Lancaster Colony (LANC) has a dividend track record that few companies can rival. The company has increased its cash dividend for 55 consecutive years after the February increase to 60 cents per share quarterly. Continuous quarterly dividends have been paid since 1963 and that makes LANC one of just 14 companies in the entire market with a dividend increase streak of that length. That puts the company among the elite Dividend Kings, a small group of stocks that have increased their payouts for at least 50 consecutive years. You can see the full list of all 25 Dividend Kings here.

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

Click here to download my Dividend Kings Excel Spreadsheet now. Keep reading this article to learn more.

Click here to access our Members Area where you can easily download all our Excel databases in one place.

Dividend Kings are the best of the best when it comes to rewarding shareholders with cash and this article will discuss LANC’s dividend and valuation outlook.

Business Overview

LANC began its operations back in 1961 after several small glass and related houseware manufacturing companies combined together. The new company almost immediately began rewarding its shareholders with quarterly cash dividends and eventually went public in 1969, the same year it began operations in the foodservice business with the Marzetti brand acquisition.

The company manufactures and distributes a fairly narrow product assortment split into two major categories: frozen and non-frozen. It makes salad dressings and various dips under the Marzetti brand, frozen breads under the Sister Schubert’s and New York brands, as well as caviar, noodles, croutons, flatbreads and other bread products under a variety of smaller brands. The Marzetti and New York brands are the cash cows for LANC, offering its core products of dips and dressings as well as croutons and frozen breads, respectively. LANC sells what amounts to accessories for meals and does it very well.

Source: Company website

LANC also has partnerships with major consumer brands like Olive Garden, Jack Daniel’s, Buffalo Wild Wings (BWLD) and Weight Watchers (WTW), licensing the respective trademarks to produce products for grocery store shelves. A portion of the proceeds of these products goes to the license owners but these agreements are a way for LANC to diversify away from its own core brands.

LANC’s market cap is just over $3B and the company is expected to produce about $1.2B in revenue this fiscal year. Over 95% of LANC’s sales are made in the US so currency risk is not a factor. It sells its products through the Retail and Foodservice divisions, offering its frozen and non-frozen products through those channels.

Two-thirds of LANC’s total sales are non-frozen products like dressings, dips, flat breads and croutons. The remaining third is frozen products like garlic bread and yeast rolls. Lancaster has leadership positions in its core brands including New York, Sister Schubert’s, Flat Out (flat breads) and Marzetti while it is more focused on growth with its smaller brands.

One major risk to LANC’s revenue streams, however, is its reliance upon two major distributors. Wal-Mart (WMT) represented 17% of total sales for LANC in 2017 and also holds a significant accounts receivables balance. WMT could decide to offer less shelf space to LANC’s brands, offer additional competitive products or decide to stop carrying the brands altogether. LANC’s reliance upon WMT is high on its own but when you combine it with its similar reliance upon McLane, it is a bit more worrisome.

McLane is a foodservice distributor, a category where LANC competes heavily with its Marzetti brand products for quick service and casual dining customers. McLane represented 16% of total sales in 2017 and while the customer list is long and diverse for McLane, it could move to another set of brands for service to its customers. Both of these customers – Wal-Mart and McLane – offer significant concentration risk to LANC with about one-third of the company’s total sales combined.

Should either of these companies alter their current arrangements with LANC, the results would be significantly negative. Customer concentration risk is fairly common among smaller manufacturing firms and LANC certainly fits the bill, which is something investors should monitor closely.

Growth Prospects

LANC’s recent Q2 report showed that it is experiencing some growth troubles as a variety of factors have played into its relatively weak performance thus far this year. Total sales fell 2.2% in the second quarter as both Retail and Foodservice saw lower revenue. Retail’s revenue was down 1.9% as strength in its Olive Garden dressings line, a full quarter of Angelic Bakehouse – a recent acquisition – and lower coupon costs were more than offset by constrained sales of New York frozen garlic breads.

