Next week I will be in Washington, D.C., attending Evercore ISI’s Energy Policy & Geopolitics Conference, where I will be visiting senior staff from the White House infrastructure team and House Energy and Commerce Committee. I will also be meeting with John Fagan, head of the Treasury Department’s Markets Room, and Robin Dunnigan, the Bureau of Energy Resource’s Deputy Assistant Secretary for Energy Diplomacy. Among the topics of discussion will include energy independence, legal and policy issues impacting the energy sector, tax reform and geopolitical risks in Syria, Russia and Iran.

I want to extend my gratitude for this opportunity to Evercore ISI chairman Ed Hyman, who was ranked as the top economist by Institutional Investor magazine for 35 straight years, from 1980 to 2014. I’ll have much to share with our investment team when I return.

Let’s Get Fiscal

President Donald Trump today tweeted his frustration with the “ridiculous standard of the first 100 days,” claiming that no matter what he accomplishes during this period, the “media will kill” it.

There’s some truth here. No U.S. president in modern history has been so vehemently and routinely lambasted by a hostile press corps as Trump has. Harsh jabs have even been thrown by business news sources such as the Wall Street Journal and Bloomberg, which are normally pretty centrist.

But for those keeping score, Trump’s 100th day arrives next Sunday, April 29, and it would be disingenuous to describe his tenure so far as smooth sailing. He’s faced a number of significant setbacks and distractions, including federal judges’ smackdown of his two travel bans, a failure to repeal and replace Obamacare and an ongoing investigation into his administration’s possible collusion with the Russian government in the months leading up to the November election.

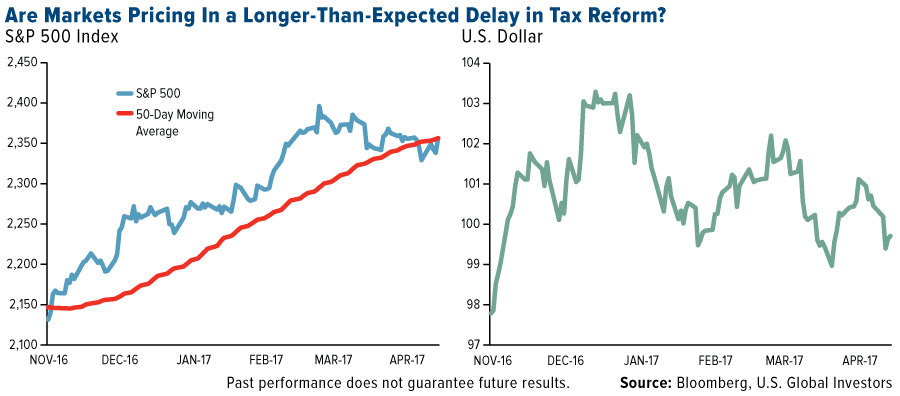

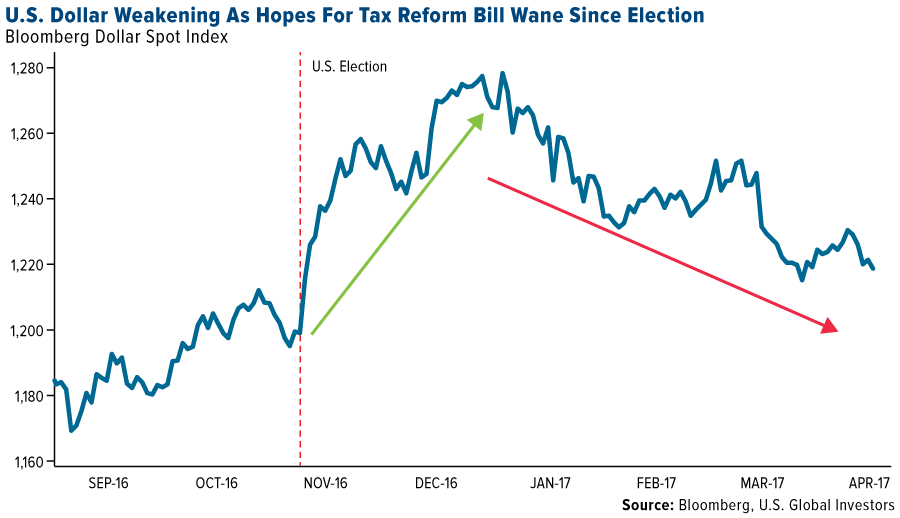

Although consumer confidence remains at scorching-hot levels, markets are beginning to express doubt in Trump’s ability to streamline corporate tax and regulation reform. From their all-time high in mid-March, blue chip stocks have given back more than 1 percent, while the U.S. dollar has contracted more than 3.4 percent since late December.

I believe this response is way overdone. BCA geopolitical strategist Marko Papic said as much during his visit to our office last month. Marko insisted that tax reform is still on its way, despite Congress’ earlier failure to repeal Obamacare. Just this week, House Speaker Paul Ryan said lawmakers were putting the “finishing touches” on a new health care bill—one that reportedly might scrap protections for people with preexisting conditions—while Treasury Secretary Steven Mnuchin reassured Americans they can soon expect to see proposals for “the most significant change to the tax code since Reagan.”

As I write this, Trump says a “massive” tax reform package could be unveiled as early as next week.

