Logica Capital commentary for the month of March 31, 2022.

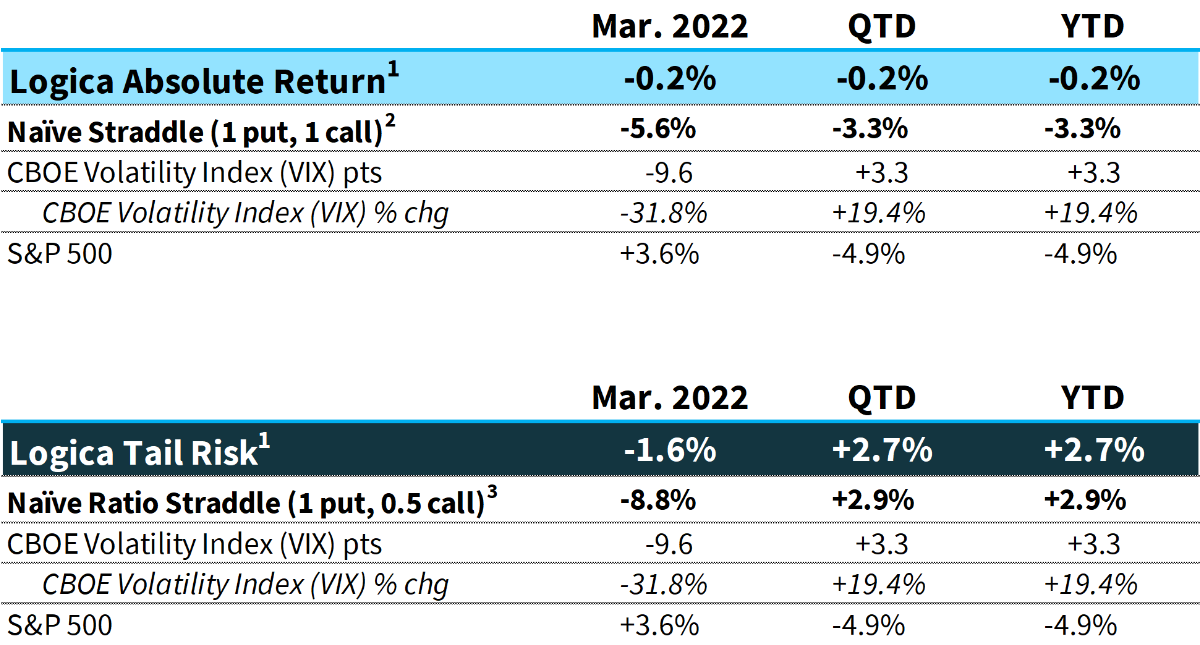

Logica Absolute Return (LAR) – Upside/Downside Convexity – No Correlation

- Tactical/dynamic balanced Put/Call allocation – Straddle

Logica Tail Risk (LTR) – Max Downside Convexity – Strong Negative Correlation

- Tactical/dynamic downside tilted Put/Call allocation – Ratio Straddle

Q1 2022 hedge fund letters, conferences and more

Click here to view/download as PDF

Summary

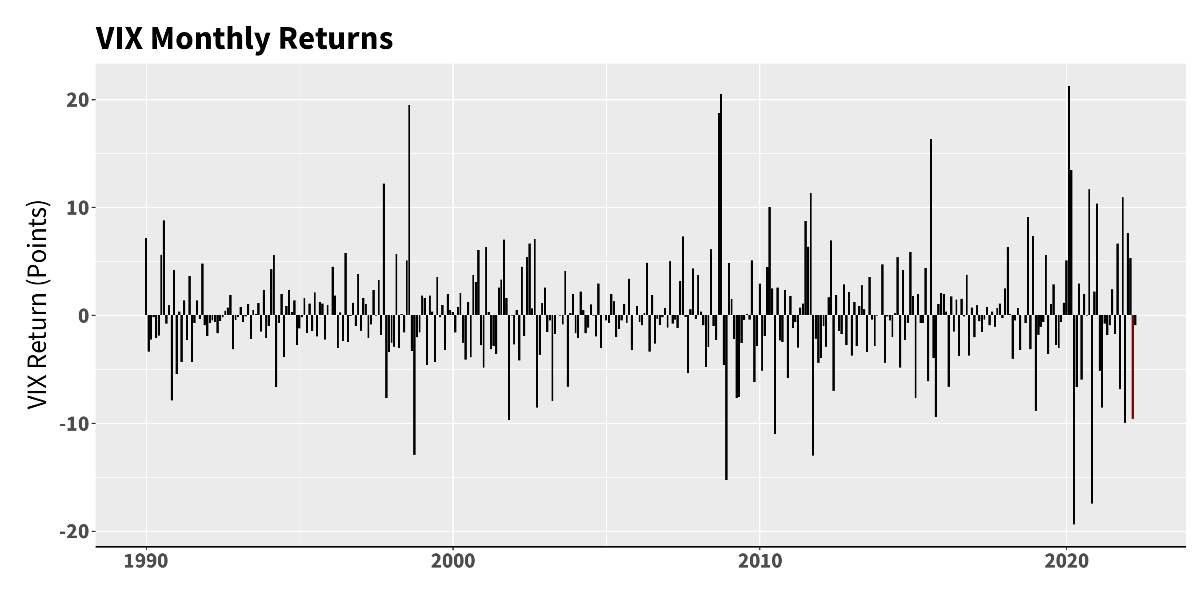

With early/mid-month fireworks to the downside and threats of a lower low, we continued to observe a muted reaction from implied volatility as compared with other crisis environments. Following that sell-off, the S&P 500 roared back to new “local” highs, during which implied volatility was absolutely crushed. In fact, the CBOE Volatility Index (VIX) posted one of its 10 worst calendar month returns in the past 30+ years. In total, we witnessed a far greater reaction from Implied Volatility to the recovery than we did to the downside event.

1 Returns are net of fees and represent the returns of Logica Absolute Return Fund, LP and Logica Tail Risk Fund, LP, respectively. Past performance is not indicative of future results.

2 Naïve Straddle Return: a 1.5 month out, S&P 500 at-the-money put and call bought on the final trading day of prior month and sold on the final trading day of current month. This return on premium is divided by a factor of 6 to be comparable to Logica’s typical AUM-to-premium ratio. For illustration purposes only.

3 Naïve Ratio Straddle Return: a 1.5 month out, S&P 500 at-the-money put and at-the-money call (divided by 2) bought on the final trading day of prior month and sold on the final trading day of current month. This return on premium is divided by a factor of 6 to be comparable to Logica’s typical AUM-to-premium ratio. For illustration purposes only.