The Foodservice business fared slightly worse with a 2.5% decline in total sales as ongoing traffic challenges at restaurants continue to weigh on LANC’s sales to its foodservice customers. LANC has implemented some pricing increases to combat some of this slowdown but given that almost half of its sales go to restaurant customers, LANC is beholden to traffic trends at US restaurants and right now, that’s not working out in its favor. In addition, both segments were negatively impacted by insufficient freight capacity in the second quarter, causing not only a decline in sales but also an increase in freight costs, which impacted margins.

LANC has implemented a series of cost saving measures recently – including supply chain optimization and office location consolidation – in order to try and combat rising freight costs as well as commodity inflation, two factors which drove gross profit lower by more than 10% in Q2.

Keep in mind this decline was well in excess of the 2.2% decline in sales LANC saw during the quarter, implying that profitability has been significantly impacted by freight and commodity costs. Last year’s Q2 saw record-high gross profit so the bar was high for LANC, but the results from Q2 are troubling in terms of growth prospects for the company as it faces some fairly harsh realities of selling to restaurants.

Management isn’t sitting idly by, however, as there are a number of things LANC is doing to try and get growth back on track. I mentioned the Angelic Bakehouse acquisition and this is something LANC does fairly frequently. This company has been built over the last 50+ years on acquisitions of consumer brands that it takes and grows over time. That is a stated corporate goal and isn’t going to change so be on the lookout for targeted acquisitions moving forward as a primary source of growth.

The partnerships I mentioned with major consumer brands continue to grow as well as Buffalo Wild Wings sauces are a very recent addition as well as extensions of the company’s partnership with Olive Garden and its dressings. LANC continues to find ways to add to its stable of products via acquisitions, partnership extensions and some R&D on its own brands.

That said, LANC is not a growth stock by any means. Fiscal 2017 was a strong year for the Retail business as it saw revenue rise 3.6% but the Foodservice business saw revenue decline 2% for the full year. This year, the Retail business is suffering as well for the reasons outlined above in addition to another weak year for Foodservice. LANC’s core headwinds to growth are alive and well this year and as such, total sales are expected to be flat in fiscal 2018. LANC’s biggest risk to growth going forward is its exposure to restaurants.

Competitive Advantages & Recession Performance

LANC’s competitive advantage’s are mainly in its distributor partnerships with major sellers like WMT and McLane as well as its leadership positions in certain categories like croutons, frozen bread products and dressings. LANC has built a niche in these categories over the years and while its heavy reliance upon two distributors for one-third of its revenue is a potential risk, it also means the company’s competitors don’t necessarily have the same access to those large customers.

LANC is in a strong position within its core categories but that doesn’t make it immune from recessions. Earnings-per-share during and after the Great Recession are below:

- 2007 earnings-per-share of $1.45 (decrease of 42% from 2006)

- 2008 earnings-per-share of $1.28 (decrease of 12%)

- 2009 earnings-per-share of $3.17 (increase of 147%)

- 2010 earnings-per-share of $4.07 (increase of 28%)

Revenue actually fared pretty well during this period as LANC didn’t see any meaningful declines during the period and in fact, revenue was actually higher in 2008 than 2007. However, pricing and cost of goods suffered and as a result, margins declined significantly. This produced the earnings declines LANC experienced in 2007 and 2008 but to its credit, the rebound was swift and strong in 2009 and 2010.

Still, LANC is far from recession-proof because it sells products to foodservice customers – which suffer mightily during recessions and would thus order less from LANC – and consumers that may become cash-strapped during recessions and eschew the food accessories that LANC offers. LANC could easily be characterized as a cyclical stock in a sense due to these factors that are so recession-sensitive.