Such change can’t come soon enough. Since 1993, the U.S. has had a top statutory corporate tax rate of 35 percent, the highest of any other economy in the Organization for Economic Cooperation and Development (OECD). Trump expressly prefers to lower the rate to 15 percent, but I wouldn’t be surprised if it ends up between 20 and 25 percent. Regardless, tax relief would be a major win for small and mid-cap firms especially and encourage large multinational companies to repatriate foreign cash. According to one recent estimate, the top 50 largest American corporations stashed as much as $1.6 trillion overseas in 2015. It’s time we give them an incentive to bring some of that cash back home.

It’s worth pointing out that Trump is not yet lagging his predecessors in terms of delivering fiscal reform. Going back to the Kennedy administration, the average number of months into a new presidential term for fiscal legislation to be enacted is six months, according to LPL Research. It took nearly a year for the Tax Reform Act of 1969 to reach President Nixon’s desk. This week marks Trump’s third month in office, so I see no cause for alarm just yet.

| President | Action | Date Passed | Months into New Term |

|---|---|---|---|

| Kennedy | Spending Increases | June 1961 | 5 |

| Nixon | Tax Cut | December 1969 | 11 |

| Ford | Tax Cut | March 1975 | 7 |

| Reagan | Tax Cut | August 1981 | 7 |

| Clinton | Tax Increase | August 1993 | 7 |

| George W. Bush | Tax Cut | June 2001 | 5 |

| Obama | Tax Cut and Spending | February 2009 | 1 |

| Average: 6 Months | |||

| Source: LPL Research, U.S. Global Investors | |||

As for the American Recovery and Reinvestment Act of 2009, signed by President Obama not 30 days into his first term, it had already been in the works before he took office.

There are other obvious reasons for lowering the corporate tax rate. Just take a look at Singapore and Hong Kong, both of which enjoy a top tax rate of between 16 and 17 percent. Consequently, they stand as glittering marvels of the modern world.

In the World Bank’s 14th annual “Doing Business 2017” report, Singapore ranked second in the world in ease of doing business, Hong Kong fourth. The U.S., meanwhile, came in at number eight. Tax reform could have the potential of moving the country up the scale.

Banks Awaiting Deregulation

Besides tax reform, hearings are expected to take place next week on how best to loosen Wall Street regulations. At the top of the docket is the 2010 Dodd-Frank Act, for which Rep. Jeb Hensarling of Texas has drafted a 600-page replacement called the Financial Choice Act 2.0. If passed, the legislation would relax some of Dodd-Frank’s more restrictive rules and limit the powers of the Consumer Financial Protection Bureau (CFPB) and Securities and Exchange Commission (SEC). It would also roll back the so-called Volcker Rule, named for former Federal Reserve Chair Paul Volcker, which effectively bans banks from making speculative investments that don’t directly benefit their customers.

In Hensarling’s words, the Financial Choice Act “holds Wall Street and Washington accountable, ends taxpayer-funded bank bailouts and unleashes America’s economic potential.”

Also facing a questionable future is the Labor Department’s Fiduciary Rule, which regulates how financial advisors service their clients, specifically by eliminating conflicts of interest. Originally scheduled to go into effect April 10, the Trump administration has delayed it until June 9, pending review.

As I wrote back in January, the Fiduciary Rule, though well-intentioned, would inevitably limit the number of investment products available to retail investors. In an effort to remain compliant with the rule, well-meaning financial professionals would recommend only the least expensive products, regardless of whether they’re a good fit. As a result, many mutual funds—which might be better performing but have higher expenses than other investment vehicles—would fall off of brokerage firms’ platforms.

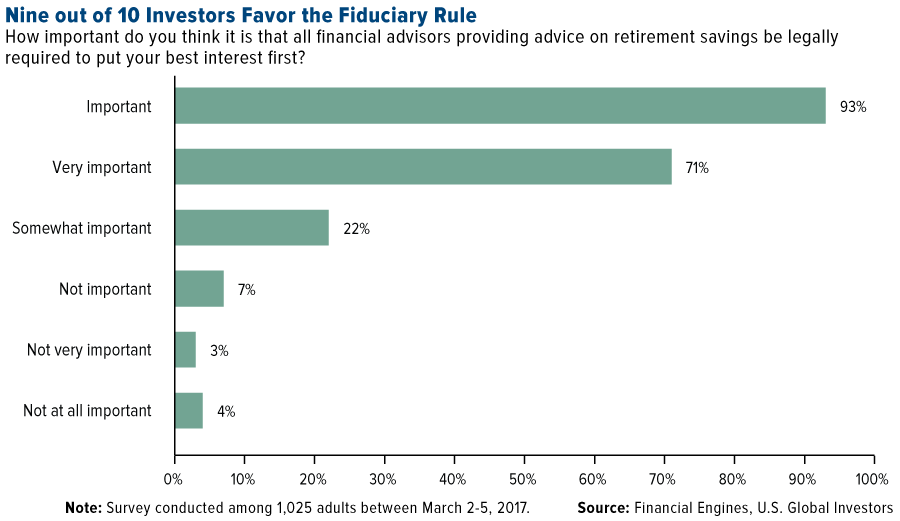

In all fairness, there’s definitely demand for improved investor service among financial professionals. In a recent survey conducted by advisory firm Financial Engines, 93 percent of respondents said they felt financial advisors should legally be required to put investors’ interests first.

However, the same survey found that nearly 70 percent of respondents had not heard of the DOL’s Fiduciary Rule. This tells me they might not have considered all the ramifications, including the good and the bad, of holding advisors to such strict standards.

A Modest Proposal

To be clear, I’m not in favor of scrapping every banking regulation that’s been introduced post-financial crisis. I am in favor of reviewing them, as Trump has ordered, and streamlining them to make them work for the financial sector and consumers rather than against them. This week Federal Reserve Governor Jerome Powell made a similar statement, cautioning policymakers against rolling back “core reforms” that in many ways have strengthened our financial system.

