolio is currently trading at fair value. However, the average FY23 H1 EPS growth was 35% and the market’s expectation for annual EPS growth is 21%. H2 2022 was, however, dominated by margin contraction as cost inflation peaked and, since then, the average margin has expanded by 50 basis points with most of our companies being able to pass on inflation to their customers. As a result, we anticipate better earnings growth in H2 2023 and therefore a lower PEG. In addition, we believe we are nearing the peak in the interest rate cycle which should also make the environment more conducive to growth stock investing.