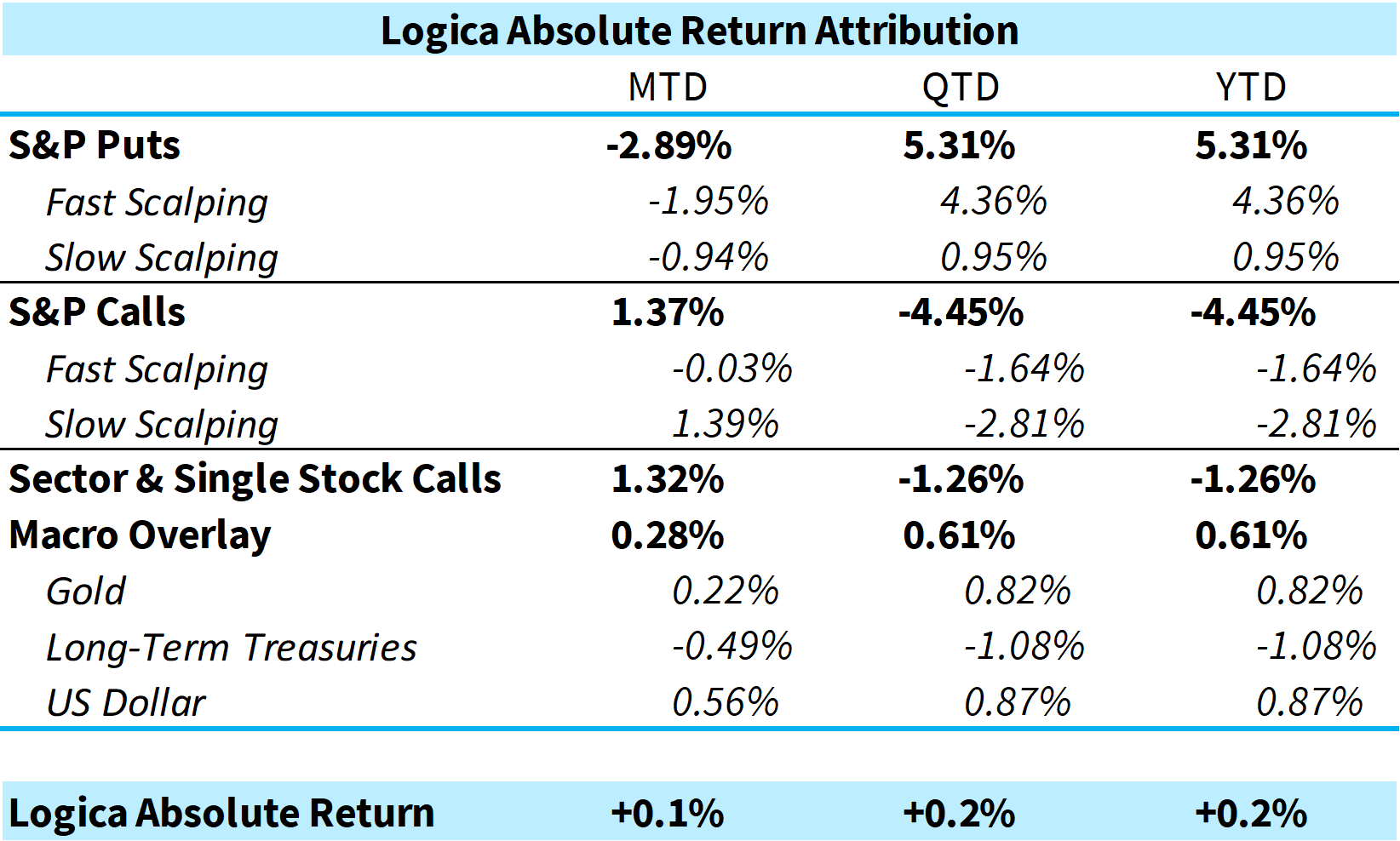

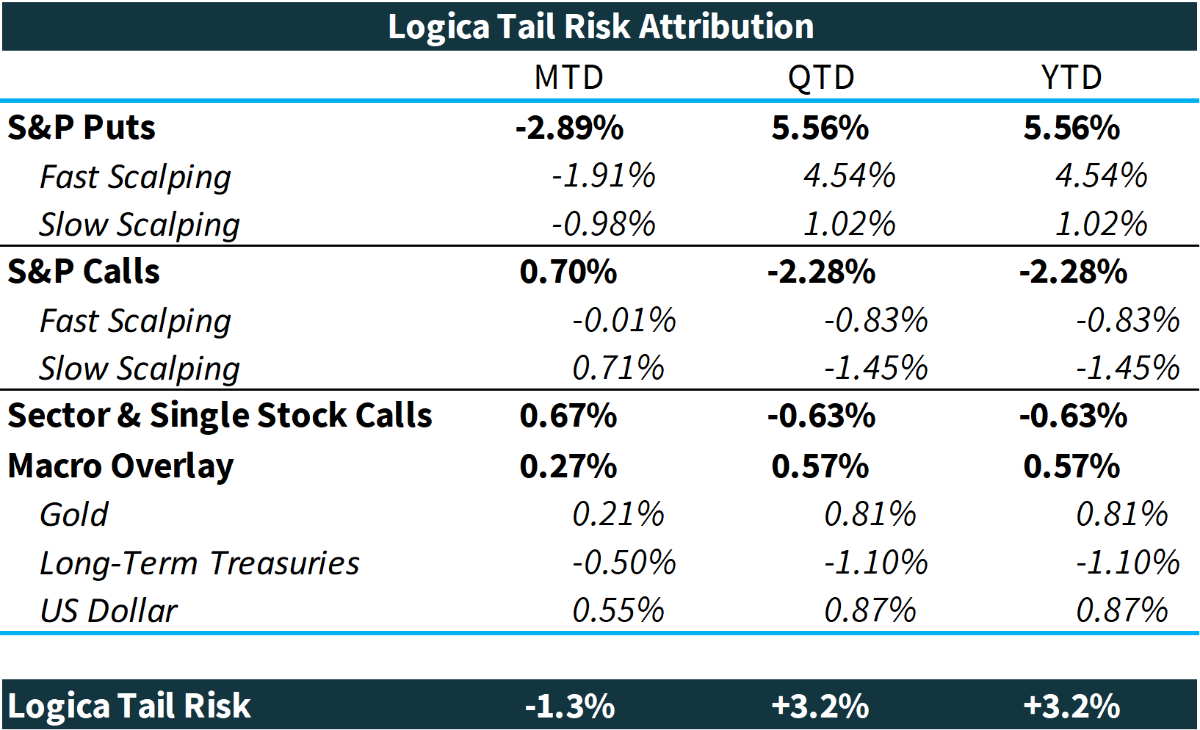

Commentary & Portfolio Return Attribution*

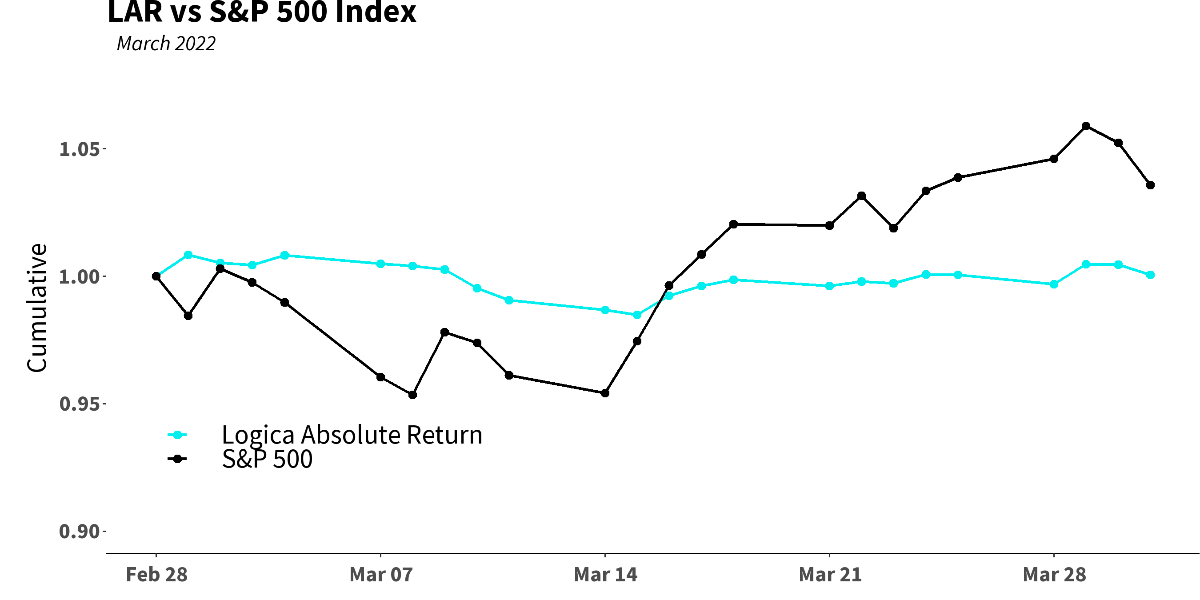

March began with the S&P 500 meeting stiff overhead resistance at its 200 day moving average and threatening to make new lows – both March 8th and 14th represented the lowest closing prices since mid-2021, albeit the low point of those days did not breach the low of Feb. 24th. Following this came a furious rally during which VIX gave back an astounding -18.9 points on an S&P move of +11.3% (more on this relationship later).

Sector & Single Stock Calls continue to impress and given our reduction of Long-Term Treasuries exposure we mentioned in our January letter, our Macro Overlay was also able to contribute positively in March. Bonds continue to get pummeled as TLT recorded its 4th worst quarterly return in the last 20 years.

Over the course of Q1, the theme is the same, and if you’ve been reading our letters, you won’t be surprised to hear us sing the praises of the alpha contributed by our Sector & Single Stock Calls module, having a similar delta notional exposure as our S&P Calls, and being down significantly less on the quarter/year. Having once again seen our selection model outperform the S&P in up markets as well as contain itself better in down markets, and further align with the years of our building and testing before we implemented this model in late 2020, we feel even more comfortable with the embedded alpha.

* For illustration purposes only. Attribution returns are composed of daily returns, gross of fees