In addition, the International Monetary Fund (IMF), in its Global Financial Stability Report, warned that a “wholesale dilution or backtracking” of existing regulations in the U.S., coupled with deep tax cuts, could lead to dangerously high financial risk-taking such as we saw pre-2008.

“Many nonfinancial firms do have the balance sheet capacity to expand investment, and reductions in corporate tax burdens could have a positive impact on their cash flow,” the IMF writes. “But reforms could also spur increased financial risk-taking and, in some scenarios, could raise leverage from already-elevated levels.”

Indeed, as you can see below, median corporate leverage among the largest U.S. companies is nearing a record high as measured by debt-to EBITDA (earnings before interest, taxes, depreciation and amortization).

Aux yeux de tous

The world will be watching France this weekend as voters head to the polls in the first round of the country’s presidential election. It’s currently a four-way race, with political novice and social liberal Emmanuel Macron polling slightly ahead of the far-right candidate Marine Le Pen. In recent days, however, radical socialist candidate Jean-Luc Mélenchon has gained impressive ground, closing in on center-right François Fillon, the former prime minister of France.

Likely influencing voters’ decisions is yesterday’s attack on Paris’ iconic Champs-Élysées boulevard—just a few blocks from the presidential palace—which left one police officer dead. ISIS has already claimed responsibility. The incident is eerily reminiscent of a 2012 French thriller film titled “Aux yeux de tous,” about a terrorist attack in Paris that occurs mere days before a presidential election.

In any case, the attack could very well boost Le Pen’s chances, as she has repeatedly taken the hardest stance toward terrorism and immigration in general. This was not lost on Trump, who tweeted that “the people of France will not take much more of this. Will have a big effect on presidential election!”

The second round of voting is scheduled for May 7. I’ll have more to say next week! Until then, happy investing!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.46 percent. The S&P 500 Stock Index rose 0.85 percent, while the Nasdaq Composite climbed 1.82 percent. The Russell 2000 small capitalization index gained 2.57 percent this week.

- The Hang Seng Composite lost 0.98 percent this week; while Taiwan was down 0.16 percent and the KOSPI rose 1.41 percent.

- The 10-year Treasury bond yield rose slightly to 2.24 percent.

Domestic Equity Market

Strengths

- Industrials was the best performing sector of the week, increasing by 1 percent versus an overall increase of 0.09 percent for the S&P 500.

- Lam Research was the best performing stock for the week, increasing 9.93 percent.

- Visa’s total payments spiked. The world’s largest payments operator earned $0.86 a share as operating revenue jumped 23.5 percent to $4.48 billion. Visa says total payments volume spiked 37.2 percent versus a year ago.

Weaknesses

- Energy was the worst performing sector for the week, falling 2.32 percent versus an overall increase of 0.09 percent for the S&P 500.

- Mattel was the worst performing stock for the week, falling 13.67 percent.

- Verizon reported quarterly results that missed estimates and said it lost subscribers who pay a monthly bill, despite the relaunch of unlimited data plans. Verizon said it lost 307,000 retail postpaid subscribers on a net basis in the first quarter.

Opportunities

- Qualcomm beats earnings. The chipmaker earned an adjusted $1.34 per share, well ahead of the $1.19 that analysts were anticipating, helping to ease concerns over its patent-licensing business.

- D.R. Horton beat on profits, helped by higher home sales. America’s largest homebuilder raised its revenue forecast for the year.

- American Express beat as card member spending jumped. The company earned $1.34 per share on revenue of $7.89 billion as card member spending grew 8 percent on a currency-adjusted basis.

Threats

- In a note to clients on Thursday on what he called “the $1 trillion flow that conquers all,” BofA’s chief investment strategist observed that the amount of financial assets added to central banks’ balance sheets was the “one flow that matters” in the market. “$1 trillion of financial assets that central banks (European Central Banks & Bank of Japan) have bought year-to-date (= $3.6tn annualized = largest CB buying in the past 10 years); ongoing Liquidity Supernova best explanation why global stocks and bonds both annualizing double-digit gains year-to-date despite Trump, Le Pen, China, macro,” Hartnett wrote. Put another way, the $1 trillion in bonds and stocks bought this year by central banks like the ECB, the BOJ and the Swiss National Bank, puts purchases on pace for $3.6 trillion in buying this year, the most dating back to the start of the global financial crisis in 2007. This dynamic could cause serious turmoil in the markets when central banks start unwinding their balance sheets.

- Shares of General Electric fell even after the company beat expectations for earnings and revenue. GE’s cash flow from industrial operations turned negative, down $1.6 billion, worse than the $600 million drop which was expected.

- The Treasury Department says it won’t issue Exxon Mobil a waiver to work in Russia. Exxon applied for a waiver from sanctions on Russia in an effort to restart its joint venture with state oil company PAO Rosneft in the Black Sea.

April 19, 2017U.S. Global Investors’ Gold Fund Earns Lipper Fund Award |

April 13, 2017Gold Moves on Trump’s U.S. Dollar Comment |

April 12, 2017What Lumber Could Mean For Gold – Copy |

The Economy and Bond Market

Strengths

- U.S. existing home sales jumped 4.4 percent to a 5.71 million rate in March, the highest in over 10 years, according to the National Association of Realtors.

- Industrial production, the Federal Reserve’s measure of U.S. goods output, was right in line with expectations for the month of March. Production increased by 0.5 percent, the exact increase expected by economists.