Valuation & Expected Returns

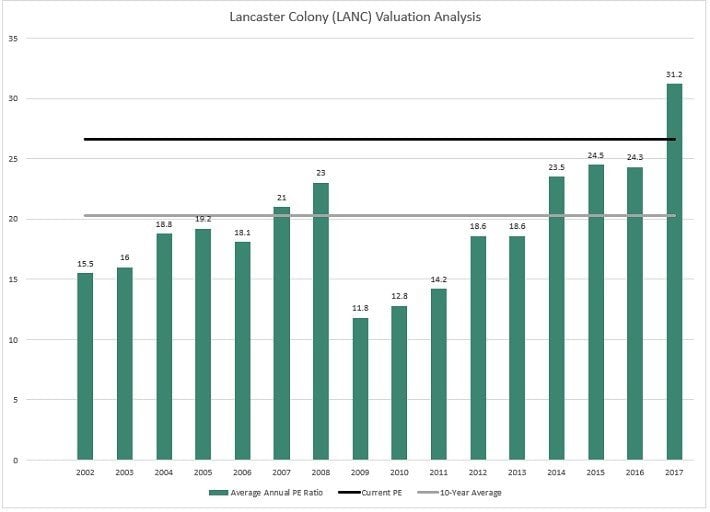

According to ValueLine, LANC is expected to earn $4.50 this year, which puts its price-to-earnings ratio at 26.6. This is a very high valuation for a stock like this.

Source: ValueLine

LANC has a strong track record over the years of producing slow and steady growth but keep in mind that it is highly-sensitive to economic downturns and if we just look at growth since 2010, it isn’t particularly impressive. If LANC earns $4.60 this year that would represent a ~13% increase from 2010’s EPS, putting annual growth in the low single digits. Analyst expectations are for just 3% EPS growth over the medium term going forward, so to be clear, LANC is not a growth stock and likely never will be.

That makes the PE a bit difficult to reconcile given that LANC’s price-to-earnings-growth ratio is off the charts and because investors typically don’t pay 26 times earnings for companies with very little growth. As a result, LANC certainly does not look like it would qualify as being undervalued in its present state.

The dividend is a potentially big draw for investors given that LANC has a world-class track record when it comes to rewarding shareholders.

While growth rates have differed, over this time frame LANC has produced an average dividend increase of more than 7% annually. This is certainly a respectable rate of dividend growth and given that the current payout is still just over half of total earnings, the dividend is well covered. That means that when the next recession does strike, earnings may suffer but the dividend shouldn’t.

The current yield isn’t particularly enticing, however, at just 2%. LANC’s stock price is very high relative to its earnings, as discussed earlier, so that means that even if LANC were to pay out more of its earnings in dividends, the yield still wouldn’t be among the top income stocks out there. Unfortunately, while LANC has a terrific history of increasing its dividend, the current yield isn’t enough to make the stock attractive against its very high valuation.

As a side note, LANC paid special dividends of $2, $5 and $5 in 2005, 2012 and 2015, respectively, offering shareholders a boost to their total returns. Obviously we cannot predict when or if these may occur again, but they were significant distributions of cash so they are worth noting.

The total return picture is a bit murky given that LANC’s dividend is worth just 2% annually and that the valuation is so high. Should a recession strike, LANC’s earnings multiple would undoubtedly suffer as net income would be at risk, as we saw earlier. Even without that, however, LANC’s PE is near its historical highs as the stock has continued to rally despite little in the way of earnings growth.

Given that revenue and earnings growth is under pressure, total returns could be in the low-single digits, once the potential impact of price-to-earnings ratio compression is accounted for.

Thus, total returns don’t look particularly attractive here either as the dividend isn’t high enough to cushion against downside risk. Given that the PE is so high and the growth outlook is so uncertain, total returns from here could very well be negative or at least very low in the coming years depending upon how the earnings multiple changes over time.

Final Thoughts

LANC is certainly not a high-yield income stock but it does have an impressive track record of dividend increases. Unfortunately the current yield isn’t high enough to warrant a position simply for the dividend and given the valuation, the risk of negative total returns is too high in the coming years.

LANC is highly susceptible to recessions so the risk of a major selloff in the stock on economic weakness is a sizable overhang, particularly at the current valuation. With all of this in mind, LANC doesn’t look like an enticing long position here despite its Dividend King status.

Thanks for reading this article. Please send any feedback, corrections, or questions to [email protected].

Article by Josh Arnold, Sure Dividend

ValueWalk readers can click here to instantly access an exclusive $100 discount on Sure Dividend’s premium online course Invest Like The Best, which contains a case-study-based investigation of how 6 of the world’s best investors beat the market over time.

{kind=link}