The Wall Street Journal published an article on January 7 challenging the safety of municipal bonds as “not [being] the reliable bet they once were.” While its headline may startle some investors, we’ve been endorsing this view for years. Municipal bonds simply aren’t a set-it-and-forget-it choice.

But that doesn’t mean we reject the notion of investing in municipal bonds as a core strategy for investors. In fact, we’ve adapted to and embraced the new municipal investment environment. Here’s why—and how—we do it.

The Market Has Evolved

It’s true. The muni market doesn’t look like it did before the global financial crisis of 2008. That crisis, when munis suffered alongside riskier markets, was the catalyst for a transformative period for an asset class that had seen little change for decades.

John Coumarianos, the author of the Journal article, spent some time discussing “high-profile distress and bankruptcy.” This is one small area where we take issue with the author while agreeing in principle on most of his other points. But it’s important, because default fears tend to loom large, while as always, default risk in the municipal market remains remote.

Only a tiny portion of the muni universe has defaulted in the 10 years since the financial crisis. The primary credit risks in the muni market remain upgrades and downgrades, not defaults. Upgrades and downgrades occur with far greater frequency than defaults.

But the municipal market has changed since 2008, and dramatically so:

Bond insurance. Thanks to muni bond insurers becoming entangled with the subprime mortgage crisis, municipal bond insurance has collapsed. In 2007, 46.8% of municipal bonds issued came with insurance. By 2017, that figure had dropped to 5.3%.

Credit quality. The demise of bond insurance exposed the underlying quality of issuers. In 2007, 69% of bonds were rated AAA. In 2017, roughly 14% of the market was AAA-rated. The net result was the creation of a municipal credit market, with commensurate risks and opportunities.

Investing challenges. Net municipal issuance has been flat since the financial crisis, as municipalities have chosen an austere path. Also, in light of regulatory changes, primary dealers are not stocking bonds on balance sheets as they once did. In 2007, dealer inventories were $50 billion. This had dropped to $14 billion by 2016.

Transaction costs. Pre-crisis costs on a purchase of $25,000 to $100,000 would have run 1.2%. We estimate that the same purchase today would cost as much as 1.6%. This is a significant penalty for individual municipal bond purchases. Further changes are afoot later this year for disclosure rules.

The capital markets, including the municipal market, are dynamic and continue to evolve. Your manager should be dynamic and evolving too. And that means being active.

Be an Active Muni Investor

There’s no question, then, that municipal market risks have increased over the past decade. What’s more, municipal market risks aren’t static. This means that they must be actively managed, not left to the vagaries of a passive ladder.

But risks aren’t the only problem with passive muni ladders.

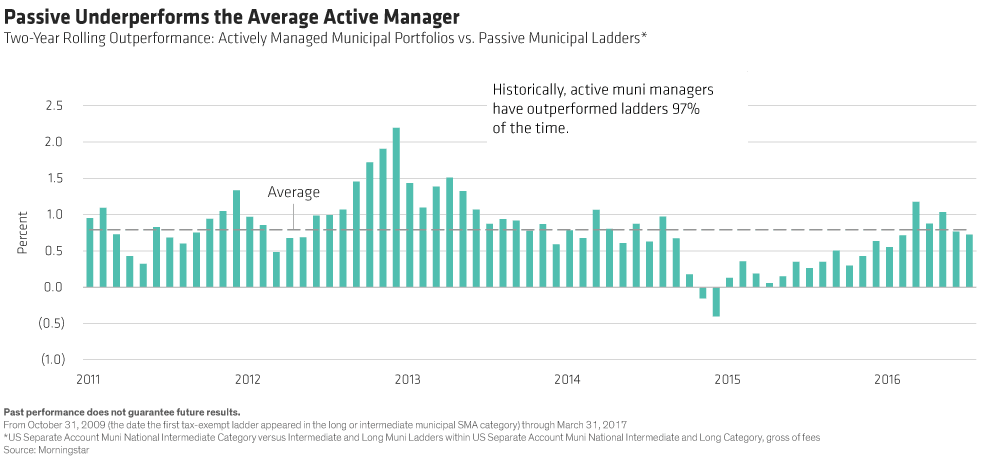

Year after year, passive muni investors lose out on yield and return. Since 2009, the average active municipal bond manager has outperformed passively managed municipal ladders (Display) in an astounding 97% of two-year rolling periods—and by an average of nearly 80 basis points.

Passive ladders also lock in low yields. While they’ll eventually begin to capture rising yields, it takes them a long time to get there. In addition, some strategies can have significantly more interest-rate risk than investors expect, and that can translate into painful volatility as rates rise.

In contrast, an actively managed municipal portfolio provides access to multiple sources of after-tax income and return potential, while also providing greater liquidity, diversification and risk control.

Have a Flexible Municipal Manager

Some kinds of actively managed portfolios have an even greater advantage. Flexible municipal mandates adhere to the three principles of municipal investing: safety, income and after-tax return. But they recognize that being nimble—namely, trading across markets and across the credit spectrum—does a better job of keeping a portfolio on track with those objectives. Here are some approaches we recommend taking today.

Shift into taxable bonds to control volatility. Small opportunistic positions in US Treasuries and other taxable bonds in municipal portfolios can buffer portfolios during volatile periods. For investors subject to high tax rates, municipal bonds continue to make sense. But relative after-tax yields fluctuate as market conditions change, and investors should take advantage of those relative changes to help manage their risk and return. Because Treasuries are very liquid, they can be bought and sold quickly and efficiently.

For example, last November, municipal issuance soared in advance of expected tax reforms that could eliminate certain types of municipals, such as private activity bonds. The excess supply depressed prices of municipal bonds, which returned (0.54)%, while Treasuries posted (0.17)%. As a result, flexible municipal portfolios with a buffer of Treasury bonds outperformed municipal-only portfolios. By the end of the month, municipals had become very attractively priced. At that point, having the ability to sell Treasuries quickly in order to buy munis at discounted prices was enviable.

Boost income with credit. The demise of bond insurance in the early post-crisis period can be seen in a positive light: it unlocked a lot of opportunity for active managers with the ability to thoroughly research lower-rated securities.

In fact, one way to increase the income of a muni portfolio today is by selectively adding mid-grade and high-yield municipal bonds. This is currently preferable to boosting income by lengthening maturity, which exposes investors to more rising-rate risk as the flat yield curve eventually steepens.

Protect yourself against inflation. Whether inflation creeps higher, as suggested by some market indicators, or volatility emerges around inflation expectations, municipal portfolios should preserve their purchasing power. A bonus: inflation protection is currently inexpensive.

Ask Your Managers if They Are Evolved

Lastly, Coumarianos pointed ominously to the returns of the Bloomberg Barclays Municipal Index during the crash of 2008. Rather than providing the expected offset to equities’ negative returns, that muni index posted (2.5)% during that period. And that was prior to the demise of bond insurance. The next equity downturn might result in an even more difficult experience for muni investors, he cautions.

We agree that it could—providing they are passive investors, and providing they have not adapted to the new environment.

And remember that even in 2008, not all municipal strategies had negative returns. Active, flexible strategies held up much better during that toxic environment. That’s why investors should demand such flexibility from their active muni managers.

Managers who have evolved along with the market should have every advantage in identifying the opportunities and navigating the challenges of the new municipal investment environment.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Article by Daryl Clements, Alliance Bernstein