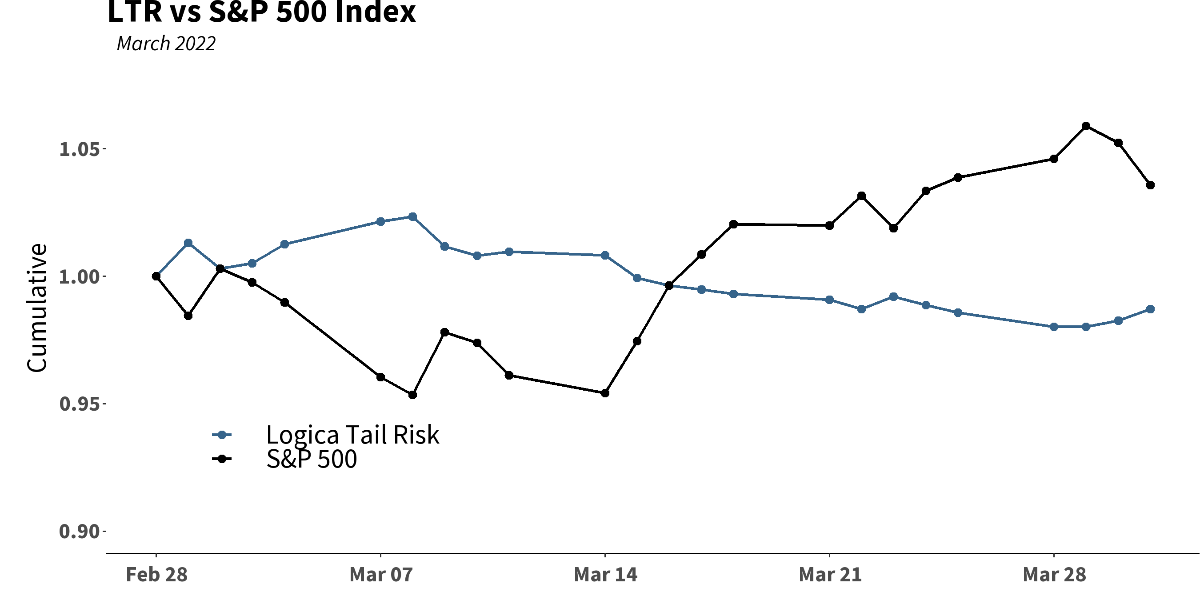

As we can see below, our strategies held up well and offered a positive return through the low point of the S&P 500 in March. As mentioned above, the whipsaws can be challenging. Preparing for more downside in the underlying while simultaneously avoiding getting absolutely crushed if the underlying violently reverses (as it did) is a very narrow needle to thread. That said, we were able to monetize some of our gains through early March and prepare for this potential reversal over the latter half of the month, and of course still honor the overall objectives of each strategy.

Months like March can be very challenging for two distinct, and almost opposite, reasons. The first reason is the destruction of implied volatility. As our strategies are entirely long volatility (no short vol legs or spread trades), we are incredibly proud to have held up as well as we did given that VIX had one of its worst calendar month returns in the past 30+ years:

“You’re on mute”