- Europe’s economic renaissance shows no signs of slowing down. “By country, faster business activity growth in France — the strongest seen since May 2011 — was offset by a moderation in Germany, albeit with the pace of German expansion still running at one of the fastest seen over the past six years,” a release from Markit announcing the data said.

Weaknesses

- U.S. retail sales, a key barometer of growth given the economy is two-thirds reliant on consumer spending, fell for a second straight month.

- U.S. consumer prices in March fell for the first time since February 2016, led by a decline in gas prices. The consumer price index fell 0.3 percent, according to the Labor Department. Economists had forecast that the index would be unchanged. Excluding the volatile costs of food and energy, so-called core CPI fell 0.1 percent, the first decline since January 2010.

- New residential construction dropped by more than expected in March, but permitting for future construction remained strong. Housing starts fell by 6.8 percent to a seasonally adjusted annual rate of 1.215 million, while permits increased by 3.6 percent at a rate of 1.26 million.

Opportunities

- President Donald Trump said that he expects to release his plan for a tax overhaul on “Wednesday or shortly thereafter.” In an interview with the Associated Press, he said he would cut the federal corporate tax rate to 15 percent from its current 35 percent level.

- The Federal Reserve’s Beige Book maintained that the economy continues to expand at a modest pace, supporting the Fed’s view that it can raise borrowing costs two more times this year.

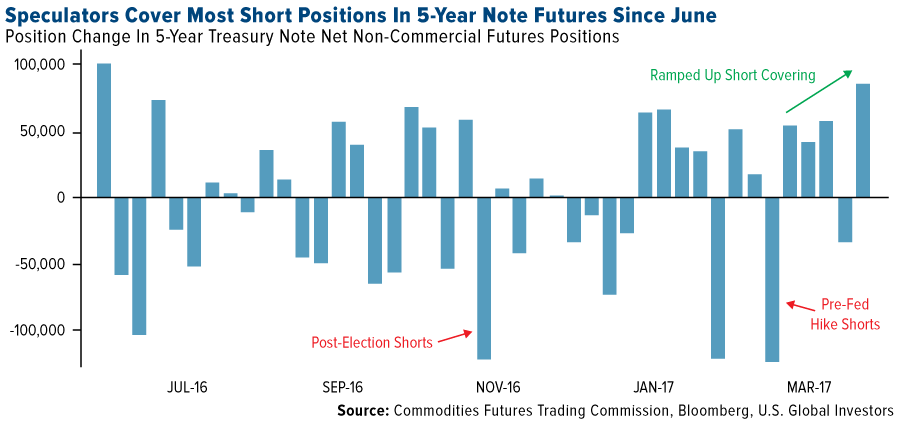

- Speculators betting against U.S. treasuries have been forced to cover their short positions as the Trump reflation trade loses steam.

Threats

- France is going to the polls on Sunday to vote in what is likely to be a highly contested presidential election. Four candidates, Emmanuel Macron, Marine Le Pen, Francois Fillon, and Jean-Luc Melenchon — are within percentage points of one another in the polls, but only two will advance to the run-off in May. The election has markets on edge as two of the candidates, Le Pen and Melenchon, have campaigned on euro-skeptic platforms. In a somewhat eerie coincidence, the betting odds of either euro-skeptic candidate winning the presidency closely mirror those of the U.K. voting in favor of Brexit. We all know how that turned out.

- The focus in the U.S. next week will be the advance first quarter GDP report on Friday. First quarter growth could be biased lower by residual seasonality issues.

- U.S. consumer confidence will be released next Tuesday. The latest measures of consumer optimism have been softening and a disappointing report would add concern about future consumer spending.

Gold Market

This week spot gold closed at $1,284.77, down $3.11 per ounce, or 0.24 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 3.62 percent. Junior-tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index off just 1.16 percent. The U.S. Trade-Weighted Dollar Index finished the week lower by 0.62 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Apr-14 | U.S. CPI YoY | 2.6% | 2.4% | 2.7% |

| Apr-16 | China Retail Sales YoY | 9.7% | 10.9% | 10.9% |

| Apr-18 | U.S. Housing Starts | 1250k | 1215k | 1303k |

| Apr-19 | Eurozone CPI Core YoY | 0.7% | 0.7% | 0.7% |

| Apr-20 | U.S. Initial Jobless Claims | 240k | 244k | 234k |

| Apr-25 | Hong Kong Exports YoY | 10.0% | — | 18.2% |

| Apr-25 | U.S. New Home Sales | 585k | — | 592k |

| Apr-25 | Conf. Board Consumer Confidence | 123.3 | — | 125.6 |

| Apr-27 | ECB Main Refinancing Rate | 0.000% | — | 0.000% |

| Apr-27 | Germany CPI YoY | 1.9% | — | 1.6% |

| Apr-27 | U.S. Durable Goods Orders | 1.4% | — | 1.8% |

| Apr-27 | U.S. Initial Jobless Claims | 240k | — | 244k |

| Apr-28 | Eurozone CPI Core YoY | 1.0% | — | 0.7% |

| Apr-28 | U.S. GDP Annualized QoQ | 1.3% | — | 2.1% |

Strengths

- All the precious metals were off slightly this week with platinum, gold and palladium off 0.16 percent, 0.24 percent and 0.28 percent, respectively. Treasuries extended their gains earlier in the week as soft inflation data from the U.S. fed into the markets and the dollar dropped, reports Bloomberg. Macro news ranging from inflation data casting doubt on the pace of rate hikes to the U.S. decision not to label any countries as currency manipulators have extended the advance in haven assets.

