One thing I learned early on – thanks to Bayes Theory – is to never look at scenarios in absolute terms.

Q2 hedge fund letters, conference, scoops etc

“That will never happen.”

“Don’t worry. It’s a sure thing.”

Instead – you need to look at outcomes in a probabilistic way.

What I mean is: look at things in the chance of them occurring

“There’s a 15% chance that will happen.”

“Given the information – I expect I’m 85% sure.”

Instead of today’s complacent attitude that “nothing bad will happen” – I think it’s more like 50/50. And each time the Federal Reserve tightens – that risk value grows.

Here’s why. . .

The problem going on in the markets is there’s growing complacency even though fundamentals don’t support any further upside.

Otherwise put – investors are feeling too comfortable and expect the market to trend higher, even though the bottom’s slowly falling out from underneath.

The risks that caused huge sell-offs earlier this year haven’t been solved. And the ‘tighter money’ path central banks worldwide are continuing on may be what triggers the next crisis.

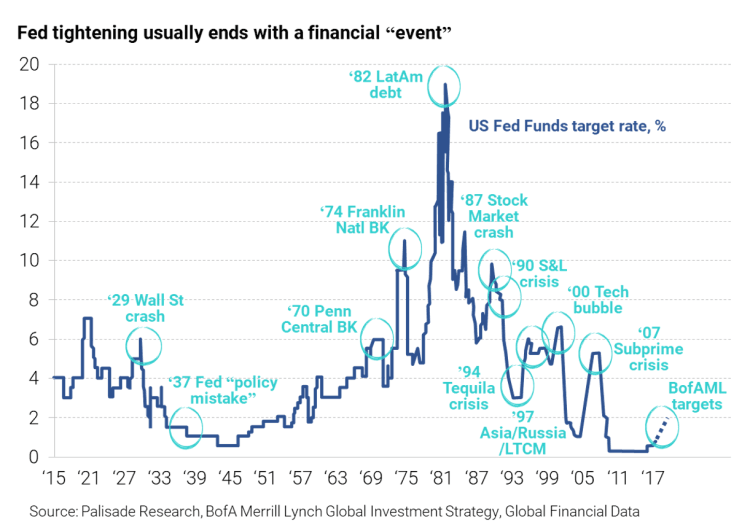

As we know from history – every time the Federal Reserve has tightened, there’s some-kind-of negative financial event. . .

The Austrian Business Cycle – created by Ludwig Von Mises – explains that during the cheap money/low rate period, markets get out of whack.

Consumers binge on debt. Corporations binge on debt. Investors overvalue not-so-great stocks. Liquidity trumps fundamentals. And economic growth increases.

But – most importantly – future demand’s into the present. . .

What I mean is: when interest rates get cut lower – a buyer can now finance that new car he wanted with low service payments. But, once he has the car – he won’t buy a new car for the next two or three years.

This is exactly what the Fed wants when they cut rates. They wish to subsidize growth today at the expense of the future.

But eventually everyone refinances their homes and buys things on credit – and must spend the next few-to-several years paying it off.

All this demand and buying causes growth to look artificially higher in the short-term – so the Fed pats themselves on the back for a job-well-done. And begins raising rates.

Now everyone who binged on debt is facing higher interest payments. And even worse – the assets they bought fall in price.

Imagine all those overleveraged home buyers in 2006 expecting the continued low-rates and rising home prices. . .

Hence the above chart showing the boom-and-bust cycle. And as you can see – these crises have become more frequent during the last 25 years.

Simply put – the markets today are riding on the tailwinds of the easy money and low-interest days.

Each time the Fed tightens – the riskier things get out there. . .

But nothing is at greater risk today than the potential collapse of world trade. Especially as China and the U.S. rotate from a trade war and into a currency war. . .

In early May – we saw the historically accurate South Korean Export Growth Indicator (aka SKEG) signal an upcoming earnings recession.

Of course, the mainstream ignored this – I doubt they even know about it.

But instead of following the complacent markets with their “nothing bad will happen to global earnings” talk – I believed things will get much worse.

And they have – because as South Korea saw collapsing growth in their exports – now the whole world is.

World trade volume is tanking – as I wrote about in early June – and it will also bring down global corporate earnings with it.

But the recent Bank of America data only bolsters our ‘coming earnings recession’ risk value. . .

Global trade sharply dropped and is now negative on a 3-month (3M) annualized basis. And this historically is followed with a collapse in global earnings.

Look at the correlation since the year 2000. . .

While world trade continues to decline – so will the corporate profits that depend on it.

And as President Trump is set to announce another $200 billion in tariffs against Chinese goods – expect things to get even worse.

The elevated markets and complacency aren’t justified by the underlying fundamentals. And until central banks begin easing and trade spats end – you must be on guard.

I’m not saying things will crash overnight – but I wouldn’t jump into risky-assets at these times.

As far as ‘weighing’ the risks of a global earnings recession – thus far, I believe there’s an 80% chance it will happen by this time next year.

And as more information comes out – I expect that percentage to increase. . .

When you look at the bigger picture all together – and the long run – there’s plenty of reasons for investors to not be complacent.

Adem Tumerkan, Editor-in-Chief, Palisade-Research

{kind=link}