Quote of 2020

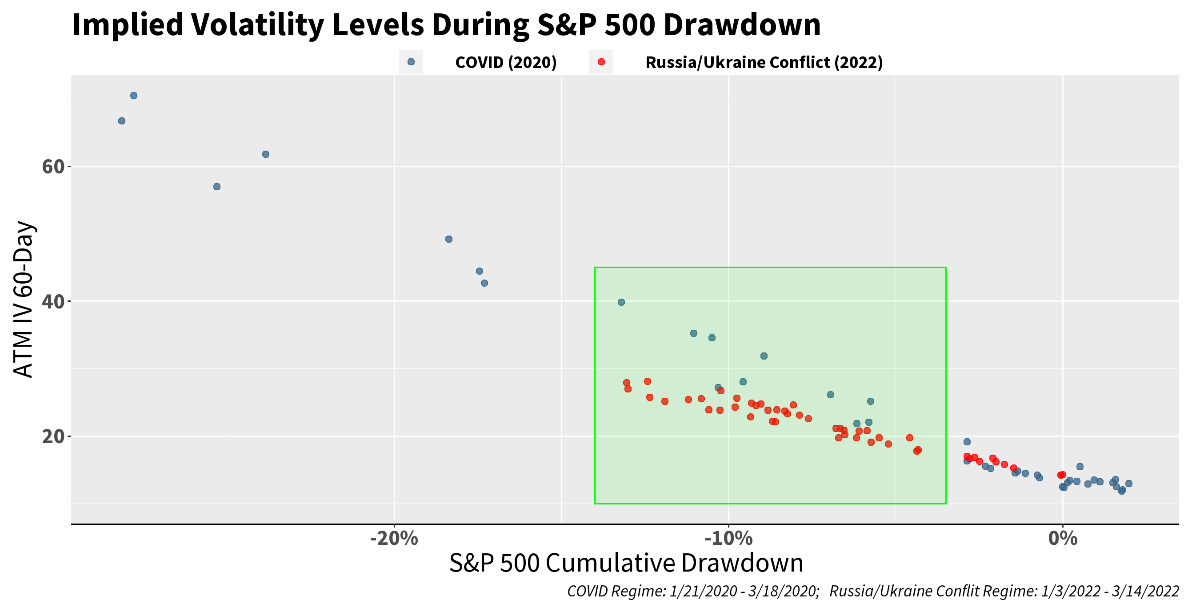

The second substantive challenge, which has actually been present throughout the entirety of Q1, has been the overall muted response of implied volatility with respect to the drawdown of the underlying (here, the S&P 500 Index). As those familiar with the essence of our strategy may know, as implied volatility rises, our objective is to monetize some of the volatility/vega we hold (scaling out of some portion of our long inventory), which is made much clearer when our signals tell us that implied volatility is also “out of whack,” or e.g., has perhaps risen more than we might expect given the move in the underlying. However, Q1 2022 demonstrated the opposite: the moves in implied volatility have been far less than one might expect given the headline/geopolitical risk and associated S&P 500 movement, and thus, have offered fewer opportunities for monetization, fewer chances for scalping, and consequently, fewer opportunities to re-load at better pricing.

To get a clearer picture of this dynamic, we can look at at-the-money implied volatility (ATM IV), and how it has behaved during this recent geopolitical turmoil versus its behavior during the COVID drawdown of Q1 2020. A picture says a thousand words, and clearly, we can see how “orderly” this drawdown has been compared to the massive uncertainty of 2020. As we always disclaim, we certainly cannot expect to always see the magnitude of implied volatility moves that we saw during 2020: we can’t expect that behavior to be the “norm” of stress events (there is no “standard anomaly!”), but it is a very useful comparison to view a truly convex event alongside what has, so far, been a mostly linear event with respect to implied volatility’s relation to the S&P 500 drawdown:

Even “linear” events typically provide a mild tailwind to long volatility strategies, of course, which can be seen in the Q1 performance of both our strategies as compared to the S&P 500. But none of these payoffs are as convex as we would hope for (and, of course, as our clients would hope for), and this is quite literally because the vol response was linear rather than convex. If our leader is not convex, we cannot follow it up as such!

“History is the version of the past events that people have decided to agree upon.” – Napolean Bonaparte

The question is why this might be so. Why would volatility be so responsive and “spiky” at certain times, while so unresponsive, and almost disengaged, during other times? While we can hypothesize about the greater uncertainty of a global pandemic attacking humanity at its core versus a local war on the other side of the globe that may be felt by the US in repercussions like rising energy prices, we are not convinced that THIS effect is the real difference, or, at least, the only difference. As per the personality of Logica, our method is to ask big questions, and then start digging into the annals of market history and behavior to try and resolve those questions. To that end, we came to an interesting conclusion.Empirically and experientially, there often appears to be a decay effect associated with cumulative crisis events, and volatility’s reaction. That is, the longer it has been since a previous crisis/stress, the more reactive volatility is (or the greater the magnitude of the spike), while the more recent a prior event has been (e.g. after a spike), the more muted the next reaction. Quite simply, it’s as if volatility “remembers” or more precisely gets used to bad news. Interestingly, this view in the data very much aligns with human behavior. When we are going through a tragedy, and something else bad happens, we take it in stride more easily than had we not already been in, or recently had, a different tragedy. In a word, we desensitize. And so does implied volatility (which, of course, is merely a result of human supply/demand acting on this desensitization).

Another way to think about this is the market’s recent experience of recovery. As the drawdown in Feb/Mar 2020 saw such a violent recovery back to new highs, and a raging bull market thereafter, the increased desensitization includes not only the recent tragedy, but also, the recent result “that all turned out fine.” In this sense, we get used to crisis alongside the market’s resilience. And consequently, implied volatility is not as jumpy. Relatedly, this behavioral dynamic also ties to the cognitive bias (or blind spot) known as Recency Bias, wherein we give greater importance to recent events over historical ones – in a sense, a memory bias. It therefore can be said that Implied Volatility’s reactivity is prone to Recency Bias in the sense that, given a recent crisis and recovery, the market is more likely to believe the same thing will happen again, and thus a muted reaction from the outset.

So what does this all mean? It’s certainly interesting to think about, but more profoundly, it’s interesting for us to understand this dynamic so that we can continue to develop more refined methods of trading and capturing the associated behavioral characteristics. As volatility traders, it is our goal to understand every facet, and develop mechanisms to manage around what we learn.

Logica Strategy Details

If you would like to learn more about our strategies, please reach out to:

[email protected]

424-652-9500