- Gold climbed to a five-month high in New York, reports Bloomberg, with the Bloomberg Dollar Spot Index falling 0.3 percent. “Gold will likely stay elevated given safe haven demand,” Barnabas Gan, economist at OCBC, said. “I won’t be surprised if gold breaches above its $1,200 handle in the foreseeable future.” On Friday, gold traders and analysts surveyed by Bloomberg were bullish on the yellow metal’s price outlook for a sixth week.

- Sberbank, Russia’s largest bank, is looking to finance the direct import of gold to India, according to Aleksei Kechko, Managing Director of the company’s Indian subsidiary. India is the world’s second largest importer of gold, and a direct trade between India and Russia would be beneficial to both countries. Russian officials have already signaled their desire to conduct transactions with BRICS nations using gold, writes Russia Insider. In related news, India’s Trade Ministry is preparing a proposal to cut the gold import duty to 2 percent in two years from 10 percent, ET Now and Newswire reports.

Weaknesses

- Silver stood out as the worst performing precious metal for the week with a loss of 3.30 percent, as hedge funds cut net bullish silver positions in the futures market. According to analysts at Commerzbank, demand for gold coins in the U.S. proved very muted in the first three months of the year. Analyst Eugen Weinberg wrote “Retail investors in the U.S. have clearly been put off by the increase in the price of gold.” The U.S. Mint sold 166,000 ounces of gold coins in the first quarter of the year, a third less than a year earlier.

- Gold fell sharply for the second day this week as someone dumped $3 billion notional ahead of the London Fix, reports ZeroHedge. In a somewhat related note, analysts from Standard Chartered believe the relative strength index implies gold prices are overbought at the moment, reports FXStreet.com, which could stall prices in coming sessions.

- Shandong Tyan Home Co. says it is no longer pursuing Barrick Gold Corp.’s stake in its Kalgoorlie Super Pit mine in Australia, reports Bloomberg. The Chinese company is blaming tightened controls on outbound investment and foreign exchange, the article continues. In other company news, Newcrest’s shut down of its Cadia mine could cost the company nearly 9 percent of annual earnings, writes UBS analysts led by James Brennan-Chong. Shares of the company fell 4.6 percent on Tuesday after it announced Cadia will not meet fiscal year 2017 guidance after the seismic event.

Opportunities

- Gold’s top forecaster for the last quarter, Intesa Sanpaola SpA, says that the metal’s price could hit $1,350 by year end, citing faster inflation and geopolitical tensions. Similarly, silver could climb to $19 an ounce by year end, after already gaining 15 percent so far in 2017. BMI Research also noted this week that it remains bullish on gold and expects silver to perform even stronger as well. Platinum and palladium on the other hand, are likely to face pressure from a slowdown in car demand in the U.S. and China, said Daniela Corsini with Intesa Sanpaola.

- According to the Bloomberg Intelligence team, the Fed could be “one and done” in 2017 when it comes to rate hikes. “Unless things are very different this time, declining crude oil prices, bond yields and copper vs. gold aren’t consistent with further interest-rate increases,” the article reads. Looking at history, expectations for higher rates may be too aggressive unless these Fed tightening companions reverse higher, the article continues. In a separate article from BI, the team writes that $1,400 gold resistance might be the new $1,300. On a related note, ZeroHedge reports this week that Li Ka-shing, the richest man in Asia, has a renewed and urgent interest in diversifying his assets into gold, both mining firms and the physical asset itself. Some of the biggest billionaire investors on the planet are seeking out the metal as wealth protection insurance.

- Seeking Alpha writes that 2016 was a record year for Klondex Mines, with production of 151,007 gold-equivalent ounces (GEOs) from its Nevada operations and 10,199 GEOs from True North. This brings total production to 161,289 GEOs, or an increase of 26.3 percent from the previous year. For 2017, Klondex is guiding for production of 210-225k GEOs. Klondex is a proven mid-tier gold producer that owns and operates all of its mines. M Partners, in a note out this week, announced that it is increasing its target for Klondex to C$8.25 from $8.00, driven by its revised estimates on Klondex’s True North mine and Midas. Even Clarus Securities writes, “Our thesis continues to be that Klondex offers best-in-class production growth, low cost production and a solid management execution track record. Clarus maintains its buy target price of $8.50 per share.

Threats

- Currency traders and strategists (who make a living in the $5.1-trillion-a-day currency market) say that the core assumptions of U.S. dollar appreciation being one of the selling points of Trump’s border tax plan is “laughable,” reports Bloomberg. These traders are saying you’d be hard-pressed to find anyone in the market who believes it will result in the greenback strengthening 25 percent as the border tax plan suggests. Another note from Bloomberg states that the dollar has resumed the downward trajectory it established at the start of the year, and could fall an additional 4 percent in the coming weeks (if one believes that the U.S. currency moves in sync with real yields and Treasuries).

- Laurence Fink, CEO of Blackrock Inc., says that lackluster growth in the U.S. economy and uncertainty around the Trump administration’s ability, poses a risk to markets, reports Bloomberg. Fink mentioned a pullback in car sales and a slowdown in M&A activity as indications of the uncertainty. “There are warning signs that things are getting darker,” he said. Speaking of the U.S. economy, U.S. central bankers appear to be on course to raise interest rates twice more this year and remain confident in their forecast for growth around 2 percent, reports Bloomberg.

- A new study out shows that exchange-traded funds appear to be making stock markets dumber and more expensive, reports Bloomberg. Researchers from Stanford University, Emory University and the Interdisciplinary Center of Herzliya in Israel uncovered evidence that higher ownership of individual stocks by ETFs widens the bid-ask spreads in those shares (making them more expensive to trade and therefore less attractive), reports Bloomberg. “Our evidence suggests the growth of ETFs may have unintended, long-run consequences for the pricing efficiency of the underlying securities,” wrote the researchers for the study. In a related matter, the SEC this month gave its final go-ahead for measures that would trigger the delisting process for an ETF should its index become overly concentrated, or stocks and bonds in an index become hard to trade.

Energy and Natural Resources Market

Strengths

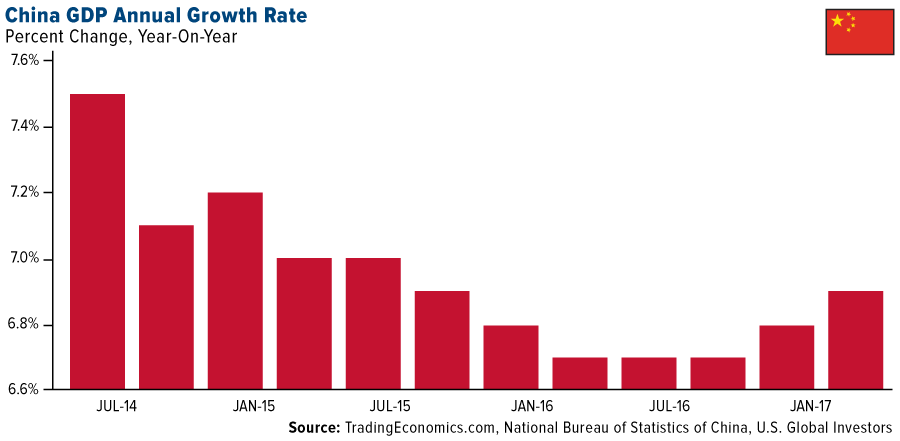

- Year-over-year GDP growth in China came in at its fastest pace in six quarters this week at 6.9 percent versus consensus estimates of 6.6 percent, according to Reuters. This marks the strongest expansion of the economy since the third quarter of 2015. The surge in the important data point is supported by an increase in fiscal stimulus which has increased industrial output, retail sales and fixed-asset investment. A positive read-through from one of the world’s largest engines of economic growth.

- The best performing sector for the week was the S&P Super Composite Containers & Packing Industry Index. The index rose 4.6 percent on the back of a flurry of new money entering the sector, as consolidation and M&A activity takes center stage.

- WestRock, an American corrugated packaging company, was the best performing stock this week finishing up 7.45 percent. The stock rose after being upgraded to a buy from Goldman Sachs.

Weaknesses

- China’s steel output surged to record highs, according to Bloomberg. Production of steel expanded 1.8 percent in the month of March from a year earlier to 72 million metric tons, reports the National Statistics Bureau, implying an average daily run rate of 2.32 million tons, beating out the previous monthly record. Output for the first quarter of this year was up 4.6 percent from a year earlier. Infrastructure and real estate demand have been the key drivers behind the commodities rally earlier this year; however, it is evident that steel makers have overestimated demand resulting in a rise much faster than actual end-user demand.

- The worst performing sector this week was the S&P Super Oil & Gas Equipment & Services Sub Industry Index. The index fell 4 percent on the back of higher than expected oil inventories in the U.S. this week.

- The worst performing stock for the week was Yara International ASA, a Norwegian chemical company. The company fell 9.45 percent on the back of releasing weaker than expected earnings for the first quarter.

Opportunities

- Iran, one of the world’s largest producers of oil, is ready to join OPEC’s production cut extension, according to an article published by Oilprice.com. The country had been exempted from the group’s production cut agreement in November; however, the country has now reached a comfortable level of output and is ready to join the agreement, provided there is consensus amongst the cartels members. A positive read-through on the fundamentals of oil.

- The aluminum market is starting to show signs of tightening as premiums are up and stocks are down. According to Reuters, signs of tightening are most evident from aluminum buyers in Japan who are beginning to pay a premium of $128 per tonne over the London metal exchanges (LME’s) cash price. In addition, to the metals market dynamics, China is proposing to cut capacity by 30 to 50 percent this year in key production regions such as Beijing, Tianjin, and Hebei in an attempt to curb the treacherous pollution problem that the country deals with.

- The International Energy Agency (IEA) says the global oil market is “very close” to coming into balance. In the organization’s monthly oil market report, the IEA made note of the fact that global oil stocks will decline this year if OPEC maintains its production cuts with allies like Russia beyond May, which may potentially support higher prices after oil’s three-year-long slump. A positive read-through for oil.

Threats

- U.S. factory output tumbled in March, according to ZeroHedge. While U.S. industrial production headlines met expectations, U.S. factory output for March fell 0.4 percent, the biggest drop on record since February of 2015. It is also noteworthy to point out that U.S. industrial production remains down almost 2 percent from the record high levels of 2014, which has never happened without the U.S. economy being in recession in history. A negative read-through for raw materials.

- Housing starts dropped the most in four months, according to Bloomberg. Housing starts dropped by 6.8 percent month-over-month in March, the lowest since November 2016. The biggest driver of the drop was a 35-percent plunge in Midwest single-family starts. As lumber is a key input for the housing sector, this is a negative read-through for lumber demand and prices.

- According to Reuters, corn is back in the spotlight as it is estimated that China is sitting on close to 250 million tonnes of the commodity, which is equal to more than a year of consumption. However, at current rates of consumption, the population will take roughly three to five years to work through current stockpiles. As farmers in the west are also facing stockpile problems, alternative ways of using corn are of the essence in order to avoid further downward pressure on the price of the agricultural commodity.

China Region

Strengths

- China’s economic results came in better than expected for the first quarter. Gross domestic product (GDP) growth year-over-year was 6.9 percent, which beat expectations of 6.8 percent. Other key results also beat expectations, with retail sales growth at 10.9 percent and industrial production growth at 7.6 percent. JP Morgan has raised its China GDP expectations from 6.6 to 6.7 percent for 2017.

- Taiwan’s year-over-year March export orders came in up 12.3 percent, ahead of expectations for a gain of 8.8 percent.

- TCC International Holdings (1136 HK) soared 37.05 percent this week, making it the top gainer in the Hang Seng Composite Index in that timeframe, after the company announced Taiwan Cement plans to take an additional TCC stake and go private.

Weaknesses

- The Shanghai Composite Index fell 2.25 percent for the week, as investor sentiment was weakened due to increased scrutiny of trading practices.

- China’s one year bond yield rose this week to its highest levels since 2015 and, as economic growth remains steady and encouraging, bond sentiment has suffered somewhat, as indicated by the yields.

- Energy constituted the worst-performing sector in the Hang Seng Composite Index for the week, falling 3.38 percent.

Opportunities

- Starting in July, China will cut the value-added tax rate for natural gas and agricultural goods. The rate will drop to 11 percent from 13 percent.

- Shanghai is hosting Asia’s biggest auto show, giving manufacturers the opportunity to show off their latest robot and battery technology. China has been the world’s largest auto market since 2009, surpassing the U.S. Chinese auto makers actually have smaller workforces than their peers in the U.S., Europe and Japan.

- Geely Automobile Holdings is launching its new upscale Lynk & Co. line of autos soon. The Lynk SUV will be made in China, and will be sold to Europe and the U.S. Geely plans capacity for 160,000 units in the first year at its Luqiao plant, where it also manufactures Volvo.

Threats

- A Bloomberg Intelligence report highlights the possibility that Thailand could run the risk of being added to the U.S. watch list for currency manipulation—a possibility that may effectively restrict Thai efforts to curb appreciation of the baht. The Trump administration hopes for more “reciprocity” in trade, and in a country by country analysis, Thailand may stand out: it has a bilateral trade surplus of about $19 billion—just below the 20 billion threshold that counts as a strike (two strikes lands a country on the watch list; three strikes demands the label of “currency manipulator”); Thailand has also, with Vietnam, made persistent, net FX purchases (a strike); and, while Thailand does not currently run a current-account surplus of larger than 3 percent of GDP, it could, the article reports, by boosting its net exports to the U.S. by a mere 6 percent this year.

- Efforts to curb housing price appreciation in China have been somewhat ineffective, exacerbating risks of an overheated market while simultaneously driving would-be borrowers to shadow banking or alternative financing methods.

- Tensions are rising in the region, as North Korea plans to test missiles regularly, even as often as weekly, according to comments by Vice-Foreign Minister Han Song-ryol in an interview with BBC. The minister warned that “all-out war” would result if the U.S. military took action. Meanwhile, U.S. Vice President Mike Pence has warned North Korea not to test the U.S.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 2.6 percent. Turkish equites rallied after Sunday’s executive presidency referendum on expectations that political noise will subside and the government will focus on boosting growth going forward.

- The Turkish lira was the best performing currency this week, gaining 1.7 percent against the U.S. dollar. Credit Suisse and Deutsche Bank issued favorable forecasts for the currency. Credit Suisse expects monetary policy to favor the lira, and Deutsche Bank sees the currency as the cheapest in the world, predicting that it will be supported by strong global growth.

- The financial sector was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 1.8 percent. Greece had a 2016 primary surplus almost seven times higher than its bailout target, but the IMF is skeptical that the performance can be maintained. It estimates at least half the surplus came from one-off measures not structural changes. The current account deficit widened in February to 937 million euros from 828 million euros a year ago.

- The Russian ruble was the worst performing currency this week, losing 40 basis points against the U.S. dollar. Despite OPEC discussions to extend oil production cuts beyond June, Brent lost 7.3 percent closing at $51.91 per barrel Friday. The ruble historically trades in tight correlation with the price of oil.

- The consumer staples sector was the worst performing sector among eastern European markets this week.

Opportunities

- A Bank of America survey shows that euro-area equites are the most favored right now. Allocation to U.S. stocks fell to the lowest level since January 2008, at net 20 percent underweight from net 1 percent overweight last month, while allocation to eurozone equities rose to a 15-month high, at net 48 percent overweight from net 27 percent overweight last month. April rotation to euro-area stocks from U.S. is the fifth largest since 1999; 83 percent of investors say U.S. stocks are overvalued.

- The Prime Minister of Great Britain, Theresa May, called snap elections for June 8; her conservative party should come out of the election with a greater majority. According to Bank Credit Analyst research, the snap election reduces the odds of a “hard Brexit.” Sterling should receive a short-term lift, it could retrace to 1.3 GBP against the dollar, the level seen immediately after last year’s Brexit referendum.

- The eurozone economy bounded into the second quarter with strong, broad-based growth, according to a survey showing businesses increased activity at the fastest rate for six years, with new orders remaining robust. Markit’s Flash Composite Purchasing Managers’ Index, seen as a good guide to growth, climbed to 56.7 from March’s 56.4 reading, the highest level since April 2011. A reading above 50 indicates growth.

Threats

- The European Commission estimates Italy’s economy to grow by 0.9 percent in 2017, the lowest rate of any member of the European Union. The country’s public debt to GDP ratio is projected to be 133.3 percent in 2017, lower only than Greece’s among EU members. Investors are focused on France as it will be holding the first round of presidential elections this Sunday, but the bigger worry to eurozone stability could present Italy with weak growth, struggling banks and high public debt.

- In last Sunday’s referendum, the people of Turkey agreed to give President Erdogan extra powers. This formal shift to executive presidency will kick in with the next dual Parliamentary and Presidential elections scheduled to be held in November 2019. In the short term, a constitutional ban on the President’s formal association with the political party will be removed, the Supreme Council of Judges and Prosecutors will be restructured, and military courts will be abolished, according to Deutsche Bank research. As expected, the state of emergency imposed after the failed coup attempt was extended for another three months. Turkey is moving toward presidential regime, a more authoritarian one.

- Donald Trump is reversing his views toward Russia and China. Once hard on China, the U.S. President is now saying that there is more business to be done with Beijing than with Moscow. Trump recently hosted Chinese President Xi Jinping, and with a growing focus on North Korea’s nuclear tests, he is looking for help from China.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| DJIA | 20,547.76 | +94.51 | +0.46% |

| S&P 500 | 2,348.69 | +19.74 | +0.85% |

| S&P Energy | 498.53 | -10.87 | -2.13% |

| S&P Basic Materials | 327.37 | +5.60 | +1.74% |

| Nasdaq | 5,910.52 | +105.37 | +1.82% |

| Russell 2000 | 1,379.85 | +34.61 | +2.57% |

| Hang Seng Composite Index | 3,306.89 | -32.74 | -0.98% |

| Korean KOSPI Index | 2,165.04 | +30.16 | +1.41% |

| S&P/TSX Global Gold Index | 217.58 | -3.50 | -1.58% |

| XAU | 86.84 | -2.56 | -2.86% |

| Gold Futures | 1,286.70 | -1.80 | -0.14% |

| Oil Futures | 49.54 | -3.64 | -6.84% |

| Natural Gas Futures | 3.10 | -0.13 | -3.90% |

| SS&P/TSX Venture Index | 824.92 | -9.70 | -1.16% |

| 10-Yr Treasury Bond | 2.24 | +0.01 | +0.27% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| DJIA | 20,547.76 | -113.54 | -0.55% |

| S&P 500 | 2,348.69 | +0.24 | +0.01% |

| S&P Energy | 498.53 | -8.52 | -1.68% |

| S&P Basic Materials | 327.37 | +1.36 | +0.42% |

| Nasdaq | 5,910.52 | +88.88 | +1.53% |

| Russell 2000 | 1,379.85 | +34.26 | +2.55% |

| Hang Seng Composite Index | 3,306.89 | -36.33 | -1.09% |

| Korean KOSPI Index | 2,165.04 | -3.26 | -0.15% |

| S&P/TSX Global Gold Index | 217.58 | +4.74 | +2.23% |

| XAU | 86.84 | +1.74 | +2.04% |

| Gold Futures | 1,286.70 | +33.90 | +2.71% |

| Oil Futures | 49.54 | +1.50 | +3.12% |

| Natural Gas Futures | 3.10 | +0.09 | +2.99% |

| SS&P/TSX Venture Index | 824.92 | +24.00 | +3.00% |

| 10-Yr Treasury Bond | 2.24 | -0.16 | -6.73% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| DJIA | 20,547.76 | +720.51 | +3.63% |

| S&P 500 | 2,348.69 | +77.38 | +3.41% |

| S&P Energy | 498.53 | -48.88 | -8.93% |

| S&P Basic Materials | 327.37 | +6.37 | +1.98% |

| Nasdaq | 5,910.52 | +355.19 | +6.39% |

| Russell 2000 | 1,379.85 | +28.01 | +2.07% |

| Hang Seng Composite Index | 3,306.89 | +192.88 | +6.19% |

| Korean KOSPI Index | 2,165.04 | +99.43 | +4.81% |

| S&P/TSX Global Gold Index | 217.58 | +5.95 | +2.81% |

| XAU | 86.84 | -1.84 | -2.07% |

| Gold Futures | 1,286.70 | +76.00 | +6.28% |

| Oil Futures | 49.54 | -2.88 | -5.49% |

| Natural Gas Futures | 3.10 | -0.10 | -3.21% |

| SS&P/TSX Venture Index | 824.92 | +27.33 | +3.43% |

| 10-Yr Treasury Bond | 2.24 | -0.22 | -9.08% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investHoldings may change daily.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 3/31/17:

Great Wall Motor Co Ltd.

BYD Electronic

Ford

Geely Automotive

Guangzhou Automobile

Sberbank of Russia PJSC

Barrick Gold Corp

Klondex MinesLtd.

Yara International ASA

Visa Inc.

Qualcomm Inc.

Exxon Mobil Corp.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The Bloomberg Dollar Spot Index (BBDXY) tracks the performance of a basket of 10 leading global currencies versus the U.S. Dollar.

The Shanghai Composite Index (SSE) is an index of all stocks that trade on the Shanghai Stock Exchange.

The S&P 500 Super Composite Containers & Packaging Industry Index is a capitalization-weighted index.

The S&P Super Oil & Gas Equipment and Services Sub Industry Index is a capitalization-weighted index.